Alcon Indices 07 15 20 (Sorted).Xlsx

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CS ETF (CH) on SLI Holding AG, Novartis AG and UBS AG

Simplified Prospectus • October 2011 ® the SLI® as at August 15, 2011 were as follows: Nestlé SA, Roche CS ETF (CH) on SLI Holding AG, Novartis AG and UBS AG. The composition of the index is Subfund of the Umbrella Fund of the Category periodically updated by SIX Swiss Exchange. “Other Funds for Traditional Investments” Risk Profile of the Subfund Simplified Prospectus The value of the Subfund’s investments is governed by the market value of investments at any given time. Depending on the prevailing stock October 2011 market trend and the performance of the stocks held in the portfolio, the net asset value can fluctuate considerably. The possibility of a depreciation Distribution in Switzerland and Liechtenstein in value over longer periods cannot be ruled out. There is no guarantee that the investors will receive a certain return and that they will be able to return their units to the fund management company for redemption at a certain price. When redeeming units, it is possible that an investor will not Note recoup the amount originally invested in the Subfund. This simplified prospectus contains a summary of the key information on CS ETF (CH) on SLI®1 (the “Subfund”). The legal and financial aspects Performance of the Subfund (in %) are governed conclusively by the full sales prospectus with integrated fund (change in the net asset value where distributions are reinvested) contract. These govern, among other things, the rights of the investors, the duties and obligations of the fund management company and the 40.0% custodian bank, and the investment policy of the Fund. -

Does International Diversification Pay?

Does International Diversification Pay? Vivek Bhargava1, Daniel K. Konku2, and D. K. Malhotra3 Advances in computer and telecommunications technology have contributed to the emergence of more integrated global financial markets, allowing for the dissemination of information and the execution of transactions on a real-time basis around the clock and around the globe. To determine if an investor can gain additional diversification benefits by investing in today’s increasingly integrated global financial markets, returns on four different indexes—Standard & Poor’s Composite 500 (S&P 500); Morgan Stanley Capital International (MSCI) World Index; Europe, Australia, and Far East (EAFE) Index; and the MSCI Europe Index—are analyzed for a 22-year period, from 1978 to 2000. Although the benefits from international diversification are decreasing, an investor is better off investing a portion of his or her portfolio in international markets, especially the European markets. Keywords: Diversification, Mutual fund selection, Risk reduction Introduction The objective of this paper is to determine whether an Globalization of financial markets is one of the most investor today can still gain diversification benefits significant economic developments over the last by investing in international markets. The monthly decade. Advances in computer and returns of four different indexes--Standard & Poor’s telecommunications technology contributed to the 500 (S&P 500); Morgan Stanley Capital International emergence of global financial markets, permitting the (MSCI) World Index; the Europe, Australia and Far dissemination of information and execution of East (EAFE) Index; and the MSCI Europe Index— transactions on a real-time basis around the clock and are analyzed over a 22-year period, from 1978 to around the globe. -

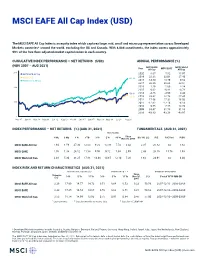

MSCI EAFE All Cap Index (USD)

