The Thomson Corporation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report 2007

The Thomson Corporation Annual Report 2007 2 To Our Shareholders 64 Financial Statements and Notes 6 I am 110 Board of Directors 18 Thomson 2007 Financial Highlights 112 Senior Management 24 Management’s Discussion and Analysis 113 Corporate Information We are like you. At Thomson, our success depends on being trusted, on staying ahead, on having the answers others need in order to succeed. We are certain we have what it takes, because we have put the right model at the center of our design. You, the professional. The Thomson Corporation is a leading provider of critical information, decision support tools and related services to professionals in the legal, financial, tax and accounting, scientific and healthcare sectors. Thomson integrates its unique proprietary databases with third party data, software and analytical tools to create essential workflow solutions for business and professional clients around the world. We provide information platforms and services to support faster, better decisions that are more informed, more considered and more immediate. We have fashioned our solutions to provide the most relevant and trusted data instantly – intelligent information that helps you put your knowledge to work. This book is a tribute to you and our thanks for the trust you place in us. 1 To Our Shareholders: 2007 was a milestone year for The Thomson Corporation. The company’s name was in the headlines more often than perhaps at any other time in its history. On a Friday in May we announced our agreement to sell Thomson Learning, and on the following Tuesday we announced an agreement to buy Reuters Group PLC for nearly $18 billion.* The sale of our Thomson Learning assets for more than $8 billion was a resounding success. -

When Information Is Abundant, a Good Filter Is Prized

WHEN INFORMATION IS ABUNDANT, A GOOD FILTER IS PRIZED In the internet age, the abundance of free information creates its own problems. This is the opportunity for the big business information groups. Tom Glocer, CEO of Thomson Reuters, argues that a path to relevant information is what people need s Stewart Brand, an early technology That statement is as true now as it was then, guru, wrote in The Media Lab nearly despite the information revolution that has A a quarter century ago, “Information occurred in the intervening years. So much wants to be free. Information also wants to information has become freely available as the be expensive. Information wants to be free internet has evolved. But businesses still need because it has become so cheap to distribute, information that helps them do commerce copy, and recombine – too cheap to meter. and are willing to pay for it. The challenge It wants to be expensive because it can be now lies in providing the most useful and immeasurably valuable to the recipient. relevant information – and in creating an That tension will not go away.” efficient path to it. 12 Brunswick Issue four Review Summer 2011 1851 Paul Julius Reuter opens an office to transmit stock market quotations and news between London 1965 and Paris over the new Thomson Newspapers Dover-Calais submarine becomes a publicly quoted telegraph cable. company on the Toronto 1934 Stock Exchange. Roy Thomson acquires his first newspaper, purchasing the Timmins Daily Press in Ontario. Since the invention of Gutenberg’s press in the were sent via the internet in 2010 alone, and the 15th century, each successive generation has been volume of information continues to grow. -

Market Index Uniflex 10%

Investment and retirement 5% 10% Market Index Uniflex 10% 25% Main Product Features 25% 6-year term (not redeemable before maturity) Guarantee of principal on maturity of 100% Low management fees of 1% per year 10% 15% $500 minimum deposit An easy way to diversify Cut-off age: 64 y/o (registered) and 70 y/o (non-registered) Even under a scenario where the return of each share is negative, this product may produce a global positive return Sector diversification of the Market Index Uniflex How it works On the settlement date, a starting level will be determined for each Canadian share included in the portfolio. On the maturity date, a ratio of the closing level over the starting level for each share will be computed. The 8 best performing shares during the 6-year term will be automatically assigned a fixed return of 60%, regardless of whether the actual return was positive or negative. The remaining 12 shares will be assigned their actual return. The global return (maximum 60%) will be calculated by averaging these 20 returns. The value at maturity will be the highest value between: the initial deposit; or the initial deposit PLUS global return (maximum 60%) Exposure to 20 Canadian companies included in the S&P/TSX 60 Index Company Sector Company Sector Metro Inc. Scotiabank Consumer staples Loblaw Companies Limited The Toronto-Dominion Bank Royal Bank of Canada Financial services Bank of Montreal Enbridge Inc. Sun Life Financial Inc. TransCanada Corporation Cenovus Energy Inc. Energy Canadian Natural Resources Limited Canadian National Railway Industrials Suncor Energy Inc. -

