Insight February 2010

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Download Annual Report 2004/05

ETHIOPIAN AIRLINES Annual Report 2004-05 WWW.ETHIOPIANAIRLINES.COM ANNUAL REPORT 2004-05 building CONTENTS on the FUTURE Management Board of Ethiopian Airlines .................................. 2 CEO’s Message............................................................................................. 3 Ethiopian Airlines Management Team ......................................... 4 Embarking on a long-range reform I. Investing for the future Continent .................................... 5 II. Continuous Change .............................................................. 5 III. Operations Review ............................................................... 5 IV. Measures to Enhance Profitability .................................. 7 V. Human Resource Development ....................................... 10 VI. Fleet Planning and Financing .......................................... 11 VII. Information Systems .......................................................... 11 VIII. Tourism Promotion ............................................................ 11 IX. Corporate Social Responsibility (CSR) Measures ....... 12 Finance ............................................................................................................. 13 Auditors Report and Financial Statements ................................ 22 Domestic Route Map .............................................................................. 40 Ethiopian Airlines Offices ...................................................................... 41 International Route Map ...................................................................... -

IATA CLEARING HOUSE PAGE 1 of 21 2021-09-08 14:22 EST Member List Report

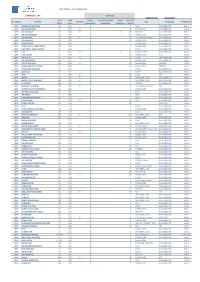

IATA CLEARING HOUSE PAGE 1 OF 21 2021-09-08 14:22 EST Member List Report AGREEMENT : Standard PERIOD: P01 September 2021 MEMBER CODE MEMBER NAME ZONE STATUS CATEGORY XB-B72 "INTERAVIA" LIMITED LIABILITY COMPANY B Live Associate Member FV-195 "ROSSIYA AIRLINES" JSC D Live IATA Airline 2I-681 21 AIR LLC C Live ACH XD-A39 617436 BC LTD DBA FREIGHTLINK EXPRESS C Live ACH 4O-837 ABC AEROLINEAS S.A. DE C.V. B Suspended Non-IATA Airline M3-549 ABSA - AEROLINHAS BRASILEIRAS S.A. C Live ACH XB-B11 ACCELYA AMERICA B Live Associate Member XB-B81 ACCELYA FRANCE S.A.S D Live Associate Member XB-B05 ACCELYA MIDDLE EAST FZE B Live Associate Member XB-B40 ACCELYA SOLUTIONS AMERICAS INC B Live Associate Member XB-B52 ACCELYA SOLUTIONS INDIA LTD. D Live Associate Member XB-B28 ACCELYA SOLUTIONS UK LIMITED A Live Associate Member XB-B70 ACCELYA UK LIMITED A Live Associate Member XB-B86 ACCELYA WORLD, S.L.U D Live Associate Member 9B-450 ACCESRAIL AND PARTNER RAILWAYS D Live Associate Member XB-280 ACCOUNTING CENTRE OF CHINA AVIATION B Live Associate Member XB-M30 ACNA D Live Associate Member XB-B31 ADB SAFEGATE AIRPORT SYSTEMS UK LTD. A Live Associate Member JP-165 ADRIA AIRWAYS D.O.O. D Suspended Non-IATA Airline A3-390 AEGEAN AIRLINES S.A. D Live IATA Airline KH-687 AEKO KULA LLC C Live ACH EI-053 AER LINGUS LIMITED B Live IATA Airline XB-B74 AERCAP HOLDINGS NV B Live Associate Member 7T-144 AERO EXPRESS DEL ECUADOR - TRANS AM B Live Non-IATA Airline XB-B13 AERO INDUSTRIAL SALES COMPANY B Live Associate Member P5-845 AERO REPUBLICA S.A. -