MSCI EAFE All Cap Index (USD) The MSCI EAFE All Cap Index is an equity index which captures large, mid, small and micro cap representation across Developed Markets countries* around the world, excluding the US and Canada. With 8,088 constituents, the index covers approximately 99% of the free float-adjusted market capitalization in each country. CUMULATIVE INDEX PERFORMANCE — NET RETURNS (USD) ANNUAL PERFORMANCE (%) (NOV 2007 – AUG 2021) MSCI EAFE MSCI World Year All Cap MSCI EAFE All Cap 300 MSCI EAFE All Cap 2020 8.67 7.82 15.97 2019 22.38 22.01 27.40 MSCI EAFE 262.28 MSCI World All Cap 2018 -14.50 -13.79 -9.52 2017 26.35 25.03 22.51 200 2016 1.29 1.00 8.24 2015 0.62 -0.81 -0.78 158.80 2014 -4.86 -4.90 4.44 149.91 2013 23.62 22.78 27.45 2012 17.56 17.32 16.03 100 2011 -12.62 -12.14 -6.13 2010 9.55 7.75 13.74 2009 33.47 31.78 31.83 2008 -43.83 -43.38 -40.97 0 Nov 07 Jan 09 Mar 10 May 11 Jun 12 Aug 13 Oct 14 Dec 15 Jan 17 Mar 18 May 19 Jul 20 Aug 21 INDEX PERFORMANCE — NET RETURNS (%) (AUG 31, 2021) FUNDAMENTALS (AUG 31, 2021) ANNUALIZED Since 1 Mo 3 Mo 1 Yr YTD 3 Yr 5 Yr 10 Yr Nov 30, 2007 Div Yld (%) P/E P/E Fwd P/BV MSCI EAFE All Cap 1.94 1.59 27.30 12.03 9.20 10.09 7.74 3.42 2.35 20.82 na 1.82 MSCI EAFE 1.76 1.38 26.12 11.58 9.00 9.72 7.34 2.99 2.43 20.10 15.76 1.93 MSCI World All Cap 2.48 5.30 31.25 17.81 14.48 14.65 12.10 7.26 1.64 24.91 na 3.04 INDEX RISK AND RETURN CHARACTERISTICS (AUG 31, 2021) ANNUALIZED STD DEV (%) 2 SHARPE RATIO 2 , 3 MAXIMUM DRAWDOWN Turnover Since 1 3 Yr 5 Yr 10 Yr 3 Yr 5 Yr 10 Yr Nov 30, (%) Period YYYY-MM-DD -

Ishares SMI®

For Professional Clients Only. iShares SMI® ETF (CH) CSSMI August Factsheet Performance, Portfolio Breakdowns and Net Assets information as at: 31-Aug- 2021 All other data as at 07-Sep-2021 Investors should read the Key Investor Information Document and Prospectus prior to investing. Capital at risk. All financial investments involve an element of risk. Therefore, the value The Fund seeks to track the performance of an index composed of the 20 largest Swiss companies. of your investment and the income from it will vary and your initial investment amount cannot Effective from 18 September 2017, the maximum weighting to any one stock is restricted to 18% on be guaranteed. a quarterly basis KEY FACTS Asset Class Equity KEY BENEFITS Fund Base Currency CHF Share Class Currency CHF Targeted exposure to the 20 largest Swiss companies 1 Fund Launch Date 06-Oct-1999 Direct investment into blue-chip companies representative of leaders in Switzerland Share Class Launch Date 06-Oct-1999 2 Benchmark Swiss Market Index (SMI®) 3 Single country and large market capitalisation companies exposure ISIN CH0008899764 Total Expense Ratio 0.35% Distribution Type Ad-Hoc Key Risks: Investment risk is concentrated in specific sectors, countries, currencies or companies. Domicile Switzerland This means the Fund is more sensitive to any localised economic, market, political or regulatory Methodology Replicated events. The value of equities and equity-related securities can be affected by daily stock market Product Structure Physical movements. Other influential factors include political, economic news, company earnings and Rebalance Frequency Quarterly significant corporate events. Counterparty Risk: The insolvency of any institutions providing UCITS No services such as safekeeping of assets or acting as counterparty to derivatives or other Use of Income Distributing instruments, may expose the Fund to financial loss. -

2017 Annual General Meeting Invitation, Proxy Statement and Annual Report

2017 Annual General Meeting Invitation, Proxy Statement and Annual Report TO OUR SHAREHOLDERS WE’VE COME A LONG WAY… So, we have come a long way. Which gives us an opportunity to put this company - now in its 35th year - When we meet people from outside Logitech, we often into a broader perspective as we look ahead. For both hear, “Wow, you really had a terrific year!”, or “What a of us, it’s an anniversary of sorts this year. Guerrino turnaround this past year or two!”. celebrates 20 years at Logitech in a few months and Bracken celebrates his first five. Let’s step back and think The truth is we started down this road five years ago. about the world in which we now play. After all, you’re That was Fiscal Year 2013, when retail sales in constant reading this because you’re interested in what’s ahead. currency fell -7% year on year. TOOLS ENHANCE OUR LIVES We made changes to our strategy, our culture and our team. And since then we’ve systematically and Let’s step way back to the dawn of humanity; even before Letter to Shareholders passionately worked toward our goal to become a design history was recorded. Our earliest tools were knives, company. A design company is not one focused on spears, the wheel, jugs and more. They enabled us to do fashion or beautiful products (although our products are things we couldn’t do on our own and became stepping beautiful). It’s a company that puts the consumer at the stones for new advances. -

