Q4 Performance Review

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Methanex Corporation Annual Information Form

METHANEX CORPORATION ANNUAL INFORMATION FORM www.methanex.com March 16, 2010 TABLE OF CONTENTS Page REFERENCE INFORMATION ...................................................................................................................................................... 3 CAUTION REGARDING FORWARD-LOOKING STATEMENTS .......................................................................................... 4 THE COMPANY ............................................................................................................................................................................... 6 BUSINESS OF THE COMPANY .................................................................................................................................................... 7 What is Methanol? ................................................................................................................................................................. 7 Our Operations ...................................................................................................................................................................... 7 DEVELOPMENT OF THE BUSINESS AND CORPORATE STRATEGY ............................................................................... 7 Global Leadership.................................................................................................................................................................. 7 Low Cost .............................................................................................................................................................................. -

Page 1 of 2 Reporting Issuer List - Cover Page

Alberta Securities Commission Page 1 of 2 Reporting Issuer List - Cover Page Reporting Issuers Default When a reporting issuer is noted in default, standardized codes (a number and, if applicable a letter, described in the legend below) will be appear in the column 'Nature of Default'. Every effort is made to ensure the accuracy of this list. A reporting issuer that does not appear on this list or that has inappropriately been noted in default should contact the Alberta Securities Commission (ASC) promptly. A reporting issuer’s management or insiders may be subject to a Management Cease Trade Order, but that order will NOT be shown on the list. Legend 1. The reporting issuer has failed to file the following continuous disclosure document prescribed by Alberta securities laws: (a) annual financial statements; (b) an interim financial report; (c) an annual or interim management's discussion and analysis (MD&A) or an annual or interim management report of fund performance (MRFP); (d) an annual information form; (AIF); (e) a certification of annual or interim filings under National Instrument 52-109 Certification of Disclosure in Issuers' Annual and Interim Filings (NI 52-109); (f) proxy materials or a required information circular; (g) an issuer profile supplement on the System for Electronic Disclosure By Insiders (SEDI); (h) a material change report; (i) a written update as required after filing a confidential report of a material change; (j) a business acquisition report; (k) the annual oil and gas disclosure prescribed by National Instrument -

Finning International Inc. (TSX: FTT) Price Target CAD$ 30.00 Industrial Equipment Wholesale and Servicing Rating Buy Finning Is Winning Share Price (Sep

Analyst: Piero Ferrando, BCom. ‘22 [email protected] Equity Research Canada Finning International Inc. (TSX: FTT) Price Target CAD$ 30.00 Industrial Equipment Wholesale and Servicing Rating Buy Finning Is Winning Share Price (Sep. 06 Close) CAD$ 22.90 September 06, 2019 Total Return 31% Finning International, or the Company, is the world’s largest Key Statistics Caterpillar equipment dealer delivering service to customers for 52 Week H/L $33.02/$21.34 85 years, with operations in Canada, the UK & Ireland, and South Market Capitalization $3.74B America. The Company provides sales, rental, parts, and support Average Daily Trading Volume $526k services for Caterpillar equipment, engines, and complementary equipment across various industries including mining, forestry, Net Debt $1.70B agriculture, construction, power systems, and paving. Enterprise Value $5.90B Net Debt/EBITDA FY18 1.7x Thesis Finning is among the largest equipment wholesalers in the world, Diluted Shares Outstanding 163M with a globally renowned reputation and presence. The Free Float 99.8% Company’s recent South American ERP implementation struggles Dividend Yield FY18 2.7% have resulted in a 1 year 20%+ share price drop. However, it’s WestPeak’s Forecast proven strong cost control and industry leading ROIC have positioned it well to pursue growth initiatives, specifically in the 2018E 2019E 2020E growing industrial landscape of Western Canada. Revenue $6.99B $7.71B $8.56B EBITDA $610M $686M $771M Drivers Net Income $232M $227M $303M Upcoming multi billion-dollar opportunities relating to Liquified Natural Gas (LNG) in northern British Columbia present a critical EPS $1.38 $1.39 $1.85 opportunity for Finning. -

DFA Canada Canadian Vector Equity Fund - Class a As of July 31, 2021 (Updated Monthly) Source: RBC Holdings Are Subject to Change

