Capital Markets: Debt

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Why Switzerland?

Why Switzerland? Marwan Naja, AS Investment Management January, 2010 I. Executive Summary Swiss Equities Have Outperformed: Here is a fact you probably did not know: The Swiss equity market has arguably been the best performing developed world market over the past 20, 10, 5 and 2 years. The SPI Index, which incorporates over 200 Swiss stocks, is the best performing index in Swiss Franc (“CHF”), US Dollars (“USD”), Euro (“EUR”) and British Pounds (“GBP”) over the past 20 years1,10 years, 5 years, and 2 years when compared to similar broad-based total return indices in the United States (S&P 500 Total Return), the United Kingdom (FTSE 350 Total Return), Germany (CDAX), France (SBF 120 Total Return) and Japan (TOPIX Total Return)2. For most of these periods the magnitude of the outperformance is significant. Furthermore, the Swiss market has exhibited attractive risk characteristics including lower volatility than comparable markets. Figure 1: SPI 20 Year Performance (red) Compared to Major Developed Indices in CHF3 1 The 20 year comparable excludes the EUR which has not existed for that duration and the French SBF 120 TR which was established in 1990 and has underperformed the SPI over the 19 year period. 2 The Swiss market is the best performer in our local currency comparison (stripping out the foreign exchange effects) over 20 years and marginally trails the FTSE 350 for the 10 year, 5 year and 2 year comparisons. 3 Source of all graphs is Bloomberg unless otherwise indicated. Why Switzerland? AS Investment Management Contents I. Executive Summary ............................................................................................................ 1 Swiss Equities Have Outperformed ................................................................................... -

Aktienmarkt Schweiz Lukrative Klettertour Zu Neuen Kursgipfeln

all about investment products #8 August 2017 14. Jahrgang CHF 12.50 www.payoff.ch AKTIENMARKT SCHWEIZ LUKRATIVE KLETTERTOUR ZU NEUEN KURSGIPFELN Interview Marc Possa, Geschäftsführer & Partner bei [vv] vermögensverwaltung ag Seite 10 Learning Curve VSTOXX: Der Puls der europäischen Aktienmärkte Seite 15 IN EINER WELT IM WANDEL KÖNNEN KLEINE EINSÄTZE GROSSE WIRKUNG ZEIGEN MINI-FUTURE ZERTIFIKATE Mit Mini-Future Zerti katen lassen sich kurzfristige Markttrends bereits mit geringem Einsatz ausnutzen, und das sowohl bei steigenden als auch fallenden Kursen. Zudem bieten Mini-Future Zerti kate eine einfache und kostengünstige Möglichkeit, ein beste- hendes Portfolio gegen sinkende Kurse abzusichern. www.bnpparibasmarkets.ch Mitglied bei: [email protected] +41 (0)58 212 68 50 Wir machen Sie darauf aufmerksam, dass die Gespräche auf der angegebenen Telefonnummer aufgezeichnet werden. Bei Ihrem Anruf erklären Sie sich mit dieser Geschäftspraxis einverstanden. Risikohinweis: Dieses Werbeinserat stellt keinen vereinfachten Prospekt im Sinne von Art. 5 des Bundesgesetzes über die kollektiven Kapitalanlagen oder Emissionsprospekt im Sinne der Art. 652a und 1156 des Schweizerischen Obligationenrechts dar. Es handelt sich zudem weder um eine Aufforderung, noch um eine Empfehlung zum Kauf. Die in diesem Werbeinserat beschriebenen Produkte werden von BNP ParibasIssuance B.V. ausgegeben und sind derivative Finanzinstrumente. Der alleinverbindliche Prospekt in englischer Sprache kann direkt bei BNP Paribas Securities Services, Paris, Zweigniederlassung Zürich, Selnaustrasse 16, Postfach, 8022 Zürich, oder unter der Tel. +41 58 212 63 35 bezogen werden. Die Produkte qualifi zieren nicht als Anteile einer kollektiven Kapitalanlage im Sinne des Bundesgesetzes über die kollektiven Kapitalanlagen und sind daher auch nicht der Aufsicht der Eidgenössischen Finanzmarktaufsicht (FINMA) unterstellt. -

