About Calicut

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

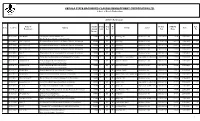

2015-16 Term Loan

KERALA STATE BACKWARD CLASSES DEVELOPMENT CORPORATION LTD. A Govt. of Kerala Undertaking KSBCDC 2015-16 Term Loan Name of Family Comm Gen R/ Project NMDFC Inst . Sl No. LoanNo Address Activity Sector Date Beneficiary Annual unity der U Cost Share No Income 010113918 Anil Kumar Chathiyodu Thadatharikathu Jose 24000 C M R Tailoring Unit Business Sector $84,210.53 71579 22/05/2015 2 Bhavan,Kattacode,Kattacode,Trivandrum 010114620 Sinu Stephen S Kuruviodu Roadarikathu Veedu,Punalal,Punalal,Trivandrum 48000 C M R Marketing Business Sector $52,631.58 44737 18/06/2015 6 010114620 Sinu Stephen S Kuruviodu Roadarikathu Veedu,Punalal,Punalal,Trivandrum 48000 C M R Marketing Business Sector $157,894.74 134211 22/08/2015 7 010114620 Sinu Stephen S Kuruviodu Roadarikathu Veedu,Punalal,Punalal,Trivandrum 48000 C M R Marketing Business Sector $109,473.68 93053 22/08/2015 8 010114661 Biju P Thottumkara Veedu,Valamoozhi,Panayamuttom,Trivandrum 36000 C M R Welding Business Sector $105,263.16 89474 13/05/2015 2 010114682 Reji L Nithin Bhavan,Karimkunnam,Paruthupally,Trivandrum 24000 C F R Bee Culture (Api Culture) Agriculture & Allied Sector $52,631.58 44737 07/05/2015 2 010114735 Bijukumar D Sankaramugath Mekkumkara Puthen 36000 C M R Wooden Furniture Business Sector $105,263.16 89474 22/05/2015 2 Veedu,Valiyara,Vellanad,Trivandrum 010114735 Bijukumar D Sankaramugath Mekkumkara Puthen 36000 C M R Wooden Furniture Business Sector $105,263.16 89474 25/08/2015 3 Veedu,Valiyara,Vellanad,Trivandrum 010114747 Pushpa Bhai Ranjith Bhavan,Irinchal,Aryanad,Trivandrum -

Hill Station

MOUNTAINS & HILLSTATIONS HILL STATION • A hill station is a town located at a higher elevation than the nearby plain which was used by foreign rulers as an escape from the summer heat as temperatures are cooler in high altitudes. MUNNAR ➢ Munnar the famed hill station is located in the Idukki district of the southwestern Indian state of Kerala. ➢ Munnar is situated in the Western Ghats range of mountains. ➢ The name Munnar is believed to mean "three rivers", referring to its location at the confluence of the Mudhirapuzha, Nallathanni and Kundaly rivers. ➢ The hill station had been the summer resort of the British Government during the colonial era. ➢ Munnar also has the highest peak in South India – Anamudi, which towers over 2695 meters ➢ Munnar is also known for Neelakurinji, a rare plant which flowers only once in twelve years. ➢ The Eravikulam National Park, Salim Ali Bird Sanctuary and tea plantations are its major attractions. DEVIKULAM HILL STATION • Devikulam is located in the Idukki district in Kerala. Situated at an altitude of 1800 meters above sea level, this hill station will give you peace, serenity and breathtaking natural beauty. • The Devi Lake, which is said to have mineral water, is a gift from the nature. • It is said that Goddess Sita (Wife of Lord Rama) bathed in the lake after which it is named since then, skin-ailments treating water of the lake OOTY • Ooty is one of the best hill stations in India and also known as Udhagamandalam, Ooty is often referred to as ‘Queen of hill stations’. • It is the capital of Nilgiris district in the state of Tamilnadu. -

Cammino Verso Il Futuro Realizzare L’Aatmanirbhar Bharat Grazie Alle Innovazioni Potpourri

