2013 Minnesota Mining Tax Guide

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Northshore Mining Fact Sheet

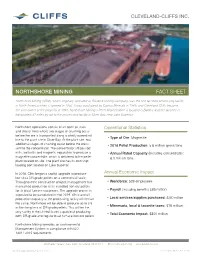

CLEVELAND-CLIFFS INC. NORTHSHORE MINING FACT SHEET Northshore Mining (NSM), which originally operated as Reserve Mining Company, was the first taconite processing facility in North America when it opened in 1956. It was purchased by Cyprus Minerals in 1989, and Cleveland-Cliffs became the sole owner of the property in 1994. Northshore Mining’s Peter Mitchell Mine is located in Babbitt and the taconite is transported 47 miles by rail to the processing facility in Silver Bay, near Lake Superior. Northshore operations consist of an open pit truck Operational Statistics and shovel mine where two stages of crushing occur before the ore is transported along a wholly owned rail • Type of Ore: Magnetite line to the plant site in Silver Bay. At the plant site, two additional stages of crushing occur before the ore is • 2018 Pellet Production: 5.6 million gross tons sent to the concentrator. The concentrator utilizes rod mills, ball mills and magnetic separation to produce a • Annual Rated Capacity (includes concentrate): magnetite concentrate, which is delivered to the pellet 6.0 million tons plant located on-site. The plant site has its own ship loading port located on Lake Superior. In 2018, Cliffs began a capital upgrade to produce Annual Economic Impact low silica DR-grade pellets on a commercial scale. Throughout the construction project, management has • Workforce: 529 employees maintained production of its standard iron ore pellets for its blast furnace customers. The upgrade project is • Payroll (including benefits) $85 million expected to be completed in mid-2019. While overall production capacity at the processing facility will remain • Local services/supplies purchased: $200 million the same, Northshore will be able to produce up to 3.5 • Minnesota, local & taconite taxes: $16 million million long tons of DR-grade pellets. -

! 1! ! ! FINAL REPORT to the LEGISLATURE MINNESOTA TACONITE WORKERS HEALTH STUDY DATE: November 24, 2014 TO: FROM: COPIES

! ! FINAL REPORT TO THE LEGISLATURE MINNESOTA TACONITE WORKERS HEALTH STUDY DATE: November 24, 2014 TO: Sen. David Tomassoni, chair Senate Jobs and Economic Growth Committee 317 Capitol Sen. Tony Lourey, chair Senate Health and Human Services Finance Division 120 Capitol Sen. Kathy Sheran, chair Senate Health, Human Services and Housing Committee 120 Capitol Rep. Tim Mahoney, chair House Jobs and Economic Development Finance & Policy Committee 591 State Office Building Rep. Sheldon Johnson, chair House Labor, Workplace and Regulated Industries 549 State Office Building Rep. Tom Huntley, chair Health and Human Services Finance Committee 585 State Office Building Rep. Tina Liebling, chair House Health and Human Services Policy Committee 367 State Office Building FROM: John R. Finnegan, Jr., dean and professor (E-mail: [email protected]; Phone: 612 625 1179) Jeffrey Mandel, associate professor, principal investigator (E-mail: [email protected]; Phone: 612 626 9308) COPIES: Iron Range Legislative Delegation Rep. David Dill Rep. Mary Murphy Sen. Tom Bakk Rep. John Persell Rep. Tom Anzelc Sen. Tom Saxhaug Rep. Carly Melin Rep. Jason Metsa 1! ! ! November 24, 2014 Dear Legislators: We are pleased to present the final report on our research regarding the health status of taconite workers. This report covers the assessments made by the University of Minnesota School of Public Health (SPH). The Natural Resources Research Institute will be submitting a separate report on the environmental characterization work that they have been doing. This report contains the SPH’s efforts in occupational exposure, mortality and cancer incidence, case-control studies and the respiratory health survey of taconite workers and spouses. -

ITP Mining: Energy and Environmental Profile of the U.S. Mining Industry: Chapter 4: Iron