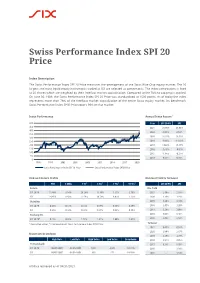

Swiss Performance Index SPI 20 Price

Swiss Performance Index SPI 20 Price Index Description The Swiss Performance Index SPI 20 Price measures the development of the Swiss Blue Chip equity market. The 20 largest and most liquid equity instruments traded at SIX are selected as components. The index composition is fixed to 20 shares which are weighted by their freefloat market capitalisation. Compared to the SMI no capping is applied. On June 30, 1988, the Swiss Performance Index SPI 20 Price was standardised at 1500 points. As of today the index represents more than 78% of the freefloat market capitalization of the entire Swiss equity market. Its benchmark Swiss Performance Index SPI® Price covers 99% of that market. Index Performance Annual Index Return¹ 500 Year SPI 20 PR SPI 450 2021 23.96% 25.98% 400 2020 -0.55% 0.61% 350 2019 26.35% 26.51% 300 250 2018 -9.44% -11.43% 200 2017 14.02% 16.37% 150 2016 -6.78% -4.67% 100 2015 -1.84% -0.25% 50 2014 9.51% 9.73% 0 1996 1999 2002 2005 2008 2011 2014 2017 2020 Swiss Performance Index SPI 20 Price Swiss Performance Index SPI® Price Risk and Return Profile Dividend Yield & Turnover YTD 3 Mths 1 Yr¹ 3 Yrs¹ 7 Yrs¹ 15 Yrs¹ SPI 20 PR SPI Return Div. Yield SPI 20 PR 15.40% 8.94% 20.26% 11.16% 5.17% 2.78% 2021 2.80% 2.58% SPI 16.65% 8.68% 22.59% 10.78% 6.01% 3.23% 2020 3.36% 3.19% Volatility 2019 3.24% 3.10% SPI 20 PR 0.63% 0.53% 0.74% 0.59% 0.38% 0.29% 2018 3.45% 3.20% SPI 0.61% 0.50% 0.72% 0.58% 0.36% 0.28% 2017 3.29% 3.09% Tracking Err. -

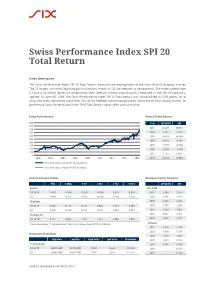

Swiss Performance Index SPI 20 Total Return

Swiss Performance Index SPI 20 Total Return Index Description The Swiss Performance Index SPI 20 Total Return measures the development of the Swiss Blue Chip equity market. The 20 largest and most liquid equity instruments traded at SIX are selected as components. The index composition is fixed to 20 shares which are weighted by their freefloat market capitalisation. Compared to the SMI no capping is applied. On June 30, 1988, the Swiss Performance Index SPI 20 Total Return was standardised at 1500 points. As of today the index represents more than 78% of the freefloat market capitalization of the entire Swiss equity market. Its benchmark Swiss Performance Index SPI® Total Return covers 99% of that market. Index Performance Annual Index Return¹ 900 Year SPI 20 TR SPI 810 2021 29.20% 30.89% 720 630 2020 2.79% 3.82% 540 2019 30.43% 30.40% 450 2018 -6.31% -8.59% 360 270 2017 17.79% 19.98% 180 2016 -3.38% -1.41% 90 2015 1.15% 2.68% 0 1996 1999 2002 2005 2008 2011 2014 2017 2020 2014 12.94% 13.00% Swiss Performance Index SPI 20 Total Return Swiss Performance Index SPI® Total Return Risk and Return Profile Dividend Yield & Turnover YTD 3 Mths 1 Yr¹ 3 Yrs¹ 7 Yrs¹ 15 Yrs¹ SPI 20 TR SPI Return Div. Yield SPI 20 TR 18.63% 8.94% 23.83% 14.68% 8.61% 6.03% 2021 2.80% 2.58% SPI 19.66% 8.72% 25.98% 14.08% 9.28% 6.32% 2020 3.36% 3.19% Volatility 2019 3.24% 3.10% SPI 20 TR 0.63% 0.53% 0.74% 0.60% 0.38% 0.29% 2018 3.45% 3.20% SPI 0.61% 0.50% 0.72% 0.58% 0.36% 0.28% 2017 3.29% 3.09% Tracking Err. -

