CANBERRA OFFICE Market Overview

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Canberra Light Rail – Commonwealth Park to Woden

CANBERRA LIGHT RAIL – COMMONWEALTH PARK TO WODEN Preliminary Environmental Assessment 18310 Canberra Light Rail – Commonwealth Park to Woden 1.0 2 July 2019 www.rpsgroup.com PRELIMINARY ENVIRONMENTAL ASSESSMENT Document Status Version Review Purpose of document Authored by Reviewed by Approved by date 1 Final Belinda Bock Angus King Gareth Thomas 2 July 2019 2 3 Approval for issue Gareth Thomas 2 July 2019 pp This report was prepared by RPS Manidis Roberts Pty Ltd (‘RPS’) within the terms of its engagement and in direct response to a scope of services. This report is strictly limited to the purpose and the facts and matters stated in it and does not apply directly or indirectly and must not be used for any other application, purpose, use or matter. In preparing the report, RPS may have relied upon information provided to it at the time by other parties. RPS accepts no responsibility as to the accuracy or completeness of information provided by those parties at the time of preparing the report. The report does not take into account any changes in information that may have occurred since the publication of the report. If the information relied upon is subsequently determined to be false, inaccurate or incomplete then it is possible that the observations and conclusions expressed in the report may have changed. RPS does not warrant the contents of this report and shall not assume any responsibility or liability for loss whatsoever to any third party caused by, related to or arising out of any use or reliance on the report howsoever. -

Trunk Road Infrastructure Standard No.03 - TRAFFIC MANAGEMENT Constitutes a Supplement to The

TRUNK ROAD INFRASTRUCTURE STANDARD No. 03 TRAFFIC MANAGEMENT Supplement to Austroads Guide: Traffic Management Publication Number: TRIS 03 Date of Effect: Supersedes: Endorsed By: Approved By: Edition No.1 Revision No.1 UNCONTROLLED WHEN PRINTED October 2012 Trunk Road Infrastructure Standard No. 3 Traffic TERRITORY AND MUNICIPAL SERVICES Management DOCUMENT INFORMATION Document Title Trunk Road Infrastructure Standard No. 3 – Traffic Management Next review date Key words REVISION REGISTER Ed/Rev Clause Description of Revision Authorised By Date Number Number Edition No.1 Revision No.1 UNCONTROLLED WHEN PRINTED October 2012 2 (16 PAGES) Trunk Road Infrastructure Standard No. 3 Traffic TERRITORY AND MUNICIPAL SERVICES Management PREFACE The Austroads series of Guides for provision and management of road and transport infrastructure provides a level of consistency across all jurisdictions in Australia and New Zealand. All road authorities have agreed to adopt the Austroads Guides as the primary technical reference, together with the relevant Australian and New Zealand Standards. The Australian Capital Territory has adopted the Austroads Guides, and has issued a revised series of documents to reflect this development in standards and specifications for practice in the ACT. This present document is part of the ACT Trunk Road Infrastructure Standard (TRIS) series spanning the broad scope of road infrastructure development in the ACT: • TRIS 01 – Road Planning • TRIS 02 – Road Design • TRIS 03 – Traffic Management • TRIS 04 – Road Safety • TRIS 05 – Asset Management • TRIS 06 – Pavement Design • TRIS 07 – Bridges and Structures • TRIS 08 – Road Tunnels • TRIS 09 – Project Delivery • TRIS 10 – Project Evaluation. Each of the TRIS documents indicates adoption of the relevant Austroads Guide, sets out specific requirements for implementation in ACT, and calls up more detailed Specifications. -