Liste-Exploitants-Aeronefs.Pdf

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, XXX C(2009) XXX final COMMISSION REGULATION (EC) No xxx/2009 of on the list of aircraft operators which performed an aviation activity listed in Annex I to Directive 2003/87/EC on or after 1 January 2006 specifying the administering Member State for each aircraft operator (Text with EEA relevance) EN EN COMMISSION REGULATION (EC) No xxx/2009 of on the list of aircraft operators which performed an aviation activity listed in Annex I to Directive 2003/87/EC on or after 1 January 2006 specifying the administering Member State for each aircraft operator (Text with EEA relevance) THE COMMISSION OF THE EUROPEAN COMMUNITIES, Having regard to the Treaty establishing the European Community, Having regard to Directive 2003/87/EC of the European Parliament and of the Council of 13 October 2003 establishing a system for greenhouse gas emission allowance trading within the Community and amending Council Directive 96/61/EC1, and in particular Article 18a(3)(a) thereof, Whereas: (1) Directive 2003/87/EC, as amended by Directive 2008/101/EC2, includes aviation activities within the scheme for greenhouse gas emission allowance trading within the Community (hereinafter the "Community scheme"). (2) In order to reduce the administrative burden on aircraft operators, Directive 2003/87/EC provides for one Member State to be responsible for each aircraft operator. Article 18a(1) and (2) of Directive 2003/87/EC contains the provisions governing the assignment of each aircraft operator to its administering Member State. The list of aircraft operators and their administering Member States (hereinafter "the list") should ensure that each operator knows which Member State it will be regulated by and that Member States are clear on which operators they should regulate. -

UPDATED ON: 18-03-2019 STATION AIRLINE IATA CODE AWB Prefix ON-LINE CARGO HANDLING FREIGHTER RAMP HANDLING RAMP LINEHAUL IMPORT

WFS CARGO - CUSTOMERS LIST DENMARK - CPH SERVICES UPDATED ON: 18-03-2019 IATA AWB CARGO FREIGHTER RAMP RAMP IMPORT STATION AIRLINE ON-LINE GSA TRUCKING TERMINAL CODE Prefix HANDLING HANDLING LINEHAUL EXPORT CPH AMERICAN AIRLINES AA 001 X E NAL WALLENBORN HAL 1 CPH DELTA AIRLINES DL 006 X X I/E PROACTIVE WALLENBORN HAL1 CPH AIR CANADA AC 014 X X X I/E HWF DK WALLENBORN HAL 1 CPH UNITED AIRLINES UA 016 X I/E NORDIC GSA WALLENBORN HAL1 CPH LUFTHANSA LH 020 X X I/E LUFTHANSA CARGO WALLENBORN HAL1 CPH US AIRWAYS US 037 X I/E NORDIC GSA WALLENBORN HAL1 CPH DRAGON AIR XH 043 X I NORDIC GSA WALLENBORN HAL1 CPH AEROLINEAS ARGENTINAS AR 044 X E CARGOCARE WALLENBORN HAL1 CPH LAN CHILE - LINEA AEREA LA 045 X E KALES WALLENBORN HAL1 CPH TAP TP 047 X X x I/E SCANPARTNER WALLENBORN HAL1 CPH AER LINGUS EI 053 X I/E NORDIC GSA N/A HAL1 CPH AIR France AF 057 X X I/E KL/AF KIM JOHANSEN HAL2 CPH AIR SEYCHELLES HM 061 X E NORDIC GSA WALLENBORN HAL1 CPH CZECH AIRLINES OK 064 X X I/E AviationPlus VARIOUS HAL1 CPH SAUDI AIRLINES CARGO SV 065 X I/E AviationPlus VARIOUS HAL1 CPH ETHIOPIAN AIRLINES ET 071 X E KALES WALLENBORN HAL1 CPH GULF AIR GF 072 X E KALES WALLENBORN HAL1 CPH KLM KL 074 X X I/E KL/AF JDR HAL2 CPH IBERIA IB 075 X X I/E UNIVERSAL GSA WALLENBORN HAL1 CPH MIDDLE EAST AIRLINES ME 076 X X E UNIVERSAL GSA WALLENBORN HAL1 CPH EGYPTAIR MS 077 X E HWF DK WALLENBORN HAL1 CPH BRUSSELS AIRLINES SN 020 X X I/E LUFTHANSA CARGO JDR HAL1 CPH SOUTH AFRICAN AIRWAYS SA 083 X E CARGOCARE WALLENBORN HAL1 CPH AIR NEW ZEALAND NZ 086 X E KALES WALLENBORN HAL1 CPH AIR -

