Reliance Industries Limited: Ratings Reaffirmed

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

RELIANCE BRANDS Limited 1

RELIANCE BRANDS LIMITED 1 Reliance Brands Limited Financial Statements 2019-20 2 RELIANCE BRANDS LIMITED Independent Auditor’s Report To The Members of Reliance Brands Limited Report on the Audit of the Financial Statements Opinion We have audited the Financial Statements of Reliance Brands Limited (“the Company”), which comprise the Balance Sheet as at 31st March 2020, the Statement of profit and loss, Statement of changes in equity and Statement of Cash Flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies and other explanatory information (hereinafter referred to as “ Financial Statements”). In our opinion and to the best of our information and according to the explanations given to us, the aforesaid financial statements give the information required by the Companies Act, 2013 (“the Act”) in the manner so required and give a true and fair view in conformity with the accounting principles generally accepted in India, of the state of affairs of the Company as at March 31, 2020, and its Loss including Other Comprehensive Income, changes in equity and its cash flows for the year ended on that date. Basis for Opinion We conducted our audit in accordance with the Standards on Auditing specified under section 143(10) of the Act. Our responsibilities under those Standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Company in accordance with the Code of Ethics issued by the Institute of Chartered Accountants of India together with the ethical requirements that are relevant to our audit of the Financial Statements under the provisions of the Act and the Rules thereunder, and we have fulfilled our other ethical responsibilities in accordance with these requirements and the Code of Ethics. -

18 December 2020 Reliance and Bp Announce First Gas from Asia's

18 December 2020 Reliance and bp announce first gas from Asia’s deepest project • Commissioned India's first ultra-deepwater gas project • First in trio of projects that is expected to meet ~15% of India’s gas demand and account for ~25% of domestic production Reliance Industries Limited (RIL) and bp today announced the start of production from the R Cluster, ultra-deep-water gas field in block KG D6 off the east coast of India. RIL and bp are developing three deepwater gas projects in block KG D6 – R Cluster, Satellites Cluster and MJ – which together are expected to meet ~15% of India’s gas demand by 2023. These projects will utilise the existing hub infrastructure in KG D6 block. RIL is the operator of KG D6 with a 66.67% participating interest and bp holds a 33.33% participating interest. R Cluster is the first of the three projects to come onstream. The field is located about 60 kilometers from the existing KG D6 Control & Riser Platform (CRP) off the Kakinada coast and comprises a subsea production system tied back to CRP via a subsea pipeline. Located at a water depth of greater than 2000 meters, it is the deepest offshore gas field in Asia. The field is expected to reach plateau gas production of about 12.9 million standard cubic meters per day (mmscmd) in 2021. Mukesh Ambani, chairman and managing director of Reliance Industries Limited added: “We are proud of our partnership with bp that combines our expertise in commissioning gas projects expeditiously, under some of the most challenging geographical and weather conditions. -

Factsheetmarch11

March 2011 EQUITY OUTLOOK The Indian benchmark indices ended FII Equity Flows: Turn Buyers for First Time in 2011 March on a positive note after being 7,000 Cash (US$m) 6,373 6,000 Futures (US$m) 5,580 down ~13% between January and 5,000 3,777 4,159 February 2011. The benchmark gained 4,000 3,000 2,405 Gaurav Kapur 2,220 1,556 2,100 1,740 SENIOR MANAGER - EQUITY about 5.6% during March 2011, 2,000 1,358 1,299 1,000 406 329 making it the second best performing 231 0 -1,000 -529 -363 market in the world for the month. The CNX midcap index also was -737 -993 -826 -2,000 -1,016 -1,257 -1,989 -1,387 up 5.8% over the same period. FIIs were net buyers of ~US$1.5 bn -3,000 -4,000 -3,417 during March, however, they are still net sellers worth around 1 1 1 0 0 0 0 0 0 0 0 0 1 1 1 1 1 1 1 1 1 1 1 1 - - - - - - - - - - - - r l t r b n y v c n g p a c u p e a a o e US$650 mn year-to-date. u u e J J M F O A J N D A S M Source: Morgan Stanley Research Asia was the best performing Emerging Markets region in March, rising by 7.1%, while Emerging Markets Ex Asia (+4.7%), despite underperforming, remained resilient in the face of the ongoing political turmoil in the neighboring Middle East North Africa (MENA) region and the rumbling sovereign debt crisis in Europe. -

