The Russian Federation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

"Waves" of the Russia's Presidential Reforms Break About Premier's "Energy-Rocks"

AFRICA REVIEW EURASIA REVIEW "Waves" of the Russia's Presidential Reforms Break About Premier's "Energy-Rocks" By Dr. Zurab Garakanidze* Story about the Russian President Dmitry Medvedev’s initiative to change the make-up of the boards of state-owned firms, especially energy companies. In late March of this year, Russian President Dmitry Medvedev demanded that high-ranking officials – namely, deputy prime ministers and cabinet-level ministers that co-ordinate state policy in the same sectors in which those companies are active – step down from their seats on the boards of state-run energy companies by July 1. He also said that October 1 would be the deadline for replacing these civil servants with independent directors. The deadline has now passed, but Medvedev‟s bid to diminish the government‟s influence in the energy sector has run into roadblocks. Most of the high-level government officials who have stepped down are being replaced not by independent managers, but by directors from other state companies in the same sector. Russia‟s state-owned oil and gas companies have not been quick to replace directors who also hold high-ranking government posts, despite or- ders from President Dmitry Medvedev. High-ranking Russian officials have made a show of following President Medvedev‟s order to leave the boards of state-run energy companies, but government influence over the sector remains strong. This indicates that the political will needed for the presidential administration to push eco- nomic reforms forward may be inadequate. 41 www.cesran.org/politicalreflection Political Reflection | September-October-November 2011 Russia's Presidential Reforms | By Dr. -

Crimea: Anatomy of a Decision

Crimea: Anatomy of a decision Daniel Treisman President Vladimir Putin’s decision to seize the Crimean peninsula from Ukraine and incorporate it into Russia was the most consequential of his first 15 years in power.1 It had profound implications for both foreign and domestic policy as well as for how Russia was viewed around the world. The intervention also took most observers—both in Russia and in the West—by surprise. For these reasons, it is a promising case from which to seek insight into the concerns and processes that drive Kremlin decision-making on high-stakes issues. One can distinguish two key questions: why Putin chose to do what he did, and how the decision was made. In fact, as will become clear, the answer to the second question helps one choose among different possible answers to the first. Why did Putin order his military intelligence commandos to take control of the peninsula? In the immediate aftermath, four explanations dominated discussion in the Western media and academic circles. A first image—call this “Putin the defender”—saw the Russian intervention as a desperate response to the perceived threat of NATO enlargement. Fearing that with President Viktor Yanukovych gone Ukraine’s new government would quickly join the Western military alliance, so the argument goes, Putin struck preemptively to prevent such a major strategic loss and to break the momentum of NATO’s eastward drive (see, e.g., Mearsheimer 2014). 1 This chapter draws heavily on “Why Putin Took Crimea,” Foreign Affairs, May/June, 2016. A second image—“Putin the imperialist”—cast Crimea as the climax of a gradually unfolding, systematic project on the part of the Kremlin to recapture the lost lands of the Soviet Union. -

Russia's Foreign Policy Change and Continuity in National Identity

Russia’s Foreign Policy Russia’s Foreign Policy Change and Continuity in National Identity Second Edition Andrei P. Tsygankov ROWMAN & LITTLEFIELD PUBLISHERS, INC. Lanham • Boulder • New York • Toronto • Plymouth, UK Published by Rowman & Littlefield Publishers, Inc. A wholly owned subsidiary of The Rowman & Littlefield Publishing Group, Inc. 4501 Forbes Boulevard, Suite 200, Lanham, Maryland 20706 http://www.rowmanlittlefield.com Estover Road, Plymouth PL6 7PY, United Kingdom Copyright © 2010 by Rowman & Littlefield Publishers, Inc. All rights reserved. No part of this book may be reproduced in any form or by any electronic or mechanical means, including information storage and retrieval systems, without written permission from the publisher, except by a reviewer who may quote passages in a review. British Library Cataloguing in Publication Information Available Library of Congress Cataloging-in-Publication Data Tsygankov, Andrei P., 1964- Russia's foreign policy : change and continuity in national identity / Andrei P. Tsygankov. -- 2nd ed. p. cm. Includes bibliographical references and index. ISBN 978-0-7425-6752-8 (cloth : alk. paper) -- ISBN 978-0-7425-6753-5 (paper : alk. paper) -- ISBN 978-0-7425-6754-2 (electronic) 1. Russia (Federation)--Foreign relations. 2. Soviet Union--Foreign relations. 3. Great powers. 4. Russia (Federation)--Foreign relations--Western countries. 5. Western countries--Foreign relations--Russia (Federation) 6. Nationalism--Russia (Federation) 7. Social change--Russia (Federation) I. Title. DK510.764.T785 2010 327.47--dc22 2009049396 ™ The paper used in this publication meets the minimum requirements of American National Standard for Information Sciences—Permanence of Paper for Printed Library Materials, ANSI/NISO Z39.48-1992. Printed in the United States of America It is the eternal dispute between those who imagine the world to suit their policy, and those who arrange their policy to suit the realities of the world. -

