Minda Corp Kotak

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

TWO WHEELERS : MOTOR CYCLES M/S Royal Enfield Motors Ltd M/S Bajaj Auto Ltd M/S Honda Motorcycle & Scooter India Pvt. Ltd M

TWO WHEELERS : MOTOR CYCLES M/s Royal Enfield Motors Ltd Sl No. Index No. Nomenclature 1 63022-E Motor Cycle 350cc STD (12 Volt) Bullet Electra 2 63107-X Bullet Classic 500 3 64003-P Classic 500 Desert Strom 499cc 4 64004-H Thunderbird UCE 350cc 5 64005-I Classic 350cc 346 6 64006-S Bullet Electra UCE 346cc M/s Bajaj Auto Ltd Sl No. Index No. Nomenclature 1 63024-P Motor Cycle Bajaj Pulsar DTSi (150cc Electric Start) 2 63029-K Motor Cycle Bajaj Discover DTS-Si (Electric Start) 3 63030-X Motor Cycle Bajaj Discover 150 cc (Electric Start) 4 63032-D Bajaj Platina Motor Cycle DZ-02 (100cc) Alloy Wheel 5 63174-A Bajaj Platina 125 (With Electric Start) 6 63175-D Bajaj Discover 125 Drum Brake (Electric Start) 7 63176-E Bajaj Pulsar 135 LS (With Electric Start) 8 63177-L Bajaj Pulsar 180 (With Electric Start) 9 63178-P Bajaj Pulsar 220 (Without Full Fairing) (With Electric Start) 10 63179-H Bajaj Pulsar 220 F (With Full Fairing) (With Electric Start) 11 63180-I Bajaj Avenger 220 (With Electric Start) 12 64000-D Bajaj Discover 125 ST DTS-I Electric Start Disc Brake 13 64001-E Bajaj Discover 125 DTS-I Electric Start Disc Brake 14 64002-L Bajaj Discover 100 DTS-I Electric Start 4 Gears Drum Brake M/s Honda Motorcycle & Scooter India Pvt. Ltd Sl No. Index No. Nomenclature 1 63009-A Motor Cycle Honda CB Shine Self Drum Alloy (125 cc) 2 63010-D ‘Honda’ Unicorn (Self) Motor Cycle 4 Stroke Single Cylinder Air Cooled 150 cc 3 63122-L Honda CB Twister (Self Disc Alloy) 110cc 4 63124-H Honda CBR 150R STD 149.4cc 5 63125-I Honda ‘CBF Stunner’ (Self Disk Alloy) 125 cc 6 63128-K Honda CBR 150R DLX 149.4cc 7 63188-L Honda CB Trigger (STD) 149.1cc 8 63189-P Honda Dream Yuga (Self Drum Alloy) 109cc 9 63190-H Honda CB Twister 110cc (Self Drum Alloy) 10 63193-T Honda Dream Yuga (Kick Drum Alloy) 109cc 11 63194-K Honda Dream NEO (Kick Drum Spoke) 109cc 12 63195-X Honda Dream NEO (Kick Drum Alloy) 109cc 13 63196-A Honda Dream NEO (Self Drum Spoke) 109cc 14 63197-D Honda CBR 250R STD 249.6cc 15 63198-E Honda CBR 250R ABS 249.6cc M/s TVS Motor Company Ltd Sl No. -

