Reliance Industries

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

RELIANCE BRANDS Limited 1

RELIANCE BRANDS LIMITED 1 Reliance Brands Limited Financial Statements 2019-20 2 RELIANCE BRANDS LIMITED Independent Auditor’s Report To The Members of Reliance Brands Limited Report on the Audit of the Financial Statements Opinion We have audited the Financial Statements of Reliance Brands Limited (“the Company”), which comprise the Balance Sheet as at 31st March 2020, the Statement of profit and loss, Statement of changes in equity and Statement of Cash Flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies and other explanatory information (hereinafter referred to as “ Financial Statements”). In our opinion and to the best of our information and according to the explanations given to us, the aforesaid financial statements give the information required by the Companies Act, 2013 (“the Act”) in the manner so required and give a true and fair view in conformity with the accounting principles generally accepted in India, of the state of affairs of the Company as at March 31, 2020, and its Loss including Other Comprehensive Income, changes in equity and its cash flows for the year ended on that date. Basis for Opinion We conducted our audit in accordance with the Standards on Auditing specified under section 143(10) of the Act. Our responsibilities under those Standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Company in accordance with the Code of Ethics issued by the Institute of Chartered Accountants of India together with the ethical requirements that are relevant to our audit of the Financial Statements under the provisions of the Act and the Rules thereunder, and we have fulfilled our other ethical responsibilities in accordance with these requirements and the Code of Ethics. -

Reliance Industries

25 July 2021 1QFY22 Results Update | Sector: Oil & Gas Reliance Industries Estimate change CMP: INR2,105 TP: INR2,485 (+18%) Buy TP change Rating change O2C and Telecom deliver; Retail is recovering gradually EBITDA for the consolidated/standalone business rose 38%/61% YoY in Motilal Oswal values your support in the 1QFY22 on a low base of last year (2% beat). On a QoQ basis, consolidated Asiamoney Brokers Poll 2021 for India Research, Sales, Corporate Access and revenue/EBITDA is up -6%/1%. RJio’s EBITDA was in line (up 23% YoY), while Trading team. We request your ballot. the same for Retail grew 79% YoY (6% beat) on a low base. Despite the impact of the second COVID wave, RJio held its ground after the push from the Jio Phone launch in 4QFY21. Revenue/EBITDA grew 4% QoQ (in line) on a steady 14.4m net subscriber additions, along with flattish ARPU. EBITDA margin expanded 10bp QoQ to 47.9%. Bloomberg RIL IN Reliance Retail’s revenue/EBITDA grew 19%/79% YoY (6% EBITDA beat) as Equity Shares (m) 6,339 the second COVID wave had a lesser impact v/s that in 1QFY21, cushioned M.Cap.(INRb)/(USDb) 13793.7 / 185.4 by the e-commerce business, swift recovery, and lesser intensity of the 52-Week Range (INR) 2369 / 1830 lockdown. Compared to pre-COVID levels (1QFY20), EBITDA was flat. 1, 6, 12 Rel. Per (%) -6/-6/-37 The company reported an O2C EBITDA that was 6% higher than our estimate 12M Avg Val (INR M) 28673 at INR114.6b (+61% YoY, +12% QoQ). -

Statutory Reports

CORPORATE MANAGEMENT GOVERNANCE FINANCIAL NOTICE Corporate Governance Report OVERVIEW REVIEW STATEMENTS highest standards of ethics. It has before exceptional items 23.7%. The of the Board while nurturing a culture thus become crucial to foster and financial markets have endorsed our where the Board works harmoniously sustain a culture that integrates all sterling performance and the market for the long-term benefit of the “Between my past, the present and the future, there is one common factor: components of good governance by capitalisation has increased by CAGR Company and all its stakeholders. The carefully balancing the inter-relationship of 31.5% during the same period. In Chairman guides the Board for effective Relationship and Trust. This is the foundation of our growth.” among the Board of Directors, Board terms of distributing wealth to our governance in the Company. Committees, Finance, Compliance & shareholders, apart from having a Shri Dhirubhai H. Ambani The Chairman takes a lead role in Assurance teams, Auditors and the track record of uninterrupted dividend Founder Chairman managing the Board and facilitating Senior Management. Our employee payout, we have also delivered effective communication among satisfaction is reflected in the stability consistent unmatched shareholder Directors. The Chairman actively works of our senior management, low attrition returns since listing. The result of our with the Human Resources, Nomination across various levels and substantially initiative is our ever widening reach and Remuneration Committee to higher productivity. Above all, we feel and recall. Our shareholder base has plan the Board and Committees’ honoured to be integral to India’s social grown from 52,000 after the IPO composition, induction of directors to development. -

