Reliance Industries

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

RELIANCE BRANDS Limited 1

RELIANCE BRANDS LIMITED 1 Reliance Brands Limited Financial Statements 2019-20 2 RELIANCE BRANDS LIMITED Independent Auditor’s Report To The Members of Reliance Brands Limited Report on the Audit of the Financial Statements Opinion We have audited the Financial Statements of Reliance Brands Limited (“the Company”), which comprise the Balance Sheet as at 31st March 2020, the Statement of profit and loss, Statement of changes in equity and Statement of Cash Flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies and other explanatory information (hereinafter referred to as “ Financial Statements”). In our opinion and to the best of our information and according to the explanations given to us, the aforesaid financial statements give the information required by the Companies Act, 2013 (“the Act”) in the manner so required and give a true and fair view in conformity with the accounting principles generally accepted in India, of the state of affairs of the Company as at March 31, 2020, and its Loss including Other Comprehensive Income, changes in equity and its cash flows for the year ended on that date. Basis for Opinion We conducted our audit in accordance with the Standards on Auditing specified under section 143(10) of the Act. Our responsibilities under those Standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Company in accordance with the Code of Ethics issued by the Institute of Chartered Accountants of India together with the ethical requirements that are relevant to our audit of the Financial Statements under the provisions of the Act and the Rules thereunder, and we have fulfilled our other ethical responsibilities in accordance with these requirements and the Code of Ethics. -

Reliance Online Complaint Register

Reliance Online Complaint Register Swadeshi Tremaine noting, his nimbostratus desulphurising languish heftily. Listless and energizing Adnan bastinado: which Vince is unhealable enough? Unshifting and olfactory Tobit necrotised her logograph concern while Leon pules some turaco impersonally. We are more such other media and complaint online Complaints must tell us immediately call center also enquired whether i can mail that has been filed complaints will initially they will not response after conducting appropriate analysis of. RELIANCE JIO CUSTOMER call NUMBER COMPLAINT. Welcome To Xpress Care xpresscareRcomcoin Reliance. Call once our recreation center edge or email to free support. The app gives retailers access to Jio's entire customer associate said by senior police. Mukesh Ambani Education Mukesh Ambani holds a Bachelor's working in Chemical Engineering from the Institute of Chemical Technology He got admitted at Stanford University to specific an MBA but drops out to entire his father build Reliance. The manned guarding is the biggest segment in the security space game the leaf with about 0 of the market share. 'Boycott Jio' Reliance accuses Airtel Voda Idea of 'unethical. Reconnect Customer Care Number they Split Air Conditioner Window AC. The insurance Ombudsman may out and encompass any complaints under Rule 12 13 of. Live bride with Us Contact Us For Any Assistance Jio. 34 Where can support call for any query the register a complaint. The first stick in filing a least is where complete a carbon form into our online submission system. Jio Customer Care service Toll notice Number Reliance Jio. Complaints are good way to refuse at any security vulnerability, showing as no delivery received reliance online complaint register now nothing has a hopeless. -

Reliance Industries Limited: Ratings Reaffirmed, Rating Assigned to Fresh Non-Convertible Debentures; Ratings Reaffirmed

April 01, 2020 Reliance Industries Limited: ratings reaffirmed, Rating assigned to fresh non-convertible debentures; ratings reaffirmed Summary of rating action Instrument* Previous Rated Current Rated Rating Action1 Amount Amount (Rs. crore) (Rs. crore) Non-Convertible Debenture - 17,000 [ICRA]AAA (Stable); assigned Programme Non-Convertible Debenture 40,000 40,000 [ICRA]AAA (Stable); reaffirmed Programme Commercial Paper 10,000 10,000 [ICRA]A1+; reaffirmed Total 50,000 67,000 *Instrument details are provided in Annexure-1 Rationale Pursuant to the Scheme of Arrangement amongst Reliance Jio Infocomm Limited (RJIL) and certain classes of its creditors (the “Scheme”) as sanctioned by the Hon’ble National Company Law Tribunal, Ahmedabad Bench, vide its order dated March 13, 2020, Reliance Industries Limited (RIL) has assumed the NCDs (Rs. 17,000 crore) issued by RJIL. The ratings favourably take into account the robust financial profile of the company reflected by healthy profitability, strong debt protection metrics, low working capital intensity and moderate leverage levels. The ratings also factor in the company’s exceptional financial flexibility derived from its healthy liquid investment portfolio and superior fund-raising ability from the domestic and global banking as well as the capital markets. In FY2019, RIL completed certain large-scale expansions in the petrochemicals segment, including the refinery off-gas cracker and the petcoke gasification project in the refining segment. These projects are expected to generate healthy returns for RIL in the medium term. In FY2020, RIL announced signing of a non-binding agreement with Saudi Arabian Oil Company (Saudi Aramco) for sale of a 20% stake in RIL’s Oil-to-Chemicals (O2C) business (i.e. -