LIBRO INDIA 2021 a Color FINAL Agosto.Indd

India-América Latina: Relación comercial e inversión India–Latin America: Trade and investment relationship India-América Latina: Relación comercial e inversión India–Latin America: Trade and investment relationship Sadcidi Zerpa de Hurtado Aparajita Gangopadhyay Alberto José Hurtado Briceño Editores Grupo de Estudios Económicos sobre Asia Universidad de Los Andes India-América Latina: Relación comercial e inversión India–Latin America: Trade and investment relationship © Sadcidi Zerpa de Hurtado Aparajita Gangopadhyay Alberto José Hurtado Briceño Editores 1ra Edición, 2021 Grupo de Estudios Económicos sobre Asia Universidad de Los Andes © Para esta edición Prachi Agarwal Nanno Mulder Aravind Krishnan Paridhi Pardeshi Hari Seshasayee Devika Misra Alberto José Hurtado Briceño Sadcidi Zerpa de Hurtado Soraya Caro Vargas Francisco Daniel Trejos-Mateus Paola Andrea Baroni Tamara Spagnolo Karol Stefany Rojas Tole Karen Lorena Gutiérrez Masmela Saul Martínez González Ramón Alonso Dugarte Rangel Francisco Javier Haro Navejas Raquel Isamara León Aparaajita Pandey Hecho el depósito de Ley Depósito legal: ME2021000274 E-Book: ME2021000276 ISBN: 978-980-11-2048-3 E-Book: 978-980-11-2049-0 Imágenes internas: www.pixabay.com Cuidado de los textos: Sadcidi Zerpa de Hurtado Aparajita Gangopadhyay Alberto José Hurtado Briceño Diseño y cuidado digital José Gregorio Vásquez Edición digital, 2021 La presente publicación fue evaluada y aprobada por el Dr. Manuel Gonzalo, Universidad Nacional de General Sarmiento, Argentina, y el Dr. Juan Miguel Massot, Universidad -

Mahindra Tractors Eyes Sales Growth in FY15 with Arjun Novo Business Today

21/03/2015 Mahindra tractors eyes sales growth in FY15 with Arjun Novo Business Today THE INDIA TODAY GROUP India Today Aaj Tak Headlines Today Business Today Men's Health Wonder Woman Cosmopolitan Oye! 104.8FM Travel Plus Bag it Today BIZ WRAP MARKETS FINANCES INDUSTRY TECH FEATURES VIDEOS OPINION PHOTOS B-SCHOOL DEBATE MORE GN Singh aims to change SENSEX 28261.08 NIFTY 8570.90 US$ R6s. 2.32 GOLD R2s. 5925 Type Stock Name drug regulatory structure 208.59 0.73% 63.75 0.74% 0 115 0.45% Mutual Funds Lookup Type Commodity Home SECTORS Auto Story Search Mahindra tractors eyes sales growth in FY15 with Arjun Novo PTI Kolkata Last Updated: October 15, 2014 | 17:10 IST LATEST MUST READ TECH NEWS Sebi slams firms for 'gender bias' in boardroom AAP govt hikes water charges by 10 per cent Coal auction: Govt rejects bids of JSPL, Balco Industries Delhihites may face water-shortage problem in summer (Photo: Reuters) Delhi HC bars Glenmark from selling two drugs RELATED Mahindra & Mahindra, which is gearing up to launch MORE airconditioned tractors, is optimistic about sales growth in the segment during the current financial year despite a 4 per cent DON'T MISS decline in the industry in the first half of the year. Arjun Novo may establish M&M as tech leader "Unseasonal and deficit rain caused degrowth in tractor industry in the first half. With launch of our new Arjun Novo we expect to register growth for the full year. Mahindra had seen a marginal growth of 0.6 per cent in tractor sales in H1," Mahindra Farm equipment VP marketing Ravindra Shahane M&M cuts growth forecast for tractor said. -

Here's Why We're the World's #1 Selling Tractor

HERE’S WHY WE’RE THE WORLD’S #1 SELLING TRACTOR. DEMING PRIZE JAPAN QUALITY MEDAL 2003 2007 A WHOLE HERD OF BEEFED UP MODELS TO CHOOSE FROM. eMax S SERIES The Tier IV emissions-compliant eMax S sub-compact tractors have once again redefined the sub-compact market with tractors that offer true tractor performance. Featuring a complete range of available attachments and implements including a factory installed cab, drive-over mower deck, snow removal equipment and a backhoe that can be added at any time, you have a powerful and versatile tractor that provides the industry’s best value. MAX SERIES The series features industry-redefining sub-compact and mid-compact models. The backbone of all Max series tractors is a full-length tractor frame that allows users to install a backhoe at any time. The Max series tractors have a wide range of attachments and implements, including a driver-over mowing deck, snow blowers, blades, brooms and feature the highest capacity loaders in the market. Factory-installed cab is available for the Max XL series. 1500 SERIES The high-performance premium 4WD, Tier IV mCRD-powered, 1500 series compact tractors are designed for light to medium applications. These 25.6 to 38.7 HP models are available with options like heavy-duty loaders and backhoes; gear, shuttle or hydrostatic transmissions; soft or integrated cabs; ag, industrial, or turf tires; drive-over mid-mount mowers; and many available implements. 2500 SERIES Economical and easy-to-operate 4WD, Tier IV mCRD-powered, tractors are designed for general purpose farming and agriculture, livestock operations and grounds maintenance. -