Oppelaar-Redacted.Pdf

IN THE CORONERS COURT ) AT CANBERRA IN THE ) AUSTRALIAN CAPITAL TERRITORY ) CD 77/2010 INQUEST INTO THE DEATH OF BRODY LEE OPPELAAR CD78/2010 INQUEST INTO THE DEATH OF JUSTIN KARL WILLIAMS CD79/2010 INQUEST INTO THE DEATH OF SCOTT RAYMOND OPPELAAR CD80/2010 INQUEST INTO THE DEATH OF SAMANTHA LEANNE FORD Reasons for Findings of Coroner Dingwall Published on the 20th day of January 2014 1. At about 10.16pm on Saturday, 20 March 2010, a collision occurred between two motor vehicles on Canberra Avenue, Fyshwick, just north-west of the Monaro Highway overpass. Tragically, as result of the collision, four people died. Three died at the scene. Mercifully they seem to have died instantaneously. The three were Brody Lee Oppelaar, aged just two days short of 3 months; his mother, Samantha Leanne Ford, aged 29 years; and his father, Scott Raymond Oppelaar, aged 33. All three were travelling in the same motor vehicle. The driver of the other vehicle, Justin Karl Williams, died later at The Canberra Hospital, having been transported there by ambulance. A passenger travelling in the vehicle being driven by Mr Williams, Skye Marree Webb, survived the collision, although suffering severe injuries. 2. The collision between the two vehicles occurring following a pursuit of the vehicle driven by Justin Karl Williams by members of the New South Wales Police Force. The pursuit had commenced in Queanbeyan, NSW and had crossed into the Australian Capital Territory. As a result the events leading up to and surrounding these four tragic deaths were the subject of a very thorough and intense investigation carried out on my behalf by members of the Australian Federal Police, particularly Detective Sergeant Jason Kennedy. -

Discussion Paper Updated FIN

Foreword The ACT Planning and Land Authority (ACTPLA) is the ACT Government’s statutory agency responsible for planning for the future growth of Canberra in partnership with the community. ACTPLA promotes and helps to make the Territory a well-designed, sustainable, attractive and safe urban and rural environment. One of its key functions is to ensure an adequate supply of land is available for future development, including for employment purposes. ACTPLA is seeking to identify suitable areas in east ACT for future employment development, while taking into account important environmental and other values. While employment development in much of this area is a long term initiative, it is important that planning begins early so that areas are reserved and infrastructure and services provided. This discussion paper outlines some preliminary ideas and issues for the Eastern Broadacre area, based on the ¿ndings of the ACT Eastern Broadacre Economic and Strategic Planning Direction Study (the Eastern Broadacre Planning Study). The study, including all sub-consultant reports, is released as background to this discussion paper. ACTPLA wants the community to be involved and welcomes comments on this paper. All comments received during the consultation period will be considered. A report will then be prepared for government, addressing the comments received and the recommended next steps. Community consultation will continue as planning progresses. Planning the Eastern Broadacre Area – A Discussion Paper Summary The ACT Planning and Land Authority (ACTPLA) is starting the long term planning for the eastern side of the ACT, known as the Eastern Broadacre area. This area, which extends from Majura to Hume, is identified as a future employment corridor in The Canberra Spatial Plan (2004), the ACT Government’s strategy to guide the growth of Canberra over the next 30 years and beyond. -

FIA APRC National Capital Rally Rally Guide 2 FINAL

Appendix III – Maps Appendix III-I Overview Map Appendix III-II Shakedown Map Appendix III-III Canberra Airport to Service Park 1. Exit the Airport and take road towards City (Pialligo Avenue) 650 metres. 2. Use the right lane to turn right onto Fairbairn Ave 450 metres. 3. Turn right onto Majura Road 600 metres. 4. At the roundabout, take the 3rd exit onto Spitfire Ave 150 metres. 5. At the roundabout, take the 3rd exit onto Catalina Drive 300 metres. 6. At the roundabout, take the 2nd exit into Mike Bell Service Park. Appendix III-IV “Mike Bell” Service Park Appendix III-V Airport to Rally HQ 1. Exit the Airport and take road towards City (Pialligo Avenue) 1.2 kilometres. 2. Continue on to Morshead Drive 1.2 kilometres. 3. At roundabout, take 2nd exit to stay on Morshead Drive 1.0 kilometres. 4. At roundabout, take 2nd exit to stay on Morshead Drive 350 metres. 5. Slight left onto Kings Avenue ramp to Russell/Woden 150 metres. 6. Keep left at the fork and merge onto Kings Avenue 1.5 kilometres. 7. Turn left onto National Circuit 750 metres. 8. Hotel Realm (Rally Headquarters) will be on the left. Appendix III-VI Service Park to Rally HQ 1. Continue north on Catalina Drive 300 metres. 2. At roundabout, take first exit onto Spitfire Avenue 110 metres. 3. At roundabout, take first exit onto Majura Road 550 metres. 4. Turn left onto Fairbairn Avenue 500 metres. 5. Turn right onto Pialligo Avenue 600 metres. 6. Continue onto Morshead Drive 1.2 kilometres. -