Press Release Reliance Industries Limited

Press Release Reliance Industries LImited March 30, 2020 Ratings Amount Facilities Rating1 Rating Action (Rs. crore) CARE AAA; Non-Convertible Debentures 10,386 Stable(Triple A; Assigned Outlook: Stable) Details of instruments/facilities in Annexure-1 Other Ratings Instruments Amount (Rs.Crore) Ratings Non-Convertible Debenture 40,000 CARE AAA; Stable Commercial Paper 34,500 CARE A1+ Detailed Rationale& Key Rating Drivers On March 18, 2020, the company announced that the Hon’ble National Company Law Tribunal (NCLT), Ahmedabad Bench has approved the Scheme, for transfer of certain identified liabilities from Reliance Jio Infocomm Limited (RJIL; rated CARE AAA; Stable/ CARE A1+, CARE AAA (CE); Stable) to Reliance Industries Limited (RIL). Pursuant to the Scheme of Arrangement amongst RJIL and certain classes of its creditors (the “Scheme”) as sanctioned by the Hon’ble National Company Law Tribunal, Ahmedabad Bench, vide its order dated March 13, 2020, RIL has assumed the NCDs issued by RJIL. The rating continues to factor in the immensely experienced and resourceful promoter group, highly integrated nature of operations with presence across the entire energy value chain, diversified revenue streams, massive scale of downstream business with one of the most complex refineries, established leadership position in the petrochemical segment as well as strong financial risk profile characterized by robust capital structure, stable cash flows and healthy liquidity position. The rating also factors in the increasing wireless subscriber base which has led its digital services business to attain a leadership position in the industry as well as the various steps announced by the management to reduce the debt on a consolidated level. -

Admission Brochure 2021-22

An Institution of National Importance by an Act of Parliament ADMISSION BROCHURE 2021-22 Est. in 2016 by Ministry of Education (Formerly Ministry of Human Resource Development) Government of India INDIAN INSTITUTE OF INFORMATION TECHNOLOGY, NAGPUR (IIITN) is one of the 20 Indian Institutes of Information Technology established under Public-Private Partnership Scheme by Ministry of Human Resource Development, Government of India. IIITN has been declared as an “Institution of National Importance” under the provisions of Indian Institute of Information Technology (Public-Private Partnership) Act, 2017. The Institute started functioning during the year 2016-17 and operating from its permanent campus in Nagpur under the aegis of Department of Higher Education, Ministry of Education and is supported by Department of Higher Education, Government of Maharashtra and Tata Consultancy Services, Mumbai as Industry Partner. Institute’s Mandate One of the main objectives of the Institute is to develop competent and capable youth imbued with the spirit of innovation and entrepreneurship with the social and environmental orientation to meet the knowledge needs of the country and provide Global Leadership in Information Technology & Allied Fields. Institute’s Vision The Institute aspires to attain the status of a top-notch Institution in Information Technology and Allied Fields and to emerge as an elite Research Institution by imparting futuristic quality education of Global Standards to corroborate the status of an “Institution of National Importance”. Institute’s Mission To undertake socially relevant, industry oriented In-House Research & Development Programmes as well as to undertake cutting-age research through Public-Private Participation in Information Technology & Allied Fields. -

