2019 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

I- THIRD SUPPLEMENT DATED 5 MAY 2021 to the BASE

THIRD SUPPLEMENT DATED 5 MAY 2021 TO THE BASE PROSPECTUS DATED 5 AUGUST 2020 UNIBAIL-RODAMCO-WESTFIELD SE (incorporated in the Republic of France as a European public company with limited liability) RODAMCO SVERIGE AB (incorporated in the Kingdom of Sweden as a public company with limited liability) (each as Issuers) EURO 20,000,000,000 Guaranteed Euro Medium Term Note Programme guaranteed in each case by UNIBAIL-RODAMCO-WESTFIELD SE UNIBAIL-RODAMCO-WESTFIELD N.V. (other than in the case of Notes issued by itself) (FORMERLY WFD UNIBAIL-RODAMCO N.V.) (incorporated in The Netherlands as a public company with limited liability) URW AMERICA INC. WEA FINANCE LLC (incorporated in Delaware as a corporation with (formed in Delaware as a limited liability company) shareholders that have limited liability) WCL FINANCE PTY LIMITED WESTFIELD AMERICA TRUST (incorporated in Australia as a proprietary company (established in Australia as a unit trust and in respect of limited by shares) which Westfield America Management Limited is the trustee) WESTFIELD CORPORATION LIMITED WFD TRUST (incorporated in Australia as a public company limited (established in Australia as a unit trust and in respect of by shares) which Westfield America Management Limited is the trustee) WESTFIELD UK & EUROPE FINANCE PLC (incorporated in the United Kingdom as a public company with limited liability) (each as Guarantors) This third supplement (the "Third Supplement") is supplemental to, and should be read in conjunction with, the base prospectus dated 5 August 2020 which received approval no. 20-380 from the Autorité des marches financiers ("AMF") on 5 August 2020, the first supplement (the "First Supplement") dated 23 November 2020 which received approval no. -

2015 Annual Results 19 August 2015 Agenda

2015 Annual Results 19 August 2015 Agenda • Merger update and strategic focus Angus McNaughton • Financial results Richard Jamieson Angus McNaughton Richard Jamieson • Portfolio performance Chief Executive Officer CFO and EGM Investments Stuart Macrae • Development update Jonathan Timms • FY16 focus and guidance Stuart Macrae Jonathan Timms Angus McNaughton EGM Leasing EGM Development 2 Merger update and strategic focus Angus McNaughton Cranbourne Park, VIC Merger benefits on track with a strong platform for growth • Strategic focus remains unchanged • Operational cost synergies on track • Over 60% of operational cost savings1 already locked in • Merger financing savings achieved1 with over $100m lower cost • Weighted average cost of debt reduced to 4.2% • Integration is on program • Key operational teams finalised and team co-locations underway • Solid FY15 performance • Statutory net profit of $675.1m • Underlying earnings up 6.2%2 • Development pipeline increased to $3.1b and current projects on or ahead of plan The Myer Centre Brisbane, QLD 1. On a run-rate or annualised basis. 2. On an aggregate basis. 4 Strategic focus remains unchanged Retail real estate • We will own, manage and develop Australian retail assets across the spectrum • Portfolio composition will evolve as developments occur and asset recycling continues Operational excellence • High performance intensive asset management approach • Continuous improvement of systems and processes • Strongly committed to responsible investment and sustainability • Development of a fully -