LYF Smartphone+ Introduces Special Edition LYF F1 – a Device Designed to Deliver Enhanced Experience Over Advanced 4G Network

MEDIA RELEASE LYF Smartphone+ introduces special edition LYF F1 – a device designed to deliver enhanced experience over advanced 4G network Special Edition device features cutting-edge technology that works best with Jio – the world’s largest all-4G network Mumbai, 21st October 2016: Reliance Retail today launched LYF F1, a Special Edition future- ready device from LYF Smartphone+. From introducing VoLTE in smartphones across all price segments to offering advanced features, such as dual camera, smart gestures and voice command controls, LYF continues to spearhead the transition in smartphone technology. With F1, LYF presents a future ready device designed to deliver an enhanced experience over advanced networks. Equipped with carrier aggregation (CA) support, LYF F1 is designed to tap the fullest potential of Jio, the world’s largest all-IP network. The CA technology gives users vastly improved data transfer rates and unmatched browsing experience. This feature is known to boost battery life. Importantly, F1 comes equipped with Rich Communication Services – a set of evolved Messaging services and enriched calling features. The evolved Messaging feature, an enhancement of the existing SMS feature on LTE network, allows group chat, file and location sharing, and much more through the good old SIM-based messaging. Enriched calling lets the user set context to a call by adding location, image, urgency and customised message. Loaded with a 16 MP rear camera, LYF F1 is designed for low-light photography, powered by advanced software technology. Other camera features include a unique multi-focus mode, and electronic image stabilisation that allows steady video recording while in motion. -

Reliance Industries

1 November 2020 2QFY21 Results Update | Sector: Oil & Gas Reliance Industries Estimate change CMP: INR2,054 TP: INR2,240 (+8%) Buy TP change Rating change Consumer biz cushions sharp fall in Oil and Gas biz Reliance Industries (RIL)’s 2QFY21 consolidated/standalone business EBITDA was Bloomberg RIL IN down 14%/44% YoY. This was weighed by sharp decline in refining Equity Shares (m) 6,339 throughput/margin and a weak Retail biz (hurt by the lockdown), but partly offset M.Cap.(INRb)/(USDb) 13524.8 / 180 by the growing Digital business. 52-Week Range (INR) 2369 / 867 RJio’s revenue/EBITDA growth slowed to 6%/7% QoQ (in-line) due to the 1, 6, 12 Rel. Per (%) -12/24/41 combination of 3% ARPU and subscriber growth each, coupled with 60bp margin 12M Avg Val (INR M) 29721 expansion to 42.6%. Reliance Retail’s net revenues were flat YoY at INR366b (in-line). This is Financials & Valuations (INR b) commendable despite the lockdown and lack of footfall at stores in 2QFY21. Y/E March FY21E FY22E FY23E Net Sales 5,438 7,191 7,845 During the quarter, RIL operated its refining and petrochemical units at >90% EBITDA 823 1,217 1,397 despite the much lower utilization rates of its Indian peers – the company is Net Profit 418 677 809 enjoying the benefits of its integrated Oils-to-Chemicals (O2C) business model. Adj. EPS (INR) 64.8 105.1 125.6 Despite a poor SG GRM benchmark, RIL reported a GRM of USD5.7/bbl. RIL EPS Gr. -