Tpg to Invest ₹ 4,546.80 Crore in Jio Platforms Tpg's Deep

TPG TO INVEST ₹ 4,546.80 CRORE IN JIO PLATFORMS TPG’S DEEP CAPABILITIES IN TECH INVESTING TO SUPPORT JIO’S INITIATIVES TOWARDS DEVELOPING THE DIGITAL SOCIETY JIO PLATFORMS FUND RAISING FROM MARQUEE GLOBAL TECHNOLOGY INVESTORS CROSSES ₹ 1 LAKH CRORE Mumbai, June 13, 2020: Reliance Industries Limited (“Reliance Industries”) and Jio Platforms Limited (“Jio Platforms”), India’s leading digital services platform, announced today that global alternative asset firm TPG will invest ₹ 4,546.80 crore in Jio Platforms at an equity value of ₹ 4.91 lakh crore and an enterprise value of ₹ 5.16 lakh crore. The investment will translate into a 0.93% equity stake in Jio Platforms on a fully diluted basis for TPG. With this investment, Jio Platforms has raised ₹ 102,432.45 crore from leading global technology investors including Facebook, Silver Lake, Vista Equity Partners, General Atlantic, KKR, Mubadala, ADIA, and TPG since April 22, 2020. Jio Platforms, a wholly-owned subsidiary of Reliance Industries, is a next-generation technology platform focused on providing high-quality and affordable digital services across India, with more than 388 million subscribers. Jio Platforms has made significant investments across its digital ecosystem, powered by leading technologies spanning broadband connectivity, smart devices, cloud and edge computing, big data analytics, artificial intelligence, Internet of Things, augmented and mixed reality and blockchain. Jio Platforms’ vision is to enable a Digital India for 1.3 billion people and businesses across the country, including small merchants, micro-businesses and farmers so that all of them can enjoy the fruits of inclusive growth. TPG is a leading global alternative asset firm founded in 1992 with more than $79 billion of assets under management across a wide range of asset classes, including private equity, growth equity, real estate and public equity. -

February 17, 2020

February 17, 2020 The Manager, Listing Department The General Manager The National Stock Exchange of India Ltd. The Bombay Stock Exchange Limited Exchange Plaza Listing Department Bandra Kurla Complex 15th Floor, P J Towers Bandra (E) Mumbai-400 051 Dalal Street, Mumbai-400 001 NSE Trading Symbol- DEN BSE Scrip Code- 533137 Dear Sirs, Sub.: Media Release titled “Scheme of Amalgamation and Arrangement amongst Network18, TV18, Den & Hathway” Dear Sirs, Attached is the Media Release being issued by the Company titled “Scheme of amalgamation and Arrangement amongst Network18, TV18, Den & Hathway”. You are requested to take the above on record. Thanking You, FCS No. :6887 MEDIA RELEASE Scheme of Amalgamation and Arrangement amongst Network18, TV18, Den & Hathway Consolidates media and distribution businesses of Reliance Creates Media & Distribution platform comparable with global standards of reach, scale and integration News Broadcasting business of TV18 to be housed in Network18 Cable and Broadband businesses of Den and Hathway to be housed in two separate wholly-owned subsidiaries of Network18 February 17, 2020: Reliance Industries (NSE: RELIANCE) announced a consolidation of its media and distribution businesses spread across multiple entities into Network18. Under the Scheme of Arrangement, TV18 Broadcast (NSE: TV18), Hathway Cable & Datacom (NSE: HATHWAY) and Den Networks (NSE: DEN) will merge into Network18 Media & Investments (NSE: NETWORK18). The Appointed Date for the merger shall be February 1, 2020. The Board of Directors of the respective companies approved the Scheme of Amalgamation and Arrangement at their meetings held today. The broadcasting business will be housed in Network18 and the cable and ISP businesses in two separate wholly owned subsidiaries of Network18. -

Jio Platforms Limited 1

JIO PLATFORMS LIMITED 1 Jio Platforms Limited Financial Statements 2020-21 2 JIO PLATFORMS LIMITED INDEPENDENT AUDITORS’ REPORT To The Members of Jio Platforms Limited Report on the Audit of the Standalone Financial Statements Opinion We have audited the accompanying standalone financial statements of Jio Platforms Limited (“the Company”), which comprise the Balance Sheet as at 31st March, 2021 the Statement of Profit and Loss including Other Comprehensive Income, the Statement of Changes in Equity and the Statement of Cash Flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies and other explanatory information (hereinafter referred to as “standalone financial statements”). In our opinion and to the best of our information and according to the explanations given to us, the aforesaid standalone financial statements give the information required by the Companies Act, 2013 (“the Act”) in the manner so required and give a true and fair view in conformity with the accounting principles generally accepted in India, of the state of affairs of the Company as at 31st March, 2021, its profit including total comprehensive income, the statement of changes in equity and its cash flows for the year ended on that date. Basis for Opinion We conducted our audit in accordance with the Standards on Auditing (SAs) specified under section 143(10) of the Act. Our responsibilities under those Standards are further described in the Auditor’s Responsibility for the Audit of the Standalone Financial Statements section of our report. We are independent of the Company in accordance with the Code of Ethics issued by the Institute of Chartered Accountants of India (ICAI) together with the ethical requirements that are relevant to our audit of the standalone financial statements under the provisions of the Act and the Rules made thereunder, and we have fulfilled our other ethical responsibilities in accordance with these requirements and the ICAI’s Code of Ethics. -