Energy and Environmental Profile of the U.S. Mining Industry 4 Iron The chemical element iron is the fourth most common element in the Earth's crust and the second most abundant metal. About five percent of the Earth's crust is composed of iron. The metal is chemically active and is found in nature combined with other elements in rocks and soils. In its natural state, iron is chemically bonded with oxygen, water, carbon dioxide, or sulfur in a variety of minerals. Forms of Iron Minerals, Ores, and Rocks Iron occurs mainly in iron-oxide ores. Some ores are a mixture of minerals rich in iron. Other iron ores are less rich and have a large number of impurities. The most important iron ore- forming minerals are: • Magnetite - Magnetite (Fe3O4) forms magnetic black iron ore. There are large deposits of magnetite in Russia and Sweden. • Hematite - Hematite (Fe2O3) is a red iron ore. Hematite occurs in almost all forms, from solid rock to loose earth. It is the most plentiful iron ore and occurs in large quantities throughout the world. • Goethite - Goethite (Fe2O3.H2O), a brown ore, contains iron. • Limonite - Limonite (Fe2O3.H2O) is a yellow-brown iron ore. Limonite is a collective term for impure goethite and a mixture of hydrated iron oxides. Iron 4-1 Energy and Environmental Profile of the U.S. Mining Industry Taconite contains low-grade iron in fine specks and bands. It is an extremely hard and flinty - containing about 25 - 30 percent iron. The iron in taconite occurs principally as magnetite and hematite and finely dispersed with silica in sedimentary deposits. -

Mining on the Mesabi Iron Range?

What’s Happening in Mining on the Mesabi Iron Range? Dan Jordan Mining & Minerals Program Supervisor Iron Range Resources Projects that must go through Environmental Review lvpmn.org 23 Project locations 13 Developers $6 billion dollars = Approximate total value of all projects Large Scale Developments 2005 - 2011 The Iron Range has a history of large scale projects that can transform the landscape. But, not since the 1960’s and early 1970’s has the region seen so many large scale projects under consideration all at the same time • Excelsior Energy Project $2,000,000,000 • Minnesota Steel Industries project in Nashwauk $1,650,000,000 • Machine #7 at the UPM paper mill in Grand Rapids $650,000,000 • Franconia Minerals – Birch Lake & Maturi Extension $616,000,000 • PolyMet’s NorthMet Project $380,000,000 • Keetac Plant Expansion $300,000,000 • Mesabi Nugget Production Scale Plant in Hoyt Lakes $235,000,000 • Taconite Plant Capacity Expansion $275,000,000 & Alternate Energy Improvements • MP Allete Clay Boswell Unit 3 Retrofit $200,000,000 • Laurentian Energy Project for Hibbing and Virginia $80,000,000 Total $6,386,000,000 Currently 6 Taconite Mines are in operation in Minnesota 2004 Foreign ownership: Stelco 14.7% of HibTac Today: Global ownership & competition United States Steel 2007 Name Production Employees Ownership Million Tons Minntac 12.751 1210 US Steel Corp. Keewatin Taconite 5.220 385 US Steel Corp. Managed by Cleveland Cliffs Mining Co. 2007 Name Production Emp. Ownership Million Tons ArcelorMittal 62.3% Hibbing 7.266 689 U S Steel Corp. 14.7% Taconite Cleveland-Cliffs 25% Northshore 4.975 511 Cleveland-Cliffs 100% Mining United Cleveland-Cliffs 70% 5.279 431 Taconite Laiwu Steel Group 30% 2007 Name Production Emp Ownership Million Tons ArcelorMittal 2.708 533 ArcelorMittal 100% Minorca Mine Inc. -