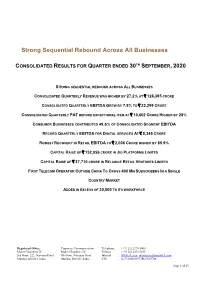

Strong Sequential Rebound Across All Businesses

Strong Sequential Rebound Across All Businesses CONSOLIDATED RESULTS FOR QUARTER ENDED 30TH SEPTEMBER, 2020 STRONG SEQUENTIAL REBOUND ACROSS ALL BUSINESSES CONSOLIDATED QUARTERLY REVENUE WAS HIGHER BY 27.2% AT ` 128,385 CRORE CONSOLIDATED QUARTERLY EBITDA GREW BY 7.9% TO ` 23,299 CRORE CONSOLIDATED QUARTERLY PAT BEFORE EXCEPTIONAL ITEM AT ` 10,602 CRORE HIGHER BY 28% CONSUMER BUSINESSES CONTRIBUTED 49.6% OF CONSOLIDATED SEGMENT EBITDA RECORD QUARTERLY EBITDA FOR DIGITAL SERVICES AT ` 8,345 CRORE ROBUST RECOVERY IN RETAIL EBITDA TO ` 2,006 CRORE HIGHER BY 85.9% CAPITAL RAISE OF ` 152,056 CRORE IN JIO PLATFORMS LIMITED CAPITAL RAISE OF ` 37,710 CRORE IN RELIANCE RETAIL VENTURES LIMITED FIRST TELECOM OPERATOR OUTSIDE CHINA TO CROSS 400 MN SUBSCRIBERS IN A SINGLE COUNTRY MARKET ADDED IN EXCESS OF 30,000 TO ITS WORKFORCE Registered Office: Corporate Communications Telephone : (+91 22) 2278 5000 Maker Chambers IV Maker Chambers IV Telefax : (+91 22) 2278 5185 3rd Floor, 222, Nariman Point 9th Floor, Nariman Point Internet : www.ril.com; [email protected] Mumbai 400 021, India Mumbai 400 021, India CIN : L17110MH1973PLC019786 Page 1 of 19 STRATEGIC UPDATES • Jio Platforms Limited, a wholly owned subsidiary of Reliance Industries Limited, raised ₹ 152,056 crore from leading global investors including Facebook, Google, Silver Lake, Vista Equity Partners, General Atlantic, KKR, Mubadala, ADIA, TPG, L Catterton, PIF, Intel Capital and Qualcomm Ventures. • Reliance Retail Ventures Limited (RRVL), a wholly owned subsidiary of Reliance Industries Limited, raised ` 37,710 crore of investments from leading global investors including Silver Lake, KKR, General Atlantic, Mubadala, GIC, TPG and ADIA. -

Reliance Industries

14 April 2020 Company Update Reliance Industries Investment in consumer business paying BUY off, upgrade to Buy CMP (as on 13 Apr 20) Rs 1,191 Target Price Rs 1,400 RIL stock has corrected by 25% from its peak over the past 4 months driven by global economic slowdown concerns. Our view that the stock price correction NIFTY 8,994 is overdone, and the stock should outperform, is premised on 1) Non-cyclical domestic consumer business accounting for 56% of FY21E EBITDA (31% in KEY CHANGES OLD NEW FY19), 2) The stock factoring only an USD 3.0/bbl FY21E refining margin, 49% Rating ADD BUY lower than Global Financial Crises (GFC) quarterly trough and 3) Interest Price Target Rs 1,566 Rs 1,400 Coverage ratio of 4.3x and Net Debt/EBITDA of 1.6x in FY22E (12-35% better FY21E FY22E than the FY19 lows). The stock offers 18% upside at our TP of INR 1,400. EPS % -27% -10% No financial stress even under economic slowdown conditions KEY STOCK DATA We estimate that even with refining margins of USD 5.9/bbl (lowest quarterly Bloomberg code RIL IN margin during the Global Financial Crises and 36% lower than 3QFY20) and Petchem margins at a discount of 29% to 3QFY20 (lowest quarterly margin in No. of Shares (mn) 6,339 last 13 years), RIL’s FY21E EBITDA would be INR 775bn, more than adequate to MCap (Rs bn) / ($ mn) 7,737/101,358 service its INR 2.9trn of debt. 6m avg traded value (Rs mn) 17,400 52 Week high / low Rs 1,618/876 Jio: Next catalysts-Mobile revenue growth, fibre broadband ramp-up With about USD 50bn (50% of market cap) invested in telecom, Jio’s revenue STOCK PERFORMANCE (%) market share growth and monetisation continues to drive a significant 3M 6M 12M proportion of the value creation opportunity for RIL’s shareholders. -

India Internet a Closer Look Into the Future We Expect the India Internet TAM to Grow to US$177 Bn by FY25 (Excl

