Bank of Sustainability

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ililllililffiill$Iilmmfiil 3 1379 0T 158383 9

ililllililffiill$iilmmfiil 3 1379 0t 158383 9 THAI TOURISTS' SATISFACTION WI.IEN TRAVELING AROUND RATTANAKOSIN ISLAND BY TRAM JEERANUN KIJSAWANGWONG Adviso r: Assistant Professo r Prceyacha t Utta mayodh in a A RESEARCII PAPER SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER ARTS ,IN OF ENGLISH FOR CAREERS LANGUAGE INSTITUTE, THAMMASAT UNIVERSITY BANGKOK, TIIAILAND MARCH 2OO7 %*/ /,1o 8i,,7,,/;,*cn/a - ," 2i 1.3. tm . ABSTRACT This research is conducted for the academic purpose of strongly focusing on the tourism and hospitality industry. The centers of attention for this study are understanding as well as discovering the motivation that encourages people to use the Tram's service and evaluate Thai tourist satisfaction toward traveling around Rattanakosin island by tram. Obtaining this information will help to promote Thai Tourism and generate more awareness in Thai people to travel more in their territory. Moreover, the provider of service to the tram can use this database to improve their service quality. The main objective of this research is to measure the degree of Thai tourist satisfaction with services and facilities when traveling around Rattanakosin Island by tram. The sample size of this research is 100 Thai tourists, who travel around Rattanakosin Island by tram in December,2006. The subject will be chosen by the accidental sampling method. The instrument used in this research is the self- administered questionnaire. In addition, the instrument in data analysis is the Statistical Package for Social Sciences (SPSS) version I I The respondents agreed, that the reason that they chose to travel around Rattanakosin Island by tram is because they did not want to walk, which makes them tired. -

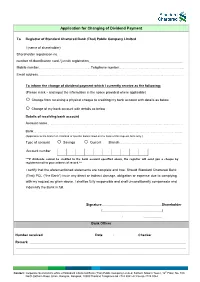

Application for Changing of Dividend Payment

Application for Changing of Dividend Payment To Registrar of Standard Chartered Bank (Thai) Public Company Limited I (name of shareholder) Shareholder registration no. number of identification card / juristic registration Mobile number………………………………………………….……….....Telephone number…………………..……………………………………….……………….. Email address……………………………………………………………………………………………………………….……………………………………………………………… To inform the change of dividend payment which I currently receive as the following: (Please mark and input the information in the space provided where applicable) Change from receiving a physical cheque to crediting my bank account with details as below Change of my bank account with details as below Details of receiving bank account Account name………………………………………………………………………………………………………………………………………………………..…….….. Bank………………………………………………………………………………………………………………………………………………………..……………………….... (Applicable to the branch in Thailand of specific banks listed on the back of this request form only.) Type of account Savings Current Branch…………………………………………………….……………………. Account number ***If dividends cannot be credited to the bank account specified above, the registrar will send you a cheque by registered mail to your address of record.*** I certify that the aforementioned statements are complete and true. Should Standard Chartered Bank (Thai) PCL (“the Bank”) incur any direct or indirect damage, obligation or expense due to complying with my request as given above. I shall be fully responsible and shall unconditionally compensate and indemnify the Bank in full. Signature Shareholder ( ) / / Bank Officer Number received Date / / Checker Remark Contact: Corporate Secretariat’s office of Standard Chartered Bank (Thai) Public Company Limited, Sathorn Nakorn Tower, 12th Floor, No. 100 North Sathorn Road, Silom, Bangrak, Bangkok, 10500 Thailand Telephone 66 2724 8041-42 Fax 66 2724 8044 Documents to be submitted for changing of dividend payment (All photocopies must be certified as true) For Individual Person 1. -