Boris Nemtsov 27 February 2015 Moscow, Russia

Boris Nemtsov 27 February 2015 Moscow, Russia the fight against corruption, embezzlement and fraud, claiming that the whole system built by Putin was akin to a mafia. In 2009, he discovered that one of Putin’s allies, Mayor of Moscow City Yury Luzhkov, BORIS and his wife, Yelena Baturina, were engaged in fraudulent business practices. According to the results of his investigation, Baturina had become a billionaire with the help of her husband’s connections. Her real-estate devel- opment company, Inteco, had invested in the construction of dozens of housing complexes in Moscow. Other investors were keen to part- ner with Baturina because she was able to use NEMTSOV her networks to secure permission from the Moscow government to build apartment build- ings, which were the most problematic and It was nearing midnight on 27 February 2015, and the expensive construction projects for developers. stars atop the Kremlin towers shone with their charac- Nemtsov’s report revealed the success of teristic bright-red light. Boris Nemtsov and his partner, Baturina’s business empire to be related to the Anna Duritskaya, were walking along Bolshoy Moskovo- tax benefits she received directly from Moscow retsky Bridge. It was a cold night, and the view from the City government and from lucrative govern- bridge would have been breathtaking. ment tenders won by Inteco. A snowplough passed slowly by the couple, obscuring the scene and probably muffling the sound of the gunshots fired from a side stairway to the bridge. The 55-year-old Nemtsov, a well-known Russian politician, anti-corrup- tion activist and a fierce critic of Vladimir Putin, fell to the ground with four bullets in his back. -

Annual-Report-2018 Eng.Pdf

Russian International Affairs Council CONTENTS /01 GENERAL INFORMATION 4 /02 RIAC PROGRAM ACTIVITIES 16 /03 RIAC IN THE MEDIA 58 /04 RIAC WEBSITE 60 /05 FINANCIAL STATEMENTS 62 3 Russian International ANNUAL REPORT 2018 Affairs Council The General Meeting of RIAC members is the The main task of the RIAC Scientific Council is to ABOUT THE COUNCIL supreme governing body of the Partnership. The formulate sound recommendations for strategic key function of the General Meeting is to ensure decisions in RIAC expert, research, and publishing The non-profit partnership Russian compliance with the goals of the Partnership. The activities. General Meeting includes 160 members of the International Affairs Council (NP RIAC) is Council. The Vice-Presidency was introduced to achieve 01 the goals of the Partnership in cooperation with a Russian membership-based non-profit The RIAC Board of Trustees is a supervisory body government bodies and local authorities of the organization. The partnership was established of the Partnership that monitors the activities of Russian Federation and foreign states, the Partnership and their compliance with the international organizations, and Russian and by the resolution of its founders pursuant statutory goals. foreign legal entities. The candidate for Vice- President is approved by the RIAC Presidium for a to Decree No. 59-rp of the President of the The Presidium of the Partnership is a permanent one-year term. Russian Federation “On the Establishment collegial governing body of the Partnership that consists of not less than five and no more than RIAC Corporate Members of the Non-Profit Partnership Russian fifteen members, including the President and According to the Charter, legal citizens of the the Director General of the Partnership, who Russian Federation or entities established in International Affairs Council” dated February 2, have a vote in the decision-making process. -