© 2020 Thomson Reuters. No Claim to Original U.S. Government Works. 1 Actavis Holdco, Inc

Actavis Holdco, Inc. v. State of Connecticut, 2020 WL 749132 (2020) 2020 WL 749132 (U.S.) (Appellate Petition, Motion and Filing) Supreme Court of the United States. ACTAVIS HOLDCO, INC., et al., Petitioners, v. STATE OF CONNECTICUT, et al., Respondents. No. 19-1010. February 11, 2020. On Petition for Writ of Certiorari to the United States Court of Appeals for the Third Circuit Petition for Writ of Certiorari Michael W. McConnell, Wilson Sonsini, Goodrich & Rosati, PC, 650 Page Mill Road, Palo Alto, CA 94304. Catherine E. Stetson, Hogan Lovells US LLP, 555 Thirteenth Street, NW, Washington, DC 20004. John P. Elwood, Arnold & Porter LLP,, 601 Massachusetts, Avenue, NW, Washington, D.C. 20001. Steffen N. Johnson, Wilson Sonsini, Goodrich & Rosati, PC, 1700 K Street, NW, Washington, DC 20006, (202) 973-8800, [email protected]. Michael H. McGinley, Dechert LLP, 1900 K Street, NW, Washington, DC 20006, for petitioners. Chul Pak, Daniel P. Weick, Wilson Sonsini Goodrich & Rosati, PC, 1301 Ave. of the Americas, 40th Floor, New York, New York, 10019, (212) 999-5800. Seth C. Silber, Jeffrey C. Bank, Wilson Sonsini Goodrich & Rosati, PC, 1700 K Street, NW, Washington, D.C. 20006, (202) 973-8800. Adam K. Levin, Benjamin F. Holt, Justin W. Bernick, Hogan Lovells US LLP, 555 Thirteenth Street, NW, Washington, D.C. 20004, (202) 637-5600, Counsel for Petitioners, Mylan Inc., Mylan, Pharmaceuticals Inc., Mylan, N. V., and UDL, Laboratories, Inc. Sheron Korpus, Seth A. Moskowitz, Kasowitz Benson Torres, LLP, 1633 Broadway, New York, New York, 10019, (212) 506-1700, for petitioners Actavis Pharma, Inc., and Actavis Holdco U.S., Inc. -

BMO Growth GIC Reference Portfolio

BMO® Growth GIC December 2011 - Series 56 Term 4 Years 100% Principal Protected Minimum Investment $1000 Maximum Rate of Return for the Term 17.00% (4.25% annually*) This medium term GIC allows you to participate in the growth This GIC may be right for you if you: of Canadian stocks with no risk to your principal investment. It are looking to diversify your portfolio with a medium term offers the potential to generate returns based on the investment peformance of a basket of 15 large Canadian companies. would like principal protection Reference Portfolio are willing to forego a guaranteed return for the potential to earn higher market-linked returns Company can keep your money invested until the end of the term Royal Bank of Canada (RY) Manulife Financial Corp. (MFC) Bank of Nova Scotia (The) (BNS) This GIC is an excellent way for you to gain access to the Toronto-Dominion Bank (The) (TD) returns on a portfolio of 15 large Canadian companies with the Canadian Imperial Bank of Commerce (CM) security of principal protection. Thomson Reuters (TRI) Principal protection - 100% of your original investment is returned to you at maturity Sun Life Financial Inc. (SLF) Manitoba Telecom Inc. (MBT) Higher return potential based on the performance of a portfolio of Canadian stocks Brookfield Asset Management, Class A (BAM.A) ® TransCanada Corp. (TRP) Designed in partnership with BMO Capital Markets , a market leader in creating innovative investment solutions Power Financial Corp. (PWF) Enbridge Inc. (ENB) Guaranteed by Bank of Montreal National Bank of Canada (NA) Eligible for Canada Deposit Insurance Corporation (CDIC) Teck Resources Ltd., Class B (TCK.B) deposit insurance up to applicable limits CI Financial Corp. -