Fondation De Placement Swiss Life Actions Suisse Large Caps Indexées

31 août 2021 Fondation de placement Swiss Life Actions Suisse Large Caps Indexées Fortune nette (VNI) en mio. CHF : 237.75 Valeur nette d'inventaire par droit en CHF : 148.85 Stratégie d'investissement Performance Placement dans des titres de participation de sociétés représentées dans le SPI 20. Mise en oeuvre indexée, le benchmark étant entièrement reproduit («full replication»). L’écart entre la pondération par société et celle du benchmark ne peut être supérieur à +/- 0,5 point de pourcentage. Réalisation au moyen du Swiss Life iFunds (CH) Equity Switzerland (CHF); fonds de placement de droit suisse de la catégorie "Autres fonds en placements traditionnels". Évolution de la valeur en devise de référence (base 100) Info. sur le produit Numéro de valeur: 39561885 ISIN: CH0395618850 LEI: 254900P0FZIREAGSUQ60 Code Bloomberg: SLASLCI SW Benchmark: SPI 20 Total Return® Monnaie: CHF Pays d’origine: Suisse Date de création: 01/02/2018 Valeur de lancement: 100.00 Clôture de l'exercice: 30.09 Les performances passées ne préjugent pas des performances futures. Souscription/Rachat: journalier Délai final d’acceptation: 14h30 Commission de souscription/rachat: Performances en devise de référence aucune Pratique de distribution: Capitalisation PERFORMANCES CUMULÉES PERFORMANCES ANNUALISÉES Asset Manager selon YTD 1 MOIS 1 AN 3 ANS 5 ANS 10 ANS ORIGINE Swiss Life Best Select Invest Plus®: Pictet Asset Management SA GROUPE DE PLACEMENT 18.23% 2.30% 23.28% 14.19% - - 11.75% Conseil externe: BENCHMARK 18.63% 2.34% 23.83% 14.67% - - 12.19% PPCmetrics fournit les prestations suivantes: conseil concernant la bonne structure de mandat, aide à la sélection de gestionnaires de fortune adéquats et Données statistiques soutien dans le cadre de la surveillance 1 AN 3 ANS 5 ANS 10 ANS ORIGINE continue du gestionnaire de fortune, ainsi (annualisées) qu’évaluation des résultats des placements. -

Swiss Reference Rates

Swiss Reference Rates Internationally, overnight interest rates play a significant role in determining the yield curve. Going forward, the point of departure for Switzerland’s yield curve is SARON®, a reference rate based on data from the Swiss franc repo market. Repo transactions represent an important instrument A reference rate must provide a representative picture of for banks in their daily liquidity management activities. market events, in order for it to be accepted by the mar- Repo transactions have become a key pillar of the money ket and regularly used for transactions. Between 2015 and markets – even the Swiss National Bank (SNB) uses repo 2017 the average daily volume on which SARON is based transactions as a means of implementing its monetary on amounted from CHF 4 to 8 billion (see chart), about policy. 44% of which is attributable to the volume of CHF repo transactions. The rest is based on the volume of repre- The new reference rate, SARON, will play an influential sentative tradable quotes. The volume increased during role in financial markets. The Swiss Reference Rates com- the financial crisis, reaching around CHF 14 billion on av- prise a total of 32 benchmark rates that cover a term spec- erage. The decline during the later stages of the crisis was trum ranging from overnight (ON) to 12 months (12M) plus the result of the massive liquidity injections by the SNB, two distinct indices for the ON term. The relevant calcu- which rendered part of interbank business superfluous. lations are based on CHF repo transactions concluded The Swiss Reference Rates rules were drawn up in collab- in the interbank market as well as on indicative quotes oration with the SNB. -

