The Case for a Global Perspective

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

North Carolina Supplemental Retirement Plans Investment Performance March 31, 2015

North Carolina Supplemental Retirement Plans Investment Performance March 31, 2015 Services provided by Mercer Investment Consulting, Inc. Table of Contents Table of Contents 1. Capital Markets Commentary 2. Executive Summary 3. Total Plan 4. US Equity 5. International Equity 6. Global Equity 7. Inflation Responsive 8. US Fixed Income 9. Stable Value 10. GoalMaker Portfolios 11. Disclaimer Capital Markets Commentary Performance Summary: Quarter in Review Market Performance Market Performance First Quarter 2015 1 Year DOMESTIC EQUITY DOMESTIC EQUITY Russell 3000 1.8 Russell 3000 12.4 S&P 500 1.0 S&P 500 12.7 Russell 1000 1.6 Russell 1000 12.7 Russell 1000 Growth 3.8 Russell 1000 Growth 16.1 Russell 1000 Value -0.7 Russell 1000 Value 9.3 Russell Midcap 4.0 Russell Midcap 13.7 Russell 2000 4.3 Russell 2000 8.2 Russell 2000 Growth 6.6 Russell 2000 Growth 12.1 Russell 2000 Value 2.0 Russell 2000 Value 4.4 INTERNATIONAL EQUITY INTERNATIONAL EQUITY MSCI ACWI 2.3 MSCI ACWI 5.4 MSCI ACWI Small Cap 4.4 MSCI ACWI Small Cap 3.2 MSCI AC World ex US 3.5 MSCI AC World ex US -1.0 MSCI EAFE 4.9 MSCI EAFE -0.9 MSCI EAFE Small Cap 5.6 MSCI EAFE Small Cap -2.9 MSCI EM 2.2 MSCI EM 0.4 FIXED INCOME FIXED INCOME Barclays T-Bill 1-3 months 0.0 Barclays T-Bill 1-3 months 0.0 Barclays Aggregate 1.6 Barclays Aggregate 5.7 Barclays TIPS 5-10 yrs 1.4 Barclays TIPS 5-10 yrs 2.9 Barclays Treasury 1.6 Barclays Treasury 5.4 Barclays Credit 2.2 Barclays Credit 6.7 Barclays High Yield 2.5 Barclays High Yield 2.0 Citi WGBI -2.5 Citi WGBI -5.5 JP GBI-EM Global Div. -

Does International Diversification Pay?

Does International Diversification Pay? Vivek Bhargava1, Daniel K. Konku2, and D. K. Malhotra3 Advances in computer and telecommunications technology have contributed to the emergence of more integrated global financial markets, allowing for the dissemination of information and the execution of transactions on a real-time basis around the clock and around the globe. To determine if an investor can gain additional diversification benefits by investing in today’s increasingly integrated global financial markets, returns on four different indexes—Standard & Poor’s Composite 500 (S&P 500); Morgan Stanley Capital International (MSCI) World Index; Europe, Australia, and Far East (EAFE) Index; and the MSCI Europe Index—are analyzed for a 22-year period, from 1978 to 2000. Although the benefits from international diversification are decreasing, an investor is better off investing a portion of his or her portfolio in international markets, especially the European markets. Keywords: Diversification, Mutual fund selection, Risk reduction Introduction The objective of this paper is to determine whether an Globalization of financial markets is one of the most investor today can still gain diversification benefits significant economic developments over the last by investing in international markets. The monthly decade. Advances in computer and returns of four different indexes--Standard & Poor’s telecommunications technology contributed to the 500 (S&P 500); Morgan Stanley Capital International emergence of global financial markets, permitting the (MSCI) World Index; the Europe, Australia and Far dissemination of information and execution of East (EAFE) Index; and the MSCI Europe Index— transactions on a real-time basis around the clock and are analyzed over a 22-year period, from 1978 to around the globe. -

MSCI EAFE All Cap Index (USD)