Taconite Iron Ore NESHAP Economic Impact Analysis EPA-452/R-03-015 August 2003

Taconite Iron Ore NESHAP Economic Impact Analysis EPA-452/R-03-015 August 2003 Taconite Iron Ore NESHAP Economic Impact Analysis By: Katherine Heller Brooks M. Depro Jui-Chen Yang Laurel Clayton RTI International* Health, Social, and Economics Research Research Triangle Park, North Carolina 27709 Prepared for: John L. Sorrels U.S. Environmental Protection Agency Office of Air Quality Planning and Standards Innovative Strategies and Economics Group (ISEG) (C339-01) Research Triangle Park, NC 27711 Contract No. 68-D-99-024 *RTI International is a trade name of Research Triangle Institute. CONTENTS Section Page Executive Summary...................................................ES-1 1 Introduction .................................................... 1-1 2 Industry Profile .................................................. 2-1 2.1 The Supply Side ........................................... 2-3 2.1.1 Taconite Pellet Production Processes, Inputs and Outputs .... 2-3 2.1.1.1 Mining of Crude Ore .......................... 2-3 2.1.1.2 Beneficiation ................................. 2-5 2.1.1.3 Agglomeration ............................... 2-8 2.1.2 Types of Products .................................... 2-8 2.1.3 Major By-Products, Co-Products, and Input Substitution Possibilities ....................................... 2-10 2.1.4 Costs of Production and Worker Productivity ............. 2-11 2.1.4.1 Costs of Production .......................... 2-11 2.1.4.2 Variations in Worker Productivity by Establishment Size ........................... 2-12 2.2 The Demand Side......................................... 2-13 2.2.1 Uses and Consumers ................................ 2-13 2.2.1.1 Uses ...................................... 2-13 2.2.1.2 Consumer Characteristics ...................... 2-15 2.2.2 Product Characteristics .............................. 2-15 2.2.3 Substitution Possibilities in Consumption ................ 2-15 2.3 Industry Organization ...................................... 2-17 2.3.1 Taconite Manufacturing Facility Characteristics .......... -

Iron Mining and Frac Sand, a Bibliography

Iron Mining and Frac Sand Compiled by Patricia Reichert, January 2012 Back to Tap the Power Page Renewed interest in taconite, a lower grade iron ore, in the Gogebic Range would create Wisconsin's first open pit mine; previous iron mines were underground. New horizontal drilling technology for hydrofracturing (hydraulic fracturing) to extract previously unreachable petroleum and natural gas deposits has increased demand for "frac sand," a silica sand uniform in size and hardness found in abundance in the driftless area. This Tap the Power focuses on these two types of mining, the last major revision to Wisconsin mining regulations in the 1970s, and some documentation from Minnesota, which has a long history with iron mining. Annual Report to the Legislature: Minnesota Taconite Workers Health Study / University of Minnesota School of Public Health. 2009-2011. www.leg.state.mn.us/edocs/edocs.asp?oclc number=317403197 [via the Minnesota Legislative Reference Library] Biennial Report / Wisconsin Mining Investment and Local Impact Fund Board. 2001/2003. (Rev/Min/r) The board administers the fund created to help municipalities alleviate costs associated with social, educational, environmental, and economic impacts of metalliferous mineral mining. Previous reports also available in the library. www.dor.state.wi.us/ra/bie01- 03.html The Economic Impact of Ferrous and Non-Ferrous Mining on the State of Minnesota and on the Arrowhead Region and Douglas County, WI / University of Minnesota-Duluth Labovitz School of Business and Economics. March 2009. https://lsbe.d.umn.edu/departments/bber/projects/2009MNMiningImpact.pdf Iron Mining in the Lake Superior Basin / Great Lakes Indian Fish & Wildlife Commission, Environmental Section. -

Hibbing Taconite Company

HIBBING TACONITE COMPANY About Hibbing Taconite Company: 2020 Data Hibbing Taconite Company produces about 7.8 million tons of standard iron-bearing pellets and mines about 29 million tons of ore annually. Hibbing is a joint venture between Cleveland-Cliffs and U.S. Steel. The pellets are shipped to Cleveland-Cliffs’ facility in Burns Harbor, Indiana. Facility Facts Plant Leadership Chad Asgaard Union Leadership Chris Johnson Employees 730 Production 5.5 million long tons of iron ore pellets in 2020 Products Iron ore pellets Principal Production Open pit truck and shovel mine, concentrator utilizing single stage crushing, Facilities AG mill and magnetic separation to produce magnetite concentrate and on-site pellet plant. About Cleveland-Cliffs Cleveland-Cliffs is the largest flat-rolled steel producer in North America. Founded in 1847 as a mine operator, Cleveland-Cliffs also is the largest manufacturer of iron ore pellets in North America. The Company is vertically integrated from mined raw materials and direct reduced iron to primary steelmaking and downstream finishing, stamping, tooling and tubing. The Company serves a diverse range of markets due to its comprehensive offering of flat-rolled steel products and is the largest steel supplier to the automotive industry in North America. Headquartered in Cleveland, Ohio, Cleveland-Cliffs employs approximately 25,000 people across its mining, steel and downstream manufacturing operations in the United States and Canada. For more information, visit www.clevelandcliffs.com. Hibbing Taconite Company 4950 County Highway 5 North Hibbing, MN 55746 Telephone: 218.262.5950 www.clevelandcliffs.com © Cleveland-Cliffs Inc. Last updated 7.2021. -

