Appraisal Manual for Centrally Valued Natural Resource Property

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Page 1 of 2 Reporting Issuer List - Cover Page

Alberta Securities Commission Page 1 of 2 Reporting Issuer List - Cover Page Reporting Issuers Default When a reporting issuer is noted in default, standardized codes (a number and, if applicable a letter, described in the legend below) will be appear in the column 'Nature of Default'. Every effort is made to ensure the accuracy of this list. A reporting issuer that does not appear on this list or that has inappropriately been noted in default should contact the Alberta Securities Commission (ASC) promptly. A reporting issuer’s management or insiders may be subject to a Management Cease Trade Order, but that order will NOT be shown on the list. Legend 1. The reporting issuer has failed to file the following continuous disclosure document prescribed by Alberta securities laws: (a) annual financial statements; (b) an interim financial report; (c) an annual or interim management's discussion and analysis (MD&A) or an annual or interim management report of fund performance (MRFP); (d) an annual information form; (AIF); (e) a certification of annual or interim filings under National Instrument 52-109 Certification of Disclosure in Issuers' Annual and Interim Filings (NI 52-109); (f) proxy materials or a required information circular; (g) an issuer profile supplement on the System for Electronic Disclosure By Insiders (SEDI); (h) a material change report; (i) a written update as required after filing a confidential report of a material change; (j) a business acquisition report; (k) the annual oil and gas disclosure prescribed by National Instrument -

Ecology: Biodiversity and Natural Resources Part 1

CK-12 FOUNDATION Ecology: Biodiversity and Natural Resources Part 1 Akre CK-12 Foundation is a non-profit organization with a mission to reduce the cost of textbook materials for the K-12 market both in the U.S. and worldwide. Using an open-content, web-based collaborative model termed the “FlexBook,” CK-12 intends to pioneer the generation and distribution of high-quality educational content that will serve both as core text as well as provide an adaptive environment for learning. Copyright © 2010 CK-12 Foundation, www.ck12.org Except as otherwise noted, all CK-12 Content (including CK-12 Curriculum Material) is made available to Users in accordance with the Creative Commons Attribution/Non-Commercial/Share Alike 3.0 Un- ported (CC-by-NC-SA) License (http://creativecommons.org/licenses/by-nc-sa/3.0/), as amended and updated by Creative Commons from time to time (the “CC License”), which is incorporated herein by this reference. Specific details can be found at http://about.ck12.org/terms. Printed: October 11, 2010 Author Barbara Akre Contributor Jean Battinieri i www.ck12.org Contents 1 Ecology: Biodiversity and Natural Resources Part 1 1 1.1 Lesson 18.1: The Biodiversity Crisis ............................... 1 1.2 Lesson 18.2: Natural Resources .................................. 32 2 Ecology: Biodiversity and Natural Resources Part I 49 2.1 Chapter 18: Ecology and Human Actions ............................ 49 2.2 Lesson 18.1: The Biodiversity Crisis ............................... 49 2.3 Lesson 18.2: Natural Resources .................................. 53 www.ck12.org ii Chapter 1 Ecology: Biodiversity and Natural Resources Part 1 1.1 Lesson 18.1: The Biodiversity Crisis Lesson Objectives • Compare humans to other species in terms of resource needs and use, and ecosystem service benefits and effects. -

DFA Canada Canadian Vector Equity Fund - Class a As of July 31, 2021 (Updated Monthly) Source: RBC Holdings Are Subject to Change

DFA Canada Canadian Vector Equity Fund - Class A As of July 31, 2021 (Updated Monthly) Source: RBC Holdings are subject to change. The information below represents the portfolio's holdings (excluding cash and cash equivalents) as of the date indicated, and may not be representative of the current or future investments of the portfolio. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. By viewing this listing of portfolio holdings, you are agreeing to not redistribute the information and to not misuse this information to the detriment of portfolio shareholders. Misuse of this information includes, but is not limited to, (i) purchasing or selling any securities listed in the portfolio holdings solely in reliance upon this information; (ii) trading against any of the portfolios or (iii) knowingly engaging in any trading practices that are damaging to Dimensional or one of the portfolios. Investors should consider the portfolio's investment objectives, risks, and charges and expenses, which are contained in the Prospectus. Investors should read it carefully before investing. Your use of this website signifies that you agree to follow and be bound by the terms and conditions of -