DFA Canada Canadian Vector Equity Fund - Class A As of July 31, 2021 (Updated Monthly) Source: RBC Holdings are subject to change. The information below represents the portfolio's holdings (excluding cash and cash equivalents) as of the date indicated, and may not be representative of the current or future investments of the portfolio. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. By viewing this listing of portfolio holdings, you are agreeing to not redistribute the information and to not misuse this information to the detriment of portfolio shareholders. Misuse of this information includes, but is not limited to, (i) purchasing or selling any securities listed in the portfolio holdings solely in reliance upon this information; (ii) trading against any of the portfolios or (iii) knowingly engaging in any trading practices that are damaging to Dimensional or one of the portfolios. Investors should consider the portfolio's investment objectives, risks, and charges and expenses, which are contained in the Prospectus. Investors should read it carefully before investing. Your use of this website signifies that you agree to follow and be bound by the terms and conditions of -

Preparing for Growth: Capitalizing on a Period of Progress and Stability

Preparing for growth: Capitalizing on a period of progress and stability www.pwc.com/ca/canadianmine A year of stability Contents 2 A year of stability 3 Highlights and analysis 7 Agnico Eagle: Perfecting a successful 60 year-old strategy 9 Osisko Gold Royalties: Disrupting the cycle An interview with John Matheson, Partner, PwC Canada 11 Savvy investments in stable times Call it breathing room. Over the last year, into Eastern and Central Europe with its Canada’s major mining companies have Belt and Road Initiative (formerly One Belt entered a period of relative stability after and One Road) is increasing demand for weathering a frenzied period of boom, industrial products. bust and recovery. Globally, the geopolitical situation will About this report The sector has been paying down debt, likely remain volatile through 2018 and Preparing for growth is one of improving balance sheets and judiciously beyond. While bullion largely shrugged four publications in our annual investing in capital projects, on trend with off 2017’s world events, international Canadian mine series looking at the wider global mining industry in 2017. uncertainties could yet become an the realities and priorities of public Maintaining flexibility and increasing upward force on gold prices. The success mining companies headquartered efficiency are key goals for many executive of stock markets around the globe last in Canada. It offers a summary of financial analysis of the top 25 teams as they try to position themselves to year dampened general investor interest listings by market capitalization on capitalize on the next stages of the cycle. in gold equities, with the precious metal the TSX and complements our Junior Some companies have sought to enhance traditionally serving as a hedge against mine 2017 report, which analyzes the operations through acquisitions, but on market downturns, said David Smith, top 100 listings on the TSX Venture the whole, 2017 saw few eye-popping Senior Vice President of Finance and Chief Exchange (TSX-V). -

IEA: the Role of Critical Minerals in Clean Energy Transitions

The Role of Critical Minerals in Clean Energy Transitions World Energy Outlook Special Report INTERNATIONAL ENERGY AGENCY The IEA examines the full spectrum of IEA member countries: Spain energy issues including oil, gas and Australia Sweden coal supply and demand, renewable Austria Switzerland energy technologies, electricity Belgium Turkey markets, energy efficiency, access to Canada United Kingdom energy, demand side management Czech Republic United States and much more. Through its work, the Denmark IEA advocates policies that will Estonia IEA association countries: enhance the reliability, affordability Finland Brazil and sustainability of energy in its 30 France China member countries, 8 association Germany India countries and beyond. Greece Indonesia Hungary Morocco Please note that this publication is Ireland Singapore subject to specific restrictions that Italy South Africa limit its use and distribution. The Japan Thailand terms and conditions are available Korea online at www.iea.org/t&c/ Luxembourg Mexico This publication and any map included herein are Netherlands without prejudice to the status of or sovereignty New Zealand over any territory, to the delimitation of international frontiers and boundaries and to the Norway name of any territory, city or area. Poland Portugal Slovak Republic Source: IEA. All rights reserved. International Energy Agency Website: www.iea.org The Role of Critical Minerals in Clean Energy Transitions Foreword Foreword Ever since the International Energy Agency (IEA) was founded in world to anticipate and navigate possible disruptions and avoid 1974 in the wake of severe disruptions to global oil markets that damaging outcomes for our economies and our planet. shook the world economy, its core mission has been to foster secure This special report is the most comprehensive global study of this and affordable energy supplies. -