EQUITY RESEARCH | July 27, 2020 | 10:48PM IST India Internet A Closer Look Into the Future We expect the India internet TAM to grow to US$177 bn by FY25 (excl. payments), 3x its current size, with our broader segmental analysis driving the FY20-25E CAGR higher to 24%, vs 20% previously. We see market share likely to shift in favour of Reliance Industries (c.25% by For the exclusive use of [email protected] FY25E), in part due to Facebook’s traffic dominance; we believe this partnership has the right building blocks to create a WeChat-like ‘Super App’. However, we do not view India internet as a winner-takes-all market, and highlight 12 Buy names from our global coverage which we see benefiting most from growth in India internet; we would also closely watch the private space for the emergence of competitive business models. Manish Adukia, CFA Heather Bellini, CFA Piyush Mubayi Nikhil Bhandari Vinit Joshi +91 22 6616-9049 +1 212 357-7710 +852 2978-1677 +65 6889-2867 +91 22 6616-9158 [email protected] [email protected] [email protected] [email protected] [email protected] 85e9115b1cb54911824c3a94390f6cbd Goldman Sachs India SPL Goldman Sachs & Co. LLC Goldman Sachs (Asia) L.L.C. Goldman Sachs (Singapore) Pte Goldman Sachs India SPL Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. -

Store Code Format Store Name Store Address 3507 My JIO MATRUCHYA

Store Code Format Store Name Store address Reliance Digital Xpress Mini, Shop No 08 Ground Floor M/s.Mogal 3507 My JIO MATRUCHYA BLDG KA Brothers Matruchya Building , Shivaji Path Station Road, Near Sony Showroom, Kalyan (W), PIN - 421301 Reliance Digital Xpress Mini, Shop No 04 Ground Floor Citi Centre, 3508 My JIO CITI CENTRE Opp. Arihant Apartment, Dhamankar Naka Bhiwandi 421302 Reliance Digital Xpress Mini, 21,Shop No. B 28, Kalpak Estate 3541 My JIO ANTOP HILL S.M.Road, Antop Hill, Mumbai 400037 Reliance Digital Xpress Mini, Shop No.14, Cebestial Apt, Vasai 3559 My JIO CEBESTIAL APT. VAS Nalasopara Link Road, Vasai (E) , 401207 Reliance Digital Xpress Mini, Shop no 4 manwani society 206 laxmi 3561 My JIO LAXMI APT. WORLI N apt dr annie beasant road near city bakery worli naka mumbai 4000018 Reliance Digital Xpress Mini, Shop No. 6 Arpan Arcade, CST Road, 3575 My JIO ARPAN ARCADE KURLA Kurla (W). Mumbai 400070 Reliance Digital Xpress Mini, Digital Xpress mini, Ludo Mall, Ward 3754 My JIO LUDO MALL PRABHAD Agar Bazar, Churchwadi Junction, S K Bole Road, Kashinath Dhuru Road, Prabhadevi, Dadar West, Mumbai 400028, Maharashtra Reliancedigital Retail Ltd., Ground Floor & First Floor V N Purav 3796 Digital PARC CHEMBUR Road Chembur, Near Swastik Mill Compound, Chembur Mumbai, 400071,Maharashtra Reliance Digital Xpress Mini, Baggey Bags, Shop No 2, Chembur 6144 My JIO BAGGEY BAGS Guest House, Plot No.3 A, B N Acharya Marg, Chembur (E), Mumbai 400071 Reliance Digital Xpress Mini, Shop no 11 ground floor star mall mc 6155 My JIO STAR MALL -

Reliance Retail Performance

Reliance Retail Performance ➢ 6th fastest growing retailer globally1; Ranked 94th in the list of Global Powers of Retailing1 ➢ One of the World’s fastest store expansion, added ~10 stores a day in last 2 years; crossed 10,000 store milestone ➢ Reliance Retail operates more stores than any other organised retailer. ➢ Registered over 500 million footfalls in FY19, growth of 44% Y-o-Y ➢ Extended physical store presence to 6,600+ cities across India ➢ Added 2,829 stores during the year; Now operate 10,415 stores covering over 22 mn sq.ft. of retail space ➢ Over 113,000 people employed Crossed a record milestone of 10,000 stores 1. Source: Deloitte Report Titled “Global Powers of Retailing” 2019 47 Reliance Retail’s Journey Reliance Retail Revenues All figures in ₹ Crore 130,566 Reliance Retail EBITDA Revenue CAGR: ➢ Last 5 years: 55% ➢ Last 10 years: 44% 69,198 6,201 33,765 EBITDA CAGR: 21,075 17,640 2,529 14,556 10,845 ➢ Last 5 years: 76% 6,102 7,636 1,179 3,344 4,565 784 857 363 31 -518 -341 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 Retailer of a Global Scale Global Ranking Source: Global powers of retailing 2019, Deloitte; Reliance Retail ranking basis FY18 financial numbers 48 Financial Performance ➢ FY 2018-19 Revenues at ₹ 1,30,566 crore, nearly doubling from FY 2017-18 ➢ FY 2018-19 EBITDA at ₹ 6,201 crore, 2.5x FY18 full year EBITDA ➢ EBITDA margin of 4.7% vs 3.7% last year; Core Retail EBITDA margin at 7.0% vs 6.0% last year ➢ 4Q FY 2018-19 Revenues at ₹ 36,663 crore, up 52% Y-o-Y and 3% Q-o-Q ➢ 4Q FY 2018-19 EBITDA at -

