Region Brochure Africa

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Can Corporate Power Positively Transform Angola and Equatorial Guinea?

Can Corporate Power Positively Transform Angola and Equatorial Guinea? Published in Wayne Visser ed. Corporate Citizenship in Africa. Greenleaf Publications, UK, 2006. Authors: Jose A. Puppim de Oliveira Brazilian School of Public and Business Administration – EBAPE Getulio Vargas Foundation – FGV Praia de Botafogo 190, room 507 CEP: 22253-900, Rio de Janeiro - RJ, BRAZIL Phone: (55-21) 2559-5737 Fax: (55-21) 2559-5710 e-mail: [email protected] & Saleem H. Ali Rubenstein School of Environment and Natural Resources University of Vermont 153 S. Prospect St., Burlington VT, 05452, USA Ph: 802-656-0173 Fx: 802-656-8015 Email: [email protected] 1 ABSTRACT While there is considerable literature on the adverse effects of oil development on developing economies through “Dutch Disease” or “Resource Curse” hypotheses, studies have neglected to pose the question in terms of positive causal factors that certain kinds of oil development might produce. We do not dispute the potential for negative effects of certain kinds of oil development but rather propose that some of the negative causality can be managed and transformed to lead to positive outcomes. Using a comparative study of oil company behavior in Angola and Equatorial Guinea, the research detects three main factors that have affected the behavior of oil companies since the Earth Summit in 1992. First, there is a growing movement of corporate social responsibility in businesses due to changes in leadership and corporate culture. Second, the ‘globalization’ of environmental movements has affected the behavior of companies through threats of litigation and stakeholder action. Third, governments in Africa have increasingly become stricter in regulating companies for environmental and social issues due to a transformation of domestic norms and international requirements. -

African Development Bank Project Summary Note

AFRICAN DEVELOPMENT BANK Reference No: P-AO-HAB-009 Task Managers: F. Marques, T. Babatunde PROJECT SUMMARY NOTE BANCO MILLENNIUM ATLANTICO, S.A. ANGOLA APRIL 2020 Project Summary Note (PSN) for Banco Millennium Atlântico, S.A. (“BMA”): On April 15, 2020, the Board of Directors of the African Development Bank approved a USD 40 million integrated financial package to Banco Millennium Atlântico, S.A. (“BMA”) Angola. The financing package consists of a USD 32 million line of credit from the African Development Bank and an additional USD 8 million in parallel financing from the Africa Growing Together Fund (AGTF), a co-financing fund sponsored by the People’s Bank of China and administered by the African Development Bank. This project will support BMA’s emerging multi-sectorial portfolio of indigenous Small and Medium-sized Enterprises (“SMEs”) operating predominantly in agriculture and agroindustry as well as domestic manufacturing. This loan BMA shall be on-lent to provide long-term financing required by BMA to support a diversified pipeline of transformative sub-projects which will create direct and indirect jobs and contribute critically needed foreign exchange savings through import substitution and establish a foundation for export to neighboring countries thereby promoting intra-regional trade. Overall, this project shall foster local production, stimulate job creation and ultimately contribute towards the country’s attainment of inclusive and sustainable growth as well as economic diversification. Under the current challenges of covid-19 outbreak and oil price collapse faced by Angola, this project will contribute to the private sector resilience. Banco Millennium Atlântico BMA is among the largest commercial banks in Angola and a leading financier of domestic firms especially SMEs. -