Mahindra Everyday

ISSUE 1, 2013 ISSUE 1, 2013 WHAT’S INSIDE? Mahindra e2o Launched: Set to Redefine the Future of Mobility World Class Tractor Plant Inaugurated in Andhra Pradesh MSSSPL’s Golden Journey Of 50 Years 8th Annual Mahindra Excellence in Theatre Awards Announced Special Feature: The Mahindra Institute of Quality Mahindra Everyday 1 ISSUE 1, 2013 CONTENTS CULTURAL COVER STORY 04 OUTREACH 35 Mahindra USA’s exciting and eventful On the art and culture front, initiatives story of growth and success, from showcased old world culture, the world’s 1994 to date. best guitar and music talent, excellence in theatre and more. INTERNATIONAL AWARDS FOR OPERATIONS 11 EXCELLENCE 40 The Mahindra Group’s international A spectrum of awards, including the action stretched from Serbia to Sri first Mahindra Sustainability awards Lanka, South Africa and elsewhere recognising diverse sustainability around the globe. initiatives, was recently presented. SECTOR BRIEFS 13 SUSTAINABILITY 47 As ever there was plenty happening Efforts and initiatives towards across sectors and in all spheres of preserving, safeguarding and sustaining action – new plants, new products, our planet and its precious resources. distinguished visitors, certifications and celebrations. Please write in to [email protected] to give feedback on this issue. ME TEAM Associate Editors: Zarina Hodiwalla, Darius Lam Soumi Rao Chandrika Rodrigues Col. Abhijit Dasgupta AS, Kandivli MLDL Mahindra Management Dev. Center Asha Sabharwal Stella Rozario AS, Nashik MTWL Santosh Tandav Mahindra Partners Shirish Kulkarni Pradeep Zoting AS, Igatpuri FES, Nagpur Vrinda Pisharody Tech Mahindra & K.P. Narsimha Rao Pavitra Kamdadai Mahindra Satyam AS, Zaheerabad MNEPL Rajeev Malik Venecia Paulose Martin Cisneros Preeti Nair MVML, Chakan Mahindra USA Mahindra Navistar Edited and Published by Roma Balwani Nitin Panday Swapnil Soudagar Pooja Thawrani for Mahindra & Mahindra Limited, Gateway Mahindra Swaraj Systech Mahindra Reva Building, Apollo Bunder, Mumbai 400 001. -