Russi-Monitor-Monthl

MONTHLY May 2020 CONTENTS 3 17 28 POLAND AND DENMARK BEGIN BELARUS RAMPS UP RUSSIAN ECONOMY COMES CONSTRUCTION OF BALTIC DIVERSIFICATION EFFORTS BADLY BECAUSE OF PANDEMIC PIPE PROJECT TO CHALLENGE WITH U.S. AND GULF CRUDE RUSSIAN GAS DOMINANCE PURCHASES POLAND AND DENMARK BEGIN CONSTRUCTION OF BALTIC PIPE PROJECT CORONAVIRUS IN RUSSIA: BAD NEWS FOR 3 TO CHALLENGE RUSSIAN GAS DOMINANCE 20 THE COUNTRY MOSCOW: THE CAPITAL RUSSIA UNVEILS RESCUE PLAN FOR OIL 5 OF RUSSIAN CORONAVIRUS OUTBREAK 22 SECTOR VLADIMIR PUTIN SUFFERS PRESTIGIOUS 6 FAILURE IN VICTORY DAY CELEBRATIONS 23 TENSIONS RISE IN THE BLACK SEA RUSSIA EASES LOCKDOWN YET OFFERS ROSNEFT, TRANSNEFT IN NEW FEUD OVER 8 LITTLE SUPPORT TO CITIZENS 25 TRANSPORTATION TARIFFS ROSNEFT’S SECHIN ASKS OFFICIALS FOR NEW TAX RELIEFS DESPITE RECENT GAZPROM IS TURNING TOWARDS CHINA, 10 MISHAPS 27 BUT THERE ARE PROBLEMS FRADKOV REMAINS AT THE HELM OF THE RUSSIAN ECONOMY COMES BADLY 12 KREMLIN’S “INTELLIGENCE SERVICE” 28 BECAUSE OF PANDEMIC RUSSIA STEPS UP DIPLOMATIC EFFORTS AS RUSSIA AIMS TO BOOST MILITARY FACILITIES 14 KREMLIN AIDE KOZAK VISITS BERLIN 30 IN SYRIA GAZPROM’S NATURAL GAS EXPORT RUSSIA–NATO TENSIONS CONTINUE ON 16 REVENUE DECLINED DRAMATICALLY IN Q1 32 BOTH FLANKS BELARUS RAMPS UP DIVERSIFICATION RUSSIA, BELARUS SQUABBLE OVER GAS EFFORTS WITH U.S. AND GULF CRUDE DELIVERIES IN NEW CHAPTER OF ENERGY 17 PURCHASES 34 WAR RUSSIA’S ROSNEFT HAS NEW OWNERSHIP RUSSIA FACES BIGGEST MILITARY THREAT 19 STRUCTURE BUT SAME CEO 36 FROM WEST, SHOIGU SAYS 2 www.warsawinstitute.org 4 May 2020 POLAND AND DENMARK BEGIN CONSTRUCTION OF BALTIC PIPE PROJECT TO CHALLENGE RUSSIAN GAS DOMINANCE Construction of a major gas pipeline from Norway is to begin in the coming days, Polish President Andrzej Duda said in the morning of May 4. -

Black Sea Container Market and Georgia's Positioning

European Scientific Journal November 2018 edition Vol.14, No.31 ISSN: 1857 – 7881 (Print) e - ISSN 1857- 7431 Black Sea Container Market and Georgia’s Positioning Irakli Danelia, (PhD student) Tbilisi State University, Georgia Doi:10.19044/esj.2018.v14n31p100 URL:http://dx.doi.org/10.19044/esj.2018.v14n31p100 Abstract Due to the strategically important geographical location, Black Sea region has a key transit function throughout between Europe and Asia. Georgia, which is a part of Black sea area, has a vital transit function for Caucasus Region, as well as for whole New Silk Road area. Nevertheless, still there is no evidence what kind of role and place Georgia has in The Black Sea container market. As the country has ambition to be transit hub for containerizes cargo flows between west and east and is actively involved in the process of formation “One Belt One Road” project, it is very important to identify Country’s current circumstances, capacities and future potential. Because of this, the purpose of the study is to investigate cargo flows and opportunities of the Black Sea container market, level of competitiveness in the area and define Georgia’s positioning in the regional Container market. Keywords: Geostrategic Location, New Silk Road, Transit Corridor, Cargo flow, Container market, Georgia, Black Sea Methodology Based on practical and theoretical significance of the research the following paper provides systemic, historical and logical generalization methods of research in the performance of the work, scientific abstraction, analysis and synthesis methods are also used. Introduction Since the end of the Cold War, the Black Sea region has no longer been a static border between the West and the East. -

Caucasian Review of International Affairs (CRIA) Is a Quarterly Peer-Reviewed Free, Non-Profit and Only-Online Academic Journal Based in Germany