Kuwait Passenger Airline Industry

July 2010 Industry Research Kuwait Passenger Airline Industry Summary Report Contents Middle East is emerging as a major aviation force driven by the regions Summary strong economic growth, ambitious expansion plans, and favorable Middle East Aviation Industry demographics. The majority population in the Middle East, particularly in the Gulf region is non-nationals, which form a sizeable travelling Kuwait Airline Industry population, primarily to their countries of origin. This is further supported Kuwait airways privatization by a rising younger population with high disposable income. The financial Airline Operators in Kuwait crisis has negatively affected the economies of the GCC region, despite Kuwait Airways that the aviation sector maintained a healthy growth. The GCC countries Wataniya Airways are highly reliant on the oil sector and hence face major challenges in Jazeera Airways diversifying the economy. The governments are focusing on real estate, Conclusion trade, tourism etc to diversify. List of related research The lack of railway network in the GCC region, a vibrant young population, liberalization of aviation sector, and rising disposable income Appendix has contributed to the robust growth in air traffic leading to the development of airports, expansion of fleet capacity and entrance of new operators. The region’s aviation sector has also been greatly helped by Analyst the global market liberalization, which were previously limited by Jyoti Prakash Singh restrictive controls. The major airlines in the region benefits from Associate Manager geographical location, young aircraft fleet, and low operating cost. Most j.singh @capstandards.com of the airlines focus is on high quality and timeliness at reasonable prices. -

DAQCP MEMBERS Created By: DAQCP Website Date: 20.07.2021

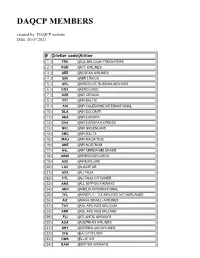

DAQCP MEMBERS created by: DAQCP website Date: 20.07.2021 # 3-letter code Airline 1 FRH ACE BELGIUM FREIGHTERS 2 RUN ACT AIRLINES 3 AEE AEGEAN AIRLINES 4 EIN AER LINGUS 5 AFL AEROFLOT RUSSIAN AIRLINES 6 BOX AEROLOGIC 7 KZR AIR ASTANA 8 BTI AIR BALTIC 9 ACI AIR CALEDONIE INTERNATIONAL 10 DLA AIR DOLOMITI 11 AEA AIR EUROPA 12 OVA AIR EUROPA EXPRESS 13 GRL AIR GREENLAND 14 AMC AIR MALTA 15 MAU AIR MAURITIUS 16 ANE AIR NOSTRUM 17 ASL AIR SERBIA BELGRADE 18 ABW AIRBRIDGECARGO 19 AXE AIREXPLORE 20 LAV ALBASTAR 21 AZA ALITALIA 22 CYL ALITALIA CITYLINER 23 ANA ALL NIPPON AIRWAYS 24 AEH AMELIA INTERNATIONAL 25 TFL ARKEFLY - TUI AIRLINES NETHERLANDS 26 AIZ ARKIA ISRAELI AIRLINES 27 TAY ASL AIRLINES BELGIUM 28 ABR ASL AIRLINES IRELAND 29 FLI ATLANTIC AIRWAYS 30 AUA AUSTRIAN AIRLINES 31 AHY AZERBAIJAN AIRLINES 32 CFE BA CITYFLYER 33 BMS BLUE AIR 34 BAW BRITISH AIRWAYS 35 BEL BRUSSELS AIRLINES 36 GNE BUSINESS AVIATION SERVICES GUERNSEY LTD 37 CLU CARGOLOGICAIR 38 CLX CARGOLUX AIRLINES INTERNATIONAL S.A 39 ICV CARGOLUX ITALIA 40 CEB CEBU PACIFIC 41 BCY CITYJET 42 CFG CONDOR FLUGDIENST GMBH 43 CTN CROATIA AIRLINES 44 CSA CZECH AIRLINES 45 DLH DEUTSCHE LUFTHANSA 46 DHK DHL AIR LTD. 47 EZE EASTERN AIRWAYS 48 EJU EASYJET EUROPE 49 EZS EASYJET SWITZERLAND 50 EZY EASYJET UK 51 EDW EDELWEISS AIR 52 ELY EL AL 53 UAE EMIRATES 54 ETH ETHIOPIAN AIRLINES 55 ETD ETIHAD AIRWAYS 56 MMZ EUROATLANTIC 57 BCS EUROPEAN AIR TRANSPORT 58 EWG EUROWINGS 59 OCN EUROWINGS DISCOVER 60 EWE EUROWINGS EUROPE 61 EVE EVELOP AIRLINES 62 FIN FINNAIR 63 FHY FREEBIRD AIRLINES 64 GJT GETJET AIRLINES 65 GFA GULF AIR 66 OAW HELVETIC AIRWAYS 67 HFY HI FLY 68 HBN HIBERNIAN AIRLINES 69 HOP HOP! 70 IBE IBERIA 71 ICE ICELANDAIR 72 ISR ISRAIR AIRLINES 73 JAL JAPAN AIRLINES CO. -