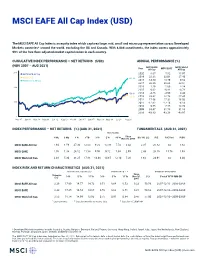

MSCI EAFE All Cap Index (USD) The MSCI EAFE All Cap Index is an equity index which captures large, mid, small and micro cap representation across Developed Markets countries* around the world, excluding the US and Canada. With 8,088 constituents, the index covers approximately 99% of the free float-adjusted market capitalization in each country. CUMULATIVE INDEX PERFORMANCE — NET RETURNS (USD) ANNUAL PERFORMANCE (%) (NOV 2007 – AUG 2021) MSCI EAFE MSCI World Year All Cap MSCI EAFE All Cap 300 MSCI EAFE All Cap 2020 8.67 7.82 15.97 2019 22.38 22.01 27.40 MSCI EAFE 262.28 MSCI World All Cap 2018 -14.50 -13.79 -9.52 2017 26.35 25.03 22.51 200 2016 1.29 1.00 8.24 2015 0.62 -0.81 -0.78 158.80 2014 -4.86 -4.90 4.44 149.91 2013 23.62 22.78 27.45 2012 17.56 17.32 16.03 100 2011 -12.62 -12.14 -6.13 2010 9.55 7.75 13.74 2009 33.47 31.78 31.83 2008 -43.83 -43.38 -40.97 0 Nov 07 Jan 09 Mar 10 May 11 Jun 12 Aug 13 Oct 14 Dec 15 Jan 17 Mar 18 May 19 Jul 20 Aug 21 INDEX PERFORMANCE — NET RETURNS (%) (AUG 31, 2021) FUNDAMENTALS (AUG 31, 2021) ANNUALIZED Since 1 Mo 3 Mo 1 Yr YTD 3 Yr 5 Yr 10 Yr Nov 30, 2007 Div Yld (%) P/E P/E Fwd P/BV MSCI EAFE All Cap 1.94 1.59 27.30 12.03 9.20 10.09 7.74 3.42 2.35 20.82 na 1.82 MSCI EAFE 1.76 1.38 26.12 11.58 9.00 9.72 7.34 2.99 2.43 20.10 15.76 1.93 MSCI World All Cap 2.48 5.30 31.25 17.81 14.48 14.65 12.10 7.26 1.64 24.91 na 3.04 INDEX RISK AND RETURN CHARACTERISTICS (AUG 31, 2021) ANNUALIZED STD DEV (%) 2 SHARPE RATIO 2 , 3 MAXIMUM DRAWDOWN Turnover Since 1 3 Yr 5 Yr 10 Yr 3 Yr 5 Yr 10 Yr Nov 30, (%) Period YYYY-MM-DD -

CNBC.Com Financial-Decoupling.Html

CNBC.com https://www.cnbc.com/2020/12/16/msci-deletes-chinese-stocks-in-sign-of-us-china- financial-decoupling.html CHINA MARKETS Stock index giant MSCI to remove some Chinese stocks under U.S. pressure PUBLISHED WED, DEC 16 202012:31 AM ESTUPDATED WED, DEC 16 20202:16 AM EST Evelyn Cheng @CHENGEVELYN KEY POINTS • MSCI, one of the largest stock index companies in the world, announced Tuesday that it would remove 10 Chinese securities from its indexes. • The announcement follows similar moves by S&P Dow Jones Indices, FTSE Russell and U.S.-based trading app Robinhood to limit customers’ exposure to the affected Chinese stocks. • MSCI plans to launch versions of the indexes that keep the deleted names. BEIJING — Global investors are turning cautious on investing in some Chinese companies named in a U.S. government executive order. MSCI, one of the largest stock index companies in the world, announced Tuesday that it would remove 10 Chinese securities from its indexes effective at the close of businesses on Jan. 5, 2021. The removals follow U.S. President Donald Trump’s order on Nov. 12 that bans American companies and individuals from owning shares of Chinese companies that the White House alleges supports China’s military. “This itself is not economically earthshaking, but it is something that makes you take note because it was pretty quick how all this happened,” said James Early, CEO of investment research firm Stansberry China. “It’s not MSCI. It’s market participants driving this. ... They’re doing this because the market is telling them they have to.” MSCI said in a release its decision was based on responses from more than 100 market participants worldwide, who noted the “extensive presence” of U.S. -