Top News Before the Bell Stocks To

TOP NEWS • A hunt for any storage space turns urgent as oil glut grows With oil depots that normally store crude oil onshore filling to the brim and supertankers mostly taken, energy companies are desperate for more space. The alternative is to pay buyers to take their U.S. crude after futures plummeted to a negative $37 a barrel on Monday. • Corporate America seeks legal protection for when coronavirus lockdowns lift Major U.S. business lobbying groups are asking Congress to pass measures that would protect companies large and small from coronavirus-related lawsuits when states start to lift pandemic restrictions and businesses begin to reopen. • Teck Resources profit falls short as lockdowns, energy unit bite Teck Resources reported a much bigger-than-expected 84% plunge in quarterly profit, hit by shutdowns due to the coronavirus outbreak and weak performance in its energy unit. • U.S. energy industry steps up lobbying for Fed's emergency aid -letters The U.S. energy industry has asked the Federal Reserve to change the terms of a $600 billion lending facility so that oil and gas companies can use the funds to repay their ballooning debts, according to a letter seen by Reuters. • Coca-Cola sees 2nd quarter sales hit from coronavirus lockdown Coca-Cola forecast a significant hit to current-quarter results as restaurants, theaters and other venues that represent about half of the company's revenue remain closed because of the coronavirus pandemic. BEFORE THE BELL Canada's main stock index futures slid as U.S. oil futures continued to trade in the negative after their first ever sub-zero dive on Monday, furthering concerns of a global recession in the coming months. -

Investor Fact Sheet – Scotiabank Q1 2021

Investor Fact Sheet – Scotiabank Q1 2021 Our Business Four Business Lines1,2,3,4 Scotiabank is a leading bank in the Americas and the only bank 40% with operations in Canada, US and the Pacific Alliance countries. Canadian Banking Guided by our purpose: “for every future”, we help our customers, 17% their families and their communities achieve success through a Business Line International broad range of advice, products and services, including personal Earnings Banking and commercial banking, wealth management and private 24% $2.3B banking, corporate and investment banking, and capital markets. Global Banking and Markets 19% TSX: BNS; NYSE: BNS Global Wealth http://www.scotiabank.com Management Follow us on Twitter @ScotiabankViews. Other Financial Information Reasons to Invest in Scotiabank Pre-Tax, Pre Provision Profit4 $3,892 million (+5% Y/Y) • Leading bank in the Americas Total Assets5 $1,164 billion o Top 3 bank in Canada and top 5 bank in the Pacific Alliance Net Loans and Acceptances5 $618 billion ~94% of earnings from the Americas o Deposits5 $769 billion • Diversified exposure to high quality growth markets Employees5,6 ~90,000 Unique Americas footprint provides diversified exposure to o 5 higher growth, high ROE banking markets Branches and Offices 2,597 5 o 229 million people in the Pacific Alliance countries comprise the ABMs 8,716 6th largest economy in the world • Increasing scale and market share in core markets Medium-term Financial Objectives o Competitive scale and increasing market share in core markets Q1 2021 Actual o Competitive advantages in technology, risk management, and 2,4 funding versus competitors EPS Growth 7%+ +3% Return on Equity 14%+ 14.4%2,4 • Strong risk culture: solid credit quality, well provisioned +3.0%2,4 o Strong Canadian risk management culture with strong Operating Leverage Positive capabilities in AML and cybersecurity +3.4% (Ex. -