CCCAUCASIAN REVIEW OF IIINTERNATIONAL AAAFFAIRS Vol. 4 (((2(222)))) spring 2020201020 101010 RUSSIAN ENERGY POLITICS AND THE EU: HOW TO CHANGE THE PARADIGM VLADIMER PAPAVA & MICHAEL TOKMAZISHVILI AUTHORITARIANISM AND FOREIGN POLICY : THE TWIN PILLARS OF RESURGENT RUSSIA LUKE CHAMBERS THE GEORGIA CRISIS : A NEW COLD WAR ON THE HORIZON ? HOUMAN A. SADRI & NATHAN L. BURNS ENFORCEABILITY OF A COMMON ENERGY SUPPLY SECURITY POLICY IN THE EU EDA KUSKU “A SSEMBLING ” A CIVIC NATION IN KAZAKHSTAN : THE NATION -BUILDING ROLE OF THE ASSEMBLY OF THE PEOPLES OF KAZAKHSTAN NATHAN PAUL JONES NEW GEOPOLITICS OF THE SOUTH CAUCASUS FAREED SHAFEE CLIMBING THE MOUNTAIN OF LANGUAGES : LANGUAGE LEARNING IN GEORGIA HANS GUTBROD AND MALTE VIEFHUES , CRRC “DRAMATIC CHANGES IN THE POLITICAL ORDER ARE TYPICALLY NOT THE PROVINCE OF DEMOCRACIES ” INTERVIEW WITH DR. JULIE A. GEORGE , CITY UNIVERSITY OF NEW YORK ISSN: 1865-6773 www.cria -online.org EDITOR-IN-CHIEF: Nasimi Aghayev EDITORIAL BOARD: Dr. Tracey German (King’s College Dr. Robin van der Hout (Europa-Institute, London, United Kingdom) University of Saarland, Germany) Dr. Andrew Liaropoulos (Institute for Dr. Jason Strakes (Analyst, Research European and American Studies, Greece) Reachback Center East, USA) Dr. Martin Malek (National Defence Dr. Cory Welt (Georgetown University, Academy, Austria) USA) INTERNATIONAL ADVISORY BOARD: Prof. Hüseyin Bagci , Middle East Prof. Werner Münch , former Prime Technical University, Ankara, Turkey Minister of Saxony-Anhalt, former Member of the European Parliament, Germany Prof. Hans-Georg Heinrich, University of Vienna, Austria Prof. Elkhan Nuriyev , Director of the Centre for Strategic Studies under the Prof. Edmund Herzig , Oxford University, President of the Republic of Azerbaijan UK Dr. -

Patronage of Vladimir Putin

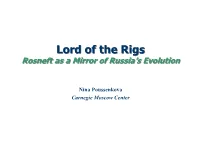

LLorord of the d of the RiRigsgs RosRosnenefftt a as s a a MMiirrrror oor off Rus Russisia’sa’s Ev Evololututiionon Nina Poussenkova Carnegie Moscow Center PortPortrraiaitt of of RosneRosneft ft E&P Refining Marketing Projects Yuganskneftegas Komsomolsk Purneftegas Altainefteproduct Sakhalin 3, 4, 5 Sakhalinmorneftegas Tuapse Kurgannefteproduct Vankor block of fields Severnaya Neft Yamalnefteproduct West Kamchatka shelf Polar Lights Nakhodkanefteproduct Black and Azov Seas Sakhalin1 Vostoknefteproduct Kazakhstan Vankorneft Arkhangelsknefteproduct Algiers Krasnodarneftegas Murmansknefteproduct CPC Stavropolneftegas Smolensknefteproduct VostochnoSugdinsk block Grozneft Artag Verkhnechonsk KabardinoBalkar Fuel Co Neftegas Karachayevo Udmurtneft Cherkessknefteproduct Kubannefteproduct Tuapsenefteproduct Stavropoliye ExYuganskneftegas: 2004 oil production (21 mt) – 4.7% of Russia’s total CEO – S.Bogdanchikov BoD Chairman – I.Sechin Proved oil reserves – 4.8% of Russia’s total With Yuganskneftegas: > 75% owned by the state Rosneftegas 2006 oil production (75 mt) – 15% of Russia’s total 9.44% YUKOS >14% sold during IPO Proved oil reserves – 20% of Russia’s total RoRosnesneftft’s’s Saga Saga 1985 1990 1992 1995 2000 2005 2015 KomiTEK Sibneft LUKOIL The next ONACO target ??? Surgut TNK Udmurtneft The USSR Slavneft Ministry of Rosneftegas the Oil Rosneft Rosneft Rosneft Rosneft Rosneft Industry 12 mt 240 mt 20 mt 460 mt 75 mt 595 mt VNK 135 mt Milestones: SIDANCO 1992 – start of privatization Severnaya Neft 1998 – appointment of S.Bogdanchikov -