THE ROUGH GUIDE to Bangkok BANGKOK

ROUGH GUIDES THE ROUGH GUIDE to Bangkok BANGKOK N I H T O DUSIT AY EXP Y THANON L RE O SSWA H PHR 5 A H A PINKL P Y N A PRESSW O O N A EX H T Thonburi Democracy Station Monument 2 THAN BANGLAMPHU ON PHE 1 TC BAMRUNG MU HABURI C ANG h AI H 4 a T o HANO CHAROEN KRUNG N RA (N Hualamphong MA I EW RAYAT P R YA OAD) Station T h PAHURAT OW HANON A PL r RA OENCHI THA a T T SU 3 SIAM NON NON PH KH y a SQUARE U CHINATOWN C M HA H VIT R T i v A E e R r X O P E N R 6 K E R U S N S G THAN DOWNTOWN W A ( ON RAMABANGKOK IV N Y E W M R LO O N SI A ANO D TH ) 0 1 km TAKSIN BRI DGE 1 Ratanakosin 3 Chinatown and Pahurat 5 Dusit 2 Banglamphu and the 4 Thonburi 6 Downtown Bangkok Democracy Monument area About this book Rough Guides are designed to be good to read and easy to use. The book is divided into the following sections and you should be able to find whatever you need in one of them. The colour section is designed to give you a feel for Bangkok, suggesting when to go and what not to miss, and includes a full list of contents. Then comes basics, for pre-departure information and other practicalities. The city chapters cover each area of Bangkok in depth, giving comprehensive accounts of all the attractions plus excursions further afield, while the listings section gives you the lowdown on accommodation, eating, shopping and more. -

1 Banpu Public Company Limited 2

Signatory Companies of Thailand's Private Sector Collective Action Coalition Against Corruption's Declaration of Intent No. Company 1 Banpu Public Company Limited 2 Bualuang Securities Public Company Limited 3 Bangkok Bank Public Company Limited 4 BBL Asset Management Company Limited 5 BBV Systems Company Limited 6 Bangchak Petroleum Public Company Limited 7 Bumrungrad Hospital Public Company Limited 8 Central Plaza Hotel Public Company Limited 9 CIMB Thai Bank Public Company Limited 10 Central Pattana Public Company Limited 11 Total Access Communication Public Company Limited 12 Eastern Water Resources Development and Management Public Company Limited 13 Electricity Generating Public Company Limited 14 Kasikornbank Public Company Limited 15 Kiatnakin Bank Public Company Limited 16 KPMG Phoomchai Business Advisory Company Limited 17 Krung Thai Bank Public Company Limited 18 Kang Yong Electric Public Company Limited 19 MBK Public Company Limited 20 MCOT Public Company Limited 21 MFEC Public Company Limited 22 Nation Multimedia Group Public Company Limited 23 Pfizer (Thailand) Limited 24 Phatra Capital Public Company Limited 25 Pranda Jewelry Public Company Limited Signatory Companies of Thailand's Private Sector Collective Action Coalition Against Corruption's Declaration of Intent No. Company 26 PTT Public Company Limited 27 PTT Exploration and Production Public Company Limited 28 PricewaterhouseCoopers Thailand 29 Sabina Public Company Limited 30 Somboon Advance Technology Public Company Limited 31 Siam Commercial Bank Public Company -

BANGKOK 101 Emporium at Vertigo Moon Bar © Lonely Planet Publications Planet Lonely © MBK Sirocco Sky Bar Chao Phraya Express Chinatown Wat Phra Kaew Wat Pho (P171)

© Lonely Planet Publications 101 BANGKOK BANGKOK Bangkok In recent years, Bangkok has broken away from its old image as a messy third-world capital to be voted by numerous metro-watchers as a top-tier global city. The sprawl and tropical humidity are still the city’s signature ambassadors, but so are gleaming shopping centres and an infectious energy of commerce and restrained mayhem. The veneer is an ultramodern backdrop of skyscraper canyons containing an untamed universe of diversions and excesses. The city is justly famous for debauchery, boasting at least four major red-light districts, as well as a club scene that has been revived post-coup. Meanwhile the urban populous is as cosmopolitan as any Western capital – guided by fashion, music and text messaging. But beside the 21st-century façade is a traditional village as devout and sacred as any remote corner of the country. This is the seat of Thai Buddhism and the monarchy, with the attendant splendid temples. Even the modern shopping centres adhere to the old folk ways with attached spirit shrines that receive daily devotions. Bangkok will cater to every indulgence, from all-night binges to shopping sprees, but it can also transport you into the old-fashioned world of Siam. Rise with daybreak to watch the monks on their alms route, hop aboard a long-tail boat into the canals that once fused the city, or forage for your meals from the numerous and lauded food stalls. HIGHLIGHTS Joining the adoring crowds at Thailand’s most famous temple, Wat Phra Kaew (p108) Escaping the tour -