Manulife Dividend Income Class1,2 EQUITY Series T6 · Performance As at August 31, 2021 · Holdings As at July 31, 2021

Manulife Dividend Income Class1,2 EQUITY Series T6 · Performance as at August 31, 2021 · Holdings as at July 31, 2021 Portfolio advisor: Manulife Investment Why Invest Management Limited Managed by the Manulife Essential Equity Team all companies are viewed under the same fundamental proprietary lens, using a scalable and repeatable process driven by the team's fundamental beliefs unchanged since the team's founding in 1996. The team's focus is on creating a high returning conglomerate portfolio consisting of diversified businesses to Management ensure that revenue and earnings come from many different sources. As a result, no single event will have a large negative impact on the portfolio. The fund aims to provide investors with a portfolio of Canadian and U.S. dividend paying diversified Conrad Dabiet businesses, which in aggregate have high and stable profitability, minimal financial leverage and at an attractive valuation. The outcome is a portfolio of securities that together create value at a pace faster than the benchmark. The fund is ideal for clients looking for long term growth and tax efficient monthly income. Alan Wicks Growth of $10,000 since inception7 Chris Hensen 36,000 $32,948 30,000 Jonathan Popper ($) 24,000 18,000 Fund Codes (MMF) 12,000 6,000 Series FE LL2 LL3 DSC Other 2013 2014 2015 2016 2017 2018 2019 2020 2021 Advisor 8545 8045 8745 8445 — Advisor - DCA 28545 28045 28745 28445 — F — — — — 8645 Calendar Returns (%) F - DCA — — — — 28645 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 FT6 — — — — 1218 — — 24.43 -

Investor Fact Sheet – Scotiabank Q2 2021

Investor Fact Sheet – Scotiabank Q2 2021 Our Business Four Business Lines1,2,3,4 Scotiabank is a leading bank in the Americas and the only bank with operations in Canada, US and the Pacific Alliance countries. 41% Canadian Guided by our purpose: “for every future”, we help our customers, Banking YTD their families and their communities achieve success through a 18% Business Line International broad range of advice, products and services, including personal Earnings Banking and commercial banking, wealth management and private 23% $4.5B banking, corporate and investment banking, and capital markets. Global Banking TSX: BNS; NYSE: BNS and Markets 18% Global Wealth http://www.scotiabank.com Management Follow us on Twitter @ScotiabankViews. Other Financial Information 5 Reasons to Invest in Scotiabank Pre-Tax, Pre Provision Profit $3,720 million (+2% Y/Y) Total Assets6 $1,125 billion Leading bank in the Americas • Net Loans and Acceptances6 $623 billion Top 3 bank in Canada and top 5 bank in the Pacific Alliance o Deposits6 $757 billion o >95% of earnings from the Americas Employees6,7 ~90,000 • Diversified exposure to high quality growth markets Branches and Offices6 2,569 o Unique Americas footprint provides diversified exposure to higher growth, high ROE banking markets ABMs6 8,695 o 229 million people in the Pacific Alliance countries comprise the 6th largest economy in the world Medium-term Financial Objectives • Increasing scale and market share in core markets Q2 2021 Actual 2021 YTD Actual o Competitive scale and increasing market -