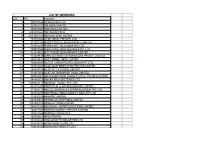

List of Importers S.N

LIST OF IMPORTERS S.N. IEC Importer 1 888015356 20 MICRONS LTD. 2 793012112 3M INDIA LIMITED 3 388038047 ABB INDIA LIMITED. 4 3892000662 ABI SNOWATECH 5 2503001335 ABIRAMI SOAP WORKS 6 799008966 ACER INDIA (PRIVATE) LTD 7 713020253 ADVICS SOUTH INDIA PRIVATE LIMITED 8 711002207 AGRIPLAST TECH INDIA PVT LTD 9 799008966 AGRITRADE INDIA SERVICES PVT LTD 10 312019882 AGT FOODS INDIA PRIVATE LIMITED 11 712023836 AISIN AUTOMOTIVE KARNATAKA PRIVATE LIMITED 12 288002822 AKZO NOBEL INDIA LIMITED 13 799009091 ALCON LABORATORIES (INDIA) PVT LTD., 14 503082058 ALOK MASTERBATCHES PRIVATE LIMITED 15 288007735 ALSTOM T & D INDIA LIMITED 16 711017956 ALSTOM TRANSPORT INDIA LIMITED 17 497016061 AMALGAMATIONS VALEO CLUTCH PRIVATE LIMITED 18 988006723 AMARA RAJA BATTERIES LTD 19 3306001414 AMAZON WOOD PVT. LTD. 20 488016207 AMBATTUR CLOTHING PRIVATE LIMITED 21 311009174 AMCOL MINERALS & MATERIALS INDIA PVT LTD 22 407034293 AMPHENOL OMNICONNECT INDIA PVT LTD 23 415900018 ANANDA VIKATAN 24 907000657 APARNA ENTERPRISES LIMITED 25 1088000720 APOLLO TYRES LIMITED 26 988001292 AQUAMALL WATER SOLUTIONS LIMITED 27 402017986 ARISTON AGENCY PRIVATE LIMITED 28 300022964 ARKEMA CHEMICALS 29 300062401 ARMSTRONG 30 588169340 ARO GRANITE INDUSTRIES LTD 31 588130311 ASAHI INDIA GLASS LTD 32 798014911 ASHIRVAD PIPES PVT LTD 33 488014336 ASHOK LEYLAND LIMITED 34 388010789 ASIAN PAINTS LTD 35 412001951 ASIAN TRADING COMPANY 36 796005532 AT & S INDIA PRIVATE LIMITED 37 707010462 ATS ELGI LIMITED 38 2588000011 AUROBINDO PHARMA LIMITED 39 507039807 AUTOLIV INDIA PVT. LTD. 40 903006499 AVANTI FEEDS LTD. 41 497016753 BASF CATALYSTS INDIA PVT LTD., 42 388007257 BASF INDIA LIMITED 43 288012101 BATA INDIA LIMITED 44 596004729 BECTON DICKINSON INDIA PRIVATE LIMITED 45 788013441 BEML LIMITED, 46 388167084 BENNETT COLEMAN & CO LTD 47 288019539 BERGER PAINTS INDIA LIMITED 48 788001027 BHARAT ELECTRONICS LTD. -

Logistics Management in Indian Automotive Component Industry

Logistics Management in Indian Automotive Component Industry Dr. W. K. SARWADE M.com, M.B.A. Ph.D. Professor Department of commerce Dr. Babasaheb Ambedkar Marathwada University, Aurangabad-431004 1 Logistics Management in Indian Automotive Component Industry Abstract Many of the leading firms in the Indian automotive component industry have an efficient logistics management system. Having an efficient logistics management system is no longer a choice but a necessarily for these firms considering the global opportunities that have opened for this industry. The Indian automotive component industry has shown tremendous growth over the last decade. Today it has 480 companies, employees more than 2,50,000 people and has an estimated turnover of approximately Rs 45,000 crore (US$ 10 billion). On export front also, the industry has grown by leaps and bounds, generating an overseas sales of to Rs. 8,190 Crores (US$ 1.8 billion) in 2005-06, which is nearly three times of what it exported in 2001-02 (US$ 578 million)1. Keywords:- logistics, employees, automotive, management, employees 2 Introduction: The Indian automotive component industry has shown tremendous growth over the last decade. Today it has 480 companies, employees more than 2,50,000 people and has an estimated turnover of approximately Rs 45,000 crore (US$ 10 billion). On export front also, the industry has grown by leaps and bounds, generating an overseas sales of to Rs. 8,190 Crores (US$ 1.8 billion) in 2005-06, which is nearly three times of what it exported in 2001-02 (US$ 578 million)1. The tremendous growth in the automotive component sector over the last few years is shown in table 1: Table 1: Growth in Production and Exports in the Indian Automotive Component Industry (Rs. -