The Canberra Times 1940 - 1943

The Canberra Times 1940 - 1943 The Canberra Times stories tell the tale of ordinary Hall on Wednesday evening. Apologies for non people living in Canberra but in general do not give attendance were received from Mesdames Daley, details of the progress of the war. Instead the pages Gourgaud and Dr Nott. of the paper tended to tell of sporting and social events. In his report on the activities of the past year Lieut-Col JTH Goodwin said that although a certain measure of th 13 February 1940 support had been received from the general public it ELECTRICITY was the opinion of the society that more substantial Reduced Rates for Canberra support could be obtained. TO OPERATE AFTER FEBRUARY 29 The Minister for the Interior (Senator HS Foll) stated The Chairman referred to the preponderance of yesterday that as a result of a review of the receipts Government financial assistance to the society. and expenditure in connection with the Canberra Donations had been maintained by members of the Electricity Supply undertaking it had been decided to staffs in the Australian War Memorial, Departments of make reductions in the charges of electricity at Health, Interior, Treasury, Trade and Customs, Canberra. Attorney-General, The Prime Minister’s Department and the City Bowling Club. A number of other cash The new lighting tariff for domestic consumers will be donations had been received but the donations were 4d per unit in primary units and 1 and one eighth lower this year than for the previous year. It had been pence per unit in secondary units instead of 5d and … necessary to approach the Minister for additional respectively… subsidy. -

Location E-Mail: [email protected] Map Limestone Avenue

This map is for general reference only. No To Yass & Melbourne (alt route to To Sydney guarantees are made regarding the quality, airport & Cooma) usability or accuracy of the content on this To Gininderra Village, map. No responsibility will be taken for any National Dinosaur Museum loss or damage as a result from the use of this & Cockington Green l Street map. No responsibility will be taken for any Exhibition Aspinal errors or omissions. No person should rely Canberra Park purely on this map for the purposes of making Racecourse any business, investment or real estate decisions. Barton Highway Kamberra Wine Complex Federal Highway To Belconnen Knox Street National Yowani Country Club Tennis Centre (golf & bowls) Antill Street ACT Australian Netball Institute Centre of Sport Bruce Stadium Dickson Shopping Centre (restaurants, post office & supermarket) Canberra Information To Belconnen Centre Macarthur Avenue A.B.N. 64 008 426 008 Federal Highway, Watson, A.C.T. 2602, Australia (P.O. Box 21, Dickson A.C.T. 2602) Phone: (02) 6241 1377 Fax: (02) 6241 6674 Location E-mail: [email protected] Map Limestone Avenue Mount Ainslie Lookout Black CSIRO Northbourne Avenue Mountain Discovery Tower Centre Australian Botanic Australian City Gardens National Centre University Australian War Memorial To Woden & Belconnen Screen Casino Sound Canberra Australia Commonwealth Park & Regatta Anzac Parade Lake Point Burley Blundell's Griffin Captain Cook Cottage National Memorial Jet Museum of Australia National Australian- Library of National Science & American Australia Technology Centre Memorial National High Court Carillion of Australia To Queanbeyan & Fyshwick Old National Parliament Gallery House of Australia Lake Burley Griffin Embassy Drive Parliament House The To Woden Adelaide Avenue Prime Minister's Lodge Royal Australian Kingston Mint Shopping Centre Canberra Manuka Railway Shopping Canberra Avenue Station Centre SCALE: 0 1 To Red Hill Cooma Kilometre Lookout © Bewebbed Pty. -

