Fremantle Inner Harbour Container Movement Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Risky Roads Survey Results 2014 Metropolitan Local Government Areas: Risky Roads Survey Results 2014 2014

Metropolitan Regional Local Government Areas: Risky Roads Survey Local Results 2014 Government Areas 2014 Risky Roads Survey Results 2014 Metropolitan Local Government Areas: Risky Roads Survey Results 2014 2014 in those areas. Alarmingly in regions like the Wheatbelt two out of three road deaths were local Executive Summary residents on local roads. While we can all do our part to improve the attitudes of drivers we must also work towards The RAC represents over 800,000 Western Australian members and advocates on their behalf on improving the road environment to meet the needs of road users now and into the future. matters including affordable motoring, environmental sustainability, public transport and safe road The results from the Risky Roads campaign are publicly available at www.rac.com.au/riskyroads use. The RAC represents all road users on the WA Road Safety Council and has strong alliances with local government, Main Roads WA (MRWA) and community road safety organisations. Having a safe road environment is important for all road users because the right infrastructure can be the difference between a fatal crash and a minor collision. Last year on average one person died on WA roads nearly every two days. The RAC’s Risky Roads campaign is WA’s biggest public infrastructure survey and is undertaken to provide a snapshot of community perceptions, insight for road authorities and assist in identifying trends in traffic flow, infrastructure and safety. The 2014 campaign ran during April and May, providing Western Australians’ the opportunity to express their views and nominate sub-standard roads and intersections throughout the state. -

Mr Dean Nalder GATEWAY WA PROJECT G

Extract from Hansard [ASSEMBLY — Thursday, 16 June 2016] p3582b-3583a Mrs Glenys Godfrey; Mr Dean Nalder GATEWAY WA PROJECT — TRAFFIC NOISE Grievance MRS G.J. GODFREY (Belmont) [9.29 am]: My grievance this morning is to the Minister for Transport. Gateway WA was designed to cater for an expected doubling by 2030 of both passenger air travel and freight and container transport in the Kewdale area. The project also helped by addressing some of the state’s most accident-prone intersections. The Gateway WA project began in 2013 and was funded with $676 million in federal government funds and $310 million from the state government. The Gateway WA project is to date the largest road project undertaken by Main Roads and I was pleased to attend the official opening in April this year along with the Prime Minister, Hon Malcom Turnbull, MP; the federal Minister for Infrastructure and Transport, Hon Darren Chester, MP; the state Minister for Transport, Hon Dean Nalder, MLA; and the federal member for Swan, Steve Irons, MP. The Gateway project has produced some impressive statistics—165 lane kilometres of road constructed, 460 000 tonnes of asphalt laid, 21 kilometres of principal shared path built for cyclists and pedestrians, the planting of over one million plants, approximately 1 000 people working on the project at its peak, 11 bridges built, four new interchanges constructed, seven intersection upgrades, the widening of Tonkin Highway to six lanes between Great Eastern Highway and Roe Highway, and the upgrade of Leach Highway to an expressway standard from Orrong Road to Perth Airport. -

Western Australia the P11arijaceutical Register Western Australia

[5371 OF WESTERN AUSTRALIA (Published by Authority at 3 .30 p.m .) No, 12] PERTH : TUESDAY, 27th FEBRUARY [1979 THE P11ARIJACEUTICAL REGISTER OF WESTERN AUSTRALIA 82687/2/79 27 February, 1979 .] GOVERNMENT GAZETTE, W .A. 539 THE PHARMACEUTICAL REGISTER OF WESTERN AUSTRALIA THE subjoined Register is published in accordance with the provisions of Clause 25 of the Pharmacy Act, 1964 . E. P. WALSH, Perth, January, 1979. Registrar. Date of No. Name Address Qualification Registra- tion 1808 Abel, Clifford Robert Kalgoorlie c/c Great Brit. 6/6/78 1811 Abel, Veronica Ann Kalgoorlie .. .. .... .... c/c Great Brit. 1/8/78 1817 Abrahams, Susan Lillian 63 Harcourt Drive, Hillarys c/c N.S.W. 5/9/78 1474 Accordino, Tony Joseph .... 16A Manchester Street, Victoria Park Assoc. W.A. 1/2/72 1085 Adams, Michael Thomas 33 Wincanton Road, Karrinyup Final W.A. 4/2/64 966 Adams, Rodney John .... 7 Emberson Street, Morley Final W.A. 7/2/61 341 Adlard, Edith Emma 42 Lyons Street, Cottesloe .... Final W.A. 5/7/27 1469 Aivaliotis, Sylvia .... 51 Robinson Avenue, Perth Assoc. W.A. 10/12/71 1116 Albury, Jill Mary .... 36 Widdicombe Street, Myaree Final W.A. 14/12/64 979 Alford, Cherry 196 Stock Road, Melville ... Assoc. W.A. 10/12/71 472 Allan, Griffith David Tapley 34 Napoleon Street, Cottesloe .... .... Final W.A. 16/2/37 435 Allan, James Thomas .... 44 Gloucester Crescent, Shoalwater Bay .... Final W.A. 2/4/35 1137 Allan, Peter Griffith .... 44 Bay View Terrace, Mosman Park Final W.A. 5/3/65 1497 Allen, Barbara . -