Iron Mining in the Lake Superior Basin

Iron Mining In the Lake Superior Basin Minntac Iron Mine in Minnesota Project Report 11-1 October 2011 Great Lakes Indian Fish & Wildlife Commission Environmental Section P.O. Box 9 Odanah, WI 54861 (715) 682-6619 1 Introduction A new taconite mine in the Penokee Range of Wisconsin is being discussed and may eventually be proposed. The Board of Commissioners of the Great Lakes Indian Fish and Wildlife Commission has indicated an interest in developing scoping level information about how taconite mining is conducted in Michigan and Minnesota, where active taconite mines are located. This document's intent is twofold: first, to inform readers about the process and some of the impacts associated with taconite mining; second, to provide initial analysis based on the very limited information that has been provided by the Penokee project proponent. Topics include: removal of ore, ore processing, generation and storage of tailings, removal and storage of non-target waste rock, development of mine-related infrastructure, and reclamation. Understanding more about the taconite mining process, its consequences in neighboring states and potential considerations in Wisconsin can support a more informed discussion about a mine in the Penokee Range. What is taconite iron ore and where is it found? Taconite is a low-grade magnetic iron ore. When high- grade iron ore was plentiful, taconite was considered a waste rock and was not used. But as the supply of high-grade iron ore decreased, the mining industry began to view taconite as a resource. Eventually a process was developed to create __Taconite mine in Minnesota. Forest on far ridge. -

The Lake Superior Iron Ranges: Geology and Mining

THE LAKE SUPERIOR IRON RANGES: GEOLOGY AND MINING William F. Cannon, U.S. Geological Survey, Reston, VA 20192 ECONOMIC AND STRATEGIC SIGNIFICANCE OF LAKE SUPERIOR IRON Currently the only source of domestic iron ore. In recent years, Lake Superior ores provided roughly 85% of U.S. demand. Annual production varies but is generally about 50 million tons of concentrate valued at about $2 billion. An iron range is an elongate belt of layered sedimentary rocks in which one or more layers consist of banded iron-formation, a rock composed of alternating iron-rich and iron-poor layers on a scale of a few centimeters. Banded iron-formation from the Gogebic Range MINING HISTORY First ore discoveries and mines: Marquette Range, Michigan: Ore discovered 1844, first ore shipment 1852 Menominee Range, Michigan: Discovered 1846, first mine 1870 Gogebic Range, Michigan and Wisconsin: discovered 1848, first mine 1884 Iron River, Michigan: discovered 1851, first mine 1881 Vermillion Range, Minnesota: discovered 1882, first mine 1884 Mesabi Range, Minnesota: discovered 1866, first mine 1890 Cuyuna Range, Minnesota: discovered 1904, first mine 1910 A BRIEF HISTORY OF MINING PHASE 1. The initial phase of mining, from discovery until the 1950’s, was for direct shipping ore (also called natural ore). These ores were pockets of high grade iron concentrations that formed within banded iron formations by leaching of silica by surface water or deeply circulating ground water. PHASE 2. Beginning in the late 1950’s a transition from direct shipping ore to taconite production began. Within a decade it supplanted direct shipping ore. Taconite is produced from metallurgically favorable parts of banded iron-formation and requires concentration and pelletizing at the mine site. -