FM First China Fund, LLC

FM First China Fund, LLC JANUARY 2020 INVESTMENT OBJECTIVE FM First China Fund, LLC (the "Fund") invests in publicly-traded companies that either derive a majority of their revenues from, or maintain a majority of their assets in, mainland China. The investment objective of the Fund is to achieve long-term capital appreciation using a value-oriented approach modeled after the investment style of New York-based First Manhattan Co. The local team, with a deep network in China, seeks to apply a time-tested Western value approach to investing in what they view as an inefficient Eastern market. We manage a relatively concentrated portfolio where, based on the average of quarter end holdings since inception, the Fund’s top ten holdings have represented more than 60% of its assets under management. PERFORMANCE & FUND STATISTICS The tables below set forth performance and other information for the Fund (after fees and expenses) as of 12/31/2019.1,2,3 FM First MSCI China Hang Seng Fund vs. MSCI Period-End AUM Year China Fund Index Index China Index ($ million)4 2019 4 1 . 7 % 23.5% 13.0% +18.2 317 2018 ( 1 2 . 2 % ) (18.9%) (10.5%) +6.7 230 2017 4 7 . 8 % 54.1% 41.3% (6.3) 248 2016 ( 1 3 . 4 % ) 0.9% 4.3% (14.3) 173 2015 9 . 6 % (7.8%) (3.9%) +17.4 211 2014 2 . 5 % 8.0% 5.5% (5.5) 191 2013 2 1 . 3 % 3.6% 6.6% +17.7 146 2012 3 4 . 8 % 22.7% 27.5% +12.1 44 2011 ( 1 1 . -

CNBC Model ETF Retirement Portfolios Investment Strategy As of July 25Th, 2013 (Previous Portfolio Strategies Begin on Pg

CNBC Model ETF Retirement Portfolios Investment Strategy as of July 25th, 2013 (previous portfolio strategies begin on pg. 4) Purple = Changes as of July, 25, 2013 7/25/2013 CNBC ETF Retirement CNBC ETF Retirement CNBC ETF Retirement Asset Class Type ETF Ticker Portfolio 30 Portfolio 50 Portfolio 70 Cash Cash/Cash Equivalent Core Guggenheim Enhanced Short Duration Bond ETF GSY 0 SELL 7.5 Equity US Equity Core SPDR S&P 500 SPY 17.5 12.5 5 US Equity Overweight Schwab U.S. Dividend Equity SCHD 7.5 5 5 US Equity Overweight Vanguard MidCap VO 5 5 5 US Equity Overweight Technology Select Sector SPDR XLK 5 5 2.5 ACWI exUS Equity Core db Xtrackers MSCI EAFE Hedged Eq DBEF 17.5 12.5 5 ACWI exUS Equity Overweight WisdomTree Japan Hedged Equity DXJ 5 5 2.5 ACWI exUS Equity Overweight iShares MSCI Europe Financials EUFN 5 5 2.5 ACWI exUS Equity Overweight EGShares Emerging Markets Consumer ECON 7.5 5 2.5 ACWI exUS Equity Overweight PowerShares S&P International Low Volatility IDLV 5 5 5 Bonds US Bonds Core iShares Core Total US Bond Market ETF AGG 2.5 10 25 US Bonds Overweight iShares iBoxx $ Invest Grade Corp Bond LQD 5 5 Global Bonds Overweight WisdomTree Emerging Markets Local Debt ELD 2.5 5 7.5 Opportunity Opportunity PowerShares Senior Loan Portfolio BKLN 5 5 5 Opportunity Market Vectors Gold Miners GDX 0 0 0 Opportunity Vanguard Global exUS Real Estate VNQI 5 5 5 Opportunity Peritus High Yield ETF HYLD 5 5 5 Opportunity PowerShares DB US Dollar Index Bullish UUP SELL SELL SELL Opportunity Surplus iShares Barclays 13 Year Credit Bond CSJ 5 5 5 Totals 100 100 100 ETF Selections GSY: Guggenheim Enhanced Short Duration Bond ETF An alternative to cash that offers an enhanced yield and a relatively reasonable expense ratio. -