Project Reliable

Good morning jury members and members of the audience. During this presentation we will present a process improvement project & share with you our learning's and experiences and how we have increased (i)Liquid Hydrocarbon Production of GAIL Gandhar, (ii) High Pressure Gas (HP) Gas quantity from ONGC Gandhar, (iii) Net Profit of GAIL Gandhar by suppling SRG to Gas Gathering Station-IV ONGC Gandhar Using Lean Gas Line of Reliance Industries Limited by using a structured DMAIC methodology. 1 We(GAIL) are in presence of these Business Vertices. 2 There are 5 subsidiary and 18 joint ventures of GAIL. 3 Process flow diagram of GAIL Gas Processing Unit Gandhar, Which is situated at Bharuch District of Gujarat. Which are associated with Oil and natural gas corporation (ONGC), Gujarat Narmada Valley Fertilizer Limited (GNFC), Gas Gathering Station No- 4 (GGS-IV M/s ONGC ), National Thermal Power Corporation Limited (NTPC), Reliance Industries Limited Dahej as upstream source and down stream consumers. 4 Steps followed in this project listed here 5 In Project background for identification, planning and prioritization of problems done in this step. 6 In This step GAIL shows our project planning and identification of opportunity area to increase our turnover. 7 These the mode of suggestions, ideas, problems identification are welcome either through online portal or offline portal are listed here. 8 Here we have shown how idea’s are generated or problem are listed through brainstorming and SAP for identification of problem. 9 In GAIL gandhar we have characterized our process area in A,B,C,D,E class for stratification of problem’s. -

LYF Smartphone+ Introduces Special Edition LYF F1 – a Device Designed to Deliver Enhanced Experience Over Advanced 4G Network

MEDIA RELEASE LYF Smartphone+ introduces special edition LYF F1 – a device designed to deliver enhanced experience over advanced 4G network Special Edition device features cutting-edge technology that works best with Jio – the world’s largest all-4G network Mumbai, 21st October 2016: Reliance Retail today launched LYF F1, a Special Edition future- ready device from LYF Smartphone+. From introducing VoLTE in smartphones across all price segments to offering advanced features, such as dual camera, smart gestures and voice command controls, LYF continues to spearhead the transition in smartphone technology. With F1, LYF presents a future ready device designed to deliver an enhanced experience over advanced networks. Equipped with carrier aggregation (CA) support, LYF F1 is designed to tap the fullest potential of Jio, the world’s largest all-IP network. The CA technology gives users vastly improved data transfer rates and unmatched browsing experience. This feature is known to boost battery life. Importantly, F1 comes equipped with Rich Communication Services – a set of evolved Messaging services and enriched calling features. The evolved Messaging feature, an enhancement of the existing SMS feature on LTE network, allows group chat, file and location sharing, and much more through the good old SIM-based messaging. Enriched calling lets the user set context to a call by adding location, image, urgency and customised message. Loaded with a 16 MP rear camera, LYF F1 is designed for low-light photography, powered by advanced software technology. Other camera features include a unique multi-focus mode, and electronic image stabilisation that allows steady video recording while in motion. -