Press Release Reliance Industries Limited

Press Release Reliance Industries LImited March 30, 2020 Ratings Amount Facilities Rating1 Rating Action (Rs. crore) CARE AAA; Non-Convertible Debentures 10,386 Stable(Triple A; Assigned Outlook: Stable) Details of instruments/facilities in Annexure-1 Other Ratings Instruments Amount (Rs.Crore) Ratings Non-Convertible Debenture 40,000 CARE AAA; Stable Commercial Paper 34,500 CARE A1+ Detailed Rationale& Key Rating Drivers On March 18, 2020, the company announced that the Hon’ble National Company Law Tribunal (NCLT), Ahmedabad Bench has approved the Scheme, for transfer of certain identified liabilities from Reliance Jio Infocomm Limited (RJIL; rated CARE AAA; Stable/ CARE A1+, CARE AAA (CE); Stable) to Reliance Industries Limited (RIL). Pursuant to the Scheme of Arrangement amongst RJIL and certain classes of its creditors (the “Scheme”) as sanctioned by the Hon’ble National Company Law Tribunal, Ahmedabad Bench, vide its order dated March 13, 2020, RIL has assumed the NCDs issued by RJIL. The rating continues to factor in the immensely experienced and resourceful promoter group, highly integrated nature of operations with presence across the entire energy value chain, diversified revenue streams, massive scale of downstream business with one of the most complex refineries, established leadership position in the petrochemical segment as well as strong financial risk profile characterized by robust capital structure, stable cash flows and healthy liquidity position. The rating also factors in the increasing wireless subscriber base which has led its digital services business to attain a leadership position in the industry as well as the various steps announced by the management to reduce the debt on a consolidated level. -

Reliance Mart Is One Such Subsidiary

CHAPTER 1 INTRODUCTION The Reliance Group founded by Dhirubhai H.Ambani (1932-2002), is India’s largest private sector enterprise, with businesses in the energy and materials value chain. The company Reliance Industries Limited was co-founded by Dhirubhai Ambani and his brother Champaklal Damani as Reliance Commercial Corporation. In 1965 the partnership was ended and DhiruBhai continued. Reliance was established as a textile concerns in the year 1966. This company followed a diversified a diversification strategy since its inception. It vertically integrated. This resulted in formation of many subsidiaries. Reliance Mart is one such subsidiary. Reliance Mart is a part of the Reliance Industries is actually the largest conglomerate in India. Reliance mart is the subsidiary company of Reliance Industries. Founded in 2006 and based in Mumbai, It is the largest retailer in India in terms of revenue. Its retail outlets offer foods, groceries, apparel and footwear, lifestyle and home improvement products, electronic goods and farm implements and inputs. The company’s outlets also provide vegetables, fruits and flower. It focuses on consumer goods, consumer durables, travel services, energy, entertainment and leisure, and health and well being products, as well as on educational products and services. Backward vertical integration has been the cornerstone of the evolution and growth of Reliance. Starting with textiles in the late seventies, Reliance pursued a strategy of backward vertical integration – in polyester, fibre intermediates, plastics, petrochemicals, petroleum refining and oil and gas exploration and production – to be fully integrated along the materials and energy value chain. The group’s activities span exploration and production of oil and gas, petroleum refining and marketing, petrochemicals (polyester, fibre intermediaries, plastics and chemicals), Textiles, retail and special economic zones. -

Merchants Where Online Debit Card Transactions Can Be Done Using ATM/Debit Card PIN Amazon IRCTC Makemytrip Vodafone Airtel Tata