Scythian Horses Shed Light on Animal Domestication

NATIONAL PRESS RELEASE I PARIS I 27 APRIL 2017 Scythian horses shed light on animal domestication By studying the genome of Scythian horses, an international team of researchers is outlining the relations that these nomads from Iron Age Central Asia had with their horses—and lifting the veil on some of the mysteries of animal domestication. Published in the journal Science on April 28, 2017, this research was led by Ludovic Orlando, CNRS senior researcher at the Laboratory of Molecular Anthropology and Image Synthesis (CNRS/Université Toulouse III – Paul Sabatier/Université Paris Descartes) and professor at the Natural History Museum of Denmark.1 Nomadic Scythian herders roamed vast areas spanning the Central Asian steppes during the Iron Age (from approximately the ninth to the first century BCE (Before Common Era)). They were known for their exceptional equestrian skills, and their leaders were buried with sacrificed stallions at grand funerary ceremonies. The genomes of a few of these equids were fully sequenced as part of this study, so as to form a better understanding of the relations that the Scythian people developed with their horses. The researchers sequenced the genomes of thirteen 2,300–2,700-year-old stallions from the Scythian royal burial tombs of Arzhan (Russian Republic of Tuva, in the outer reaches of Mongolia) and Berel’ (Kazakh Altai Mountains). They also sequenced the genome of a mare from an older culture, found in Chelyabinsk (Russia), and which is 4,100 years old. By studying the variants carried by certain specific genes, they were able to deduce a large diversity in the coat coloration patterns of Scythian horses, ranging from bay to black by way of chestnut. -

Of the Conventional Wisdom

M ASSAC H US E TTS INSTITUT E O F T E C H NO L O G Y M ASSAC H US E TTS INSTITUT E O F T E C H NO L O G Y December 2007 M IT Ce NT er F O R I NT er NATIONA L S TU D I E S 07-22 of the Conventional Wisdom Russia: An Energy Superpower? Carol R. Saivetz MIT Center for International Studies s Vladimir Putin nears the end of his second term as Russian Apresident, it is clear that energy exports have become a major component of a resurgent Russia’s foreign policy. According to the conventional wisdom, Russia’s vast resources make it a superpower to be reckoned with. Not only is it a major supplier of natural gas to the states of the former Soviet Union, it sells oil and natural gas to Europe and it has made new contract commitments for both oil and gas to China. Additionally, as the January 2006 cut-off of gas to Ukraine, the January 2007 oil and gas cut-off to Belarus, and Gazprom’s threat (again) to Ukraine in the wake of the September 2007 parliamentary elections indicate, Russia is willing to use its resources for political purposes. The conventional wisdom continues that none of this is surprising. Putin acceded to the Russian presidency resolved to restore Russia’s superpower status and to use energy Center for International Studies to that end. The Russian Federation’s Energy Strategy, dated August 28, 2003, formally Massachusetts Institute of Technology Building E38-200 states that Russia’s natural resources should be a fundamental element in Moscow’s diplo- 292 Main Street macy and that Russia’s position in global energy markets should be strengthened.1 In his Cambridge, MA 02139 own dissertation, Putin argued that the energy sector should be guided by the state and T: 617.253.8093 used to promote Russia’s national interests.2 And, the rector of the Mining Institute in F: 617.253.9330 which Putin wrote his dissertation and currently one of his energy advisors wrote: “In the [email protected] specific circumstances the world finds itself in today, the most important resources are web.mit.edu/cis/ hydrocarbons . -

Organized Crime 1.1 Gaizer’S Criminal Group

INTRODUCTION ......................................................................................................... 4 CHAPTER I. ORGANIZED CRIME 1.1 Gaizer’s Criminal Group ..................................................................................6 1.2 Bandits in St. Petersburg ............................................................................ 10 1.3 The Tsapok Gang .......................................................................................... 14 Chapter II.CThe Corrupt Officials 2.1 «I Fell in Love with a Criminal» ................................................................20 2.2 Female Thief with a Birkin Bag ...............................................................24 2.3 «Moscow Crime Boss».................................................................................29 CONTENTS CHAPTER III. THE BRibE-TAKERS 3.1 Governor Khoroshavin’s medal «THE CRIMINAL RUSSIA PARTY», AN INDEPENDENT EXPERT REPORT «For Merit to the Fatherland» ..................................................................32 PUBLISHED IN MOSCOW, AUGUST 2016 3.2 The Astrakhan Brigade ...............................................................................36 AUTHOR: ILYA YASHIN 3.3 A Character from the 1990s ......................................................................39 MATERiaL COMPILING: VERONIKA SHULGINA HAPTER HE ROOKS TRANSLATION: C 4. T C EVGENia KARA-MURZA 4.1 Governor Nicknamed Hans .......................................................................42 GRAPHICS: PavEL YELIZAROV 4.2 The Party