Blue Chips Bremsklötze Des

all about investment products #8 August 2018 15. Jahrgang CHF 12.50 www.payoff.ch BLUE CHIPS BREMSKLÖTZE DES Interview Daniel Mewes, Leiter Investment Solutions, PostFinance Seite 12 Learning Curve Rappenspalter auf dem Trading-Floor Seite 17 2 EDITORIAL HERAUSGEBERIN Derivative Partners AG SWISSNESS IM DEPOT Splügenstrasse 10, 8002 Zürich Telefon 043 305 05 30 www.derivativepartners.com Die August-Ausgabe widmen wir, passend zum Bundesfeiertag, REDAKTIONSLEITUNG dem heimischen Aktienmarkt. Gutes liegt oft näher als man Dieter Haas denkt! Doch bei allem Investment-Patriotismus wirft insbeson- [email protected] dere die Analyse der Schweizer Blue-Chips Fragen auf. Alle Daniel Manser Geschäftsführer AUTORENTEAM Jumbos im Swiss Market Index – Nestlé, Novartis und Roche Andreas Hausheer, Jürgen Kob, Martin Raab – stecken mitten in einem schwierigen Transformationsprozess. [email protected] Ein Kursvergleich über 20 Jahre zeigt schonungslos die schwache ANZEIGEN Wertsteigerung dieser Titel. Einzig mit üppigen Dividenden wur- Isabelle Tschugmall den die Aktionäre stets geschickt zufriedengestellt. In unserer [email protected] Titelstory stellen wir sinnvolle Alternativen mit direktem Bezug DESIGN UND LAYOUT zum Schweizer Aktienmarkt vor. Katsara Somrej [email protected] Wer investiert, muss sich auch über sinnvolles, effizientes Order- DRUCK routing Bescheid wissen. Zumindest sollte man als Anleger eine Triner AG Grundahnung haben, was wo wieviel kostet und welcher Broker Schmiedgasse 7 bzw. Depotbank was alles an Service leistet. Wir haben die Mühe 6431 Schwyz auf uns genommen und von 15 Anbietern die jeweiligen Preise ABOS UND ADRESSÄNDERUNGEN und Leistungen konsolidiert. Schade, haben drei bekannte Ban- [email protected] ken eine Offenlegung der abgefragten Konditionen verweigert ERSCHEINUNGSWEISE/ABO – zu beschäftigt mit wichtigeren Dingen. -

Vontobel Fund (CH)

Vontobel Asset Management Vontobel Fund (CH) Annual Report 2018/2019 U M B R E L L A F U N D U N D E R S W I S S L A W O F T H E T Y P E "O T H E R F U N D S F O R T R A D I T I O N A L I N V E S T M E N T S" Audited annual report as at February 28, 2019 for the period from March 1, 2018 to February 28, 2019 This document is not an offer to purchase or subscribe to units but is for informational purposes only. Units of an investment fund under Swiss law may only be subscribed on the basis of the current prospectus, including the fund contract, the current annual and semi-annual reports and the Key Investor Information Document. An investment in this fund entails risks, which are described in the prospectus. All documents may be obtained free of charge from Vontobel Fonds Services AG, Gotthardstrasse 43, 8022 Zurich, as fund management company, from Bank Vontobel AG, Gotthardstrasse 43, 8022 Zurich, and from RBC Investor Services Bank S.A., Esch-sur-Alzette, Zurich branch, Bleicherweg 7, 8027 Zurich, as paying agents, or via funds.vontobel.com. We also recommend that you contact your personal account manager or another advisor before making any investments. Vontobel Fund (CH) Contents Organisation 2 Basic data 4 Performance 14 Vontobel Fund (CH) - Sustainable Swiss Equity 17 Vontobel Fund (CH) - Ethos Equities Swiss Mid & 25 Small Vontobel Fund (CH) - Swiss Franc Core Bond 31 Vontobel Fund (CH) - Swiss Franc Corporate Bond 40 Vontobel Fund (CH) - Pension Invest Yield 53 Vontobel Fund (CH) - Pension Invest Balanced 73 Vontobel Fund (CH) -