Quarterly Market Review

Quarterly Market Review [Third Quarter 2018] www.rathbonewarwick.com Quarterly Market Review [Third Quarter 2018] This report features world capital market performance Overview: and a timeline of events for the past quarter. It begins with a global overview, then features the returns of stock and Market Summary bond asset classes in the US and international markets. World Stock Market Performance The report also illustrates the impact of globally diversified portfolios and features a quarterly topic. World Asset Classes US Stocks International Developed Stocks Emerging Markets Stocks Select Country Performance Select Currency Performance vs. US Dollar Real Estate Investment Trusts (REITs) Commodities Fixed Income Impact of Diversification Rathbone Warwick Investment Management (“RWIM”) is a Registered Investment Adviser. This document is solely for informational purposes. Advisory services are only offered to clients or prospective clients where RWIM and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RWIM unless a client service agreement is in place. www.rathbonewarwick.com Market Summary [Index Returns] Global International Emerging Global Bond US Stock Developed Markets Real US Bond Market Market Stocks Stocks Estate Market ex US Q3 2018 STOCKS BONDS 7.12% 1.31% -1.09% -0.03% 0.02% -0.17% Since Jan. 2001 Avg. Quarterly Return 2.0% 1.5% 2.9% 2.6% 1.1% 1.1% Best 16.8% 25.9% 34.7% 32.3% 4.6% 4.6% Quarter 2009 Q2 2009 Q2 2009 Q2 2009 Q3 2001 Q3 2008 Q4 Worst -22.8% -21.2% -27.6% -36.1% -3.0% -2.7% Quarter 2008 Q4 2008 Q4 2008 Q4 2008 Q4 2016 Q4 2015 Q2 Past performance is not a guarantee of future results. -

Notice of Filing of Proposed Rule Change to List and Trade Options on the MSCI EAFE Index and on the MSCI Emerging Markets Index

SECURITIES AND EXCHANGE COMMISSION (Release No. 34-74430; File No. SR-CBOE-2015-023) March 4, 2015 Self-Regulatory Organizations; Chicago Board Options Exchange, Incorporated; Notice of Filing of Proposed Rule Change to List and Trade Options on the MSCI EAFE Index and on the MSCI Emerging Markets Index Pursuant to Section 19(b)(1) of the Securities Exchange Act of 1934 (the “Act” or “Exchange Act”),1 and Rule 19b-4 thereunder,2 notice is hereby given that on February 26, 2015, the Chicago Board Options Exchange, Incorporated (the “Exchange” or “CBOE”) filed with the Securities and Exchange Commission (the “Commission”) the proposed rule change as described in Items I, II, and III below, which Items have been prepared by the Exchange. The Commission is publishing this notice to solicit comments on the proposed rule change from interested persons. I. Self-Regulatory Organization’s Statement of the Terms of Substance of the Proposed Rule Change CBOE proposes to list and trade options that overlie the MSCI EAFE Index and the MSCI Emerging Markets Index (“EAFE options” and “EM options”). EAFE and EM options would be P.M., cash-settled contracts with European-style exercise. The text of the proposed rule change is available on the Exchange’s Web site (http://www.cboe.com/AboutCBOE/CBOELegal RegulatoryHome.aspx), at the Exchange’s Office of the Secretary, and at the Commission. II. Self-Regulatory Organization’s Statement of the Purpose of, and Statutory Basis for, the Proposed Rule Change In its filing with the Commission, the self-regulatory organization included statements concerning the purpose of and basis for the proposed rule change and discussed any comments it 1 15 U.S.C. -

MSCI ACWI Ex Ireland Index (USD)

