Taconite Iron Ore NESHAP Economic Impact Analysis EPA-452/R-03-015 August 2003

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Northshore Mining Fact Sheet

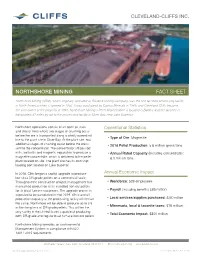

CLEVELAND-CLIFFS INC. NORTHSHORE MINING FACT SHEET Northshore Mining (NSM), which originally operated as Reserve Mining Company, was the first taconite processing facility in North America when it opened in 1956. It was purchased by Cyprus Minerals in 1989, and Cleveland-Cliffs became the sole owner of the property in 1994. Northshore Mining’s Peter Mitchell Mine is located in Babbitt and the taconite is transported 47 miles by rail to the processing facility in Silver Bay, near Lake Superior. Northshore operations consist of an open pit truck Operational Statistics and shovel mine where two stages of crushing occur before the ore is transported along a wholly owned rail • Type of Ore: Magnetite line to the plant site in Silver Bay. At the plant site, two additional stages of crushing occur before the ore is • 2018 Pellet Production: 5.6 million gross tons sent to the concentrator. The concentrator utilizes rod mills, ball mills and magnetic separation to produce a • Annual Rated Capacity (includes concentrate): magnetite concentrate, which is delivered to the pellet 6.0 million tons plant located on-site. The plant site has its own ship loading port located on Lake Superior. In 2018, Cliffs began a capital upgrade to produce Annual Economic Impact low silica DR-grade pellets on a commercial scale. Throughout the construction project, management has • Workforce: 529 employees maintained production of its standard iron ore pellets for its blast furnace customers. The upgrade project is • Payroll (including benefits) $85 million expected to be completed in mid-2019. While overall production capacity at the processing facility will remain • Local services/supplies purchased: $200 million the same, Northshore will be able to produce up to 3.5 • Minnesota, local & taconite taxes: $16 million million long tons of DR-grade pellets. -

Cleveland-Cliffs Inc Cleveland-Cliffs 1100 Superior Avenue 2004 Annual Report Cleveland, OH 44114-2589 Cleveland-Cliffs Inc Cleveland-Cliffs

Cleveland-Cliffs Inc Cleveland-Cliffs 1100 Superior Avenue 2004 Annual Report Cleveland, OH 44114-2589 www.cleveland-cliffs.com Cleveland-Cliffs Inc • 2004 Annual Report Company Profile Cleveland-Cliffs Inc DIRECTORS Cleveland-Cliffs Inc, headquartered in Cleveland, Ohio, is the largest producer of iron OFFICERS Director ore pellets in North America and sells the majority of its pellets to integrated steel Years With Since Company companies in the United States and Canada. The Company operates six iron 1997 John S. Brinzo (6) ore mines located in Michigan, Minnesota and Eastern Canada. 35 John S. Brinzo, 63 Chairman, President and Chief Executive Offi cer Chairman, President and Chief Executive Offi cer of the Company 1996 Ronald C. Cambre (2,4,6) Cliffs is in its 158th year of service to the steel industry. 4 David H. Gunning, 62 Former Chairman and Chief Executive Offi cer Vice Chairman Newmont Mining Corporation International mining company 32 William R. Calfee, 58 Executive Vice President-Commercial 1999 Ranko Cucuz (2,4,5) Former Chairman and Chief Executive Offi cer 23 Donald J. Gallagher, 52 Hayes Lemmerz International, Inc. Senior Vice President, International supplier of wheels to the auto industry Chief Financial Offi cer and Treasurer 2001 David H. Gunning (6) 4 Randy L. Kummer, 48 Vice Chairman of the Company CORE VALUES Senior Vice President-Human Resources 1986 James D. Ireland, III (1,3,5,6) 32 James A. Trethewey, 60 Managing Director Senior Vice President-Business Development Capital One Partners, Inc. Private equity investment fi rm SAFE PRODUCTION record production with: lack of injuries...good housekeeping and 25 Dana W. -

