Sports Newsletter

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

High School Leaflet

Equipment HIRE: £60 per term OR £150 per year for a set of two posts. KORFBALL (suitable for 16 children to play at the same time). OR £250 for 2 sets per year. £100 for one term. IN YOUR (suitable for a whole class of 32 children on two courts) BUY BACK SCHEME: HIGH CHOOL S If you take part in this Club School Link, Harrow Korfball will reduce the cost of purchase from £780 to £580 per set of posts. AND If you no longer want them, we will buy back the posts in the first year at 100% (£580). This reduces to 60% in year 2. The posts come with a 10 year warrantee. All prices include deliv- ery. KORFBALLS (size 4 or 5) cost £29 per ball when ordered at the same time through Harrow Korfball. We suggest ordering a mini- mum of 4. There is no buy back on balls. Also available is a ‘Teaching Children Korfball’ Manual at £25 which includes 10 lesson plans. The aim We are looking for schools to introduce this fantastic international sport and establish a long term link with your local club. We will give you as much support as possible and look forward to working with you for a new generation of athletes from our boroughs. We will invite you to tournaments and help set up a community club if you want. We have the opportunity to set this generation on the path to representing GB at the 2028 Olympics. Email: [email protected] www.harrowkorfball.com WHAT IS KORFBALL? WHAT WE CAN DO FOR YOU Korfball is the only team sport designed to be mixed, Create a link with Harrow Korfball, a Change4Life sport and it works. -

UNO Template

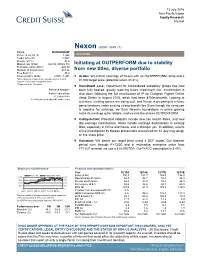

13 July 2016 Asia Pacific/Japan Equity Research Internet Nexon (3659 / 3659 JT) Rating OUTPERFORM* Price (12 Jul 16, ¥) 1,444 INITIATION Target price (¥) 1,900¹ Chg to TP (%) 31.6 Market cap. (¥ bn) 629.93 (US$ 6.10) Initiating at OUTPERFORM due to stability Enterprise value (¥ bn) 440.12 Number of shares (mn) 436.24 from new titles, diverse portfolio Free float (%) 35.0 52-week price range 2,065 - 1,401 ■ Action: We initiate coverage of Nexon with an OUTPERFORM rating and a *Stock ratings are relative to the coverage universe in each ¥1,900 target price (potential return 31.6%). analyst's or each team's respective sector. ¹Target price is for 12 months. ■ Investment case: Impairment for consolidated subsidiary gloops has now Research Analysts been fully booked, greatly reducing future impairment risk. Amortization is Keiichi Yoneshima also down following the full amortization of IP for Dungeon Fighter Online 81 3 4550 9740 (Arad Senki) in August 2015, which had been ¥700mn/month. Looking at [email protected] revenues, existing games are doing well, and Nexon is preparing to release game iterations under existing strong brand titles. Even though the rising yen is negative for earnings, we think Nexon’s foundations in online gaming make its earnings quite reliable, and we rate the shares OUTPERFORM. ■ Catalysts/risk: Potential catalysts include new title launch dates, and new title earnings contributions. Risks include earnings deterioration in existing titles, especially in China and Korea, and a stronger yen. In addition, results of the investigation by Korean prosecutors announced on 12 July may weigh on the share price. -