Merchants where online Debit Card Transactions can be done using ATM/Debit Card PIN Amazon IRCTC Makemytrip Vodafone Airtel Tata Sky Bookmyshow Flipkart Snapdeal icicipruterm Odisha tax Vodafone Bharat Sanchar Nigam Air India Aircel Akbar online Cleartrip Cox and Kings Ezeego one Flipkart Idea cellular MSEDC Ltd M T N L Reliance Tata Docomo Spicejet Airlines Indigo Airlines Adler Tours And Safaris P twentyfourBySevenBooking Abercrombie n Kent India Adani Gas Ltd Aegon Religare Life Insur Apollo General Insurance Aviva Life Insurance Axis Mutual Fund Bajaj Allianz General Ins Bajaj Allianz Life Insura mobik wik Bangalore electricity sup Bharti axa general insura Bharti axa life insurance Bharti axa mutual fund Big tv realiance Croma Birla sunlife mutual fund BNP paribas mutural fund BSES rajdhani power ltd BSES yamuna power ltd Bharat matrimoni Freecharge Hathway private ltd Relinace Citrus payment services l Sistema shyam teleservice Uninor ltd Virgin mobile Chennai metro GSRTC Club mahindra holidays Jet Airways Reliance Mutual Fund India Transact Canara HSBC OBC Life Insu CIGNA TTK Health Insuranc DLF Pramerica Life Insura Edelweiss Tokio Life Insu HDFC General Insurance IDBI Federal Life Insuran IFFCO Tokio General Insur India first life insuranc ING Vysya Life Insurance Kotak Mahindra Old Mutual L and T General Insurance Max Bupa Health Insurance Max Life Insurance PNB Metlife Life Insuranc Reliance Life Insurance Royal Sundaram General In SBI Life Insurance Star Union Daiichi Life TATA AIG general insuranc Universal Sompo General I -

Consolidated Approved Company List

Consolidated approved company list CONSOLIDATED APPROVED COMPANY LIST CONSOLIDATED APPROVED COMPANY NORMS STATE INSTITUTE ACTION UNIQUE COMPANY LIST CATEGORY ID CODE 3M INDIA LIMITED ELITE E00001 ABB INDIA LIMITED ELITE E00519 ACCENTURE SOLUTIONS PRIVATE ELITE EXCEPTION CATEGORY S05819 LIMITED CHANGE ADANI ENTERPRISES LIMITED ELITE E00002 (FORMERLY ADANI EXPORTS LIMITED) ADANI PORTS AND SPECIAL ECONOMIC ELITE E00003 ZONE LIMITED ADITYA BIRLA FINANCE LIMITED ELITE E00006 ADITYA BIRLA FINANCIAL SERVICES ELITE E00007 GROUP ADITYA BIRLA GROUP POWER PROJECTS ELITE E00008 ADITYA PHARMACARE PRIVATE LIMITED ELITE NAME E00011 (formerly ADITYA PHARMA PRIVATE CHANGE LIMITED) AKZO NOBEL INDIA LIMITED ELITE E00013 ALKALOIDA CHEMICAL COMPANY ZRT. ELITE E00014 ALKEM LABORATORIES LIMITED ELITE E00015 ALLAHABAD BANK ELITE E00016 AMARA RAJA BATTERIES LIMITED ELITE E00020 AMAZON DEVELOPMENT CENTRE (INDIA) ELITE CATEGORY S00220 PRIVATE LIMITED CHANGE AMBUJA CEMENTS LIMITED ELITE E00021 AMDOCS DEVELOPMENT CENTER INDIA ELITE CATEGORY S00230 LLP CHANGE AMERICAN EXPRESS(INDIA) PRIVATE ELITE CATEGORY S00236 LIMITED CHANGE ANDHRA BANK ELITE E00022 ANZ OPERATIONS AND TECHNOLOGY ELITE CATEGORY S00280 PRIVATE LIMITED CHANGE APOLLO HOSPITALS ENTERPRISE ELITE E00023 LIMITED CATEGORY S05823 ARVIND LIMITED ELITE CHANGE CATEGORY P01165 ASEA BROWN BOVERI(PABBL) ELITE CHANGE ASHOK LEYLAND LIMITED ELITE E00025 ASIAN PAINTS LIMITED ELITE E00026 ASSOCIATED BUILDING COMPANY ELITE E00027 ASSOCIATED CEMENT COS LIMITED ELITE E00028 (ACC LIMITED) ATOS INDIA PRIVATE LIMITED ELITE -

LYF Smartphone+ Introduces Special Edition LYF F1 – a Device Designed to Deliver Enhanced Experience Over Advanced 4G Network