Metropolitan Road Fact Sheet

1. What are Main Roads and Highways in the Perth metropolitan area? Metropolitan In the Perth metropolitan area, the following highways and main roads (whole or part) are under the care and control of Main Roads Road Fact Sheet Western Australia: Albany Highway Albany Highway – starts at Welshpool Road and finishes at Metropolitan Boundary Armadale Road Starts at Albany Highway and finishes at Kwinana Freeway Brearley Avenue Starts at Great Eastern Highway and finishes at Airport boundary Brookton Starts at Albany Highway and finishes at Highway the Metropolitan Boundary Canning Highway Starts at Causeway and finishes at Stirling Highway Causeway Cockburn Road Starts at Hampton Road and finishes at Russell Road Garratt Road Bridge Great Eastern Starts at Causeway into Johnson Street Highway right at James Street into East Street and right at Great Eastern Highway to Roe Highway intersection and then through Greenmount, Mundaring and past the Lakes Turn-off to the Metropolitan Boundary west of Linley Valley Road Great Eastern Starts at Great Eastern Highway and Highway Bypass finishes at Roe Highway Great Southern Starts at Great Eastern Highway to Highway Metropolitan Boundary approx. 2.5 km Graham Farmer Starts at Tunnel and finishes at Freeway Chamberlain Road Great Northern Starts at Roe Highway to Metropolitan Highway Boundary near parking bay 300 metres south of Brand Highway Guildford Road Starts on south side of bridge over Graham Farmer Freeway on East Parade and finishes at Johnson Street, Guildford High Street Starts at Carrington Street -

Transport Impact Assessment State Football Centre

Transport Impact Assessment State Football Centre Transport Impact Assessment State Football Centre CW1142300 Prepared for Carabiner 8 December 2020 8 December 2020 Cardno i Transport Impact Assessment State Football Centre Contact Information Document Information Cardno (WA) Pty Ltd Prepared for Carabiner ABN 77 009 119 000 Project Name State Football Centre 11 Harvest Terrace File Reference CW1142300-TR-R001-B- West Perth WA 6005 State_Football_Centre_TIA- Australia V3EH-JM.docx www.cardno.com Job Reference CW1142300 Phone +61 8 9273 3888 Fax +61 8 9486 8664 Date 8 December 2020 Version Number B Author(s): Edmond Hoang Effective Date 8/12/2020 Traffic Engineer Approved By: Jacob Martin Date Approved 8/12/2020 Team Leader – Transport Planning Document History Version Effective Date Description of Revision Prepared by Reviewed by A 07/12/2020 For Issue EH DH/JM B 08/12/2020 For Issue EH DH/JM © Cardno. Copyright in the whole and every part of this document belongs to Cardno and may not be used, sold, transferred, copied or reproduced in whole or in part in any manner or form or in or on any media to any person other than by agreement with Cardno. This document is produced by Cardno solely for the benefit and use by the client in accordance with the terms of the engagement. Cardno does not and shall not assume any responsibility or liability whatsoever to any third party arising out of any use or reliance by any third party on the content of this document. Our report is based on information made available by the client. -

![Extract from Hansard [COUNCIL — Tuesday, 10 May 2016] P2484c-2485A Hon Helen Morton](https://docslib.b-cdn.net/cover/6509/extract-from-hansard-council-tuesday-10-may-2016-p2484c-2485a-hon-helen-morton-2556509.webp)

Extract from Hansard [COUNCIL — Tuesday, 10 May 2016] P2484c-2485A Hon Helen Morton

Extract from Hansard [COUNCIL — Tuesday, 10 May 2016] p2484c-2485a Hon Helen Morton GATEWAY WA PROJECT Statement HON HELEN MORTON (East Metropolitan) [9.47 pm]: I wanted to congratulate everybody involved in the very successful completion of the Perth Airport and freight access project. The project has delivered a really safe and more efficient transport network around Perth Airport and the freight and industrial areas of Kewdale and Forrestfield. The project began in 2013 and the full scope of the works was completed by the end of the first quarter of 2016. It was opened on 12 April 2016 by the Prime Minister, the state transport minister, Hon Dean Nalder, and the federal transport minister, Hon Darren Chester; many other members of Parliament were there to celebrate the very successful project. It was completed ahead of the planned consolidation of the domestic and international Perth Airport terminals, which was an important milestone for that project. The project is valued at around about $1 billion and is the largest road project undertaken to date in Perth. The federal government contributed $676 million and the state government $310 million. The Gateway WA project, as it is referred to, is a stunning success in every respect. I use that road nearly every day and marvel at how easy and safe it is, and at the pure enjoyment of travelling from Kalamunda to the city now that that project has been completed. It will be enjoyed by thousands of people for decades to come. This project is a fantastic asset for Western Australia and for all Western Australians. -