Preparing for Growth: Capitalizing on a Period of Progress and Stability

Preparing for growth: Capitalizing on a period of progress and stability www.pwc.com/ca/canadianmine A year of stability Contents 2 A year of stability 3 Highlights and analysis 7 Agnico Eagle: Perfecting a successful 60 year-old strategy 9 Osisko Gold Royalties: Disrupting the cycle An interview with John Matheson, Partner, PwC Canada 11 Savvy investments in stable times Call it breathing room. Over the last year, into Eastern and Central Europe with its Canada’s major mining companies have Belt and Road Initiative (formerly One Belt entered a period of relative stability after and One Road) is increasing demand for weathering a frenzied period of boom, industrial products. bust and recovery. Globally, the geopolitical situation will About this report The sector has been paying down debt, likely remain volatile through 2018 and Preparing for growth is one of improving balance sheets and judiciously beyond. While bullion largely shrugged four publications in our annual investing in capital projects, on trend with off 2017’s world events, international Canadian mine series looking at the wider global mining industry in 2017. uncertainties could yet become an the realities and priorities of public Maintaining flexibility and increasing upward force on gold prices. The success mining companies headquartered efficiency are key goals for many executive of stock markets around the globe last in Canada. It offers a summary of financial analysis of the top 25 teams as they try to position themselves to year dampened general investor interest listings by market capitalization on capitalize on the next stages of the cycle. in gold equities, with the precious metal the TSX and complements our Junior Some companies have sought to enhance traditionally serving as a hedge against mine 2017 report, which analyzes the operations through acquisitions, but on market downturns, said David Smith, top 100 listings on the TSX Venture the whole, 2017 saw few eye-popping Senior Vice President of Finance and Chief Exchange (TSX-V). -

Natural Resources, Spring 1999

NATURAL RESOURCES MANAGEMENT AND PROTECTION TASK FORCE REPORT PRESIDENT’S COUNCIL ON SUSTAINABLE DEVELOPMENT The views expressed in this report are those of the Task Force members and were not the subject of endorsement by the full Council. Many of the federal officials who serve on the Council also serve on the Council’s Task Forces and participated actively in developing the Task Force’s recommendations, but those recommendations do not necessarily reflect Administration policy. PRESIDENT’S COUNCIL ON SUSTAINABLE DEVELOPMENT TASK-FORCE-REPORT-ON-NATURAL RESOURCES To obtain copies of this Report, please contact: President’s Council on Sustainable Development 730 Jackson Place, NW Washington, D.C. 20503 1-800-363-3732 (202) 408-5296 Website: http://www.whitehouse.gov/PCSD TASK FORCE MEMBERSHIP CO-CHAIRS Richard Barth, Chairman, President, and CEO, Ciba-Geigy Corporation James R. Lyons, Undersecretary for Natural Resources and the Environment, U.S. Department of Agriculture Theodore Strong, Executive Director, Columbia River Inter-Tribal Fish Commission MEMBERS Bruce Babbitt, Secretary, U.S. Department of the Interior James Baker, Undersecretary for Oceans and Atmosphere, National Oceanic and Atmospheric Administration, U.S. Department of Commerce Carol Browner, Administrator, U.S. Environmental Protection Agency A.D. Correll, Chairman and CEO, Georgia-Pacific Corporation Fred D. Krupp, Executive Director, Environmental Defense Fund Michele Perrault, International Vice President, Sierra Club John C. Sawhill, President and CEO, The Nature Conservancy PRESIDENT’S COUNCIL ON SUSTAINABLE DEVELOPMENT TASK-FORCE-REPORT-ON-NATURAL RESOURCES TABLE OF CONTENTS PREFACE. i EXECUTIVE SUMMARY. ii INTRODUCTION. 1 CHAPTER 1:TASK FORCE APPROACH. 5 The Role of the Watershed. -