African Dialects

African Dialects • Adangme (Ghana ) • Afrikaans (Southern Africa ) • Akan: Asante (Ashanti) dialect (Ghana ) • Akan: Fante dialect (Ghana ) • Akan: Twi (Akwapem) dialect (Ghana ) • Amharic (Amarigna; Amarinya) (Ethiopia ) • Awing (Cameroon ) • Bakuba (Busoong, Kuba, Bushong) (Congo ) • Bambara (Mali; Senegal; Burkina ) • Bamoun (Cameroons ) • Bargu (Bariba) (Benin; Nigeria; Togo ) • Bassa (Gbasa) (Liberia ) • ici-Bemba (Wemba) (Congo; Zambia ) • Berba (Benin ) • Bihari: Mauritian Bhojpuri dialect - Latin Script (Mauritius ) • Bobo (Bwamou) (Burkina ) • Bulu (Boulou) (Cameroons ) • Chirpon-Lete-Anum (Cherepong; Guan) (Ghana ) • Ciokwe (Chokwe) (Angola; Congo ) • Creole, Indian Ocean: Mauritian dialect (Mauritius ) • Creole, Indian Ocean: Seychelles dialect (Kreol) (Seychelles ) • Dagbani (Dagbane; Dagomba) (Ghana; Togo ) • Diola (Jola) (Upper West Africa ) • Diola (Jola): Fogny (Jóola Fóoñi) dialect (The Gambia; Guinea; Senegal ) • Duala (Douala) (Cameroons ) • Dyula (Jula) (Burkina ) • Efik (Nigeria ) • Ekoi: Ejagham dialect (Cameroons; Nigeria ) • Ewe (Benin; Ghana; Togo ) • Ewe: Ge (Mina) dialect (Benin; Togo ) • Ewe: Watyi (Ouatchi, Waci) dialect (Benin; Togo ) • Ewondo (Cameroons ) • Fang (Equitorial Guinea ) • Fõ (Fon; Dahoméen) (Benin ) • Frafra (Ghana ) • Ful (Fula; Fulani; Fulfulde; Peul; Toucouleur) (West Africa ) • Ful: Torado dialect (Senegal ) • Gã: Accra dialect (Ghana; Togo ) • Gambai (Ngambai; Ngambaye) (Chad ) • olu-Ganda (Luganda) (Uganda ) • Gbaya (Baya) (Central African Republic; Cameroons; Congo ) • Gben (Ben) (Togo -

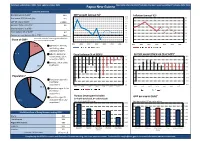

Papua New Guinea

Factsheet updated April 2021. Next update October 2021. Papua New Guinea Most data refers to 2019 (*indicates the most recent available) (~indicates 2020 data) Economic Overview Nominal GDP ($US bn)~ 23.6 GDP growth (annual %)~ 16.0 Inflation (annual %)~ 8.0 Real annual GDP Growth (%)~ -3.9 14.0 7.0 GDP per capita ($US)~ 2,684.8 12.0 10.0 6.0 Annual inflation rate (%)~ 5.0 8.0 5.0 Unemployment rate (%)~ - 6.0 4.0 4.0 Fiscal balance (% of GDP)~ -6.2 2.0 3.0 Current account balance (% of GDP)~ 0.0 13.9 2.0 -2.0 Due to the method of estimating value added, pie 1 1.0 Share of GDP* chart may not add up to 100% -4.0 1 -6.0 0.0 2013 2015 2017 2019 2021 2023 2025 2013 2015 2017 2019 2021 2023 2025 1 17.0 Agriculture, forestry, 1 and fishing, value added (% of GDP) 1 41.6 Industry (including Fiscal balance (% of GDP)~ Current account balance (% of GDP)~ 1 construction), value 0.0 40.0 1 added (% of GDP) -1.0 30.0 1 Services, value added -2.0 20.0 1 36.9 (% of GDP) -3.0 10.0 1 -4.0 0.0 1 -5.0 -10.0 Population*1 -6.0 -20.0 1 3.5 Population ages 0-14 -7.0 -30.0 1 (% of total population) -8.0 -40.0 1 35.5 2013 2015 2017 2019 2021 2023 2025 2013 2015 2017 2019 2021 2023 2025 Population ages 15-64 1 (% of total 1 population) 1 Human Development Index Population ages 65 GDP per capita ($US)~ (1= highly developed, 0= undeveloped) 61.0 1 and above (% of total Data label is global HDI ranking Data label is global GDP per capita ranking 1 population) 0.565 3,500 1 0.560 3,000 1 2,500 0.555 World Bank Ease of Doing Business ranking 2020 2,000 0.550 Ghana 118 1,500 0.545 The Bahamas 119 1,000 Papua New Guinea 120 0.540 500 153 154 155 156 157 126 127 128 129 130 Eswatini 121 0.535 0 Cameroon Pakistan Papua New Comoros Mauritania Vanuatu Lebanon Papua New Laos Solomon Islands Lesotho 122 Guinea Guinea 1 is the best, 189 is the worst UK rank is 8 Compiled by the FCDO Economics and Evaluation Directorate using data from external sources. -

Ghana, Lesotho, and South Africa: Regional Expansion of Water Supply in Rural Areas