13.4 in Principle Support of the Orrong Road, Leach Highway to Great

13.4 In principle support of the Orrong Road, Leach Highway to Great Eastern Highway, Expressway Concept developed by Main Roads Western Australia Location Carlisle Lathlain Welshpool Reporting officer Frank Squadrito Responsible officer John Wong Voting requirement Simple majority Attachments 1. PC A-142- Combined-plans [13.4.1 - 2 pages] 2. D 20 22958 Approval Granted - Planning Control Area - 142 Orrong Road [13.4.2 - 4 pages] 3. Main Roads Western Australia - Community feedback dated March 2020 - Orrong Road Planning Study Up [13.4.3 - 3 pages] 4. Main Roads Western Australia - Orrong Road Planning Design Concept - Revision B [13.4.4 - 1 page] 5. D 20 48721 Orrong Road Planning Study response letter from Main Roads WA dated 16 June 2020 [13.4.5 - 9 pages] 6. Orrong Road schematic diagram [13.4.6 - 1 page] Recommendation That Council provides “in principle” support for the Main Roads Western Australia Orrong Road Planning Design Concept, Revision B subject to: a) Comprehensive detailed traffic impact assessment, considering the local road impacts being submitted to the Town prior to detailed design works being initiated. b) Input and involvement by Council’s representatives on detailed design outcomes. c) Detailed design drawings impacting Council assets shall be submitted and approved by the relevant departments and to the satisfaction of the Town of Victoria Park. Purpose For Council to consider and provide “In Principle” support for the current 2020 Concept design prepared by Main Roads Western Australia for the Orrong Road Planning Study (between Great Eastern Highway and Leach Highway). Background 1. In late May 2019, the Town received formal advice that Main Roads was undertaking a planning study to identify the best solution for upgrading Orrong Road between Great Eastern Highway and Leach Highway. -

Ordinary Council Meeting Agenda – 15 October 2019

Ordinary Council Meeting Agenda – 15 October 2019 Please be advised that an Ordinary Council Meeting will be held at 6:30 pm on Tuesday 15 October 2019 in the Council Chambers, Administration Centre at 99 Shepperton Road, Victoria Park. Mr Anthony Vuleta – Chief Executive Officer 10 October 2019 Table of contents Item Page no 1 Declaration of opening .................................................................................................................................4 2 Announcements from the Presiding Member .....................................................................................4 3 Attendance.........................................................................................................................................................6 3.1 Apologies..................................................................................................................................................6 3.2 Approved leave of absence ...............................................................................................................6 4 Declarations of interest.................................................................................................................................7 5 Public question time.......................................................................................................................................8 5.1 Response to public questions taken on notice at the Ordinary Council Meeting held on 17 September 2019 ........................................................................................................................8 -

Traffic Signals Safety and Efficiency Project

Project: Traffic Signals Safety and Reference: 232984 Efficiency Project Prepared for: RAC WA Revision: 2 Transport Analysis Report 9 October 2013 Contents 1. Introduction 5 1.1 Project purpose 5 1.2 Approach 5 2. Perth Context 6 2.1 Governance 6 2.2 Traffic signals system 6 3. Methodology 7 3.1 Stage One – Initial investigations 7 3.2 Stage Two – SCATS options testing 8 4. Site Overviews 9 4.1 Tonkin Highway/ Kelvin Road 9 4.2 Orrong Road 12 5. Model Build and Calibration: Existing Situation 20 5.1 Overview 20 5.2 Data sources 22 5.3 Assumptions 22 5.4 Model calibration and validation 23 6. Option Testing: Tonkin Highway/ Kelvin Road 27 6.1 Option plan 27 6.2 Option testing results 27 6.3 Summary results 29 7. Option Testing: Orrong Road 30 7.1 Option plan 30 7.2 Option testing results 30 7.3 Summary results 34 8. Key Findings and Conclusions 35 9. Recommendations 40 Appendices Appendix A Further Crash Data Project 232984 9 October 2013 Revision 2 Page 1 Appendix B Calibration Details Appendix C Modelling Delay Outputs Appendix D SCATS Counts Comparison Index of Figures Figure 4-1: Tonkin Highway/ Kelvin Road site location map 9 Figure 4-2: Tonkin Highway/ Kelvin Road site location map 9 Figure 4-3: Tonkin Highway/ Kelvin Road intersection layout 10 Figure 4-4: Orrong Road looking northwest to Oats Street 13 Figure 4-5: Orrong Road site location map 13 Figure 4-6: Orrong Road/ Francisco Street intersection layout 14 Figure 4-7: Orrong Road/ Archer Street intersection layout 14 Figure 4-8: Orrong Road/ Wright Street intersection layout -