ANNUNCIO DI UN NUOVO FERMENTO Appello dell’India all’ONU per una pace mondiale sostenibile IL SOUND DEL FUTURO Gli strumenti indiani tradizionali Volume 34 | Numero 05 | 2020 incontrano un avatar moderno nella musica elettronica PIANTE MIRACOLOSE Esperimenti con il bambù CAMMINO VERSO IL FUTURO Realizzare l’aatmanirbhar bharat grazie alle innovazioni POTPOURRI Pot-pourri Eventi della stagione NOVEMBRE, 2020 DEV DEEPAVALI Celebrato 15 giorni dopo il diwali, il Dev Deepavali viene 29 festeggiato a Varanasi e Prayagraj. I gradini che conducono al sacro fiume Gange si animano con le luci scintillanti di centinaia di lampade di terra. Il significato religioso di questa festa della luce risiede nella convinzione che, in questo giorno, gli dei e le dee scendono sulla Terra per festeggiare. DOVE: Uttar Pradesh 30 NOVEMBRE, 2020 1-5 DICEMBRE, 2020 FESTIVAL DI KONARK Questo festival di cinque giorni si tiene presso il Tempio del Sole di Konark, nell’Odisha, e richiama autorevoli artisti, di fama nazionale e internazionale, che eseguono l’odissi, il bharatanatyam, la danza del Manipur e altre danze e musiche classiche, folk e tribali indiane. In concomitanza con questo festival, si tiene anche un festival internazionale di arte della sabbia, presso la vicina spiaggia di Chandrabhaga. DOVE: Konark, Odisha GURU NANAK JAYANTI Questo festival commemora la nascita del primo Guru Sikh, Guru Nanak Dev Ji. Le celebrazioni iniziano due giorni prima del giorno a gurudwaras e includono una recita di 48 ore del Guru Granth Sahib, una processione chiamata Nagarkirtan guidata da cinque uomini che sorreggono la bandiera triangolare Sikh, Nishan Sa-hib, e un’esibizione di arti marziali. -

Decisions of Regional Transport Authority, Kozhikode in Themeeting Held on 4-3-2017 at Collectorate Conference Hall, Kozhikode

1 Decisions of Regional Transport Authority, Kozhikode in themeeting held on 4-3-2017 at Collectorate Conference Hall, Kozhikode. PRESENT: 1. SRI.U.V. JOSE, IAS, DISTRICT COLLECTOR AND CHAIRMAN, REGIONAL TRANSPORT AUTHORITY, KOZHIKODE. 2. Dr.P.M.MOHAMMED NAJEEB, DEPUTY TRANSPORT COMMISSIONER AND MEMBER OF REGIONAL TRANSPORT AUTHORITY, KOZHIKODE. Item No. 1 Heard. Granted concurrence for renewal of regular stage carriage permit in respect of KL 10 P 4599 as LSOS without prejudice to the right of the primary authority to fix the class of service according to the length of route and subject to verification of scheme violation if any by the original authority. Item No. 2 Heard. Granted concurrence for renewal of regular stage carriage permit in respect of KL 05 AB 3666 as LSOS without prejudice to the right of the primary authority to fix the class of service according to the length of route and subject to verification of scheme violation if any by the original authority. Item No. 3 Heard. Granted concurrence for renewal of regular stage carriage permit in respect of KL 05 AE 1825 and KL 05 AH 4972 as LSOS without prejudice to the right of the primary authority to fix the class of service according to the length of route and subject to verification of scheme violation if any by the original authority Item No. 4 Heard, the class/Type of service and distance covered in this jurisdiction are not mentioned in the agenda. Hence, decision on the application is 1 2 2 adjourned with direction to Secretary to place the matter in the ensuing meeting with all details. -

ADIP Beneficiary Data 2017-18

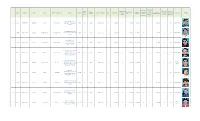

Boarding Travel cost Age / Fabrication/ and No. of days whether Monthly Total Cost of Subsidy paid to out Totel of State District Date Name Father's / Husband's Address Gender Birth Type of Aid Given Qty. Cost of Aid Fitment Loadging for which accompanie Category PHOTO Income Aid Provided station (12+13+14+15) Year Charge Expences stayed d by escort beneficiary paid Puthenpeedika, Tana, 1 Kerala Malappuram 10-01-18 Nuhman Muhammed Pullippadam, Malappuram- Male 16 2,666 TLM 12 - 18 1 6,140.00 0 6140.00 6,140.00 0 0 6,140.00 0 YES Muslim (OBC) 676542 Nediyapparambil House, 2 Kerala Malappuram 10-01-18 Akshay Dev V K Damodaran N P Nilambur Post, Malappuram- Male 17 3,500 TLM 12 - 18 1 6,140.00 0 6140.00 6,140.00 0 0 6,140.00 0 YES Muslim (OBC) 679329 Veluthedath House, Vadakkumpadam Post, 3 Kerala Malappuram 10-01-18 Akshaya K R Radhakrishnan Female 16 4000 TLM 12 - 18 1 6,140.00 0 6140.00 6,140.00 0 0 6,140.00 0 YES Muslim (OBC) Vandoor, Nilambur, Malappuram Panthalingal, Kaattumunda, Pallippad, Naduvath, 4 Kerala Malappuram 10-01-18 Aslah P Mustafa P Male 12 2,500 TLM 12 - 18 1 6,140.00 0 6140.00 6,140.00 0 0 6,140.00 0 YES Muslim (OBC) Mambad Village, Thiruvali, Malappuram-679328 Cheenkanniparackal, Kattmunda, Naduvath Post, Christian 5 Kerala Malappuram 10-01-18 Sneha Philipose Philipose Female 17 4000 TLM 12 - 18 1 6,140.00 0 6140.00 6,140.00 0 0 6,140.00 0 YES Vandoor Village, Thiruvali, General Malappuram-679328 Palakkodan, Chenakkulangara, Naduvath 6 Kerala Malappuram 10-01-18 Linju P Narayanan Female 14 1500 TLM 12 - 18 1 6,140.00 -