Quarterly Market Review

Quarterly Market Review [Third Quarter 2018] www.rathbonewarwick.com Quarterly Market Review [Third Quarter 2018] This report features world capital market performance Overview: and a timeline of events for the past quarter. It begins with a global overview, then features the returns of stock and Market Summary bond asset classes in the US and international markets. World Stock Market Performance The report also illustrates the impact of globally diversified portfolios and features a quarterly topic. World Asset Classes US Stocks International Developed Stocks Emerging Markets Stocks Select Country Performance Select Currency Performance vs. US Dollar Real Estate Investment Trusts (REITs) Commodities Fixed Income Impact of Diversification Rathbone Warwick Investment Management (“RWIM”) is a Registered Investment Adviser. This document is solely for informational purposes. Advisory services are only offered to clients or prospective clients where RWIM and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RWIM unless a client service agreement is in place. www.rathbonewarwick.com Market Summary [Index Returns] Global International Emerging Global Bond US Stock Developed Markets Real US Bond Market Market Stocks Stocks Estate Market ex US Q3 2018 STOCKS BONDS 7.12% 1.31% -1.09% -0.03% 0.02% -0.17% Since Jan. 2001 Avg. Quarterly Return 2.0% 1.5% 2.9% 2.6% 1.1% 1.1% Best 16.8% 25.9% 34.7% 32.3% 4.6% 4.6% Quarter 2009 Q2 2009 Q2 2009 Q2 2009 Q3 2001 Q3 2008 Q4 Worst -22.8% -21.2% -27.6% -36.1% -3.0% -2.7% Quarter 2008 Q4 2008 Q4 2008 Q4 2008 Q4 2016 Q4 2015 Q2 Past performance is not a guarantee of future results. -

The Case for a Global Perspective

Schwab Center for Financial Research The case for a global perspective Jeffrey Kleintop, CFA Chief Global Investment Strategist What the Masters can teach us about investing Global stocks have tended to provide returns similar to those of U.S. stocks over long-term periods in the Markets have become more globally diversified of late, forcing investors to adopt a past. Valuations point to similar 5—10% annualized broader, worldwide perspective. This is a theme relevant even in championship golf, total returns across the world’s major regions in the where the national diversity of players in the 2015 Masters tournament bears an uncanny future (page 10). resemblance to stocks in the MSCI All Country World Index. Just as top players can be found on the world’s golf courses, savvy investors can be found on the world’s stock exchanges. But the lessons don’t stop there. 5–10% Geographic distribution of players at the Masters Annualized and stocks in the MSCI All Country World Index total returns Masters players MSCI AC World Index 50% U.S. 51% 16% Europe* 16% Avoiding the traps During the worst 10-year period for 13% Emerging Markets 14% stocks over the past 45 years, U.S. stocks fell an annualized 4.2%, 1.0% 12% U.K. 7% while global stocks lost 2.5% and International international stocks measured by 7% Asia Pacific 9% the MSCI EAFE Index lost only 2.5% 1.0% (page 6). Global 2% Canada 3% 4.2% * Excluding the U.K. Source: Charles Schwab, MSCI data as of April 10, 2015. -

Why Switzerland?

Why Switzerland? Marwan Naja, AS Investment Management January, 2010 I. Executive Summary Swiss Equities Have Outperformed: Here is a fact you probably did not know: The Swiss equity market has arguably been the best performing developed world market over the past 20, 10, 5 and 2 years. The SPI Index, which incorporates over 200 Swiss stocks, is the best performing index in Swiss Franc (“CHF”), US Dollars (“USD”), Euro (“EUR”) and British Pounds (“GBP”) over the past 20 years1,10 years, 5 years, and 2 years when compared to similar broad-based total return indices in the United States (S&P 500 Total Return), the United Kingdom (FTSE 350 Total Return), Germany (CDAX), France (SBF 120 Total Return) and Japan (TOPIX Total Return)2. For most of these periods the magnitude of the outperformance is significant. Furthermore, the Swiss market has exhibited attractive risk characteristics including lower volatility than comparable markets. Figure 1: SPI 20 Year Performance (red) Compared to Major Developed Indices in CHF3 1 The 20 year comparable excludes the EUR which has not existed for that duration and the French SBF 120 TR which was established in 1990 and has underperformed the SPI over the 19 year period. 2 The Swiss market is the best performer in our local currency comparison (stripping out the foreign exchange effects) over 20 years and marginally trails the FTSE 350 for the 10 year, 5 year and 2 year comparisons. 3 Source of all graphs is Bloomberg unless otherwise indicated. Why Switzerland? AS Investment Management Contents I. Executive Summary ............................................................................................................ 1 Swiss Equities Have Outperformed ................................................................................... -