Effects of Information, Communication

EFFECT OF RELATIONSHIP MARKETING ON CUSTOMER SATISFACTION IN THE AIRLINE INDUSTRY IN KENYA HILDA CHEPKOECH STANLEY D53/OL/22100/2011 A RESEARCH PROJECT REPORT SUBMITTED TO SCHOOL OF BUSINESS IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE AWARD OF THE DEGREE OF MASTER OF BUSINESS ADMINISTRATION OF KENYATTA UNIVERSITY November 2013 DECLARATION This is my original work and has not been presented for the award of a degree in any other university or any other award. Signature………………………………………. Date……………………. HILDA CHEPKOECH STANLEY D53/OL/22100/2011 This project report has been submitted for examination with my approval as a university supervisor. Signature………………………………………. Date……………………. J.M. KILIKA, PhD Lecturer Department of Business Administration Kenyatta University Signature………………………………………. Date……………………. S. MUATHE, PhD Chairman Department of Business Administration Kenyatta University ii DEDICATION I dedicate this thesis to my parents who gave me the opportunity of an education and for teaching me that even the largest task can be accomplished if it is done one step at a time. To my siblings, for their love, support and encouragement to complete this task. iii ACKNOWLEDGEMENT I thank God for the wisdom and perseverance that he has bestowed upon me during this research project, and indeed, throughout my life. First and foremost, I would like to express my sincere gratitude to my supervisor Dr. James Kilika for his criticism, insightful comments, guidance, and immense knowledge that greatly helped me in compiling this project, and in making this research possible. My appreciation also goes to my friends for their continual support and encouragement throughout this program. Of course, this project would not have been possible without the participation of the subjects. -

Report Afraa 2016

AAFRA_PrintAds_4_210x297mm_4C_marks.pdf 1 11/8/16 5:59 PM www.afraa.org Revenue Optimizer Optimizing Revenue Management Opportunities C M Y CM MY CY CMY K Learn how your airline can be empowered by Sabre Revenue Optimizer to optimize all LINES A ® IR SSO A MPAGNIE S AER CO IEN C N ES N I A D ES A N A T C IO F revenue streams, maximize market share I T R I I O R IA C C A I N F O N S E S A S A ANNUAL and improve analyst productivity. REPORT AFRAA 2016 www.sabreairlinesolutions.com/AFRAA_TRO ©2016 Sabre GLBL Inc. All rights reserved. 11/16 AAFRA_PrintAds_4_210x297mm_4C_marks.pdf 2 11/8/16 5:59 PM How can airlines unify their operations AFRAA Members AFRAA Partners and improve performance? American General Supplies, Inc. Simplify Integrate Go Mobile C Equatorial Congo Airlines LINKHAM M SERVICES PREMIUM SOLUTIONS TO THE TRAVEL, CARD & FINANCIAL SERVICE INDUSTRIES Y CM MY CY CMY K Media Partners www.sabreairlinesolutions.com/AFRAA_ConnectedAirline CABO VERDE AIRLINES A pleasurable way of flying. ©2016 Sabre GLBL Inc. All rights reserved. 11/16 LINES AS AIR SO N C A IA C T I I R O F N A AFRICAN AIRLINES ASSOCIATION ASSOCIATION DES COMPAGNIES AÉRIENNES AFRICAINES AFRAA AFRAA Executive Committee (EXC) Members 2016 AIR ZIMBABWE (UM) KENYA AIRWAYS (KQ) PRESIDENT OF AFRAA CHAIRMAN OF THE EXECUTIVE COMMITTEE Captain Ripton Muzenda Mr. Mbuvi Ngunze Chief Executive Officer Group Managing Director and Chief Executive Officer Air Zimbabwe Kenya Airways AIR BURKINA (2J) EGYPTAIR (MS) ETHIOPIAN AIRLINES (ET) Mr. -