Recent Innovations and Developments in Electrochemical

About the Department About Calicut TEQIP-III Sponsored Established in 2006, the Department of Calicut is a major knowledge Hub of Kerala and Faculty Development Programme Chemical Engineering of National Institute of is the hometown of Institutions of National Technology Calicut offers programmes leading Importance including NITC, IIMK, DOEACC, Recent Innovations and to Bachelor’s Degree, Master’s Degree as well CWRDM etc. Calicut is connected by direct Developments in Electrochemical as Ph.D. In addition to these regular trains/road/air to all major cities in India. NITC is located about 22 kilometers north-east of and Chemical Process programmes, this Department is also actively involved in conducting International Calicut City. Calicut (Kozhikode), is known as Optimization Conferences, Faculty Development the city of spices. Kozhikode beach, Kappad Programmes, Job-oriented Short-term Training beach where Vasco Da Gama landed, RIDECPO-2019 Programmes and Continuing Education Thusharagiri Waterfalls, Pazhassiraja Museum, Programmes for Engineering professionals and Tali Temple and Kuttichira Masjid are some of June 17th-22nd 2019 academic faculty. The R&D projects the local attractions. undertaken in the past were sponsored by Preamble various agencies like the Ministry of Human Preservation of water resources is one of the Resource Development (MHRD), Department biggest challenges in the present era. Hence of Science & Technology (DST) and the Kerala there is a need to develop efficient technologies State Council for Science, Technology and and approach for treating and managing Environment (KSCSTE). wastewater. Electrochemical processes are gaining much attention for the treatment of About NIT Calicut drinking water and waste water. The exigency National Institute of Technology Calicut for greener energy technology has araised as an (NITC) is an Institution of National Importance, alternate for fossil fuel. -

Thenational Weekend

The National weekend Friday, May 9, 2014 www.thenational.ae 13 a cultural extravaganza in Kerala this year. Join thousands of UAE-based Keralites heading home for the Onam festival in August and September, and experience see ceremonies, snake-boat carnivals and song and dance (www.keralatourism.org) Made in Malabar Amar Grover explores northern Kerala’s Malabar Coast, discovering Islamic history, temples and a vegetarian crocodile by Tipu Sultan, the notorious “Ti- ger of Mysore”, during his Malabar campaign in the 1780s. It boasts sweeping views both of the complex and up and down the magnificent coastline stretching beyond. The sturdy walls coax us on a cir- cular walk along the crenellated ramparts, half of which directly overlook the Arabian Sea. We gam- bol along from one bastion to an- other and duck through a small gate where stairs dip to a short forti- fication protruding into the ocean. Its configuration alongside a small separate beach suggests a spot where medieval ships and boats once landed. It would be all too easy to see lit- tle else in Bekal’s hinterland. The Vivanta’s expansive grounds are tranquil, its pool idyllic, the beach almost deserted and there are few utterly compelling reasons to leave. If there’s any disappointment here, it’s the sea itself – strong currents sweeping the steeply shelving beach mean that the hotel urges guests not to swim here at all and it’s obvious that would-be bathers really ought to take care. Just beyond Kasaragod, Bekal’s nearest town, we drop by a couple of curious temples. -