MSCI ACWI Ex Ireland Index (USD)

MSCI ACWI ex Ireland Index (USD) The MSCI ACWI ex Ireland Index captures large and mid cap representation across 22 of 23 Developed Markets (DM) countries (excluding Ireland) and 27 Emerging Markets (EM) countries*. With 2,959 constituents, the index covers approximately 85% of the global equity opportunity set outside Ireland. CUMULATIVE INDEX PERFORMANCE — GROSS RETURNS (USD) ANNUAL PERFORMANCE (%) (AUG 2006 – AUG 2021) MSCI ACWI Year ex Ireland MSCI World MSCI ACWI MSCI ACWI ex Ireland 2020 16.83 16.50 16.82 MSCI World 338.06 2019 27.28 28.40 27.30 MSCI ACWI 325.46 2018 -8.90 -8.20 -8.93 300 324.55 2017 24.63 23.07 24.62 2016 8.51 8.15 8.48 2015 -1.86 -0.32 -1.84 2014 4.71 5.50 4.71 200 2013 23.42 27.37 23.44 2012 16.81 16.54 16.80 2011 -6.88 -5.02 -6.86 2010 13.25 12.34 13.21 100 2009 35.44 30.79 35.41 2008 -41.76 -40.33 -41.85 50 2007 12.31 9.57 12.18 Aug 06 Nov 07 Feb 09 May 10 Aug 11 Nov 12 Feb 14 May 15 Aug 16 Nov 17 Feb 19 May 20 Aug 21 INDEX PERFORMANCE — GROSS RETURNS (%) (AUG 31, 2021) FUNDAMENTALS (AUG 31, 2021) ANNUALIZED Since 1 Mo 3 Mo 1 Yr YTD 3 Yr 5 Yr 10 Yr Dec 31, 1998 Div Yld (%) P/E P/E Fwd P/BV MSCI ACWI ex Ireland 2.53 4.66 29.18 16.24 14.91 14.88 11.86 6.98 1.71 22.52 18.45 3.07 MSCI World 2.52 5.97 30.33 18.29 15.56 15.44 12.76 6.98 1.66 23.87 19.54 3.31 MSCI ACWI 2.53 4.67 29.18 16.24 14.91 14.88 11.86 6.97 1.71 22.54 18.46 3.07 INDEX RISK AND RETURN CHARACTERISTICS (AUG 31, 2021) ANNUALIZED STD DEV (%) 2 SHARPE RATIO 2 , 3 MAXIMUM DRAWDOWN Turnover Since 1 3 Yr 5 Yr 10 Yr 3 Yr 5 Yr 10 Yr Dec 31, (%) Period YYYY-MM-DD -