IEA: the Role of Critical Minerals in Clean Energy Transitions

The Role of Critical Minerals in Clean Energy Transitions World Energy Outlook Special Report INTERNATIONAL ENERGY AGENCY The IEA examines the full spectrum of IEA member countries: Spain energy issues including oil, gas and Australia Sweden coal supply and demand, renewable Austria Switzerland energy technologies, electricity Belgium Turkey markets, energy efficiency, access to Canada United Kingdom energy, demand side management Czech Republic United States and much more. Through its work, the Denmark IEA advocates policies that will Estonia IEA association countries: enhance the reliability, affordability Finland Brazil and sustainability of energy in its 30 France China member countries, 8 association Germany India countries and beyond. Greece Indonesia Hungary Morocco Please note that this publication is Ireland Singapore subject to specific restrictions that Italy South Africa limit its use and distribution. The Japan Thailand terms and conditions are available Korea online at www.iea.org/t&c/ Luxembourg Mexico This publication and any map included herein are Netherlands without prejudice to the status of or sovereignty New Zealand over any territory, to the delimitation of international frontiers and boundaries and to the Norway name of any territory, city or area. Poland Portugal Slovak Republic Source: IEA. All rights reserved. International Energy Agency Website: www.iea.org The Role of Critical Minerals in Clean Energy Transitions Foreword Foreword Ever since the International Energy Agency (IEA) was founded in world to anticipate and navigate possible disruptions and avoid 1974 in the wake of severe disruptions to global oil markets that damaging outcomes for our economies and our planet. shook the world economy, its core mission has been to foster secure This special report is the most comprehensive global study of this and affordable energy supplies. -

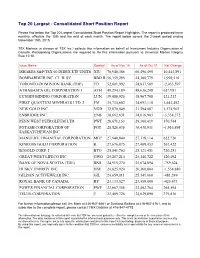

Top 20 Largest - Consolidated Short Position Report

Top 20 Largest - Consolidated Short Position Report Please find below the Top 20 Largest Consolidated Short Position Report Highlights. The report is produced twice monthly, effective the 15th and the end of each month. The report below covers the 2-week period ending November 15th, 2015. TSX Markets (a division of TSX Inc.) collects this information on behalf of Investment Industry Organization of Canada. Participating Organizations are required to file this information pursuant to Universal Market Integrity Rule 10.10. Issue Name Symbol As of Nov 15 As of Oct 31 Net Change ISHARES S&P/TSX 60 INDEX ETF UNITS XIU 70,940,386 60,496,495 10,443,891 BOMBARDIER INC. CL 'B' SV BBD.B 56,359,295 54,360,779 1,998,516 TORONTO-DOMINION BANK (THE) TD 52,801,992 54,837,589 -2,035,597 ATHABASCA OIL CORPORATION J ATH 49,294,189 48,636,208 657,981 LUNDIN MINING CORPORATION LUN 39,088,920 38,967,708 121,212 FIRST QUANTUM MINERALS LTD. J FM 35,734,602 34,091,110 1,643,492 NEW GOLD INC. NGD 32,870,049 31,294,087 1,575,962 ENBRIDGE INC. ENB 30,662,631 34,016,903 -3,354,272 PENN WEST PETROLEUM LTD. PWT 28,671,163 28,300,419 370,744 POTASH CORPORATION OF POT 28,520,036 30,436,931 -1,916,895 SASKATCHEWAN INC. MANULIFE FINANCIAL CORPORATION MFC 27,940,840 27,318,114 622,726 KINROSS GOLD CORPORATION K 27,676,875 27,409,453 267,422 B2GOLD CORP. -

Water Demand Management, Natural Resource Reconstruction and Traditional Value Systems: a Case Study from Yemen