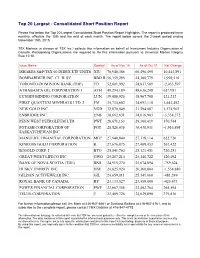

Top 20 Largest - Consolidated Short Position Report

Top 20 Largest - Consolidated Short Position Report Please find below the Top 20 Largest Consolidated Short Position Report Highlights. The report is produced twice monthly, effective the 15th and the end of each month. The report below covers the 2-week period ending November 15th, 2015. TSX Markets (a division of TSX Inc.) collects this information on behalf of Investment Industry Organization of Canada. Participating Organizations are required to file this information pursuant to Universal Market Integrity Rule 10.10. Issue Name Symbol As of Nov 15 As of Oct 31 Net Change ISHARES S&P/TSX 60 INDEX ETF UNITS XIU 70,940,386 60,496,495 10,443,891 BOMBARDIER INC. CL 'B' SV BBD.B 56,359,295 54,360,779 1,998,516 TORONTO-DOMINION BANK (THE) TD 52,801,992 54,837,589 -2,035,597 ATHABASCA OIL CORPORATION J ATH 49,294,189 48,636,208 657,981 LUNDIN MINING CORPORATION LUN 39,088,920 38,967,708 121,212 FIRST QUANTUM MINERALS LTD. J FM 35,734,602 34,091,110 1,643,492 NEW GOLD INC. NGD 32,870,049 31,294,087 1,575,962 ENBRIDGE INC. ENB 30,662,631 34,016,903 -3,354,272 PENN WEST PETROLEUM LTD. PWT 28,671,163 28,300,419 370,744 POTASH CORPORATION OF POT 28,520,036 30,436,931 -1,916,895 SASKATCHEWAN INC. MANULIFE FINANCIAL CORPORATION MFC 27,940,840 27,318,114 622,726 KINROSS GOLD CORPORATION K 27,676,875 27,409,453 267,422 B2GOLD CORP. -

AIF), the Terms “We”, “Our”, “Us” “Company” and “Finning” Mean Finning International Inc

FINNING INTERNATIONAL INC. ANNUAL INFORMATION FORM 2020 February 11, 2021 Finning International Inc. Suite 300 565 Great Northern Way Vancouver, British Columbia V5T 0H8 Finning International Inc. 2020 Annual Information Form TABLE OF CONTENTS FORWARD LOOKING INFORMATION .................................................................................................................. 4 1. CORPORATE STRUCTURE ................................................................................................................................... 6 1.1 NAME, ADDRESS AND INCORPORATION .................................................................................................................. 6 1.2 INTERCORPORATE RELATIONSHIPS ......................................................................................................................... 6 2. GENERAL DEVELOPMENT OF THE BUSINESS .............................................................................................. 7 2.1 OVERVIEW OF OPERATIONS .................................................................................................................................... 7 2.2 STRATEGIC PLAN .................................................................................................................................................... 7 2.3 THREE YEAR HISTORY ............................................................................................................................................ 8 2.4 GROWTH OPPORTUNITIES ...................................................................................................................................... -

Osler, 2020 Diversity Disclosure Practices Report

2020 Diversity Disclosure Practices Diversity and leadership at Canadian public companies By Andrew MacDougall, John Valley and Jennifer Jeffrey DIVERSITY DISCLOSURE PRACTICES Osler, Hoskin & Harcourt llp Table of contents Introduction 3 Developments in diversity: A wider focus 6 Our methodology 14 2019 full-year results 19 Mid-year results for 2020: Women on boards 23 Mid-year results for 2020: Women in executive officer positions 33 Diversity beyond gender: 2020 results for CBCA corporations 43 Who has achieved gender parity and how to increase diversity 49 Going above and beyond: Best company disclosure 64 The 2020 Diversity Disclosure Practices report provides general information only and does not constitute legal or other professional advice. Specific advice should be sought in connection with your circumstances. For more information, please contact Osler’s Corporate Governance group. 2 DIVERSITY DISCLOSURE PRACTICES Osler, Hoskin & Harcourt llp Introduction The diversity discussion blossomed this year, with continued, slow growth in the advancement of women accompanied by an expanded focus into other facets of diversity. This year new disclosure requirements under the Canada Business Corporations Act (CBCA) broadened the range of corporations required to provide disclosure regarding women in leadership positions and added new requirements for disclosure regarding visible minorities, Aboriginal peoples and persons with disabilities. Our sixth annual comprehensive report on diversity disclosure practices now covers disclosure by TSX-listed companies and CBCA corporations subject to disclosure requirements. We continue to provide detailed disclosure on TSX-listed companies to provide year-over-year comparisons. However, we now include new chapters summarizing the results of our review of CBCA company disclosure. -