Fact Sheet-Covers-Dec16-Ctc.Cdr

TOLL FREE NON TOLL FREE SMS WEBSITE 1800 425 0090 +91-40-23001181 IQ to 5757590 www.edelweissmf.com Content Market Commentary - Equity 3 Market Commentary – Debt 4 Equity Funds Edelweiss Absolute Return Fund 5 Edelweiss Arbitrage Fund 7 Edelweiss Economic Resurgence Fund 9 Edelweiss ELSS Fund 10 Edelweiss Equity Opportunities Fund 12 Edelweiss Equity Savings Advantage Fund 13 Edelweiss Mid and Small Cap Fund 15 Edelweiss Prudent Advantage Fund 17 Edelweiss Tax Advantage Fund 19 Edelweiss Top 100 Fund 20 Balanced Fund Edelweiss Balanced Advantage Fund 22 Fixed Income Funds Edelweiss Banking & PSU Debt Fund 23 Edelweiss Bond Fund 24 Edelweiss Corporate Debt Opportunities Fund 25 Edelweiss Government Securities Fund 26 Edelweiss Liquid Fund 27 Edelweiss Short Term Income Fund 28 Edelweiss Treasury Fund 29 Exchange Traded Funds Edelweiss ETF - Nifty Bank 30 Edelweiss ETF - Nifty 50 31 Edelweiss ETF - Nifty Quality 30 32 Overseas Fund of Funds Edelweiss Asean Equity Offshore Fund 33 Edelweiss Emerging Markets Opportunities Equity Offshore Fund 34 Edelweiss Europe Dynamic Equity Offshore Fund 35 Edelweiss Greater China Equity Offshore Fund 36 Edelweiss US Value Equity Offshore Fund 37 Scheme Performance (Other than Direct Plan) 38 - 44 Scheme Performance (Direct) 45 - 49 SIP Performance 50 - 51 Schemes managed by Fund Manager 52 - 53 How to Read Factsheet 54 2 Market Commentary - Equity What we said last time – Globally, the US Federal Reserve meeting could Outlook for the coming month assume significance as investors would assess the tone of monetary policy Globally, statements and policies of the newly elected President as he assumes action and its future implications. -

Flash Report Indian Truck & Bus Market 3Rd Quarter, October – December 2017 Published on February 2018

Special edition 003 Flash Report Indian Truck & Bus Market 3rd Quarter, October – December 2017 Published on February 2018 Published by RACE Innovations Pvt ltd, Chennai © 2018 RACE Innovations Pvt ltd. All rights reserved www.raceinnovations.in Contents Foreword 3 Key Highlights of the Indian Commercial Vehicle Industry 4 Statistics Bus Market 10 Market Share Buses 11 Statistics Trucks 14 Market Share Trucks 16 Statistics Haulage Tractor (Tractor-Semi Trailer/Trailer) 18 Forecasted Q4 (Jan-Mar) of 2017-18 20 RACE Product Offerings 21 Excon 2017 show a brief 22 2 www.raceinnovations.in © 2018 RACE Innovations Pvt ltd. All rights reserved Foreword Post Demonetization discords, GST (Goods and Service Tax) nearing stabilization impacting spurt in truck sales numbers during the third quarter FY2017/18(Oct-Dec) reflecting 54% growth compared to the previous year quarter FY2016/17 (Oct-Dec). It is being observed that more Foreign direct investments (FDI) is been attracted towards this sector paving way to several foreign companies to form partnership with Indian players in turn steepening demand for high performance trucks. On the contrary the seasonal bus sales continues to witness 20% drop in sales compared to previous year quarter FY2016/17(Oct-Dec), mainly owing to weaker market demands. Weaker demands are due to pre-bookings done in the previous years aimed to negate the upsurge in bus & coach price owing to various factors like the bus body code, emission change over, other regulatory fitments getting mandated. We expect the situation to continue in the next quarters until we have new purchase mandates from government like the JnNURM schemes of the last season. -

Pricol Limited(Erstwhile Pricol Pune Limited)

Pricol Limited(erstwhile Pricol Pune Limited) April 12, 2019 Summary of rated instruments Previously Rated Current Rated Instrument* Amount Amount Rating Action (Rs. crore) (Rs. crore) Term loans 31.66 148.26 [ICRA]BBB(Negative); revised Long-term fund-based 145.00 145.00 from [ICRA]BBB+ (Stable) Long-term unallocated 77.34 0.74 Short-term non-fund based 21.00 21.00 [ICRA]A3+; revised from Short-term non-fund based (sublimit) (105.00) (105.00) [ICRA]A2 Total 275.00 315.00 *Instrument details in Annexure – I Rationale The revision in ratings considers the deterioration in Pricol’s consolidated financial profile during 9M FY2019 because of weak performance of the Brazil subsidiary, the recently acquired wiping systems business and the standalone entity in India. The company’s consolidated operating margins stood at 1.2% for 9M FY2019 (1.7% for FY2018), significantly weaker than the company’s and ICRA’s earlier estimates. At the net level, Pricol’s consolidated losses widened to 5.5% during 9M FY2019 from 3.0% in FY2018, as against a net turnaround expected earlier for FY2019. The margins were predominantly impacted by a) increase in input/raw material costs in the standalone business due to higher commodity prices, surge in prices of electronic components with global shortage, and adverse forex movement; b) lower-than- anticipated revenues in the Brazil subsidiary and consequent weak absorption of fixed costs; and c) weak performance of the Czech wiping systems business with slowdown in European PV sales in the recent months and Pricol’s inability to improve the entity’s cost structure, among others. -