Shopping in Bangkok

SHOPPING IN BANGKOK Bangkok is one of Southeast Asia’s most popular shopping centers. Locally produced products are the best buys: hill tribe embroidered cottons, wood carvings, jewelry, CDs/DVDs, watches, porcelain, silk and tailoring of clothes are most popular. If you can’t buy it in Thailand, you can’t buy it! Shopping Areas: • Silom Village: 286 Silom Road near Rama IV. Charming shopping plaza with handicrafts, silk, clothes, antiques, shows. • Mah Boon Krung Center: Phayathai and Rama 1 Rd. Clothes and accessories. Tokyo Dept Store, two cinemas and fast-food places. • River City Shopping Center: Adjacent to Royal Orchid Sheraton, connected by a short bridge. 2370077-8. Arts, antiques, tailors, hair salon, jewelers. • Siam Centre/Discovery Centre: Siam Square, Rama 1 and Phyathai Rds. Two connected plazas. A 10-15 minute walk from Central World Plaza (formerly World Trade Center). • Seacon Square: Srinakarin Rd, other side of the city. One of the largest shopping plazas in Asia. Robinson’s, Lotus department stores, YOYO Land, indoor amusement park, food court, supermarket and 14 theaters! Dry cleaners in the basement. • Baiyoke Plaza & Pratunam Market: Near Indra Regent Hotel, Pratunam. Great clothes bargains, cheapest t-shirts in Bangkok. • Emporium: Sukhumvit Rd next to Queen Sirikit Park. Newish and one of the ‘glitziest’ shopping centers in Bangkok. Small designer outlets, a big department store and supermarket. • Gaysorn Plaza: Ploenchit Rd, opposite World Trade Center. Upmarket plaza with well-known designer stores and good restaurants. Planet Hollywood next door. • Oriental Place: Soi Charoen Krung 38. 2660186-95. Behind Oriental Hotel, worth going for arts and antiques. -

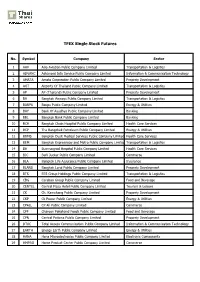

Stock Comparison

TFEX Single Stock Futures No. Symbol Company Sector 1 AAV Asia Aviation Public Company Limited Transportation & Logistics 2 ADVANC Advanced Info Service Public Company Limited Information & Communication Technology 3 AMATA Amata Corporation Public Company Limited Property Development 4 AOT Airports Of Thailand Public Company Limited Transportation & Logistics 5 AP AP (Thailand) Public Company Limited Property Development 6 BA Bangkok Airways Public Company Limited Transportation & Logistics 7 BANPU Banpu Public Company Limited Energy & Utilities 8 BAY Bank Of Ayudhya Public Company Limited Banking 9 BBL Bangkok Bank Public Company Limited Banking 10 BCH Bangkok Chain Hospital Public Company Limited Health Care Services 11 BCP The Bangchak Petroleum Public Company Limited Energy & Utilities 12 BDMS Bangkok Dusit Medical Services Public Company Limited Health Care Services 13 BEM Bangkok Expressway and Metro Public Company Limited Transportation & Logistics 14 BH Bumrungrad Hospital Public Company Limited Health Care Services 15 BJC Berli Jucker Public Company Limited Commerce 16 BLA Bangkok Life Assurance Public Company Limited Insurance 17 BLAND Bangkok Land Public Company Limited Property Development 18 BTS BTS Group Holdings Public Company Limited Transportation & Logistics 19 CBG Carabao Group Public Company Limited Food and Beverage 20 CENTEL Central Plaza Hotel Public Company Limited Tourism & Leisure 21 CK Ch. Karnchang Public Company Limited Property Development 22 CKP Ck Power Public Company Limited Energy & Utilities 23 CPALL CP All Public Company Limited Commerce 24 CPF Charoen Pokphand Foods Public Company Limited Food and Beverage 25 CPN Central Pattana Public Company Limited Property Development 26 DTAC Total Access Communication Public Company Limited Information & Communication Technology 27 EARTH Energy Earth Public Company Limited Energy & Utilities 28 HANA Hana Microelectronics Public Company Limited Electronic Components 29 HMPRO Home Product Center Public Company Limited Commerce TFEX Single Stock Futures No. -