SXI® Special Industry Indices

SXI® Special Industry Indices SXI LIFE SCIENCES® and SXI Bio+Medtech® The SXI Family consists of specially selected sector indi- of two indices: SXI LIFE SCIENCES® (Pharma, Medtech and ces. The sectors are selected according to two criteria: Biotech) and its more narrowly circumscribed sub-index, their international significance and the number of SIX SXI Bio+Medtech. These index instruments meet the listed companies that belong to them. The SXI indices growing desire of institutional investors to invest in these comprise primary listed companies and investment market segments, and they also increase the attractive- companies in case they have invested less than 50% of ness of SIX as a market for companies in these sectors. their assets in SXI shares. Another feature of the SXI To sum up, the SXI Fami ly offers Swiss and foreign com- indices is that the weighting of any individual security panies in the relevant sectors an attractive platform and is limited to 10%. The pur pose of this weight cap is to provides investors with a benchmark for the highly pros- increase diversification and relative importance of pering industry. smaller constitu ents. The SXI Family currently consists SXI® Family data Symbol Security no. ISIN Reuters RIC Bloomberg ticker SXI LIFE SCIENCES® Price SLIFEX 17810 1781076 CH0017810760 .SLIFEX SLIFEX Total Return SLIFE 1781073 CH0017810737 .SLIFE SLIFE SXI Bio+Medtech® Price SBIOMX 17811156 CH0017811156 .SBIOMX SBIOMX Total Return SBIOM 17810794 CH0017810794 .SBIOM SBIOM Equity index structure Number of Shares SPI® -

Vontobel Fund (CH) Annual Report 2020 /2021

Vontobel Asset Management Vontobel Fund (CH) Annual Report 2020 /2021 UMBRELLA FUND UNDER SWISS LAW OF THE TYPE « OTHER FUNDS FOR TRADITIONAL INVESTMENTS » Audited annual report as at February 28, 2021 for the period from March 1, 2020 to February 28, 2021 In case of a difference between the English and the German version, only the German version takes precedence. This document is not an offer to purchase or subscribe to units but is for informational purposes only. Units of an investment fund under Swiss law may only be subscribed on the basis of the current prospectus, including the fund contract, the current annual and semi-annual reports and the Key Investor Information Document. An investment in this fund entails risks, which are described in the prospectus. All documents may be obtained free of charge from Vontobel Fonds Services AG, Gotthardstrasse 43, CH-8022 Zurich, as fund management company, from Bank Vontobel AG, Gotthardstrasse 43, CH-8022 Zurich, and from RBC Investor Services Bank S.A., Esch-sur-Alzette, Zurich branch, Bleicherweg 7, CH-8027 Zurich, as paying agents, or via funds.vontobel.com. We also recommend that you contact your personal account manager or another advisor before making any investments. Vontobel Fund (CH) Contents Organisation 2 Basic data 4 Performance 13 Vontobel Fund (CH) - Sustainable Swiss Equity 15 Vontobel Fund (CH) - Ethos Equities Swiss Mid & Small 24 Vontobel Fund (CH) - Swiss Franc Corporate Bond 30 Vontobel Fund (CH) - Pension Invest Yield 43 Vontobel Fund (CH) - Pension Invest Balanced 62 -