Y ™Pnco/ Passion to Excel

PR/COL LIMITED (Formerly Pricol Pune Limited] Y ™pnco/ Passion to Excel 109, Race Course, Coimbatore 641018 , India '- +91 422 4336000 ltm +91 422 4336299 ~ [email protected] e pricol . com CIN : L34200TZ2011 PLC02219 4 • CUSTOMERS • EMPLOYEES • SHAREHOLDERS ;..._ SUPPLIERS PL/SEC/TGT/2018-19/100 Thursday,August23, 2018 Corporate Relationship Department The Manager BSE Limited Listing Department 1st Floor, New Trading Ring National Stock Exchange of India Limited Rotunda Building, P J Towers, "Exchange Plaza' , C-1 , Block G Dalal Street, Fort Bandra-Kurla Complex, Mumbai 400 001 Sandra (E), Mumbai - 400051 Scrip Code: 540293 Scrip Code : PRICOLLTD Dear Sir, Sub: 7thAnnual General Meeting - (1) AGM Proceedings (2) Presentation made at the Meeting We wish to inform you that the 7thAnnual General Meeting of the Company held on August 22, 2018 at Chamber Hall, Chamber Towers, 8/732, Avinashi Road, Coimbatore-641 018 and the business(es) mentioned in the notice of the 7th AGM dated 26th June, 2018 were transacted. In this regard we are enclosing the following : 1) Proceedings of AGM as required under Regulation 30, Part-A of Schedule-I II of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015. 2) Presentation made at the Annual General Meeting We request you to kindly take the same on record and acknowledge receipt. Thanking you, Yours faithfully, For Pricol Limited- i.~.Thamizhanban Company Secretary 1cs1· M.No: F7897 Encl: as above ISO14001 ISO/TS16949 OHSAS18001 BUREAU VERIT AS BUREAU VERITAS Certification Certification· Proceedings of the 7th Annual General Meeting of Pricol Limited held on Wednesday, the 22nd August 2018 at 4.30 p.m. -

Dependable Quality Partnering the 2-Wheeler Industry

Dependable Quality Partnering the 2-Wheeler Industry NNE INNE WI R W R AUTO MANUAL 2-WHEELER AUTO MANUAL 2-WHEELER National Engineering Industries Limited (NEIL) was founded in 1946 and is a manufacturer of Bearings under the brand NBC We belong to CK Birla Group (Group Revenue: $1.6 Bn) with diversified interests in Automotive, Construction, Consumer Goods and IT Sector We are India's largest manufacturer with production of 150 Mn Bearings (Ball Bearings, Taper Roller Bearings, DRAC and Railway Bearings) annually in over 1000 sizes from 10mm bore to 2000mm OD Our four state-of-the-art Manufacturing Facilities and Technology Centre are one of the largest in Asia We are one of the preferred suppliers to OEMs and After Market in India as well as in EU and NAFTA We are winners of the DEMING GRAND PRIZE for Quality in 2015 and all our plants are ISO/TS/OHSAS certified We are awarded rating of 5A2 by Dun & Bradstreet indicating strong financial capability AUTO MANUAL 2-WHEELER Index Page No. Honda Motorcycles & Scooter India Pvt. Ltd 01 Suzuki Motorcycle India Ltd. 06 Yamaha Motor India Pvt. Ltd. 09 Hero Motor Corp Ltd. 13 Bajaj Auto Ltd. 17 Piaggio 22 Royal Eneld Ltd. 22 TVS Motor Company 25 Mahindra Two Wheelers Ltd. 29 Application Bearing Location OE Part Number Bearing Number Per O Honda Motorcycles & Scooter India Pvt. Ltd. Activa New Engine Cam Shaft RH 91007-KWP -6000-R2 6904 1 Engine Cam Shaft LH 96100-6000-300 6000 1 Engine Crank Shaft LH 91002-KWP-D030-Y3 6007 1 Engine Crank Shaft RH 91001-KWP-D030-Y3 6205Z 1 Transmission Drive Shaft