Reliance Industries

1 November 2020 2QFY21 Results Update | Sector: Oil & Gas Reliance Industries Estimate change CMP: INR2,054 TP: INR2,240 (+8%) Buy TP change Rating change Consumer biz cushions sharp fall in Oil and Gas biz Reliance Industries (RIL)’s 2QFY21 consolidated/standalone business EBITDA was Bloomberg RIL IN down 14%/44% YoY. This was weighed by sharp decline in refining Equity Shares (m) 6,339 throughput/margin and a weak Retail biz (hurt by the lockdown), but partly offset M.Cap.(INRb)/(USDb) 13524.8 / 180 by the growing Digital business. 52-Week Range (INR) 2369 / 867 RJio’s revenue/EBITDA growth slowed to 6%/7% QoQ (in-line) due to the 1, 6, 12 Rel. Per (%) -12/24/41 combination of 3% ARPU and subscriber growth each, coupled with 60bp margin 12M Avg Val (INR M) 29721 expansion to 42.6%. Reliance Retail’s net revenues were flat YoY at INR366b (in-line). This is Financials & Valuations (INR b) commendable despite the lockdown and lack of footfall at stores in 2QFY21. Y/E March FY21E FY22E FY23E Net Sales 5,438 7,191 7,845 During the quarter, RIL operated its refining and petrochemical units at >90% EBITDA 823 1,217 1,397 despite the much lower utilization rates of its Indian peers – the company is Net Profit 418 677 809 enjoying the benefits of its integrated Oils-to-Chemicals (O2C) business model. Adj. EPS (INR) 64.8 105.1 125.6 Despite a poor SG GRM benchmark, RIL reported a GRM of USD5.7/bbl. RIL EPS Gr. -

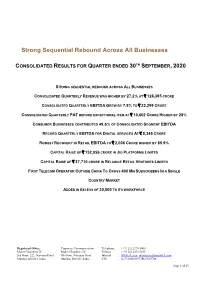

Strong Sequential Rebound Across All Businesses

Strong Sequential Rebound Across All Businesses CONSOLIDATED RESULTS FOR QUARTER ENDED 30TH SEPTEMBER, 2020 STRONG SEQUENTIAL REBOUND ACROSS ALL BUSINESSES CONSOLIDATED QUARTERLY REVENUE WAS HIGHER BY 27.2% AT ` 128,385 CRORE CONSOLIDATED QUARTERLY EBITDA GREW BY 7.9% TO ` 23,299 CRORE CONSOLIDATED QUARTERLY PAT BEFORE EXCEPTIONAL ITEM AT ` 10,602 CRORE HIGHER BY 28% CONSUMER BUSINESSES CONTRIBUTED 49.6% OF CONSOLIDATED SEGMENT EBITDA RECORD QUARTERLY EBITDA FOR DIGITAL SERVICES AT ` 8,345 CRORE ROBUST RECOVERY IN RETAIL EBITDA TO ` 2,006 CRORE HIGHER BY 85.9% CAPITAL RAISE OF ` 152,056 CRORE IN JIO PLATFORMS LIMITED CAPITAL RAISE OF ` 37,710 CRORE IN RELIANCE RETAIL VENTURES LIMITED FIRST TELECOM OPERATOR OUTSIDE CHINA TO CROSS 400 MN SUBSCRIBERS IN A SINGLE COUNTRY MARKET ADDED IN EXCESS OF 30,000 TO ITS WORKFORCE Registered Office: Corporate Communications Telephone : (+91 22) 2278 5000 Maker Chambers IV Maker Chambers IV Telefax : (+91 22) 2278 5185 3rd Floor, 222, Nariman Point 9th Floor, Nariman Point Internet : www.ril.com; [email protected] Mumbai 400 021, India Mumbai 400 021, India CIN : L17110MH1973PLC019786 Page 1 of 19 STRATEGIC UPDATES • Jio Platforms Limited, a wholly owned subsidiary of Reliance Industries Limited, raised ₹ 152,056 crore from leading global investors including Facebook, Google, Silver Lake, Vista Equity Partners, General Atlantic, KKR, Mubadala, ADIA, TPG, L Catterton, PIF, Intel Capital and Qualcomm Ventures. • Reliance Retail Ventures Limited (RRVL), a wholly owned subsidiary of Reliance Industries Limited, raised ` 37,710 crore of investments from leading global investors including Silver Lake, KKR, General Atlantic, Mubadala, GIC, TPG and ADIA.