2013 Minnesota Mining Tax Guide

Mining Tax Guide SS J. A. Campbell in Taconite Harbor, ca. 1957-1964 (2005.0038.3318), Minnesota State Representative Fred A. Cina Papers, Iron Range Research Center, Chisholm, MN November 2013 2013 Distribution of Taconite Production Tax (2012 Production Year) Total Taconite Production Tax $102,633,021* Production tax is $2.465 per taxable ton. The average taxable tonnage was 38,310,339 tons. * Includes $8,428,275 from the State General Fund (22.0 cpt) cpt = cents per taxable ton Property tax Cities and townships School districts Counties IRRRB Other relief and misc. $13,893,864 $15,799,889 $14,270,998 $29,729,364 $16,493,071 $12,445,835 32.5 cpt 36.3 cpt 41.2 cpt 37.2 cpt 43.1 cpt 77.6 cpt City and Township Taconite School Regular IRRRB Fund** Taconite Economic Mining & Conc $0.0343 Fund** County Fund** Taconite Property $3,636,468 Development Fund Fund** $1,566,247 $9,000,065 Tax Relief $1,666,971 9.5 cpt $12,231,412 $2,066,752 4.1 cpt*** 23.5 cpt 31.9 cpt 5.4 cpt 4.4 cpt Regular School County Road and IRRRB $.1572 Fund** Bridge Fund** Fixed Fund Range Association Township Fund $6,908,326 $4,486,556 Public Works $1,252,520 of Municipalities & $1,223,128 18.0 cpt*** 11.7 cpt Projects 3.2 cpt Schools** 3.2 cpt $14,826,100 $137,802 Taconite Taconite 38.7 cpt Iron Range Higher Education Acct. 0.4 cpt Taconite railroad railroad $1,915,517 5.0 cpt Municipal Aid** $1,106,935 $784,377 2.0 cpt $6,355,475 2.9 cpt *** Producer Grant Hockey 16.6 cpt & Loan Fund Hall of Fame Building $3,176,600 $76,621 Maintenance Fund 8.3 cpt 0.2 cpt Taconite railroad $1,506,072 $591,142 3.9 cpt IRR Educational 1.5 cpt Revenue Bonds Taconite $1,411,925 Referendum** 3.7 cpt Mining effects** $3,091,236 $1,758,238 8.1 cpt Taconite Env. -

! 1! ! ! FINAL REPORT to the LEGISLATURE MINNESOTA TACONITE WORKERS HEALTH STUDY DATE: November 24, 2014 TO: FROM: COPIES

! ! FINAL REPORT TO THE LEGISLATURE MINNESOTA TACONITE WORKERS HEALTH STUDY DATE: November 24, 2014 TO: Sen. David Tomassoni, chair Senate Jobs and Economic Growth Committee 317 Capitol Sen. Tony Lourey, chair Senate Health and Human Services Finance Division 120 Capitol Sen. Kathy Sheran, chair Senate Health, Human Services and Housing Committee 120 Capitol Rep. Tim Mahoney, chair House Jobs and Economic Development Finance & Policy Committee 591 State Office Building Rep. Sheldon Johnson, chair House Labor, Workplace and Regulated Industries 549 State Office Building Rep. Tom Huntley, chair Health and Human Services Finance Committee 585 State Office Building Rep. Tina Liebling, chair House Health and Human Services Policy Committee 367 State Office Building FROM: John R. Finnegan, Jr., dean and professor (E-mail: [email protected]; Phone: 612 625 1179) Jeffrey Mandel, associate professor, principal investigator (E-mail: [email protected]; Phone: 612 626 9308) COPIES: Iron Range Legislative Delegation Rep. David Dill Rep. Mary Murphy Sen. Tom Bakk Rep. John Persell Rep. Tom Anzelc Sen. Tom Saxhaug Rep. Carly Melin Rep. Jason Metsa 1! ! ! November 24, 2014 Dear Legislators: We are pleased to present the final report on our research regarding the health status of taconite workers. This report covers the assessments made by the University of Minnesota School of Public Health (SPH). The Natural Resources Research Institute will be submitting a separate report on the environmental characterization work that they have been doing. This report contains the SPH’s efforts in occupational exposure, mortality and cancer incidence, case-control studies and the respiratory health survey of taconite workers and spouses. -

ITP Mining: Energy and Environmental Profile of the U.S. Mining Industry: Chapter 4: Iron