KTB: Krung Thai Bank Public Company Limited | Annual Report

A N U L R E P O T 2 0 1 3 K r u n g h a i B k c l . TRANS FORMA TION 35 Sukhumvit Road, Klong Toey Nua Subdistrict, Wattana District, Bangkok 10110 Tel : +662 255-2222 Fax : +662 255-9391-3 KTB Call Center : 1551 Swift : KRTHTHBK http://www.ktb.co.th Annual Report 2013 K T B T r a n s f o r m a t i o n This annual report uses Green Read paper for low-eye strain and is printed with soybean ink that reduces carbon dioxide emission and has light weight for less energy consumed in delivery. Produced by : Business Risk Research Department Risk Management Sector Risk Management Group Krung Thai Bank Pcl. Designed by : Work Actually Co., Ltd. Printed by : Plan Printing Co., Ltd. Transformation…for a Sustainable Growth KTB has transformed its internal operation process and improve people capability for greater efficiency in customer services and business expansion under accurate and efficient risk management that will lead to enhanced competitiveness and readiness to make a sustainable leap together with customers, society, shareholders and stakeholders. K T B T r a n s f o r m a t i o n KTB e-Certificate ของ่าย ได้เร็ว ขอหนังสือรับรอง นิติบุคคล การประกอบธุรกิจ คนต่างด้าว สมาคมและหอการค้า 4 KTB สินเชื่อ SME เพื่อรับงานภาครัฐ หนังสือคํ้าประกันทันใจ แค่ 1 วัน Net Free Zero รับได้เลย จาก KTB netbank แบบอั้นๆ หลบไปเลย....Net Free Zero ค่าธรรมเนียม ฟรี ไม่มีอั้น ตัวจริง! มาแล้ว Annual Report 2013 Krung Thai Bank Pcl. สินเชื่อกรุงไทย 3 สบาย สินเชื่อบุคคล ที่ ให้ ชีวิต มีแต่เรื่อง สบายๆ บริการโอนเงินต่างประเทศ มุมไหนใน โลก ก็ โอนถึง ใน 1 วัน 5 สินเชื่ออเนกประสงค์ -

1 Pricewaterhousecoopers Thailand 2 AIA Company Limited 3 AIA

Certified Companies of Thailand's Private Sector Collective Action Coalition Against Corruption No. Membership Company 1 PricewaterhouseCoopers Thailand 2 AIA Company Limited 3 AIA Company Limited (Non-Life Insurance) Thailand Branch 4 Siemens Limited Thailand 5 Somboon Advance Technology Public Company Limited 6 S & P Syndicate Public Company Limited 7 Siam Cement Public Company Limited 8 KPMG Phoomchai Business Advisory Company Limited 9 Intouch Holdings Public Company Limited 10 KasikornBank Public Company Limited 11 Kasikorn Asset Management Company Limited 12 Kasikorn Securities Company Limited 13 Bangchak Petroluem Public Company Limited 14 TISCO Financial Group Public Company Limited 15 TISCO Bank Public Company Limited 16 TISCO Securities Company Limited 17 TISCO Asset Management Company Limited 18 Bank of Ayudhya Public Company Limited 19 KPMG Phoomchai Audit Limited 20 KPMG Phoomchai Tax Limited 21 The Erawan Group Public Company Limited 22 GlaxoSmithKline (Thailand) Company Limited 23 Phatra Capital Public Company Limited 24 Krungsri Asset Management Company Limited 25 Krungsri Factoring Company Limited Certified Companies of Thailand's Private Sector Collective Action Coalition Against Corruption No. Membership Company 26 Ayudhya Capital Auto Lease Public Company Limited 27 Krungsri Securities Public Company Limited 28 Siam Realty and Services Company Limited 29 Ayudhya Development Leasing Company Limited 30 Ayudhya Capital Services Company Limited 31 Krungsri Ayudhya AMC Limited 32 Krungsriayudhya Card Company Limited 33 -