Wayanadu 3 N / 4 D

Wayanadu 3 N / 4 D Wayanad Wayanad District, in the north-east of Kerala, India, was formed on November 1, 1980 as the 12th district, carved out of Kozhikode District and Kannur District. Though the the word Wayanad is believed by some to have originated from Vayal (paddy) and Naad (land), 'Land of Paddy Fields', some scholars disagree. The region was known as Mayakshetra (Maya's land) in the earliest records. Mayakshetra evolved into Mayanad and finally to Wayanad. There are many indigenous tribals in this area. It is set high on the majestic Western Ghats with altitudes ranging from 700 to 2100 m. The district is going through its worst agrarian crisis. Day 1: Arrive at Calicut / Kozhikode International airport or the railway station, our representative(s) will take you to Wayanad (about 4 hrs’ drive). You will be delighted with the mesmerizing sight of hills, caves hiding some secrets of the past, lakes reflecting the surrounding lustrous forests, small streams and miniature water falls caressing the hills and dales. So much beauty, so much charm all around; you feel a thunderbolt within. Leisure and ecstasy will wipe the weariness of long drawn journey off your brow; yes, you are safe, happy and comfortable in our guidance. We take you to the caves of Wayanad for they have a story of some ancient natives to tell you. We are with you as you move leisurely through the forests singing the tune of birds in the forests. We are with you as your feet carelessly touch the cool dew drops from the morning grass and the eyes watch a thousand suns above. -

School Phone Numbers (High School Section) All Kerala

SCHOOL PHONE NUMBERS (HIGH SCHOOL SECTION) ALL KERALA Sl.No School Code Name of School Address PIN PHONE Categary 1 11001 Sri. Annapurneshwari H.S. Agalpady Kumbdaje P.O,, Kasaragod 671551 04998 260639 A 2 11002 GOVT. H S S Kasaragod Kasargode P.O 671121 04994 221626 G 3 11003 Govt.Muslim V.H.S.S Kasaragod Thalangara P.O.,, Kasaragod 671122 04994 230479 G 4 11005 B.E.M.H.S Kasaragod Kasaragod P.O 671121 04994 4222887 A 5 11006 Govt. V.H.S.S for Girls Kasaragod Kasaragod P.O 671121 04994 230368 G 6 11007 S.A.T.H.S Manjeshwar Manjeshwar P.O.,, Kasaragod 671323 04998 273475 A 7 11008 Udaya E M H S S Udayanagar, Manjeshwar Manjeshwar P.O.,, Kasaragod 671322 9447112886 U 8 11009 Govt.V.H.S.S. Kunjathur Kunjathur P.O,, Kasaragod 671323 04998 279150 G 9 11010 Sri Vidya Vardhaka H.S, Miyapadavu Miyapadavu P.O.,, Kasaragod 671323 04998 252100 A 10 11011 Sri Vani Vijaya H.S. Kodalamogaru Kodalamogaru P.O 671323 04998 202990 A 11 11012 K.V.S.M. H.S Kurudapadavu Kurudapadavu P.O., Kasaragod 671322 04998 205357 A 12 11013 Govt H.S. Mangalpady Mangalpady P O,, Kasaragod 671324 04998 243399 G 13 11014 Govt H.S.S Shiriya Shiriya P O,, Kasaragod 671321 04998 216187 G 14 11015 Govt H.S.S Uppala Uppala P O,, Kasaragod 671322 04998 244700 G 15 11016 Govt.H.S. Bangara Manjeshwar Bangara Manjeshwar P.O.,, Kasaragod 671323 04998 272001 G 16 11017 Govt. H. S. S. -

Accused Persons Arrested in Kozhikode Rural District from 06.12.2020To12.12.2020

Accused Persons arrested in Kozhikode Rural district from 06.12.2020to12.12.2020 Name of Name of the Name of the Place at Date & Arresting Court at Sl. Name of the Age & Cr. No & Sec Police father of Address of Accused which Time of Officer, which No. Accused Sex of Law Station Accused Arrested Arrest Rank & accused Designation produced 1 2 3 4 5 6 7 8 9 10 11 Sayooj PUTHIYOTTIL, 1063/2020, u/s 26/2020, 11-12-2020 kumar,Sub BAILED BY 1 ANURAG BABU ELETTIL, Elettil vattoli 5,4(2)(j) OF Koduvally Male at 15:46 hrs inspector POLICE CHETTAKADAVU KEDO 2020 ,Koduvally 604/2020, u/s 4(2)(a), 4(2)(j) of Kerala Epidemic Diseases Ordinance MANGATTU 2020 ,3(b) of BABY MUJEEB IBRAHIM 25/2020, THIRUVAMB 11-12-2020 Thiruvambad BAILED BY 2 HOUSE, CALICUT The Kerala MATHEW, SI RAHMAN SAHIB Male ADY at 12:40 hrs y POLICE AIRPORT POST, Epidemic OF POLICE. Disease corona Virus Diseas (COVID-19) Additional Regulations - 2020 604/2020, u/s 4(2)(a), 4(2)(j) of Kerala Epidemic Diseases Ordinance Vellathodika House, Saiful Adil 2020 ,3(b) of Muhammad 23/2020, Calicut Airport (po), 11-12-2020 Thiruvambad BAILED BY 3 VTSAFUL Balussery The Kerala SI Balussery kutty VT Male Kondotty, at 12:40 hrs y POLICE AADIL Epidemic Malappuram Disease corona Virus Diseas (COVID-19) Additional Regulations - 2020 604/2020, u/s 4(2)(a), 4(2)(j) of Kerala Epidemic Diseases Ordinance MUZHIMPATTUPA 2020 ,3(b) of BABY IBRAHIM 25/2020, RAMBIL HOUSE, THIRUVAMB 11-12-2020 Thiruvambad BAILED BY 4 AYYOOB The Kerala MATHEW, SI ANAS Male CALICUT AIRPORT ADY at 12:40 hrs y POLICE Epidemic OF POLICE. -