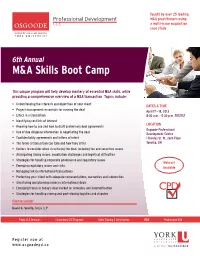

6Th Annual M&A Skills Boot Camp

Taught by over 25 leading M&A practitioners using a multi-issue acquisition case study 6th Annual M&A Skills Boot Camp This unique program will help develop mastery of essential M&A skills, while providing a comprehensive overview of a M&A transaction. Topics include: • Understanding the interests and objectives of your client DATES & TIME • Project management essentials for running the deal April 17 - 18, 2013 • Ethics in a transaction 8:30 a.m. - 5:30 p.m. EDT/EST • Identifying confl icts of interest LOCATION • Knowing how to use and how to draft preliminary deal agreements Osgoode Professional • Use of due diligence information in negotiating the deal Development Centre • Confi dentiality agreements and letters of intent 1 Dundas St. W., 26th Floor • The forms a transaction can take and how they differ Toronto, ON • Factors to consider when structuring the deal, including tax and securities issues • Anticipating timing issues, negotiation challenges and logistical diffi culties • Strategies for handling corporate governance and regulatory issues Webcast • Emerging regulatory issues and risks Available • Managing risk in international transactions • Protecting your client with adequate representations, warranties and indemnities • Structuring and planning issues in international deals • Emerging trends in today’s deal market re: remedies and indemnifi cation • Strategies for handling closing and post-closing logistics and disputes Course Leader David A. Seville, Torys LLP Public CLE Seminars Customized CLE Programs Skills Training & Certifi cation ITAW Professional LLM Register now at www.osgoodepd.ca 6th Annual M&A Skills Boot Camp Why this program is an n order to complete an acquisition in today’s M&A market, lawyers need a clear understanding of the essential building block client’s business goals, and how to structure and negotiate a deal which meets those goals. -

Downloaded from a Remote Server Together with the Software Needed to Display It

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 20-F (Mark One) [_] REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR [X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 1999 OR [_] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from _______________ to ________________ Commission file number 0-13456 Reuters Group PLC (Exact name of Registrant as specified in its charter) England (Jurisdiction of incorporation or organization) 85 Fleet Street, London EC4P 4AJ, England (Address of principal executive offices) Securities registered or to be registered pursuant to Section 12(b) of the Act: None. Securities registered or to be registered pursuant to Section 12(g) of the Act: Ordinary Shares of 25p each. Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None. Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report. Ordinary Shares of 25p each 1,422,729,960 Founders Share of £1 1 Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

IR Day 2021 Thomson Reuters Change Program

Thomson Reuters Change Program Kirsty Roth Chief Operations & Technology Officer Investor Day 2021 2 TR has Opportunity to Better Serve Customers & Access New Customer Lever #1 - Holding Company Structure to a World – Class Groups Operating Company Structure Holding Company Operating Company Big 3 Global Reuters Big 3 Customer Global Reuters Customer Print News Print News Segments* Segments* Go to Go to Market Go to Market Go to Market Achieving Go to Go to Market Market Market Benefit of Scale Product Product Product Customer Product Dev. Experience Operations & Product & Operations Operations Operations Technology Portfolio Operations & Talent Talent Talent Technology Talent & Culture A Streamlined, Integrated & Agile Operating Company is Expected to Drive Strong Operating & Financial Performance & Value for Shareholders * Big 3 Customer Segments include Legal Professionals, Corporates and Tax & Accounting Professionals 2 2 TR has Opportunity to Better Serve Customers & Access New Customer Thomson Reuters Today Groups Minimize Complexity - Significant Opportunity ~24K Employees ~62K across 76 350+ Countries SKUs Products & available for variants sale 50+ Customer 278 entitlement Thomson Websites systems Reuters 50% On-Premise 50+ Revenue Call Centers 100+ 15+ Capital Order to Cash Projects Systems 3 TR | Legal | Corporates | Tax We Will Improve Customer Experience to Drive Revenue Growth & Savings TR Change Program - 5 Key Initiatives #1. Taking an End-to-End View of the Customer Journey #2. Creating a Comprehensive Omnichannel Experience #3. Providing Tools to Sales & Support Employees with a 360º Customer View #4. Utilizing Shared Capabilities, Data & Analytics & Completing the Shift to the Cloud #5. Using Digital to Grow with Small & Medium Businesses (SMBs) 4 TR | Legal | Corporates | Tax Transitioning to a World – Class Operating Company #1.