Energy and Environmental Profile of the U.S. Mining Industry 4 Iron The chemical element iron is the fourth most common element in the Earth's crust and the second most abundant metal. About five percent of the Earth's crust is composed of iron. The metal is chemically active and is found in nature combined with other elements in rocks and soils. In its natural state, iron is chemically bonded with oxygen, water, carbon dioxide, or sulfur in a variety of minerals. Forms of Iron Minerals, Ores, and Rocks Iron occurs mainly in iron-oxide ores. Some ores are a mixture of minerals rich in iron. Other iron ores are less rich and have a large number of impurities. The most important iron ore- forming minerals are: • Magnetite - Magnetite (Fe3O4) forms magnetic black iron ore. There are large deposits of magnetite in Russia and Sweden. • Hematite - Hematite (Fe2O3) is a red iron ore. Hematite occurs in almost all forms, from solid rock to loose earth. It is the most plentiful iron ore and occurs in large quantities throughout the world. • Goethite - Goethite (Fe2O3.H2O), a brown ore, contains iron. • Limonite - Limonite (Fe2O3.H2O) is a yellow-brown iron ore. Limonite is a collective term for impure goethite and a mixture of hydrated iron oxides. Iron 4-1 Energy and Environmental Profile of the U.S. Mining Industry Taconite contains low-grade iron in fine specks and bands. It is an extremely hard and flinty - containing about 25 - 30 percent iron. The iron in taconite occurs principally as magnetite and hematite and finely dispersed with silica in sedimentary deposits. -

Mining on the Mesabi Iron Range?

What’s Happening in Mining on the Mesabi Iron Range? Dan Jordan Mining & Minerals Program Supervisor Iron Range Resources Projects that must go through Environmental Review lvpmn.org 23 Project locations 13 Developers $6 billion dollars = Approximate total value of all projects Large Scale Developments 2005 - 2011 The Iron Range has a history of large scale projects that can transform the landscape. But, not since the 1960’s and early 1970’s has the region seen so many large scale projects under consideration all at the same time • Excelsior Energy Project $2,000,000,000 • Minnesota Steel Industries project in Nashwauk $1,650,000,000 • Machine #7 at the UPM paper mill in Grand Rapids $650,000,000 • Franconia Minerals – Birch Lake & Maturi Extension $616,000,000 • PolyMet’s NorthMet Project $380,000,000 • Keetac Plant Expansion $300,000,000 • Mesabi Nugget Production Scale Plant in Hoyt Lakes $235,000,000 • Taconite Plant Capacity Expansion $275,000,000 & Alternate Energy Improvements • MP Allete Clay Boswell Unit 3 Retrofit $200,000,000 • Laurentian Energy Project for Hibbing and Virginia $80,000,000 Total $6,386,000,000 Currently 6 Taconite Mines are in operation in Minnesota 2004 Foreign ownership: Stelco 14.7% of HibTac Today: Global ownership & competition United States Steel 2007 Name Production Employees Ownership Million Tons Minntac 12.751 1210 US Steel Corp. Keewatin Taconite 5.220 385 US Steel Corp. Managed by Cleveland Cliffs Mining Co. 2007 Name Production Emp. Ownership Million Tons ArcelorMittal 62.3% Hibbing 7.266 689 U S Steel Corp. 14.7% Taconite Cleveland-Cliffs 25% Northshore 4.975 511 Cleveland-Cliffs 100% Mining United Cleveland-Cliffs 70% 5.279 431 Taconite Laiwu Steel Group 30% 2007 Name Production Emp Ownership Million Tons ArcelorMittal 2.708 533 ArcelorMittal 100% Minorca Mine Inc. -

PREFACE the Front Cover Is an Illustration Depicting Part of the Milling Operation at the Tilden Mine in Marquette County and Was Drawn by Darrell D

PREFACE The front cover is an illustration depicting part of the milling operation at the Tilden Mine in Marquette County and was drawn by Darrell D. Hodge, Jr. of the Division of Geology staff. This open pit iron ore mine is owned by the Tilden Mining Company and is operated by the Cleveland-Cliffs Iron Company. The Tilden started production in 1974 and is one of Michigan's large producers of iron ore pellets. Michigan is an important producer of many different types of minerals and mineral products. Some of these commodities are in great demand and are shipped all over the United States and abroad, while others are mined and processed for local use. State of Michigan Department of Natural Resources In 1974, Michigan led the entire U.S. in the production of Geology Division peat, iodine, calcium-magnesium chloride, magnesium compounds, marl and industrial sand. Second place for Preprint from the 1974 U.S. production was maintained for iron ore, bromine BUREAU OF MINES MINERALS YEARBOOK and gypsum. The total amount of sand and gravel produced placed Michigan in third place nationally. The Mineral Industry of Michigan The Mineral Industry of Michigan, 1974, was written and published by the U.S. Bureau of Mines as a chapter of their 1974 Minerals Yearbook, and by agreement is .additionally offered as a publication of the Division of Geology of the Michigan Department of Natural Resources as Annual Statistical Summary 23. A companion publication by the Division of Geology is the Annual Directory. The current edition is Michigan Bureau of Mines Mineral Producers, 1976. -