2017 Anti-Doping Testing Figures Report

2017 Anti‐Doping Testing Figures Please click on the sub‐report title to access it directly. To print, please insert the pages indicated below. Executive Summary – pp. 2‐9 (7 pages) Laboratory Report – pp. 10‐36 (26 pages) Sport Report – pp. 37‐158 (121 pages) Testing Authority Report – pp. 159‐298 (139 pages) ABP Report‐Blood Analysis – pp. 299‐336 (37 pages) ____________________________________________________________________________________ 2017 Anti‐Doping Testing Figures Executive Summary ____________________________________________________________________________________ 2017 Anti-Doping Testing Figures Samples Analyzed and Reported by Accredited Laboratories in ADAMS EXECUTIVE SUMMARY This Executive Summary is intended to assist stakeholders in navigating the data outlined within the 2017 Anti -Doping Testing Figures Report (2017 Report) and to highlight overall trends. The 2017 Report summarizes the results of all the samples WADA-accredited laboratories analyzed and reported into WADA’s Anti-Doping Administration and Management System (ADAMS) in 2017. This is the third set of global testing results since the revised World Anti-Doping Code (Code) came into effect in January 2015. The 2017 Report – which includes this Executive Summary and sub-reports by Laboratory , Sport, Testing Authority (TA) and Athlete Biological Passport (ABP) Blood Analysis – includes in- and out-of-competition urine samples; blood and ABP blood data; and, the resulting Adverse Analytical Findings (AAFs) and Atypical Findings (ATFs). REPORT HIGHLIGHTS • A analyzed: 300,565 in 2016 to 322,050 in 2017. 7.1 % increase in the overall number of samples • A de crease in the number of AAFs: 1.60% in 2016 (4,822 AAFs from 300,565 samples) to 1.43% in 2017 (4,596 AAFs from 322,050 samples). -

TDSSA Appendix 1

Appendix 1 Minimum Levels of Analysis for Sports and Disciplines of Olympic and IOC Recognized International Federations, and members of the Alliance of Independent Recognized Members of Sport 4 4 SPORT DISCIPLINE ESAs % GHs % GHRFs % Aikido Aikido 5 5 5 Air Sports All 0 0 0 American Football American Football 5 10 10 Aquatics Diving 0 5 5 Aquatics Swimming Sprint 100m or less 10 10 10 Aquatics Swimming Long Distance 800m or greater 30 5 5 Aquatics Swimming Middle Distance 200‐400m 15 5 5 Aquatics Open Water 30 5 5 Aquatics Synchronized Swimming 10 5 5 Aquatics Water Polo 10 10 10 Archery All 0 0 0 Athletics Combined Events 15 15 15 Athletics Jumps 10 15 15 Athletics Long Distance 3000m or greater 60 5 5 Athletics Middle Distance 800‐1500m 30 10 10 Athletics Sprint 400m or less 10 15 15 Athletics Throws 5 15 15 Automobile Sports All 5 0 0 Badminton Badminton 10 10 10 Bandy Bandy 5 10 10 Baseball Baseball 5 10 10 Basketball Basketball 10 10 10 Basketball 3 on 3 10 10 10 Basque Pelota Basque Pelota 5 5 5 Biathlon Biathlon 60 10 10 Billiards Sports All 0 0 0 Bobsleigh Bobsleigh 5 10 10 Bobsleigh Skeleton 0 10 10 Bodybuilding Bodybuilding 5 30 30 Bodybuilding Fitness 10 30 30 Boules Sports All 0 0 0 Bowling All 0 0 0 Boxing Boxing 15 10 10 Bridge Bridge 0 0 0 4 Compliance with the GHRFs MLAs and GH MLAs will be mandatory from 1 January 2017 and 1 January 2018 respectively. -

EA SPORTSTM FIFA Online 3 M Tops 3 Million Downloads in Korea

June 20, 2014 EA SPORTSTM FIFA Online 3 M Tops 3 Million Downloads in Korea Mobile app fully synced with PC-based FIFA Online 3 continues to gain popularity TOKYO – June 20, 2014 – NEXON Co., Ltd. (“Nexon”) (3659.TO), a worldwide leader in free- to-play online games, today announced that EA SPORTSTM FIFA Online 3 M, developed by EA Seoul Studio (Electronic Arts Seoul Studio LLC) and published by Nexon’s wholly-owned subsidiary, NEXON Korea Corporation, surpassed 3 million downloads in Korea on June 17th. FIFA Online 3 M is the latest instalment of the world’s bestselling sports videogame franchise, EA SPORTSTM FIFA. FIFA Online 3 M was launched on March 27, 2014 on the Naver App Store and later launched on Google Play on May 29th. Fully synced with its PC counterpart, FIFA Online 3 M offers players functional team management in a high-quality graphic mobile environment using team and player data, in- game points and other data saved on players’ PC game version. The game also features exclusive mobile-only content to further enhance players’ mobile experience. EA SPORTSTM FIFA Online 3 M EA SPORTS and the EA SPORTS logo are trademarks of Electronic Arts Inc. Official FIFA licensed product. © The FIFA name and OLP Logo are copyright or trademark protected by FIFA. All rights reserved. Manufactured under license by Electronic Arts Inc. The use of real player names and likenesses is authorized by FIFPro Commercial Enterprises BV. About NEXON Co., Ltd. http://company.nexon.co.jp/ NEXON Co., Ltd. (“Nexon”) (3659.TO) is a worldwide leader in free-to-play online games. -