Cholan Tour Pvt Ltd

+91-8068442249 Cholan Tour Pvt Ltd https://www.indiamart.com/window-tothe-world/ Let loose yourself in the midst of lush Kerala backwaters, panoramic wildlife, aromatic tea plantations, holy places and sun-kissed beaches with Kerala tours. About Us Let loose yourself in the midst of lush Kerala backwaters, panoramic wildlife, aromatic tea plantations, holy places and sun-kissed beaches with Kerala tours. Kerala, the “God’s own Country” is a destination fit for adventure, culture and of course, relaxation. With its amiable beach sights, swaying palm trees, and panoramic houseboat rides along tropical backwaters, you will come to know why National Geographic Traveller voted this south Indian state amongst ten most explored places of the world. There are many attractions, adventures and elements that make Kerala travel memorable for lifetime. Of them is the lush green forest fringed with coconut trees that allure many people to come and lay down in its grooving shade. The gracious hospitality of keralites also makes people keep visiting this state most often. Whether you’re planning an evening lounge on a shimmering beach or want to discover the splendid backwaters, we help you plan your tours to Kerala in an amazing way. From love-struck honeymooners to solo travelers, backpackers & international vacationers, this south Indian state welcomes everybody with a heart-warming embrace. With our customized tour packages you may expect the finest of services. With our Ayurveda tour packages you can rejuvenate your mind, body and soul. Relish the therapeutic massage at renowned Ayurvedic health centers, enjoy delectable south Indian cuisines & go camera crazy at monumental.. -

E-Catalogue of Kerala Tourism Videos

E-catalogue of Kerala Tourism Videos E-book produced by Department of Tourism, Government of Kerala. www.keralatourism.org Table of Contents E-catalogue of Kerala Tourism Videos Kerala Films Kerala Promo How to reach Kerala AV Guide Kochi AV Guide to Districts Greeting Videos Newsletter Videos Tourism Travel Videos Responsible Tourism Tourist Spots Hill Stations Beaches Backwaters Royalty free videos Kerala Videos Ayurveda Videos Art Forms Performing Art Forms Ritual Art Forms Folk Art Forms Tribal Art forms Festivals Theyyam Onam Thrissur Pooram Arattupuzha Pooram Thootha Pooram Cuisine of Kerala Kerala Cuisine - Veg Kerala Cuisine - Non Veg Kerala Tribal Cuisine Forest & Wildlife Village Life Ayurveda Museums and Galleries Music Music Festivals Musical Instruments Instrumental Music Crafts Video Quiz Ayurveda Quiz Kerala Quiz Kalaripayattu Folk Games Kerala Films Kerala Backwaters in Ayurvedic Your Moment is Kerala Hill Station Your Moment is Rejuvenation Waiting Holidays Waiting Holidays, Kerala Kerala Tourism Ad - Life in God's Own Your Moment is God's own canvas - Your Moment is Country Waiting Movie Destinations in Waiting Kerala Splendour of waves - Beach holidays in Kerala Kerala Promo Malappuram district, Monsoon in Kerala Reflections of GOD's Gardens of the Gods Tourism Projects Own Country ; Kerala Ayurveda in Kerala Eco -tourism, Hill Water Colors by God The Very best of station, Forests, Wayanad, Volume 1 Kerala Call of the Wild - kerala's Backwater Kerala Tourism Visuals of Kerala Promotional video Holidays Projects Western