MSCI ACWI ex Ireland Index (USD) The MSCI ACWI ex Ireland Index captures large and mid cap representation across 22 of 23 Developed Markets (DM) countries (excluding Ireland) and 27 Emerging Markets (EM) countries*. With 2,959 constituents, the index covers approximately 85% of the global equity opportunity set outside Ireland. CUMULATIVE INDEX PERFORMANCE — GROSS RETURNS (USD) ANNUAL PERFORMANCE (%) (AUG 2006 – AUG 2021) MSCI ACWI Year ex Ireland MSCI World MSCI ACWI MSCI ACWI ex Ireland 2020 16.83 16.50 16.82 MSCI World 338.06 2019 27.28 28.40 27.30 MSCI ACWI 325.46 2018 -8.90 -8.20 -8.93 300 324.55 2017 24.63 23.07 24.62 2016 8.51 8.15 8.48 2015 -1.86 -0.32 -1.84 2014 4.71 5.50 4.71 200 2013 23.42 27.37 23.44 2012 16.81 16.54 16.80 2011 -6.88 -5.02 -6.86 2010 13.25 12.34 13.21 100 2009 35.44 30.79 35.41 2008 -41.76 -40.33 -41.85 50 2007 12.31 9.57 12.18 Aug 06 Nov 07 Feb 09 May 10 Aug 11 Nov 12 Feb 14 May 15 Aug 16 Nov 17 Feb 19 May 20 Aug 21 INDEX PERFORMANCE — GROSS RETURNS (%) (AUG 31, 2021) FUNDAMENTALS (AUG 31, 2021) ANNUALIZED Since 1 Mo 3 Mo 1 Yr YTD 3 Yr 5 Yr 10 Yr Dec 31, 1998 Div Yld (%) P/E P/E Fwd P/BV MSCI ACWI ex Ireland 2.53 4.66 29.18 16.24 14.91 14.88 11.86 6.98 1.71 22.52 18.45 3.07 MSCI World 2.52 5.97 30.33 18.29 15.56 15.44 12.76 6.98 1.66 23.87 19.54 3.31 MSCI ACWI 2.53 4.67 29.18 16.24 14.91 14.88 11.86 6.97 1.71 22.54 18.46 3.07 INDEX RISK AND RETURN CHARACTERISTICS (AUG 31, 2021) ANNUALIZED STD DEV (%) 2 SHARPE RATIO 2 , 3 MAXIMUM DRAWDOWN Turnover Since 1 3 Yr 5 Yr 10 Yr 3 Yr 5 Yr 10 Yr Dec 31, (%) Period YYYY-MM-DD -

Msci Index Futures

MSCI INDEX FUTURES October 2020 MSCI Index Futures: Strong Growth 2020 highlights & records • 2020 ADV • MSCI EM futures | 191K, up 19% YoY • MSCI EAFE futures | 60K, up 42% YoY • MSCI complex | 254K, up 24% YoY • Daily volume highlights • Mar 16 - MSCI EM futures | 1.234M lots • Jun 15 - MSCI EAFE futures | 446K lots • Jun 15 - MSCI futures complex | 1.659M lots • OI Record • Mar 17 - MSCI futures complex | 2,458K New MSCI ESG Futures • MSCI EAFE ESG Leaders, MSCI EM ESG Leaders, MSCI Europe ESG Leaders, MSCI World ESG Leaders, MSCI USA ESG Leaders, MSCI Climate Change, MSCI Japan ESG Selected ESG Leaders Growth drivers • Established market quality • Efficient quarterly roll markets • Steadily growing participation from a diverse and global institutional clientele • Useful innovations like Block Trading at Index Close (BIC) • Continued expansion of product set providing greater hedging and trading opportunities INTERCONTINENTAL EXCHANGE 2 Open Interest in the contracts still growing... INTERCONTINENTAL EXCHANGE 3 … alongside solid volume growth • 2020 ADV in MSCI Emerging Markets futures | 191K, +19% YoY • 2020 ADV in MSCI EAFE futures | 60K, +42% YoY 2020 Notional ADV: EM = $10.3bn 2020 Notional ADV: EAFE = $5.6bn INTERCONTINENTAL EXCHANGE 4 Liquidity is improving relative to ETFs • Emerging markets-based ETFs used to trade almost 13x relative to futures, but now trade less than 1x as much • EAFE-based ETFs currently trade less than 1x as much relative to futures The picture can't be displayed. INTERCONTINENTAL EXCHANGE 5 September 2020 Roll VWAP • During the September 2020 roll, 333K • During the September 2020 roll, 1.46M explicit spreads traded in the MSCI EAFE explicit spreads traded in the MSCI futures Emerging Markets futures • The MSCI EAFE futures had an explicit • The MSCI Emerging Markets futures had an spread VWAP of -6.39 explicit spread VWAP of -1.96 The picture can't be displayed. -