WATER DEMAND MANAGEMENT, NATURAL RESOURCE RECONSTRUCTION AND TRADITIONAL VALUE SYSTEMS: A CASE STUDY FROM YEMEN Occasional Paper No. 14 Water Issues Study Group School of Oriental and African Studies (SOAS) University of London By G. LichtenthŠler & A.R. Turton gl3&soas.ac.uk & [email protected] INTRODUCTION: Previous research has shown that under conditions of extreme water scarcity, such as in the Middle East, natural resource reconstruction can take place (Allen & Karshenas, 1996). This may not always be the case however, as certain societies seem better able to cope with this process than others. This phenomenon has been linked to the adaptive capacity of a society (Turton, 1999) where it has been shown that all social entities are not equally endowed. A shortage of adaptive capacity has been redefined as a second- order scarcity (Ohlsson, 1998; 1999). What is currently being regarded by most researchers as a manifestation of resource scarcity is in fact probably the result of a second-order scarcity of social resources, which impacts in turn on the way that social entities deal with the first order scarcity of a natural resource such as water. In terms of this thinking, a shift in emphasis to second-order scarcities would be appropriate. Furthermore, it has been demonstrated that in a society where resource capture is being actively pursued, natural resource reconstruction is unlikely to occur because it reduces the overall legitimacy of the political system (Turton, 1999). A study of these aspects in Yemen (LichtenthŠler, 1999) is therefore considered to be extremely fruitful because of four fundamental reasons. -

Optimize and Protect Your Natural Resources

Get involved with EQIP The EQIP application process is continuous throughout the year. Information and applications Optimize can be obtained at any local NRCS Field Office. To find out if EQIP is a perfect fit for your operation, contact your local NRCS office at a and protect USDA Service Center in your area or click on to www.wa.nrcs.usda.gov. your natural Application Process The EQIP application process consists of the resources... EQIP can help producers improve irrigation water following five steps: efficiency. water that is lost to the field. 1. A landowner submits an application to In order to improve the application of water a local USDA Service Center, NRCS and make it more uniform, sprinkler irrigation office, or conservation district office. systems are cost-shared and installed. These 2. NRCS ranks each application using the systems apply water to the plant when needed locally developed natural resources at a rate the soil can manage. There is no deep ranking process. percolation or runoff with the sprinkler irrigation 3. When funds are allocated, NRCS system. What this means is a better use of the commits funds to high ranking resources; water, power, fertilizer, and chemicals applications. which equals better quality crops. 4. NRCS works with the applicant to develop an EQIP conservation plan and Irrigation Water Management contract containing practices which will With the installation of new irrigation solve identified resource problems. systems, landowners need to learn how and when 5. Following contract signature by to apply water. For most of the new systems it NRCS and the selected entity, funds is possible to apply water almost anytime it is are obligated to the project and the needed. -

Natural Resource Economics - Jason F

ECONOMICS INTERACTIONS WITH OTHER DISCIPLINES – Vol. II - Natural Resource Economics - Jason F. Shogren NATURAL RESOURCE ECONOMICS Jason F. Shogren University of Wyoming, Laramie, USA Keywords: natural resource, natural resource economics, non-renewable resource, renewable resource, biodiversity, non-market valuation Contents 1. Introduction 2. Non-renewable Resources 2.1 Optimal Depletion 2.2 Resource Scarcity 2.3 Energy 3. Renewable Resources 3.1 Fisheries (or Groundwater) 3.2 Forests 3.3 Commons and Property Rights 3.4 Regulation and Incentives 4. Protecting Biodiversity 5. Climate Protection 6. Non-market Valuation 7. Concluding Comments Acknowledgements Glossary Bibliography Biographical Sketch Summary Natural resource economics examines how society can more efficiently use its scarce natural resources, both non-renewable resources, such as minerals and fossil fuels, and renewable resources, such as fisheries and forests. Theory and empirical research explores alternative models on how people and societies choose to use and manage their limited resources. For non-renewable resources, natural resource economics suggests that theUNESCO efficient path to extract such resources – EOLSS over time is to balance the market price with both the marginal extraction costs and the opportunity cost, or shadow price of extracting the resource sooner rather than later. This shadow price is also called the user cost, resourceSAMPLE royalty, or scarcity rent. User CHAPTERS costs capture the idea that there is an additional cost for extracting a resource today since it cannot be extracted tomorrow. Theory also suggests the scarcity rent should grow at a rate equal to the rate of interest. This is called Hotelling’s rule, which says that a unit of resource extracted in any period should yield the same rent, in present value terms. -