Ghana, Lesotho, and South Africa: Regional Expansion of Water Supply in Rural Areas Water, sanitation, and hygiene are essential for achieving all the Millennium Development Goals (MDGs) and hence for contributing to poverty eradication globally. This case study contributes to the learning process on scaling up poverty reduction by describing and analyzing three programs in rural water and sanitation in Africa: the national rural water sector reform in Ghana, the national water and sanitation program in South Africa, and the national sanitation program in Lesotho. These national programs have made significant progress towards poverty elimination through improved water and sanitation. Although they are all different, there are several general conclusions that can validly be drawn from them: · Top-level political commitment to water and sanitation, sustained consistently over a long time period, is critically important to the success of national sector programs. · Clear legislation is necessary to give guidance and confidence to all the agencies working in the sector. · Devolution of authority from national to local government and communities improves the accountability of water and sanitation programs. · The involvement of a wide range of local institutions—social, economic, civil society, and media — empowers communities and stimulates development at the local scale. · The sensitive, flexible, and country-specific support of external agencies can add significant momentum to progress in the water and sanitation sector. Background and context Over the past decade, the rural water and sanitation sector in Ghana has been transformed from a centralized supply-driven model to a system in which local government and communities plan together, communities operate and maintain their own water services, and the private sector is active in providing goods and services. -

The Changing Face of Money: Preferences for Different Payment Forms in Ghana and Zambia

The Changing Face of Money: Preferences for Different Payment Forms in Ghana and Zambia Vivian A. Dzokoto Virginia Commonwealth University Elizabeth N. Appiah Pentecost University College Laura Peters Chitwood Counseling & Advocacy Associates Mwiya L. Imasiku University of Zambia Mobile Money (MM) is now a popular medium of exchange and store of value in parts of Africa, Latin America and Asia. As payment modalities emerge, consumer preferences for different payment tools evolve. Our study examines the preference for, and use of MM and other payment forms in both Ghana and Zambia. Our multi-method investigation indicates that while MM preference and awareness is high, scope of use is low in Ghana and Zambia. Cash remains the predominant mode of business transaction in both countries. Increased merchant acceptability is needed to improve the MM ecology in these countries. 1. INTRODUCTION The materiality of money has evolved over time, evidenced by the emergence of debit and credit cards in the twentieth century (Borzekowski and Kiser, 2008; Schuh and Stavins, 2010). Currently, mobile forms of payment are reaching widespread use in many regions of Sub-Saharan Africa, which is the fastest growing market for mobile phones worldwide (International Telecommunication Union [ITU], 2009). For example, M-Pesa is an extremely popular form of mobile payment in Kenya, possibly due to structural and cultural factors (Omwansa and Sullivan, 2012). However, no major form of money from the twentieth century has been completely phased out, as people exercise preferences for which form of money to use. Based on the evolution of payment methods, the current study explores perceptions and utilization of Mobile Money (MM) in Ghana, West Africa and in Zambia, South-Central Africa. -

Angola Weekly News Summary L CONTACT

Angola Weekly News Summary L CONTACT . FHONL I\0 : (212) 222-2893 FEBRUARY 5, 1916 THL U .S . Alit) Air G 0 LA Following the Congressional ban on secret U .S . aid to UNITA and FNLA, Henry Kissinger, in testimony before the Senate Foreign Lela- tions Committee, said that the Ford Administration " is now seriously considering overt financial aid " to the two groups. Kissinger claimed that there are now 11,000 Cuban troops in Angola, and said that " it is the first time that the U .s . has failed to respond to Soviet military moves outside their immediate orbit . " Kissinger also said this was "the first time the Congress has . halted the executive ' s action while it was in the process of meeting that kind of threat, " despite the fact that Congress eventually cut off funds for the war in Indochina. Following the hearings, the Senate passed the Military Aid Bill which contained a provision prohibiting military aid for Angola. Kissinger testified that the CIA is not involved in the recruit- ment of mercenaries in Angola, but when asked by Senator Charles Percy if U .S . funds are being used directly or indirectly to recruit American mercenaries, Kissinger answered, " it depends on how you define indirectly . " :MERCENARY RECRUITPMENT IN ENGLAND -_, A COVERT U .S . OPERATION Over one hundred British mercenaries, almost a third of whom are former Special Air Service soldiers, are reported to have left Britain for Angola. The group is part of over 1,000 mercenaries being sought in Britain . According to John Banks, a "military advisor " to the FNLA who fought in Nigeria with the Biafra secessionists and in South VietNam, " the money and men are available . -