Iron Mining and Frac Sand, a Bibliography

Iron Mining and Frac Sand Compiled by Patricia Reichert, January 2012 Back to Tap the Power Page Renewed interest in taconite, a lower grade iron ore, in the Gogebic Range would create Wisconsin's first open pit mine; previous iron mines were underground. New horizontal drilling technology for hydrofracturing (hydraulic fracturing) to extract previously unreachable petroleum and natural gas deposits has increased demand for "frac sand," a silica sand uniform in size and hardness found in abundance in the driftless area. This Tap the Power focuses on these two types of mining, the last major revision to Wisconsin mining regulations in the 1970s, and some documentation from Minnesota, which has a long history with iron mining. Annual Report to the Legislature: Minnesota Taconite Workers Health Study / University of Minnesota School of Public Health. 2009-2011. www.leg.state.mn.us/edocs/edocs.asp?oclc number=317403197 [via the Minnesota Legislative Reference Library] Biennial Report / Wisconsin Mining Investment and Local Impact Fund Board. 2001/2003. (Rev/Min/r) The board administers the fund created to help municipalities alleviate costs associated with social, educational, environmental, and economic impacts of metalliferous mineral mining. Previous reports also available in the library. www.dor.state.wi.us/ra/bie01- 03.html The Economic Impact of Ferrous and Non-Ferrous Mining on the State of Minnesota and on the Arrowhead Region and Douglas County, WI / University of Minnesota-Duluth Labovitz School of Business and Economics. March 2009. https://lsbe.d.umn.edu/departments/bber/projects/2009MNMiningImpact.pdf Iron Mining in the Lake Superior Basin / Great Lakes Indian Fish & Wildlife Commission, Environmental Section. -

A Journal of the Lake Superior Region

Upper Country: A Journal of the Lake Superior Region Vol. 3 2015 Upper Country: A Journal of the Lake Superior Region Vol. 3 2015 Upper Country: A Journal of the Lake Superior Region EDITOR: Gabe Logan, Ph.D. PRODUCTION AND DESIGN: Kimberly Mason and James Shefchik ARTICLE REVIEW BOARD: Gabe Logan, Ph. D. Robert Archibald, Ph. D. Russell Magnaghi, Ph. D. Kathryn Johnson, M.A. PHOTOGRAPHY CREDITS Front cover photograph by Gabe Logan AVAILABILITY Upper Country: A Journal of the Lake Superior Region, can be viewed on Northern Michigan University's Center for Upper Peninsula Studies web site: www.nmu.edu/upstudies. Send comments to [email protected] for screening and posting; or mail written comments and submit manuscripts to Upper Country, c/o The Center for Upper Peninsula Studies, 1401 Presque Isle Avenue, Room 208 Cohodas, Marquette, MI 49855. COPYRIGHT Copyright © Northern Michigan University. All rights reserved. Photocopying of excerpts for review purposes granted by the copyright holder. Responsibility for the contents herein is that of the authors. AUTHOR GUIDELINES Please address submissions in print form to Upper Country, c/o The Center for Upper Peninsula Studies, Northern Michigan University, 1401 Presque Isle Avenue, Room 208 Cohodas, Marquette, MI, USA 49855. Original papers welcomed. Short photo-essays considered; image format information available upon request. Images with misleading manipulation will not be considered for acceptance. Concurrent submissions accepted. All papers reviewed by the Article Review Board. Copyright is assigned to the Journal's copyright holder upon acceptance. Format should follow the MLA/APA/Chicago Manual guidelines. Length, 6000 words maximum. -