Arlington's Natural Resources Management Plan

ARLINGTON COUNTY, VIRGINIA Natural Resources Management Plan AN ELEMENT OF ARLINGTON COUNTY’S COMPREHENSIVE PLAN ADOPTED November 13, 2010 State Champion Post Oak Natural Resources Management Plan November 2010 Arlington County Board Jay Fisette, Chairman, Christopher Zimmerman, Vice-Chairman, and Members Barbara A. Favola, Mary Hughes Hynes and J. Walter Tejada Barbara M. Donnellan, County Manager Dinesh Tiwari, Director, Department of Parks, Recreation and Cultural Resources Caroline Temmermand, Division Chief, Parks and Natural Resources Division The Natural Resources Management Plan was prepared by Greg Zell, Natural Resource Specialist, Department of Parks, Recreation and Cultural Resources, Parks and Natural Resources Division, Conservation and Interpretation Section. The following individuals provided assistance in the development of the Natural Resources Management Plan: Jamie Bartalon, Landscape and Forestry Section Supervisor; Larry Finch, Chairman, Urban Forestry Commission; Mary Ann Lawler, Urban Forestry Commission; Steve Campbell, Urban Forestry Commission; Dean Amel, Environment and Energy Conservation Commission; Shannon Cunniff, Chairman, Environment and Energy Conservation Commission; Caroline Haynes, Park and Recreation Commission, and Jim Olivetti, Park and Recreation Commission. Front Cover Photo Credits: John White, Gary Fleming, Greg Zell, and the Arlington County Department of Community Planning, Housing & Development. Other report photos by Greg Zell, unless otherwise indicated. Map Credits: Arlington County Department -

Notice to Participating Organizations 2005-028

Notice to Participating Organizations --------------------------------------------------------------------------------------------------------------------- August 12, 2005 2005-028 Addition of Market On Close (MOC) Eligible Securities Toronto Stock Exchange will roll out MOC eligibility to the symbols of the S&P/TSX Composite Index in preparation for the quarter end index rebalancing on September 16, 2005. TSX will enable MOC eligibility in two phases: I. S&P/TSX Mid Cap Index will become MOC eligible effective September 6, 2005. II. S&P/TSX Small Cap Index will become MOC eligible effective September 12, 2005. A list of securities for each of these indices follows this notice. To ensure you are viewing the most current list of securities, please visit the Standard and Poor's website at www.standardandpoors.com prior to the above rollout dates. “S&P” is a trade-mark owned by The McGraw-Hill, Companies Inc. and “TSX” is a trade- mark owned by TSX Inc. MOC Eligible effective MOC Eligible effective September 6, 2005 September 12, 2005 S&P TSX Mid Cap S&P TSX Small Cap SYMBOL COMPANY SYMBOL COMPANY ABZ Aber Diamond Corporation AAC.NV.B Alliance Atlantis Communications Inc. ACM.NV.A Astral Media Inc. AAH Aastra Technologies Ltd. ACO.NV.X Atco Ltd. ACE.RV ACE Aviation Holdings Inc. AGE Agnico-Eagle Mines AEZ Aeterna Zentaris Inc. AGF.NV AGF Management Ltd. AGA Algoma Steel Inc. AIT Aliant Inc. ANP Angiotech Pharmaceuticals Inc. ATA ATS Automation Tooling Systems Inc. ATD.SV.B Alimentation Couche-Tard Inc. AXP Axcan Pharma Inc. AU.LV Agricore United BLD Ballard Power Systems Inc. AUR Aur Resources Inc.