EA SPORTS FIFA Online 3 Comes to China

July 24, 2013 EA SPORTS FIFA Online 3 Comes to China Tencent Games and EA Announce Publishing Agreement SHANGHAI--(BUSINESS WIRE)-- EA SPORTS™FIFA Online 3, the new PC online soccer game from the world's most popular sports videogame franchise, is coming to Chinese gamers and soccer fans. Tencent Games, under Tencent Group as the leading internet service provider in China, and Electronic Arts Inc. (NASDAQ: EA), a global leader in digital interactive entertainment, today announced an agreement through which FIFA Online 3 will be published in mainland China by Tencent Games. The first testing is expected to begin in the fourth quarter of calendar 2013. FIFA Online 3, with the exclusive license from FIFA, delivers the best technologies and all the realism and authenticity of the world's best-selling sports game franchise from EA. Players will experience improved gameplay and strategies, enhanced graphics, the latest rosters, and extensive use of official licenses, including close to 15,000 real world players from 30 leagues and 40 national teams. The game adds new techniques and features, improved artificial intelligence, enhanced animation and dynamic 5-on-5 multiplayer competition. The game is developed by EA Seoul Studio. EA SPORTS FIFA Online 3 holds the number 2 spot in Korean PC café rankings according to Gametrics. The game will also operate in Thailand and Vietnam. Steven Ma, Vice President of Tencent, said, "Tencent Games' agreement with EA is a cooperation between the leading online game company in China and the world's top sports game developer and franchise. The launch of FIFA Online 3 will provide strong momentum for the development of e-sports in China and create a true ‘virtual world of sports' for all Chinese users." Steven Ma also said, "The partnership with EA is an important milestone in Tencent Games' strategy of internationalization. -

ELECTRONIC ARTS INC. (Exact Name of Registrant As Specified in Its Charter)

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q þ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Quarterly Period Ended September 30, 2018 OR ¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Transition Period from to Commission File No. 000-17948 ELECTRONIC ARTS INC. (Exact name of registrant as specified in its charter) Delaware 94-2838567 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 209 Redwood Shores Parkway Redwood City, California 94065 (Address of principal executive offices) (Zip Code) (650) 628-1500 (Registrant’s telephone number, including area code) Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES þ NO ¨ Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). YES þ NO ¨ Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. -

ELECTRONIC ARTS Q3 FY14 PREPARED COMMENTS January 28, 2014

ELECTRONIC ARTS Q3 FY14 PREPARED COMMENTS January 28, 2014 ROB: Thank you. Welcome to EA’s fiscal 2014 third quarter earnings call. With me on the call today are Andrew Wilson, our CEO, and Blake Jorgensen, our CFO. Peter Moore, our COO, and Patrick Söderlund, our EVP of EA Studios, will be joining us for the Q&A portion of the call. Please note that our SEC filings and our earnings release are available at ir.ea.com. In addition, we have posted earnings slides to accompany our prepared remarks. Lastly, after the call, we will post our prepared remarks, an audio replay of this call, and a transcript. This presentation and our comments include forward-looking statements regarding future events and the future financial performance of the Company. Actual events and results may differ materially from our expectations. We refer you to our most recent Form 10-Q for a discussion of risks that could cause actual results to differ materially from those discussed today. Electronic Arts makes these statements as of January 28, 2014 and disclaims any duty to update them. During this call unless otherwise stated, the financial metrics will be presented on a non-GAAP basis. Our earnings release and the earnings slides provide a reconciliation of our GAAP to non-GAAP measures. These non-GAAP measures are not intended to be considered in isolation from, as a substitute for, or superior to our GAAP results. We encourage investors to consider all measures before making an investment decision. All comparisons made in the course of this call are against the same period in the prior year unless otherwise stated. -