International Civil Aviation Organization Middle East Regional Office

INTERNATIONAL CIVIL AVIATION ORGANIZATION MIDDLE EAST REGIONAL OFFICE WILDLIFE HAZARD MANAGEMENT AND CONTROL (WHMC) WORKSHOP (Khartoum, Sudan, 10-12 December 2018) SUMMARY OF DISCUSSIONS 1. INTRODUCTION 1.1 The Wildlife Hazard Management and Control (WHMC) Workshop was successfully held in Khartoum, Sudan, from 10 to 12 December 2018 and hosted by the Sudan Civil Aviation Authority (SCAA). 1.2 The Workshop was attended by eighty-five (85) participants from five (5) States (Botswana, Egypt, Iran, Kenya and Sudan). The list of participants is at Attachment A. 1.3 The Workshop was opened by H.E. Capt. Ahmed Satti Abdelrahman Bajouri, Director General, Sudan Civil Aviation Authority (SCAA) who welcomed the participants to Sudan and thanked them for their attendance to this important Workshop and wished successful deliberations and outcomes. 1.4 Mr. Fakhreldin Osman Ahmed Mehadi, Aerodromes Safety & Standards, Sudan Civil Aviation Authority (SCAA) and Mr. Mohamed Iheb Hamdi, Regional Officer, Aerodromes and Ground Aids (AGA), ICAO Middle East were the Facilitators of the Workshop. 2. DISCUSSION 2.1 The Objective of the Workshop was to raise awareness about WHMC, share experiences/best practices and promote techniques and strategies related to WHMC. It included three days of presentations (10-12 December 2018) covering relevant Wildlife Hazard Management topics and providing feedback on implementation issues, especially those related to Wildlife Hazard Management Plan. The Workshop consisted of a forum where CAAs, Airports Operators, ANSP, -

Airlines and Subsidy: Our Position ¬

Airlines and subsidy: our position ¬ Myth Airline subsidies are a “Gulf” problem FACT Market-distorting subsidies and government support are sadly present in every world region Myth Emirates is subsidised FACT Completely unsubsidised. We campaign against airline subsidies Myth Emirates accesses cheap or free fuel FACT False. We buy fuel from BP, Shell and Chevron in Dubai and worldwide at market rates Myth US and European airlines received support decades ago but are now subsidy-free FACT Bankruptcy protection and government bailouts continue to exist Airlines and subsidy: our position ¬ We understand that despite no evidence, an oft repeated myth can ultimately be accepted as conventional wisdom. In this document you will find our views on subsidy in the airline industry, thorough explanations about Emirates’ business model and our response to misrepresentations that have been levelled against us - from claims about subsidised fuel, financial support and staff conditions to environmental regulation and airport charges. Emirates believes: • A common set of transparent financial reporting metrics to measure and apply against all international carriers should be determined by IATA and ICAO on what defines a subsidy. • Governments should not provide injections, borrowings or financing to airlines, regardless of shareholding status. • All governments should pursue liberalisation and open skies with the objective to end the greatest subsidy of all – aero-political protection. Tim Clark, President, Emirates Airline 1 Contents ¬ Introduction -