Hibbing Taconite Company

HIBBING TACONITE COMPANY About Hibbing Taconite Company: 2020 Data Hibbing Taconite Company produces about 7.8 million tons of standard iron-bearing pellets and mines about 29 million tons of ore annually. Hibbing is a joint venture between Cleveland-Cliffs and U.S. Steel. The pellets are shipped to Cleveland-Cliffs’ facility in Burns Harbor, Indiana. Facility Facts Plant Leadership Chad Asgaard Union Leadership Chris Johnson Employees 730 Production 5.5 million long tons of iron ore pellets in 2020 Products Iron ore pellets Principal Production Open pit truck and shovel mine, concentrator utilizing single stage crushing, Facilities AG mill and magnetic separation to produce magnetite concentrate and on-site pellet plant. About Cleveland-Cliffs Cleveland-Cliffs is the largest flat-rolled steel producer in North America. Founded in 1847 as a mine operator, Cleveland-Cliffs also is the largest manufacturer of iron ore pellets in North America. The Company is vertically integrated from mined raw materials and direct reduced iron to primary steelmaking and downstream finishing, stamping, tooling and tubing. The Company serves a diverse range of markets due to its comprehensive offering of flat-rolled steel products and is the largest steel supplier to the automotive industry in North America. Headquartered in Cleveland, Ohio, Cleveland-Cliffs employs approximately 25,000 people across its mining, steel and downstream manufacturing operations in the United States and Canada. For more information, visit www.clevelandcliffs.com. Hibbing Taconite Company 4950 County Highway 5 North Hibbing, MN 55746 Telephone: 218.262.5950 www.clevelandcliffs.com © Cleveland-Cliffs Inc. Last updated 7.2021. -

Iron Mining in the Lake Superior Basin

Iron Mining In the Lake Superior Basin Minntac Iron Mine in Minnesota Project Report 11-1 October 2011 Great Lakes Indian Fish & Wildlife Commission Environmental Section P.O. Box 9 Odanah, WI 54861 (715) 682-6619 1 Introduction A new taconite mine in the Penokee Range of Wisconsin is being discussed and may eventually be proposed. The Board of Commissioners of the Great Lakes Indian Fish and Wildlife Commission has indicated an interest in developing scoping level information about how taconite mining is conducted in Michigan and Minnesota, where active taconite mines are located. This document's intent is twofold: first, to inform readers about the process and some of the impacts associated with taconite mining; second, to provide initial analysis based on the very limited information that has been provided by the Penokee project proponent. Topics include: removal of ore, ore processing, generation and storage of tailings, removal and storage of non-target waste rock, development of mine-related infrastructure, and reclamation. Understanding more about the taconite mining process, its consequences in neighboring states and potential considerations in Wisconsin can support a more informed discussion about a mine in the Penokee Range. What is taconite iron ore and where is it found? Taconite is a low-grade magnetic iron ore. When high- grade iron ore was plentiful, taconite was considered a waste rock and was not used. But as the supply of high-grade iron ore decreased, the mining industry began to view taconite as a resource. Eventually a process was developed to create __Taconite mine in Minnesota. Forest on far ridge. -

DISCOVERY of ORE on the MENOMINEE IRON RANGE by William J

MENOMINEE RANGE MEMORIES 11: DISCOVERY OF ORE ON THE MENOMINEE IRON RANGE By William J. Cummings, Menominee Range Historical Foundation Historian The Menominee Iron Range spanned about sixty miles, extending from Waucedah, in eastern Dickinson County, through portions of Florence County, Wisconsin, to Iron River, in western Iron County, Michigan. J.F. Hanst’s map appeared in Volume XXI of the Lake Superior Mining Institute Proceedings (1916-1917) and located mines then in operation. The Chicago & Northwestern Railroad branch line traveling northwest from Powers in Menominee County connected the mines with Escanaba, a Lake Michigan iron port in Delta County. Moving from east to west, mining settlements included the following: Dickinson County – Waucedah, Loretto, Vulcan, Norway, Quinnesec, Iron Mountain and the Felch Mountain District; Florence County – Commonwealth and Florence; Iron County – Crystal Falls, Amasa, Iron River and Stambaugh. Most of America’s iron ore had come became the nation’s major iron producing from New York and Pennsylvania during region by the late 1800’s. Since the Upper the first part of the nineteenth century, with Peninsula was so remote and smaller amounts mined in Virginia, underdeveloped, a dozen years elapsed Tennessee and Alabama. However, with before the new iron region, known as the the discovery of iron ore along the south Marquette Iron Range, began sending ore shore of Lake Superior near Negaunee in in quantity to steel mills in the East. 1844, Michigan’s Upper Peninsula, along As the Marquette Iron Range with portions of Wisconsin and Minnesota, developed, the government and private 1 MENOMINEE RANGE MEMORIES 11: DISCOVERY OF ORE ON THE MENOMINEE IRON RANGE By William J.