Sporting Activities and Governing Bodies Recognised by the Sports Councils

MASTER LIST – updated January 2016 Sporting Activities and Governing Bodies Recognised by the Sports Councils Notes: 1. Sporting activities with integrated disability in red 2. Sporting activities with no governing body in blue ACTIVITY DISCIPLINES NORTHERN IRELAND SCOTLAND ENGLAND WALES UK/GB AIKIDO Northern Ireland Aikido Association British Aikido Board British Aikido Board British Aikido Board British Aikido Board AIR SPORTS Flying Ulster Flying Club Royal Aero Club of the UK Royal Aero Club of the UK Royal Aero Club of the UK Royal Aero Club of the UK Aerobatic flying British Aerobatic Association British Aerobatic Association British Aerobatic Association British Aerobatic Association British Aerobatic Association Royal Aero Club of UK Aero model Flying NI Association of Aeromodellers Scottish Aeromodelling Association British Model Flying Association British Model Flying Association British Model Flying Association Ballooning British Balloon and Airship Club British Balloon and Airship Club British Balloon and Airship Club British Balloon and Airship Club Gliding Ulster Gliding Club British Gliding Association British Gliding Association British Gliding Association British Gliding Association Hang/ Ulster Hang Gliding and Paragliding Club Scottish Hang Gliding and Paragliding British Hang Gliding and Paragliding British Hang Gliding and Paragliding British Hang Gliding and Paragliding Paragliding Association Association Association Association Microlight British Microlight Aircraft Association British Microlight Aircraft Association -

List of Acronyms in the Anti-Doping Movement

ADOKICKSTART LIST OF ACRONYMS IN THE ANTI-DOPING MOVEMENT LIST OF ACRONYMS IN THE ANTI-DOPING MOVEMENT A AAF Adverse Analytical Finding ABCD Brazilian Anti-Doping Agency ABP Athlete Biological Passport ABPS Abnormal Blood Profile Score (ABPS) AD Anti-Doping ADAMS Anti-Doping Administration and Management System ADAMAS Anti-Doping Agency of Malaysia ADAS Anti-Doping Agency of Serbia ADD Anti-Doping Denmark ADN Anti-Doping Norway AD Anti-Doping Organisation/Organization ADOP Anti-Doping Authority Portugal ADOP Anti-Doping Organisation of Pakistan ADRs Anti-Doping Rules ADRQ Anti-Doping Results Questionnaire ADRV Anti-Doping Rules Violation AEA Spanish National Anti-Doping Agency AEP Athlete Endocrinological Passport AFLD French Agency for the Fight Against Doping AGM Annual General Meeting AHP Athlete Hematological Passport AIBA International Boxing Association AIMS Alliance of Independent Recognised Members of Sport AIOWF Association of International Olympic Winter Sports Federations ALAD Luxembourg Agency for the Fight Against Doping APF Adverse Passport Finding APMU Athlete Passport Management Unit ARISF Association of IOC Recognized International Sports Federations ASADA Australian Sports Anti-Doping Authority ASOIF Association of Summer Olympic International Federations 01 January 2019 1 Version 5.0 ADOKICKSTART LIST OF ACRONYMS IN THE ANTI-DOPING MOVEMENT ASP Athlete Steroidal Passport ATF Atypical Finding ATPF Atypical Passport Finding APF Adverse Passport Finding AZADA Azerbaijan Anti-Doping Organisation B BADC Bahamas Anti-Doping -