Agenda Briefing Forum Notes – 6 October 2020

Agenda Briefing Forum Notes – 6 October 2020 Please be advised that an Agenda Briefing Forum was held at 6:30 pm on Tuesday 6 October 2020 in the Council Chambers, Administration Centre at 99 Shepperton Road, Victoria Park. Her Worship the Mayor Karen Vernon 8 October 2020 Table of contents Item Page no 1 About the Agenda Briefing Forum ............................................................................................................. 4 2 Opening ................................................................................................................................................................. 5 3 Acknowledgement of country ...................................................................................................................... 5 4 Announcements from the Presiding Member ...................................................................................... 5 5 Attendance ........................................................................................................................................................... 7 5.1 Apologies .................................................................................................................................................... 7 5.2 Approved leave of absence ................................................................................................................. 7 6 Declarations of interest ................................................................................................................................... 8 7 Public participation -

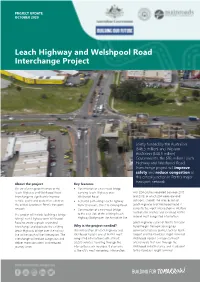

Leach Highway and Welshpool Road Interchange Project

PROJECT UPDATE OCTOBER 2020 Leach Highway and Welshpool Road Interchange Project Jointly funded by the Australian ($46.5 million) and Western Australian ($46.5 million) Governments, the $93 million Leach Highway and Welshpool Road Interchange project will improve safety and reduce congestion at this critical junction in Perth’s major transport network. About the project Key features We are planning construction of the • Construction of a new road bridge Leach Highway and Welshpool Road carrying Leach Highway over with 224 crashes recorded between 2015 interchange to significantly improve Welshpool Road and 2019, of which 204 were rear-end vehicle, cyclist and pedestrian safety at • A shared path along Leach Highway collisions. Overall, the intersection of this critical junction in Perth’s transport from Sevenoaks Street to Orrong Road Leach Highway and Welshpool Road is network. • Construction of a new road bridge currently the worst intersection in Western Australia for crashes and is ranked Perth’s The project will include building a bridge to the east side of the existing Leach second most congested intersection. taking Leach Highway over Welshpool Highway Bridge over the Armadale line Road to create a grade-separated Leach Highway is part of Perth’s Principal interchange and duplicate the existing Why is the project needed? Road Freight Network serving key Leach Highway bridge over the railway The intersection of Leach Highway and commercial activity centres such as Perth line to the south of the intersection. The Welshpool Road is one of Perth’s most Airport and the Kewdale Freight Terminal. interchange will reduce congestion and congested intersections with at least Welshpool Road is a major east-west deliver more consistent and reduced 50,000 vehicles travelling through the arterial route that runs through the journey times. -

Gazette East Canning 22102020

Thursday, October 22, 2020 perthnow.com.au/community-news Council’s dressing down CANNING Mayor Patrick Hall may not ORRONG have understood the hype, but councillors have abandoned a pro- posal to dramatically increase a clothing al- lowance for elected members and ditched the perk completely following a backlash. Under the plan pres- ented by City staff at Tuesday’s council IDEA meeting, the clothing allowance for the mayor would have more than tripled in the first year of their term from $600 to $2000 and CONTINUED PAGE 4 INSIDE SUNKEN EXPRESSWAY PLAN TO SLASH TRAVEL TIMES Sarah Brookes capacity, with up to 65,000 expressway from Great vehicles a day using the Eastern Highway that con- TELETHON A SUNKEN expressway is road. tinues Orrong Road as an Main Roads’ preferred It is predicted that elevated structure over FAMILY option to drastically cut demand will increase to as Leach Highway, merging travel times along a noto- much as 100,000 vehicles south of the Division and rious 5km stretch of per day by 2031. Bell streets intersection. FESTIVAL Orrong Road. Historical planning to Traffic modelling shows Orrong Road between upgrade Orrong Road to the preferred concept FUN GUIDE Leach Highway and Great six lanes at ground level would result in a journey of Eastern Highway has been has been deemed unviable about five minutes, a time identified as a weak link in as it would be unable to impact on land and result Main Roads is seeking saving of 35 minutes com- Page 12 the State’s road network meet future demand, in little to no improvement council support for its pre- and is operating beyond would have a significant in travel times.