Airbus Presentation

AirbusAirbus andand thethe MiddleMiddle EastEast aa storystory ofof historyhistory andand futurefuture Fouad Attar Head of Commercial, Airbus Middle East Muscat, 21st October 2009 a world of cultural diversity Airbus, a global company … with global outreach 20 languages 3 customer support centres More than 5,500 aircraft delivered 13 manufacturing sites 52,000 employees 315 operators 5 spares centres more than 88 nationalities 312 customers engineering design centres training centres 9 250 resident customer support managers 4 160 offices 24 hour customer support (365 days a year) 50 flight simulators 1 global company © AIRBUS S.A.S. All rights reserved. Confidential and proprietary document. SEPT 2009 2 Airbus, a long history © AIRBUS S.A.S. All rights reserved. Confidential and proprietary document. 3 Airbus, Middle East, example milestones A300 A300 Iranair Iranair ‘80 ‘80 A320 ‘92 A300 A320 ‘92 A300 A310/A300 ’93/’94 Egyptair A310/A300 ’93/’94 Egyptair Kuwait Airways A320 ’09 ‘80 Kuwait Airways A320 ’09 ‘80 Saudi Arabian Saudi Arabian A300 A300 Saudi Arabian A330 ’99 A380 ’08 Saudi Arabian A330 ’99 A321 ’03 A380 ’08 ‘84 Emirates A321 ’03 Emirates ‘84 Emirates MEA Emirates MEA A300 A340-600 ’06 A330 ’09 A300 A340-600 ’06 A330 ’09 PIA A320 ‘91 Qatar Airways Oman Air PIA A320 ‘91 Qatar Airways Oman Air ‘80 Egyptair A340 ‘94 ‘80 Egyptair A340 ‘94 Gulf Air A310 Gulf Air A310 A340-600 ’06 Kuwait Airways A340-600 ’06 Kuwait Airways A320 ‘92 Etihad ‘83 A320 ‘92 Etihad ‘83 Gulf Air Gulf Air A320 ‘90 A320 ‘90 Royal Jordanian Airbus Office Airbus Middle East Royal Jordanian Airbus Office Airbus Middle East Dubai Dubai Dubai Dubai ‘00 ‘06 ‘00 ‘06 8989 90 90 91 91 92 92 93 93 94 94 95 95 96 96 97 97 98 98 99 99 00 00 01 01 02 02 03 03 04 04 05 05 06 06 07 07 08 08 09 09 Source data: AIRBUS © AIRBUS S.A.S. -

The History and Development of Aviation in the State of Kuwait

The International Journal of Engineering and Science (IJES) || Volume || 6 || Issue || 4 || Pages || PP 14-20 || 2017 || ISSN (e): 2319 – 1813 ISSN (p): 2319 – 1805 The History and Development of Aviation in the State of Kuwait Fadala Hassan Alfadala Higher Institute of Telecommunication and Navigation State of Kuwait I. INTRODUCTION The aviation industry today is a growing industry but is faced with many challenges that entail “rough decisions, forcing them to ground planes, pare fleets, consolidate routes, and cut staff” (“2011 Global Aerospace Outlook,” 2011). As a result, airline companies try to survive by having leaner organizations that aspire for efficiency; they aim for competitiveness and yet work on reducing costs in all possible ways. They are bombarded with issues such as increasing or fluctuating fuel prices which affect their profit margins; there are also companies that approach challenges with a “wait and see” attitude as they await what will happen and how they will perform as situations happen; but there also those that are confronted by emerging developments that challenge them to increase their fleets, number of routes and seat capacities; they are also pressed with the need to find other lucrative businesses to augment future profitability like charging fees for checked bags, food or in-flight entertainment; they may also offer operating leases as fleet financing opportunity for many airlines. Being part of the aviation industry also requires aviation companies to keep abreast of what is new in the global aviation market. Although it is a promising market having steady growth and development, there is a growing need to continually upgrade or innovate to make the industry lucrative in a global scale.