Megatrends – Ishares Thematic Etfs Steven Lu, CFA, Blackrock Ishares APAC Distribution

Megatrends – iShares Thematic ETFs Steven Lu, CFA, BlackRock iShares APAC Distribution April 2018 FOR PROFESSIONAL AND INSTITUTIONAL INVESTORS USE ONLY EII0418A-477607-1503167 NOT FOR PUBLIC DISTRIBUTION (PLEASE READ IMPORTANT DISCLOSURES) What is the greatest insecurity of our age? Saving ENOUGH for retirement FOR PROFESSIONAL AND INSTITUTIONAL INVESTORS USE ONLY EII0418A-477607-1503167 NOT FOR PUBLIC DISTRIBUTION (PLEASE READ IMPORTANT DISCLOSURES) 2 What are Thematic Investments? EII0418A-477607-1503167 Five major megatrends shaping the globe Shifting Climate change, Demographics Technological Rapid economic resource and social breakthrough urbanisation power scarcity change The growing strength An expanding global Increasing age and size A technological According to the UN, of emerging population is of the global population revolution is having a by 2030 two thirds of economies is increasing the demand is fundamentally profound impact on the world’s population changing the balance for food and water and changing the needs of the global economy. will reside in cities.* of the global economy. putting pressure on its inhabitants. finite resources. FIVE MAJOR MEGATRENDS *Source: BlackRock, United Nations World Population Prospects: The 2015 Revision; as of July 2015. FOR PROFESSIONAL AND INSTITUTIONAL INVESTORS USE ONLY EII0418A-477607-1503167 NOT FOR PUBLIC DISTRIBUTION (PLEASE READ IMPORTANT DISCLOSURES) 4 Megatrends and how you can benefit Investment concept Shifting Thematic economic power indices iShares ETFs Climate change, resource -

Foreign Equityequity

ForeignForeign EquityEquity • All ETFs providers are placed in alphabetical order. • Click logo to buy ETF through EasyEquities website. • Risk profile included. • Research from Intellidex is included for most ETFs available on the EasyEquities site. • Provider logos click through to ETFs information on provider’s home page. • Providers Fact sheets are included. • The Total Expense Ratios (TERs) for each ETF is shown (as at March 2018). - Total Expense Ratios (TERs) Measure the costs of operating the ETF portfolios, including the management fees and costs of the issuing company. The TER is included in price of the ETF product and is not paid directly by the investor. The Ashburton Global 1200 ETF provides investors with efficient exposure RISK to the global equity market by tracking the S&P Global 1200. Ashburton Global 1200 ETF houses various global indices under one fund. Ashburton ETF Global 1200 ETF combines seven indices: the S&P 500 (US); S&P Europe Aggressive Global 1200 350; S&P TOPIX 150 (Japan); S&P/TSX 60 (Canada); S&P/ASX All Australian 50; S&P Asia 50; and S&P Latin America 40 FACT SHEET TER: 0,45% The Cloud Atlas Big50 ex-SA ETF is an investment product that invests in RISK the 50 most representative companies across the African continent. The 50 companies in this ETF track the Cloud Atlas AMI Big50 ex-SA index (beta+), which is an enhanced index designed to maximize sector and Moderate ETF country exposure Big 50 FACT SHEET TER: 0,75% The CoreShares S&P 500 ETF tracks the S&P 500® Index.