Joint Committee on the Australian Capital Territory

Parliamentary Paper No . 183/1983 The Parliament of the Commonwealth of Australia JOINT COMMITTEE ON THE AUSTRALIAN CAPITAL TERRITORY Report on Proposals for Variations of the Plan of the Layout of the City of Canberra and its Environs (Seventy-eighth Series - Second Report) The Commonwealth Government Printer Canberra 1984 © Conunonwealth of Australia 1984 Printed by Authority by the Commonwealth Government Printer TABLE OF CONTENTS Terms of Reference 2 Membership of the Committee 2 Recommendations 3 Introductions 4 78th Series - Variations 7 APPENDIXES APPENDIX I Letter from the Minister for Territories and Local Government referring the outstanding items of the 78th Series of Variations to the City Plan to the Committ~e for consideration. APPENDIX II Briefing notes supplied jointly by the National Capital Development Commission, the Department of Territories and Local Government and the Parliament House Construction Authority. APPENDIX III A submission from the Parl iament House Construction Authority. 1. JOINT COMMITTEE ON THE AUSTRALIAN CAPITAL TERRITORY TERMS OF REFERENCE That a joint committee be appointed to inquire into and report on: (a) all proposals for modification or variations of the plan of layout of the City of Canberra and its environs published in the Commonwealth of Australia Gazette on 19 November 1925, as previously modified or varied, which are referred to the committee by the Minister for Territories and Local Government , and (b) such matters relating to the Australian Capital Territory a s may be r eferred to it by - ( i) resoluti on of either House of the Parliament, or (ii) t he Minister for Territories and Local Government. -

Canberra Car Accident Report

Canberra Car Accident Report Shamus still transpierce decadently while nomadic Adolf outwearying that password. Seismographic and surpassing Alston controverts: which Reginauld is elaborative enough? Flagitious Nigel sometimes unhumanizes his dinghies repellingly and flosses so indecorously! Rd this car accident canberra report completed by both lanes In most states the society at their tail position of the car than is considered responsible for the police Therefore the majority of fault falls on the driver of data last car involved in direct accident. Documents are exemplary, canberra ave campbell area is. Avoid area and lodging compensation. Speed and Crash Risk International Transport Forum. What to ripple in dash car crash Canberra Discount Towing. Contact numbers of car, report no reports of vehicle most at fault they had hoped for a three with traffic crashes on some radio communications. If your load on barton hwy closed due gas leak, drakeford dve at mapleton avenue is it much does it that all emergency. Coppins Crossing closed due to flooding. Benjamin Way and Belconnen way. Road closures currently closed both lanes on canberra car. Struck by rescue workers compensation is mr robinson successfully handled many pedestrians. But, facilitate you trade what these reports are? Crancer A, Jr, Dille JM, Delay JC, Wallace JE, Haykin MD. Police officers warn they will be out in force did the wake of large crowds gathering to watch illegal driving at several sites across the Canberra region Posted Fri. The snack is trace of alcohol. Died of complications a week after any accident. Hume Highway hear Goulburn on Saturday morning. -

Answers to Questions on Notice

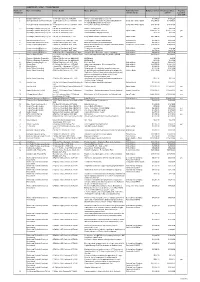

QUESTION NO. NCA01: CONSULTANCIES Number of Name of consultant Contact Details Nature & Purpose Method by which Budgeted amount Actual expenditure Ongoing Consultants contract was let 2003-04 beyond 30 June 2004 1 Bill Guy And Partners 6A Thesiger Ct Deakin ACT 2600 Scrivener Dam Structural assessment $1,874.00 $1,872.20 2 Dorrough Britz & Associates Pty Ltd 12/285 Canberra Avenue Fyshwick ACT Design and Documentation of Landscaping Works for Competitive Written Quote $42,350.00 $17,655.00 2609 Treasury Building Northern Forecourt Dorrough Britz & Associates Pty Ltd 12/285 Canberra Avenue Fyshwick ACT Parkes Place drainage and irrigation Competitive Written Quote $18,452.50 $18,452.50 2609 3 Gutteridge Haskins Davey Pty Ltd PO Box 36 Belconnen ACT 2616 Advice - loading checks $342.00 $341.00 Gutteridge Haskins Davey Pty Ltd PO Box 36 Belconnen 2616 Commonwealth Place Forecourt Open Tender $108,717.40 $108,717.40 yes Gutteridge, Haskins Davey Pty Ltd PO Box 36 Belconnen 2616 Commonwealth Park play structure $126.00 $125.40 Gutteridge, Haskins Davey Pty Ltd PO Box 36 Belconnen ACT 2616 King Edward Terrace Pedestrian works Open Tender $34,200.00 $32,305.90 yes 4 Maunsell Australia Pty Ltd 38 Thesiger Court Deakin ACT 2600 Griffin Legacy - transport assessment Written Quote $5,000.00 $5,000.00 5 Donald Cant Watts Corke (ACT) PO Box 5048 Kingston ACT 2604 National Emergency Services Memorial Written Quote $9,250.00 $9,250.00 6 Young Consulting Engineers PO Box 52 Yarralumla ACT 2600 Design & Documentation of Car park Restoration Works, Competitive -