MEDIA RELEASE LYF Smartphone+ introduces special edition LYF F1 – a device designed to deliver enhanced experience over advanced 4G network Special Edition device features cutting-edge technology that works best with Jio – the world’s largest all-4G network Mumbai, 21st October 2016: Reliance Retail today launched LYF F1, a Special Edition future- ready device from LYF Smartphone+. From introducing VoLTE in smartphones across all price segments to offering advanced features, such as dual camera, smart gestures and voice command controls, LYF continues to spearhead the transition in smartphone technology. With F1, LYF presents a future ready device designed to deliver an enhanced experience over advanced networks. Equipped with carrier aggregation (CA) support, LYF F1 is designed to tap the fullest potential of Jio, the world’s largest all-IP network. The CA technology gives users vastly improved data transfer rates and unmatched browsing experience. This feature is known to boost battery life. Importantly, F1 comes equipped with Rich Communication Services – a set of evolved Messaging services and enriched calling features. The evolved Messaging feature, an enhancement of the existing SMS feature on LTE network, allows group chat, file and location sharing, and much more through the good old SIM-based messaging. Enriched calling lets the user set context to a call by adding location, image, urgency and customised message. Loaded with a 16 MP rear camera, LYF F1 is designed for low-light photography, powered by advanced software technology. Other camera features include a unique multi-focus mode, and electronic image stabilisation that allows steady video recording while in motion. -

Reliance Industries

1 November 2020 2QFY21 Results Update | Sector: Oil & Gas Reliance Industries Estimate change CMP: INR2,054 TP: INR2,240 (+8%) Buy TP change Rating change Consumer biz cushions sharp fall in Oil and Gas biz Reliance Industries (RIL)’s 2QFY21 consolidated/standalone business EBITDA was Bloomberg RIL IN down 14%/44% YoY. This was weighed by sharp decline in refining Equity Shares (m) 6,339 throughput/margin and a weak Retail biz (hurt by the lockdown), but partly offset M.Cap.(INRb)/(USDb) 13524.8 / 180 by the growing Digital business. 52-Week Range (INR) 2369 / 867 RJio’s revenue/EBITDA growth slowed to 6%/7% QoQ (in-line) due to the 1, 6, 12 Rel. Per (%) -12/24/41 combination of 3% ARPU and subscriber growth each, coupled with 60bp margin 12M Avg Val (INR M) 29721 expansion to 42.6%. Reliance Retail’s net revenues were flat YoY at INR366b (in-line). This is Financials & Valuations (INR b) commendable despite the lockdown and lack of footfall at stores in 2QFY21. Y/E March FY21E FY22E FY23E Net Sales 5,438 7,191 7,845 During the quarter, RIL operated its refining and petrochemical units at >90% EBITDA 823 1,217 1,397 despite the much lower utilization rates of its Indian peers – the company is Net Profit 418 677 809 enjoying the benefits of its integrated Oils-to-Chemicals (O2C) business model. Adj. EPS (INR) 64.8 105.1 125.6 Despite a poor SG GRM benchmark, RIL reported a GRM of USD5.7/bbl. RIL EPS Gr. -

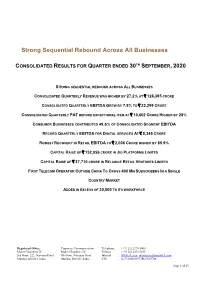

Strong Sequential Rebound Across All Businesses

Strong Sequential Rebound Across All Businesses CONSOLIDATED RESULTS FOR QUARTER ENDED 30TH SEPTEMBER, 2020 STRONG SEQUENTIAL REBOUND ACROSS ALL BUSINESSES CONSOLIDATED QUARTERLY REVENUE WAS HIGHER BY 27.2% AT ` 128,385 CRORE CONSOLIDATED QUARTERLY EBITDA GREW BY 7.9% TO ` 23,299 CRORE CONSOLIDATED QUARTERLY PAT BEFORE EXCEPTIONAL ITEM AT ` 10,602 CRORE HIGHER BY 28% CONSUMER BUSINESSES CONTRIBUTED 49.6% OF CONSOLIDATED SEGMENT EBITDA RECORD QUARTERLY EBITDA FOR DIGITAL SERVICES AT ` 8,345 CRORE ROBUST RECOVERY IN RETAIL EBITDA TO ` 2,006 CRORE HIGHER BY 85.9% CAPITAL RAISE OF ` 152,056 CRORE IN JIO PLATFORMS LIMITED CAPITAL RAISE OF ` 37,710 CRORE IN RELIANCE RETAIL VENTURES LIMITED FIRST TELECOM OPERATOR OUTSIDE CHINA TO CROSS 400 MN SUBSCRIBERS IN A SINGLE COUNTRY MARKET ADDED IN EXCESS OF 30,000 TO ITS WORKFORCE Registered Office: Corporate Communications Telephone : (+91 22) 2278 5000 Maker Chambers IV Maker Chambers IV Telefax : (+91 22) 2278 5185 3rd Floor, 222, Nariman Point 9th Floor, Nariman Point Internet : www.ril.com; [email protected] Mumbai 400 021, India Mumbai 400 021, India CIN : L17110MH1973PLC019786 Page 1 of 19 STRATEGIC UPDATES • Jio Platforms Limited, a wholly owned subsidiary of Reliance Industries Limited, raised ₹ 152,056 crore from leading global investors including Facebook, Google, Silver Lake, Vista Equity Partners, General Atlantic, KKR, Mubadala, ADIA, TPG, L Catterton, PIF, Intel Capital and Qualcomm Ventures. • Reliance Retail Ventures Limited (RRVL), a wholly owned subsidiary of Reliance Industries Limited, raised ` 37,710 crore of investments from leading global investors including Silver Lake, KKR, General Atlantic, Mubadala, GIC, TPG and ADIA. -