Annual Report 2019-20

Annual Report 2019-20 Creating Experiences The Group commissioned India’s largest integrated TV and Digital Newsroom at Mumbai. What’s Inside Corporate Overview 01 Creating Experiences 02 Across Mediums 03 Across Languages 04 Across Screens 05 Across Narratives 06 Across Genres 08 Letter to Shareholders 09 Corporate Information 10 Board of Directors Statutory Reports 12 Management Discussion and Analysis 30 Board’s Report 40 Business Responsibility Report 49 Corporate Governance Report Financial Statements 71 Standalone Financial Statements 121 Consolidated Financial Statements Notice 181 Notice of Annual General Meeting View this report online or download at www.nw18.com A large bouquet of diversified brands, crafted to meet the diverse needs of audiences across regions, cultures, segments, genres and languages, defines the ethos of Network18 Media & Investments Limited (Network18). As one of India’s largest media conglomerates, Network18 has redefined the Media and Entertainment sector of the country, while carving a distinctive niche for itself as a thought leader in the industry. With our finger on the pulse of people across the culturally contrasting milieus of Bharat and India, we remain closely connected with audiences through multiple channels of mediums, languages, platforms, screens, devices and formats. At the heart of this consumer connect lies our ability to align ourselves to the differentiated and evolving aspirations, needs and consumption patterns of people across the country. From News to Entertainment and across TV, Digital and Print, our portfolio of offerings is designed to engage with audiences across segments and genres. We create enriching experiences for them with our quality content that caters as effectively to the premium audiences as it does to the masses. -

SBI and Reliance Jio Deepen Partnership to Spur Digital Transactions by SBI Customers News, August 03, 2018

SBI and Reliance Jio deepen partnership to spur digital transactions by SBI customers News, August 03, 2018 Reliance Jio Infocomm Limited (RJIL) and State Bank of India (SBI) are entering into a digital partnership which aims at increasing SBI’s digital customer base. As per the partnership, SBI’s You Only Need One’s (YONO) digital banking features and solutions will be enabled through the MyJio platform for a seamless, integrated and superior customer experience. MyJio will also bring in financial services capabilities of SBI and Jio Payments Bank. Further, RJIL and SBI customers will benefit from Jio Prime, which would offer exclusive deals from Reliance Retail, partner brands and merchants. Additionally, the integration between SBI Rewardz and Jio Prime would offer a loyalty reward earning opportunities as well as broader redemption within Reliance Jio and other online and physical partner ecosystems to SBI customers. SBI will also make Jio as one of its preferred partners for designing and providing network and connectivity solutions. Earlier, SBI and Jio had entered into a joint venture to launch Jio Payments Bank. Speaking on the partnership, Mr. Rajnish Kumar, Chairman, SBI said, “As India’s largest bank with leadership in digital banking, we are delighted to partner with Jio, the world’s largest network. All the areas of co-operation are mutually beneficial enhancing the digital foot-print for SBI customers with superior and rewarding customer experiences.” Mukesh D. Ambani, Chairman, Reliance Industries Limited said, “The scale of the SBI customer base is unmatched globally. Jio is committed to using its superior network and platforms combined with the Retail ecosystem to accelerate digital adoption serving all the needs for SBI’s and Jio’s customers.” 1 / 2 SBI and Reliance Jio deepen partnership to spur digital transactions by SBI customers News, August 03, 2018 About Us We are Hiring Contact Us Subscribe Privacy Policy Advertise Terms & Conditions Copyright © 2010, tele.net.in All Rights Reserved 2 / 2 .