Anti-Racism Ad Vancouver Sun FINAL

B.C. Business and Community Leaders Take a Stand Against Racism: We Say NO to Hate… It Must Stop Now As business and community leaders, British Columbians, and human beings we cannot sit idly by. What we condone, we accept, and we cannot accept the growing racism and hate directed at people because of their ethnicity, culture, or faiths. Racism must be called out and it must stop now! We are all deeply disturbed by the violent, overt and subtle displays of racism we are increasingly seeing and some that are being reported in the media. This is an affront to what it means to be a citizen in our province and country. As a place that welcomes the world, what we are witnessing is not who we are or aspire to be as Canadians. Admitting this growing problem will enable us to address it. Brazen assaults on people of Chinese descent. Racist slurs directed at Indigenous peoples, visible minorities and people based on their faith. Hate messages written on buildings. The recipients of these reprehensible behaviours are our family members, friends, neighbours, colleagues, fellow business and community leaders, philanthropists, and generations of people who have helped build our province. These incidents and actions come in sharp contrast to the many generous acts of kindness and tolerance exhibited by so many British Columbians every day and particularly the compassion that we have seen during this trying time. Our cultural mosaic is the envy of the world. It is comprised of generations who were born here and those who chose to come here to make a difference, to build a better life for their families and to contribute to a better province. -

Notice to Participating Organizations 2005-028

Notice to Participating Organizations --------------------------------------------------------------------------------------------------------------------- August 12, 2005 2005-028 Addition of Market On Close (MOC) Eligible Securities Toronto Stock Exchange will roll out MOC eligibility to the symbols of the S&P/TSX Composite Index in preparation for the quarter end index rebalancing on September 16, 2005. TSX will enable MOC eligibility in two phases: I. S&P/TSX Mid Cap Index will become MOC eligible effective September 6, 2005. II. S&P/TSX Small Cap Index will become MOC eligible effective September 12, 2005. A list of securities for each of these indices follows this notice. To ensure you are viewing the most current list of securities, please visit the Standard and Poor's website at www.standardandpoors.com prior to the above rollout dates. “S&P” is a trade-mark owned by The McGraw-Hill, Companies Inc. and “TSX” is a trade- mark owned by TSX Inc. MOC Eligible effective MOC Eligible effective September 6, 2005 September 12, 2005 S&P TSX Mid Cap S&P TSX Small Cap SYMBOL COMPANY SYMBOL COMPANY ABZ Aber Diamond Corporation AAC.NV.B Alliance Atlantis Communications Inc. ACM.NV.A Astral Media Inc. AAH Aastra Technologies Ltd. ACO.NV.X Atco Ltd. ACE.RV ACE Aviation Holdings Inc. AGE Agnico-Eagle Mines AEZ Aeterna Zentaris Inc. AGF.NV AGF Management Ltd. AGA Algoma Steel Inc. AIT Aliant Inc. ANP Angiotech Pharmaceuticals Inc. ATA ATS Automation Tooling Systems Inc. ATD.SV.B Alimentation Couche-Tard Inc. AXP Axcan Pharma Inc. AU.LV Agricore United BLD Ballard Power Systems Inc. AUR Aur Resources Inc. -

Appraisal Manual for Centrally Valued Natural Resource Property

Appraisal Manual For Centrally Valued Natural Resource Property Valuation Guidelines for Natural Resource Property Preface Preface The Department of Revenue’s Local Jurisdictions District is responsible for ensuring fair, accurate, and uniform property valuations as prescribed by Arizona statutes. The Local Jurisdictions District contains the Centrally Valued Property Unit which is responsible for producing this manual. The Centrally Valued Property Unit is responsible for determining the full cash value of certain utilities, railroads, airlines, private rail cars, mines, and other complex or geographically diverse property. With the exception of airline and private rail car valuations, the values are then transmitted for entry on the individual county tax rolls for levy and collection of property taxes. The manual is produced each year to serve as a guide in the appraisal of mines and other natural resource property. The techniques, procedures, and factors described in the manual are reviewed annually and revised in accordance with standard appraisal methods and techniques along with changes in statutes, rules, and regulations. Revisions are also made based on case law decisions. The procedures described in the manual are designed to assist the appraiser in the application of the income, cost, and market approach methods of valuation to these properties for the current tax year. This manual is intended for use in ad valorem appraisal of specific centrally valued property including producing mines, certain non-producing mines, qualifying environmental technology property and oil, gas, and geothermal interests in Arizona. The guidelines in this manual are used to establish full cash values for these properties as of January 1 of the valuation year.