Media-Release-JIO-Q1-FY-2018-19

Media Release Mumbai, 27 th July 2018 CROSSED 200 MILLION SUBSCRIBERS WITHIN 21 MONTHS FROM COMMENCEMENT OF SERVICES INDUSTRY LEADING GROWTH IN SUBSCRIBER BASE TO 215.3 MILLION HEALTHY CUSTOMER TRACTION ON POST-PAID OFFERINGS DATA CONSUMPTION AT RECORD 642 CRORE GB IN THE QUARTER; 10.6GB PER USER PER MONTH; GROWING RAPIDLY STRONG FINANCIAL PERFORMANCE DESPITE COMPETITIVE INTENSITY EBITDA GROWTH OF 16.8% QOQ TO ₹3,147 CRORE IN Q1 FY 2018-19 HIGHLIGHTS OF QUARTER ’S (Q1 – FY 2018-19) PERFORMANCE Standalone Financials 1Q’ 18-19 4Q’ 17-18 QoQ Growth (₹ crore) Value of Services 9,567 8,404 13.8% Operating revenue 8,109 7,128 13.8% EBITDA 3,147 2,694 16.8% EBITDA margin 38.8% 37.8% 101bps EBIT 1,708 1,495 14.3% Net Profit 612 510 19.9% Standalone revenue from operations of ₹8,109 crore (13.8% QoQ growth) Standalone EBITDA of ₹3,147 crore (16.8% QoQ growth) and EBITDA margin of 38.8% Standalone Net Profit of ₹612 crore Subscriber base as on 30th June-18 of 215.3 million Lowest churn in the industry at 0.30% per month ARPU during the quarter of ₹134.5/ subscriber per month Total wireless data traffic during the quarter of 642 crore GB Total voice traffic during the quarter of 44,871 crore minutes Registered Office: Corporate Communications Telephone : (+91 22) 6255 5000 Maker Chambers IV Maker Chambers IV Telefax : (+91 22) 6255 5185 9th Floor, 222, Nariman Point 9th Floor, 222, Nariman Point CIN : U72900MH2007PLC234712 Mumbai 400 021, India Mumbai 400 021, India Website : www.jio.com and www.ril.com Page 1 of 7 Media Release Commenting on the results, Shri Mukesh D. -

Indian Premier League and Its Impact on India

www.ijcrt.org © 2020 IJCRT | Volume 8, Issue 4 April 2020 | ISSN: 2320-2882 INDIAN PREMIER LEAGUE AND ITS IMPACT ON INDIA 1Ajinkya Sawant, 2Ajinkya Khadse, 3Akshay Pidurkar, 4Kunal Kshirsagar Students of MBA program Department of Marketing management MIT School of Management, Pune, India 5Priyanka Kokatnur Faculty of MBA program Department of Marketing management MIT School of Management, Pune, India Abstract: This study has been undertaken to know the emergence of Indian Premier League in India. Cricket is the most favorite sport in India and its impact on Indian economy is huge. This paper focuses on the introduction of IPL, types on investment in it, the growth phase, brand crises, economic impact of IPL on different sector in India, contribution to GDP and finally new trends in India because of it. Index Terms – Indian Premier League (IPL), Cricket, Twenty20, ICC. 1. INTRODUCTION The history of cricket in India is very old. The first ever cricket match played in India was in 1864 between Madras and Calcutta. Britishers (East India company) introduced cricket in India. And as the time passes it became the most popular sport in India. People celebrate cricket as a festival and treat the players like God. The moment when it became popular in India. 1983 “World Cup” where India defeated two-time world cup holder team West Indies in final and claim the title. Kapil Dev was the captain of Indian team. 2007 “T-twenty World Cup” where India defeated Pakistan and won first ever T-twenty world cup. M.S.Dhoni was leading the team. 2011 “World Cup” where India defeated Sri Lanka and won Second world cup for India.