Does Living in an Urban Environment Confer Advantages for Childhood

Public Health Nutrition: 9(2), 187–193 DOI: 10.1079/PHN2005835 Does living in an urban environment confer advantages for childhood nutritional status? Analysis of disparities in nutritional status by wealth and residence in Angola, Central African Republic and Senegal Gina Kennedy1,*, Guy Nantel1, Inge D Brouwer2 and Frans J Kok2 1Nutrition Planning, Assessment and Evaluation Service, Food and Nutrition Division, Food and Agriculture Organization of the United Nations, Viale delle Terme di Caracalla, I-00 100 Rome, Italy: 2Division of Human Nutrition, Wageningen University, Wageningen, The Netherlands Submitted 5 January 2005: Accepted 14 June 2005 Abstract Objective: The purpose of this paper is to examine the relationship between childhood undernutrition and poverty in urban and rural areas. Design: Anthropometric and socio-economic data from Multiple Indicator Cluster Surveys in Angola-Secured Territory (Angola ST), Central African Republic and Senegal were used in this analysis. The population considered in this study is children 0–59 months, whose records include complete anthropometric data on height, weight, age, gender, socio-economic level and urban or rural area of residence. In addition to simple urban/rural comparisons, the population was stratified using a wealth index based on living conditions and asset ownership to compare the prevalence, mean Z-score and odds ratios for stunting and wasting. Results: In all cases, when using a simple urban/rural comparison, the prevalence of stunting was significantly higher in rural areas. However, when the urban and rural populations were stratified using a measure of wealth, the differences in prevalence of stunting and underweight in urban and rural areas of Angola ST, Central African Republic and Senegal disappeared. -

Angola Benin Botswana

Volume I Section III-I - Africa Angola FY 2014 FY 2015 Individual Course Dollar Individual Course Dollar Program Students Count Value Students Count Value ALP 1 1 $26,171 1 3 $51,575 FMF 1 1 $88,271 0 0 $0.00 FMS 0 0 $0.00 1 1 $0.00 IMET-1 4 7 $209,098 13 18 $580,911 Regional Centers 7 4 $19,365 0 0 $0.00 Totals: 13 13 $342,905 15 22 $632,486 1. Military Professionalization 2. Maritime and Transnational Threats 3. Adherence to Norms of Human Right 4. Civilian Control of the Military Benin FY 2014 FY 2015 Individual Course Dollar Individual Course Dollar Program Students Count Value Students Count Value FMS 19 2 $18,319 2 2 $0.00 IMET-1 5 9 $391,211 4 8 $372,449 IMET-X 1 1 $27,614 0 0 $0.00 PKO 1929 38 $1,230,359 815 8 $0.00 Regional Centers 36 3 $30,386 0 0 $0.00 Totals: 1990 53 $1,697,889 821 18 $372,449 1. Military Professionalization 2. Maritime and Transnational Threats 3. Peacekeeping 4. Adherence to Norms of Human Right 5. Civilian Control of the Military Botswana FY 2014 FY 2015 Individual Course Dollar Individual Course Dollar Program Students Count Value Students Count Value CTFP 17 13 $112,807 3 3 $40,894 FMS 29 15 $322,116 3 11 $323,719 Volume I Section III-I - Africa 1 Volume I Section III-I - Africa IMET-1 14 21 $770,900 21 26 $640,064 IMET-2 1 1 $67,249 0 0 $0.00 Regional Centers 5 5 $10,483 0 0 $0.00 Service Academies 1 1 $72,000 0 0 $0.00 Totals: 67 56 $1,355,555 27 40 $1,004,677 1. -