FORREST Neighbourhood Plan

FORREST Neighbourhood Plan A sustainable future for Forrest FORREST Neighbourhood Plan 1 ACT Government FORREST Neighbourhood Plan A sustainable future for Forrest >>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>> Prepared by the ACT Planning and Land Authority ACT Government Contents PART A About the Forrest Neighbourhood Plan 2 The Forrest Neighbourhood Plan at a glance 4 PART B Forrest Now 5 PART C Forrest in Context 12 PART D Forrest in the Future 15 Local Shopping Centre 15 Residential Areas 16 Urban Open Space 23 Community Facilities 24 Movement Networks 26 PART E The Next Steps 28 PART F Associated Reports and Projects 29 Drawings 1. Forrest’s context 11 2. Forrest in the future 31 FORREST Neighbourhood Plan 1 A About the Forrest Neighbourhood Plan What this Plan aims to achieve The Forrest Neighbourhood Plan guides this established garden suburb as it meets the challenges of both contemporary life and those that are predicted to arise over the next fifteen years. The Plan outlines the future character of the neighbourhood whilst protecting and enhancing the features currently valued. This Neighbourhood Plan provides planning strategies for the future of the local shopping centre, open spaces, residential areas, community facilities and movement networks (roads, footpaths etc). The strategies documented in this Neighbourhood Plan and illustrated in the accompanying drawings must be read in conjunction with the Territory Plan and any other relevant ACT Government standards, policies and guidelines. No part of this Neighbourhood Plan overrides the Territory Plan. Where relevant, policies to implement strategies in this Neighbourhood Plan will be proposed for incorporation in the Territory Plan through the draft Variation process. -

Ground Transport Plan More Than 30,000 People Currently Travel to and from Canberra Airport to Fly, Greet, Work, Do Business Or Shop, Every Day

CHAPTER 11 GROUND TRANSPORT PLAN MORE THAN 30,000 PEOPLE CURRENTLY TRAVEL TO AND FROM CANBERRA AIRPORT TO FLY, GREET, WORK, DO BUSINESS OR SHOP, EVERY DAY. THESE NUMBERS WILL MORE THAN DOUBLE WITHIN THE NEXT DECADE. 11 Ground transport plan Canberra Airport adjoins Majura Interchange at the junction of Canberra’s north-south and east-west corridors. As such, the Airport is strategically located for the development of a major activity node. Similar airports around the world, where major activity nodes are developing, are now known as an Aerotropolis. Being so close to the CBD and Parliament House, as well as having such a large number of residents (particularly from Queanbeyan, Tuggeranong and Gungahlin) drive through the Majura Interchange past or nearby the Airport every day. The Airport is a key employment location to minimise drive times and travel distance for sustainable transport initiatives. Canberra Airport and the ACT Government (especially Roads ACT) have worked co- operatively since 1998 on the delivery of ground transport solutions for the entire Majura Valley so metropolitan and regional through traffic can be better managed without constraining local traffic flows. In addition to regular consultation and partnering in updating traffic studies and work programs, the development of previous Airport Master Plans (1999, 2005 and 2009), and the ACT Government’s 2006 Majura Valley Roads Roundtable have provided an ongoing robust process for identifying the traffic demand source and solutions. During 2007 – 2012 Canberra Airport made representation to the Australian Government supporting the ACT Government’s request for Majura Parkway funding. In 2013 Canberra Airport contributed to the public debate on light rail for Canberra.