Thailand Itinerary

Culinary Educator: THAILAND: THE FLAVORS OF BANGKOK AND CHIANG MAI Chef Ian Chalermkittichai itinerary: ® THE CULINARY INSTITUTE OF AMERICA NOVEMBER Presented by Travel Programs 13-21, ® 2009 thailand itinerary Thailand is the land of smiles, spicy air, and tranquil countryside. A complex and historic past is reflected in their food, balanced by sweet, sour, spicy, and salty flavors. Join us for a mouth-watering journey where you will discover Ian’s favorite places, meet local cooks, taste fragrant street food, visit magnificent temples, and enjoy the boisterous river life and buzzing tuk-tuk’s. We will begin our tour at the best time of the year in the cultural center of Northern Thailand, Chiang Mai, at one of the most beautiful resorts and cooking schools in the world, the Four Seasons. The tour will come to an end in the bustling city of Bangkok, where we’ll stay at the luxurious Peninsula hotel. This is the ultimate journey for food lovers. Day 1: Friday, November 13 (Chiang Mai) You will arrive in Chiang Mai and transfer to the hotel. We will meet poolside for introductions and an overview of our culinary adventure. Dinner will follow at the hotel’s restaurant overlooking the Ping River. There we will savor delicious Thai cuisine against the riverside backdrop. Hotel: The Chedi, D Day 2: Saturday, November 14 (Chiang Mai) After breakfast we will tour Chiang Mai with Ian, stopping at the local market for an in-depth tour. There we will taste freshly made soy milk and hot donuts, and view some of the freshest produce in Asia. -

20210330-Lh-Ar2020-En.Pdf

Content Business Operation 01 Highlights of the Year 2020 7 02 Overview of Business Operation 8 03 Report of the Board of Directors 10 04 Operating Results 12 05 Business Highlights 13 06 Risk Factors 23 07 Supplementary Information 25 08 References 29 Management and Corporate Governance 09 Securities and Shareholders 32 10 Management Structure 34 11 The Nomination and Compensation Committee’s Report 51 12 Corporate Governance 52 13 Corporate Social Responsibilities Report 68 14 Internal Control and Risk Management 73 15 Risk Management and Sustainable Development Committee Report 75 16 Related Party Transactions 76 Financial Position and Operating Performance 17 Report on the Board of Directors’ Financial Responsibilities 82 18 The Audit Committee’s Report 83 19 Financial Statements 85 20 Financial Overview 187 21 Analysis of Operating Results and Financial Status 190 Other Related Information 22 Number of Registered Housing Unit in Bangkok Metropolitan Region During 2016 - 2020 208 23 Summary of Form 56-2’s Required Items in Land and Houses Plc.’s 2020 Annual Report 210 Investors can find additional securities issuer infomation in the Company’s From 56-1 disclosed at www.sec.or.th or the Company’s website at www.lh.co.th - Section 1 - Business Operation Land and Houses Public Company Limited Annual Report 2020 6 Section 1 Business Operation 2020 Highlights Land and Houses Public Co.,Ltd. & Subsidiaries 2020 2019 % Operating Result Number of active projects 94 86 9.3 Earning Ability Return on total revenues 23.01% 30.10% (7.1) Highlight -

29 June 2020 News No. 42/2020 The

Revenue Department News News No. : 42/2020 Date : 29th June 2020 Subject : The Revenue Department, partnered with 20 banks, has been launching an e-channel of tax payment without fees until the end of the year 2020 ................................................................................................................................................................................. From 1st July 2020 onwards, the Revenue Department has been partnering with 20 leading banks in order to waive fees of tax payment to a taxpayer who files a tax return via electronic channel (e-channel) until 31st December 2020. This will facilitate, be safe and reduce cost of travelling as well as risk of COVID-19 pandemic. Mrs. Sommai Siriudomset, Principal Advisor on Strategic Tax Administration (Energy Industry) spokesman of the Revenue Department revealed that “For helping an entrepreneur to reduce cost and promote e-filing and e-payment services, the Revenue Department together with 20 leading banks1 have been waiving bank transfer fees for making tax payments of every type of taxes via e-channel from now until 31st December 2020." The spokesman of the Revenue Department added that “The exclusion of fees of bank transfer via e-channel will encourage the entrepreneur to conduct financial transactions via e-channel without travelling and comply with Social Distancing policy helping to reduce risk from COVID-19 pandemic. This is a part of the Revenue Department’s intentions to upgrade the services in promoting the entrepreneurs and Thai people to conduct tax transactions from home or Tax from home.” Should there be any inquiries, please contact Area Revenue Office or RD Intelligence Center, Tel. 1161 as well as the alliance banks. ................................................................ Public Relations, Office of the Secretary The Revenue Department 90 Soi Phaholyothin 7, Phaholyothin Road, Bangkok 10400 RD Intelligence Center Tel.