A Brief History of Mining in Michigan's Marquette and Menominee Iron

A Brief History of Mining in Michigan’s Marquette and Menominee Iron Ranges The Upper Peninsula of Michigan, the “U.P.” as the locals call it, has been blessed with a wealth of mineral resources. The Native Americans were the earliest miners, using float copper left behind by the receding glaciers to make implements of many types. Copper trade goods eventually made their way throughout the Mississippi River watershed. Douglas Houghton visited copper deposits on his 1831-32 expedition. He became Michigan’s first State Geologist in 1839. His reports on the copper deposits in 1841, made the public aware of the resource potential of the U.P. Although he did not personally visit the iron deposits, he reported their existence. William Austin Burt, a government surveyor, is credited with the discovery of iron ore near Negaunee in 1844. This would become known as the Marquette Iron Range. In 1845, the Jackson Iron Company, with help from the Native Americans, discovered an iron deposit in another location that was to become the town of Negaunee. This deposit became the Jackson Mine. Ore was mined from an open pit. The Carp River Forge was opened in 1847 near Negaunee. It utilized ore from the Jackson Mine. The Michigan Iron Industry Museum, near the site of the forge, will be visited during the 2019 Mining History Association conference. Other Michigan iron ore discoveries followed as prospectors gained a better understanding of the geology and pushed into unexplored territory. Marquette Range, 1844 Eastern Menominee Range, 1845 Gogebic Range, 1848 Western Menominee Range, 1851 Gwinn District, Marquette Range, 1869 By comparison, the earliest iron ore discoveries in Minnesota occurred over 30 years later than the first discovery in Michigan. -

1 Final Report to the Legislature Minnesota

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp FINAL REPORT TO THE LEGISLATURE MINNESOTA TACONITE WORKERS HEALTH STUDY DATE: November 24, 2014 TO: Sen. David Tomassoni, chair Senate Jobs and Economic Growth Committee 317 Capitol Sen. Tony Lourey, chair Senate Health and Human Services Finance Division 120 Capitol Sen. Kathy Sheran, chair Senate Health, Human Services and Housing Committee 120 Capitol Rep. Tim Mahoney, chair House Jobs and Economic Development Finance & Policy Committee 591 State Office Building Rep. Sheldon Johnson, chair House Labor, Workplace and Regulated Industries 549 State Office Building Rep. Tom Huntley, chair Health and Human Services Finance Committee 585 State Office Building Rep. Tina Liebling, chair House Health and Human Services Policy Committee 367 State Office Building FROM: John R. Finnegan, Jr., dean and professor (E-mail: [email protected]; Phone: 612 625 1179) Jeffrey Mandel, associate professor, principal investigator (E-mail: [email protected]; Phone: 612 626 9308) COPIES: Iron Range Legislative Delegation Rep. David Dill Rep. Mary Murphy Sen. Tom Bakk Rep. John Persell Rep. Tom Anzelc Sen. Tom Saxhaug Rep. Carly Melin Rep. Jason Metsa 1 November 24, 2014 Dear Legislators: We are pleased to present the final report on our research regarding the health status of taconite workers. This report covers the assessments made by the University of Minnesota School of Public Health (SPH). The Natural Resources Research Institute will be submitting a separate report on the environmental characterization work that they have been doing. -

Iron Mining in the Lake Superior Basin

Iron Mining In the Lake Superior Basin Minntac Iron Mine in Minnesota Project Report 11-1 October 2011 Great Lakes Indian Fish & Wildlife Commission Environmental Section P.O. Box 9 Odanah, WI 54861 (715) 682-6619 1 Introduction A new taconite mine in the Penokee Range of Wisconsin is being discussed and may eventually be proposed. The Board of Commissioners of the Great Lakes Indian Fish and Wildlife Commission has indicated an interest in developing scoping level information about how taconite mining is conducted in Michigan and Minnesota, where active taconite mines are located. This document's intent is twofold: first, to inform readers about the process and some of the impacts associated with taconite mining; second, to provide initial analysis based on the very limited information that has been provided by the Penokee project proponent. Topics include: removal of ore, ore processing, generation and storage of tailings, removal and storage of non-target waste rock, development of mine-related infrastructure, and reclamation. Understanding more about the taconite mining process, its consequences in neighboring states and potential considerations in Wisconsin can support a more informed discussion about a mine in the Penokee Range. What is taconite iron ore and where is it found? Taconite is a low-grade magnetic iron ore. When high- grade iron ore was plentiful, taconite was considered a waste rock and was not used. But as the supply of high-grade iron ore decreased, the mining industry began to view taconite as a resource. Eventually a process was developed to create __Taconite mine in Minnesota. Forest on far ridge.