Aktienmarkt Schweiz Lukrative Klettertour Zu Neuen Kursgipfeln

all about investment products #8 August 2017 14. Jahrgang CHF 12.50 www.payoff.ch AKTIENMARKT SCHWEIZ LUKRATIVE KLETTERTOUR ZU NEUEN KURSGIPFELN Interview Marc Possa, Geschäftsführer & Partner bei [vv] vermögensverwaltung ag Seite 10 Learning Curve VSTOXX: Der Puls der europäischen Aktienmärkte Seite 15 IN EINER WELT IM WANDEL KÖNNEN KLEINE EINSÄTZE GROSSE WIRKUNG ZEIGEN MINI-FUTURE ZERTIFIKATE Mit Mini-Future Zerti katen lassen sich kurzfristige Markttrends bereits mit geringem Einsatz ausnutzen, und das sowohl bei steigenden als auch fallenden Kursen. Zudem bieten Mini-Future Zerti kate eine einfache und kostengünstige Möglichkeit, ein beste- hendes Portfolio gegen sinkende Kurse abzusichern. www.bnpparibasmarkets.ch Mitglied bei: [email protected] +41 (0)58 212 68 50 Wir machen Sie darauf aufmerksam, dass die Gespräche auf der angegebenen Telefonnummer aufgezeichnet werden. Bei Ihrem Anruf erklären Sie sich mit dieser Geschäftspraxis einverstanden. Risikohinweis: Dieses Werbeinserat stellt keinen vereinfachten Prospekt im Sinne von Art. 5 des Bundesgesetzes über die kollektiven Kapitalanlagen oder Emissionsprospekt im Sinne der Art. 652a und 1156 des Schweizerischen Obligationenrechts dar. Es handelt sich zudem weder um eine Aufforderung, noch um eine Empfehlung zum Kauf. Die in diesem Werbeinserat beschriebenen Produkte werden von BNP ParibasIssuance B.V. ausgegeben und sind derivative Finanzinstrumente. Der alleinverbindliche Prospekt in englischer Sprache kann direkt bei BNP Paribas Securities Services, Paris, Zweigniederlassung Zürich, Selnaustrasse 16, Postfach, 8022 Zürich, oder unter der Tel. +41 58 212 63 35 bezogen werden. Die Produkte qualifi zieren nicht als Anteile einer kollektiven Kapitalanlage im Sinne des Bundesgesetzes über die kollektiven Kapitalanlagen und sind daher auch nicht der Aufsicht der Eidgenössischen Finanzmarktaufsicht (FINMA) unterstellt. -

Swiss Leader Index Price Index Index

BLUE-CHIP INDICES 1 SWISS LEADER INDEX PRICE INDEX INDEX Index description Key facts The SLI Swiss Leader Index includes the 30 most liquid stocks traded in the » "In order to achieve the stated index objective SIX Swiss Ex-change defines Swiss equity market, the developments of which are reflected by the SPI® the general principles that govern the index methodology. SIX Swiss Family. Consequently, the index weighting of a given issue is limited by Exchange publishes the index objective and rules for all indices. means of a 9/4,5 capping model. In other words, the weighting of each of the four companies with the largest market capitalisation is capped at a » Representative: the development of the market is represented by the maximum of 9 %. The weightings of all lower-ranked companies are if index necessary capped at 4.5 %. This limitation will be calculated by applying a » Tradable: the index components are tradable in terms of company size capping factor, which as a general rule will remain constant for a three- and market month period. The SLI offers a number of advantages: for investors, the capping feature improves their stock- and sector specific diversification and, » Replicable: the development of the index can be replicated in practise with because the new index fulfils Swiss, EU and US regulatory requirements, a portfolio new markets can be opened with products based on the SLI. That, in turn, generates liquidity for the stocks included in the basket. » Stable: high index continuity » Rules-based: index changes and calculations -

Appendix D to Tradition SEF Rulebook Equities Product Listing

Appendix D to Tradition SEF Rulebook Equities Product Listing Broad-Market Equity Index Swap Product Listing Tradition SEF, Inc. I. Discussion of contracts; not readily susceptible to manipulation • Index Selection: Tradition SEF limits the indexes underlying its equity index swap offerings to well-established, publicly available third-party equity index market benchmarks. Tradition SEF believes that the size and liquidity of the cash market that underlies these indexes creates in each case a deliverable supply of underlying securities and volume of trading that would not make them easily susceptible to manipulation. Furthermore, Tradition SEF believes that the large number of participants in each market, and the calculation of each index being based on actual transaction data from major stock markets further limit the susceptibility of manipulation of these indexes. The broad-based equity indexes underlying swaps on Tradition SEF are the timeliest, recognized and reliable benchmarks for equity prices in their respective markets. The index levels are readily available and commercially acceptable as benchmarks for investors, portfolio managers and public policy makers. Tradition SEF believes that such benchmark indexes, which also underlie liquid index futures contracts on major Designated Contract Markets, and equity index exchange traded funds on stock exchanges, due to the large number of index members, ubiquity, and broad-market nature are not readily susceptible to manipulation. Furthermore, the associated index futures contracts and exchange traded funds offer a deep liquidity pool to hedge and risk-manage swaps based on such indexes’ index. Swap Contract Specifications: A discussion of Variance and Volatility Swaps: Equity Index Variance and volatility swaps pay out on the degree of stock price fluctuation, not the absolute level or direction of the underlying index.