Socially Conscious Australian Equity Holdings

Socially Conscious Australian Equity Holdings As at 30 June 2021 Country of Company domicile Weight COMMONWEALTH BANK OF AUSTRALIA AUSTRALIA 10.56% CSL LTD AUSTRALIA 8.46% AUST AND NZ BANKING GROUP AUSTRALIA 5.68% NATIONAL AUSTRALIA BANK LTD AUSTRALIA 5.32% WESTPAC BANKING CORP AUSTRALIA 5.08% TELSTRA CORP LTD AUSTRALIA 3.31% WOOLWORTHS GROUP LTD AUSTRALIA 2.93% FORTESCUE METALS GROUP LTD AUSTRALIA 2.80% TRANSURBAN GROUP AUSTRALIA 2.55% GOODMAN GROUP AUSTRALIA 2.34% WESFARMERS LTD AUSTRALIA 2.29% BRAMBLES LTD AUSTRALIA 1.85% COLES GROUP LTD AUSTRALIA 1.80% SUNCORP GROUP LTD AUSTRALIA 1.62% MACQUARIE GROUP LTD AUSTRALIA 1.54% JAMES HARDIE INDUSTRIES IRELAND 1.51% NEWCREST MINING LTD AUSTRALIA 1.45% SONIC HEALTHCARE LTD AUSTRALIA 1.44% MIRVAC GROUP AUSTRALIA 1.43% MAGELLAN FINANCIAL GROUP LTD AUSTRALIA 1.13% STOCKLAND AUSTRALIA 1.11% DEXUS AUSTRALIA 1.11% COMPUTERSHARE LTD AUSTRALIA 1.09% AMCOR PLC AUSTRALIA 1.02% ILUKA RESOURCES LTD AUSTRALIA 1.01% XERO LTD NEW ZEALAND 0.97% WISETECH GLOBAL LTD AUSTRALIA 0.92% SEEK LTD AUSTRALIA 0.88% SYDNEY AIRPORT AUSTRALIA 0.83% NINE ENTERTAINMENT CO HOLDINGS LIMITED AUSTRALIA 0.82% EAGERS AUTOMOTIVE LTD AUSTRALIA 0.82% RELIANCE WORLDWIDE CORP LTD UNITED STATES 0.80% SANDFIRE RESOURCES LTD AUSTRALIA 0.79% AFTERPAY LTD AUSTRALIA 0.79% CHARTER HALL GROUP AUSTRALIA 0.79% SCENTRE GROUP AUSTRALIA 0.79% ORORA LTD AUSTRALIA 0.75% ANSELL LTD AUSTRALIA 0.75% OZ MINERALS LTD AUSTRALIA 0.74% IGO LTD AUSTRALIA 0.71% GPT GROUP AUSTRALIA 0.69% Issued by Aware Super Pty Ltd (ABN 11 118 202 672, AFSL 293340) the trustee of Aware Super (ABN 53 226 460 365). -

Westpac Online Investment Loan Acceptable Securities List - Effective 3 September2021

Westpac Online Investment Loan Acceptable Securities List - Effective 3 September2021 ASX listed securities ASX Code Security Name LVR ASX Code Security Name LVR A2M The a2 Milk Company Limited 50% CIN Carlton Investments Limited 60% ABC Adelaide Brighton Limited 60% CIP Centuria Industrial REIT 50% ABP Abacus Property Group 60% CKF Collins Foods Limited 50% ADI APN Industria REIT 40% CL1 Class Limited 45% AEF Australian Ethical Investment Limited 40% CLW Charter Hall Long Wale Reit 60% AFG Australian Finance Group Limited 40% CMW Cromwell Group 60% AFI Australian Foundation Investment Co. Ltd 75% CNI Centuria Capital Group 50% AGG AngloGold Ashanti Limited 50% CNU Chorus Limited 60% AGL AGL Energy Limited 75% COF Centuria Office REIT 50% AIA Auckland International Airport Limited 60% COH Cochlear Limited 65% ALD Ampol Limited 70% COL Coles Group Limited 75% ALI Argo Global Listed Infrastructure Limited 60% CPU Computershare Limited 70% ALL Aristocrat Leisure Limited 60% CQE Charter Hall Education Trust 50% ALQ Als Limited 65% CQR Charter Hall Retail Reit 60% ALU Altium Limited 50% CSL CSL Limited 75% ALX Atlas Arteria 60% CSR CSR Limited 60% AMC Amcor Limited 75% CTD Corporate Travel Management Limited ** 40% AMH Amcil Limited 50% CUV Clinuvel Pharmaceuticals Limited 40% AMI Aurelia Metals Limited 35% CWN Crown Limited 60% AMP AMP Limited 60% CWNHB Crown Resorts Ltd Subordinated Notes II 60% AMPPA AMP Limited Cap Note Deferred Settlement 60% CWP Cedar Woods Properties Limited 45% AMPPB AMP Limited Capital Notes 2 60% CWY Cleanaway Waste -