Alcon Indices 07 15 20 (Sorted).Xlsx

ALCON ALC.SWX Index inclusion ACWI ex Australia Islamic Beneficiaries of ECB CDP Bloomberg EMEA ‐World Index Bloomberg Europe 500 Economic Sectors Index Bloomberg Europe 500 Health Care Index Bloomberg Europe Consumer Non‐cyclical Index Bloomberg European 500 Index Bloomberg European Consumer Non‐Cyclical Index Bloomberg World Consumer Non Cyclical Index Bloomberg World Health Care Products Index Bloomberg World Index Dow Jones Islamic Market Global ex Americas Index USD Dow Jones Switzerland Titans 30 Index CHF Euronext Low Carbon 100 Europe Index FTSE All World ex Greece Index USD FTSE All‐World ex North America Index USD FTSE Custom Composite UK All‐Share 50% Net Tax Index FTSE Developed Blended (022 & 045) PGGM Customized For NE NI CO2 Optimised PGGM FTSE Developed Europe All Cap Net Tax (US RIC) Index FTSE Developed ex US All Cap Net Tax (US RIC) Index FTSE Developed ex US Low Beta Equal Weight Net Tax (US RIC) Index FTSE Developed Large Cap Total Return Index FTSE EMEA INDEX USD FTSE Eurofirst Supersector Index FTSE RAFI All World 3000 Hedged to GBP Total Return Index FTSEurofirst 300 Economic Sector Index GEAR Global Short Index Invesco FTSE RAFI Developed Markets ex‐U.S. ETF INAV Index John Hancock Dimensional Developed International Index Knowledge Leaders Developed World TR Index Knowledge Leaders International TR Index MSCI AC Europe ESG Leaders Index STRD USD EOD MSCI EAFE Choice ESG Screened Index MSCI EAFE ESG Leaders Index MSCI Europe ESG Leaders Index MSCI Europe ex UK with Special Taxes Net Return EUR Index MSCI Europe SRI S‐Series 5% Capped Net Return EUR Index MSCI OFI Revenue Weighted Global ESG RT Price Return USD Index MSCI OFI Revenue Weighted Global ESG RT Price Return USD Index MSCI Pan Euro Index MSCI World Custom ESG Climate Series A Net in EUR MSCI World Custom ESG Climate Series A Net in GBP MSCI World ESG Leaders Index MSCI World ex US ESG Leaders Index MSCI World ex USA IMI (VRS Taxes) Net Return USD Index Page 1 ALCON MSCI World SRI S‐Series 5% Capped Net Return USD Index S&P Developed BMI (US Dollar) S&P Developed Ex‐U.S. -

Swiss Market Index (SMI®) Family

Swiss Market Index (SMI®) Family The SMI® Family: SMI®, SMIM® and SMI Expanded® of 20%. This makes the SMI fully complied with the ESMA The SMI Family, which is the best-known index family of UCITS guidelines and it can be used as a reference index SIX Swiss Exchange, comprises the 50 largest and most for the Swiss equity market in the European Union. The liquid stocks in the Swiss equity market. The blue chip in- SMIM comprises the next group of the 30 largest and most dex SMI is the most important stock index in Switzerland liquid mid-cap stocks. All SMI and SMIM stocks are con- and comprises the 20 largest stocks from the SPI. The SMI solidated in the SMI Expanded. The SMI Expanded covers covers approximately 80% of the total capitalisation of more than 90% of the capitalisation of the Swiss equity the Swiss equity market. The weights of the index compo- market. nents are capped so that no component exceeds a weight SMI® Family data Symbol Security no. ISIN Reuters RIC Bloomberg ticker SMI® Price SMI 998089 CH0009980894 .SSMI SMI Total Return SMIC 22213 CH0000222130 .SMIC SMIC SMIM® Price SMIM 1939983 CH0019399838 .SMIM SMIM Total Return SMIMC 1939982 CH0019399820 .SMIMC SMIMC SMI Expanded® Price SMIEXP 1939986 CH0019399861 .SMIEXP SMIEXP Total Return SMIEXC 1939985 CH0019399853 .SMIEXC SMIEXC Equity index structure Number of Shares SPI®-Family SMI®-Family SLI® SXI®-Family 0 Investment ® ® ® SLI Swiss SXI SXI® SXI Switzerland Index SPI Large SPI 20 SMI * ** Leader Real Estate® Special Industry Sustainability 25® 20 SMI Index® 30 Expanded®