Electronic Arts Reports Q2 Fy11 Financial Results

ELECTRONIC ARTS REPORTS Q2 FY11 FINANCIAL RESULTS Reports Q2 Non-GAAP Revenue and EPS Ahead of Expectations Reaffirms Full-Year Non-GAAP EPS and Net Revenue Guidance FIFA 11 Scores With 8.0 Million Units Sold In Need For Speed Hot Pursuit with Autolog, Ships November 16 REDWOOD CITY, CA – November 2, 2010 – Electronic Arts Inc. (NASDAQ: ERTS) today announced preliminary financial results for its second fiscal quarter ended September 30, 2010. “We had another strong quarter, beating expectations both top and bottom line,” said John Riccitiello, Chief Executive Officer. “We credit our results to blockbusters like FIFA 11 and to innovative digital offerings like The Sims 3 Ambitions and Madden NFL 11 on the iPad.” “EA reaffirms its FY11 non-GAAP guidance,” said Eric Brown, Chief Financial Officer. “EA is the world’s #1 publisher calendar year-to-date and our portfolio is focused on high- growth platforms -- high definition consoles, PC, and mobile.” Selected Quarterly Operating Highlights and Metrics: EA is the #1 publisher on high-definition consoles with 25% segment share calendar year-to date, two points higher than the same period a year ago. In North America and Europe, the high-definition console software market is growing strongly with the combined PlayStation®3 and Xbox 360® segments up 23% calendar year-to-date. The PlayStation 3 software market is up 36% calendar year-to-date. EA is the #1 PC publisher with 27% segment share at retail calendar year-to-date and strong growth in digital downloads of full-game software. For the quarter, EA had six of the top 20 selling games in Western markets with FIFA 11, Madden NFL 11, NCAA® Football 11, NHL®11, Battlefield: Bad Company™ 2 and FIFA 10. -

Electronic Arts, Inc. (EA) Q3 2014 Earnings Call

Electronic Arts, Inc. EA Q3 2014 Earnings Call Jan. 28, 2014 Company▲ Ticker▲ Event Type▲ Date▲ PARTICIPANTS Corporate Participants Rob Sison – Vice President-Investor Relations, Electronic Arts, Inc. Andrew Wilson – Chief Executive Officer & Director, Electronic Arts, Inc. Blake J. Jorgensen – Chief Financial Officer & Executive Vice President, Electronic Arts, Inc. Peter Robert Moore – Chief Operating Officer, Electronic Arts, Inc. Patrick Söderlund – Executive Vice President-EA Games Label, Electronic Arts, Inc. Other Participants Colin A. Sebastian – Analyst, Robert W. Baird & Co. Equity Capital Markets Edward S. Williams – Analyst, BMO Capital Markets (United States) Doug L. Creutz – Analyst, Cowen & Co. LLC Arvind Bhatia – Analyst, Sterne, Agee & Leach, Inc. Michael J. Olson – Analyst, Piper Jaffray, Inc. James L. Hardiman – Analyst, Longbow Research LLC Brian J. Pitz – Analyst, Jefferies LLC Drew E. Crum – Analyst, Stifel, Nicolaus & Co., Inc. Stephen D. Ju – Analyst, Credit Suisse Securities (USA) LLC (Broker) Ryan Gee – Analyst, Bank of America Merrill Lynch Mike Hickey – Analyst, The Benchmark Co. LLC Ben Schachter – Analyst, Macquarie Capital (USA), Inc. Neil A. Doshi – Analyst, CRT Capital Group LLC MANAGEMENT DISCUSSION SECTION Operator: Welcome, and thank you for standing by. At this time, all participants are in a listen-only mode. [Operator Instructions] Today’s conference is being recorded. If you have any objections, you may disconnect at this time. Now, I’ll turn the meeting over to Mr. Rob Sison, Vice President of Investor Relations. You may begin. Rob Sison, Vice President-Investor Relations Thank you. Welcome to EA’s Fiscal 2014 Third Quarter Earnings Call. With me on the call today are Andrew Wilson, our CEO; and Blake Jorgensen, our CFO.