Angola Background Paper

NATIONS UNIES UNITED NATIONS HAUT COMMISSARIAT HIGH COMMISSIONER POUR LES REFUGIES FOR REFUGEES BACKGROUND PAPER ON REFUGEES AND ASYLUM SEEKERS FROM ANGOLA UNHCR CENTRE FOR DOCUMENTATION AND RESEARCH GENEVA, APRIL 1999 THIS INFORMATION PAPER WAS PREPARED IN THE COUNTRY INFORMATION UNIT OF UNHCR’S CENTRE FOR DOCUMENTATION AND RESEARCH ON THE BASIS OF PUBLICLY AVAILABLE INFORMATION, ANALYSIS AND COMMENT, IN COLLABORATION WITH THE UNHCR STATISTICAL UNIT. ALL SOURCES ARE CITED. THIS PAPER IS NOT, AND DOES NOT, PURPORT TO BE, FULLY EXHAUSTIVE WITH REGARD TO CONDITIONS IN THE COUNTRY SURVEYED, OR CONCLUSIVE AS TO THE MERITS OF ANY PARTICULAR CLAIM TO REFUGEE STATUS OR ASYLUM. PREFACE Angola has been an important source country of refugees and asylum-seekers over a number of years. This paper seeks to define the scope, destination, and causes of their flight. The first and second part of the paper contains information regarding the conditions in the country of origin, which are often invoked by asylum-seekers when submitting their claim for refugee status. The Country Information Unit of UNHCR's Centre for Documentation and Research (CDR) conducts its work on the basis of publicly available information, analysis and comment, with all sources cited. In the third part, the paper provides a statistical overview of refugees and asylum-seekers from Angola in the main European asylum countries, describing current trends in the number and origin of asylum requests as well as the results of their status determination. The data are derived from government statistics made available to UNHCR and are compiled by its Statistical Unit. Table of Contents 1. -

Greening the Recovery in Ghana and Zambia Climate Change Is One of the Most Pressing Global Challenges

INSTITUTE OF SUSTAINABLE RESOURCES Greening the Recovery in Ghana and Zambia Climate change is one of the most pressing global challenges. According to the Intergovernmental Panel on Climate Change, action is needed to reduce global carbon emissions to net-zero by the middle of this century. Whilst Covid-19 has led to temporary reductions in emissions, the wider economic and social impacts of the pandemic risk slowing down or derailing action on climate change. This project focuses on the opportunities for integrating economic recovery and climate change policies in Ghana and Zambia. Both countries have been affected significantly by the pandemic. Reported numbers of infections and deaths are low when compared to rates in many developed economies. However, the economic impacts have been severe – for example, due to lower demand for commodities they export such oil and copper. Summary of NDC emissions targets The research team from the UK, Ghana and Zambia is Primary energy mix (2018) workingGreenhouse with gas governmentsemissions and other stakeholders to (million tonnes of CO2 equivalent) develop80 detailed plans for a low carbon recovery. This includes revisions to Ghana and Zambia’s national climate change70 strategies, known as Nationally Determined 80 Contributions (NDCs). The emissions targets included in Zambia 60 70 their first NDCs, submitted in 2015/16, are summarised Ghana below.50 They include more ambitious conditional targets 60 that depend on international assistance. Zambia 40 Ghana 50 12.6mtoe The research will explore how both countries could go 9.9mtoe 30 40 even further, and what policy options and investments could20 deliver them. This includes options for meeting 30 growing energy demand from low carbon sources rather 10 20 than fossil fuels, and the extent to which these plans could0 also help to achieve universal access to electricity. -

Agreement Between South Africa and Ghana

CONVENTION BETWEEN THE GOVERNMENT OF THE REPUBLIC OF SOUTH AFRICA AND THE GOVERNMENT OF THE REPUBLIC OF GHANA FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME AND ON CAPITAL GAINS Preamble The Government of the Republic of South Africa and the Government of the Republic of Ghana desiring to conclude a Convention for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income and on capital gains, Have agreed as follows: Article 1 Persons Covered This Convention shall apply to persons who are residents of one or both of the Contracting States. Article 2 Taxes Covered 1. This Convention shall apply to taxes on income and on capital gains imposed on behalf of a Contracting State or of its political subdivisions, irrespective of the manner in which they are levied. 2. There shall be regarded as taxes on income and on capital gains all taxes imposed on total income, and on total capital gains, or on elements of income or on elements of capital gains, including taxes on gains from the alienation of movable or immovable property and taxes on the total amounts of wages and salaries paid by enterprises. 3. The existing taxes to which the Convention shall apply are: (a) in Ghana: (i) the income tax; and (ii) the capital gains tax; (hereinafter referred to as “Ghana tax”); and (b) in South Africa: (i) the normal tax; (ii) the secondary tax on companies; and (iii) the withholding tax on royalties; (hereinafter referred to as “South African tax”).