Asx Clear – Acceptable Collateral List 28

et6 ASX CLEAR – ACCEPTABLE COLLATERAL LIST Effective from 20 September 2021 APPROVED SECURITIES AND COVER Subject to approval and on such conditions as ASX Clear may determine from time to time, the following may be provided in respect of margin: Cover provided in Instrument Approved Cover Valuation Haircut respect of Initial Margin Cash Cover AUD Cash N/A Additional Initial Margin Specific Cover N/A Cash S&P/ASX 200 Securities Tiered Initial Margin Equities ETFs Tiered Notes to the table . All securities in the table are classified as Unrestricted (accepted as general Collateral and specific cover); . Specific cover only securities are not included in the table. Any securities is acceptable as specific cover, with the exception of ASX securities as well as Participant issued or Parent/associated entity issued securities lodged against a House Account; . Haircut refers to the percentage discount applied to the market value of securities during collateral valuation. ASX Code Security Name Haircut A2M The A2 Milk Company Limited 30% AAA Betashares Australian High Interest Cash ETF 15% ABC Adelaide Brighton Ltd 30% ABP Abacus Property Group 30% AGL AGL Energy Limited 20% AIA Auckland International Airport Limited 30% ALD Ampol Limited 30% ALL Aristocrat Leisure Ltd 30% ALQ ALS Limited 30% ALU Altium Limited 30% ALX Atlas Arteria Limited 30% AMC Amcor Ltd 15% AMP AMP Ltd 20% ANN Ansell Ltd 30% ANZ Australia & New Zealand Banking Group Ltd 20% © 2021 ASX Limited ABN 98 008 624 691 1/7 ASX Code Security Name Haircut APA APA Group 15% APE AP -

2021 Annual Report Dexus Releases Its 2021 Annual Report, Which Will Be Mailed to Security Holders Who Have Elected to Receive a Hard Copy in Mid-September 2021

Dexus (ASX: DXS) ASX release 17 August 2021 2021 Annual Report Dexus releases its 2021 Annual Report, which will be mailed to Security holders who have elected to receive a hard copy in mid-September 2021. Authorised by the Board of Dexus Funds Management Limited For further information please contact: Investors Media Rowena Causley Louise Murray Senior Manager, Investor Relations Senior Manager, Corporate Communications +61 2 9017 1390 +61 2 9017 1446 +61 416 122 383 +61 403 260 754 [email protected] [email protected] About Dexus Dexus (ASX: DXS) is one of Australia’s leading fully integrated real estate groups, managing a high-quality Australian property portfolio valued at $42.5 billion. We believe that the strength and quality of our relationships will always be central to our success and are deeply committed to working with our customers to provide spaces that engage and inspire. We invest only in Australia, and directly own $17.5 billion of office, industrial and healthcare properties, and investments. We manage a further $25.0 billion of office, retail, industrial and healthcare properties for third party clients. The group’s $14.6 billion development pipeline provides the opportunity to grow both portfolios and enhance future returns. Sustainability is integrated across our business, and our sustainability approach is the lens we use to manage emerging ESG risks and opportunities for all our stakeholders. Dexus is a Top 50 entity by market capitalisation listed on the Australian Securities Exchange and is supported by more than 30,000 investors from 23 countries. With over 35 years of expertise in property investment, funds management, asset management and development, we have a proven track record in capital and risk management and delivering superior risk-adjusted returns for investors. -

Index Rebalance

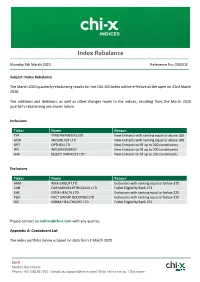

Index Rebalance Monday 9th March 2020 Reference No: 0002/20 Subject: Index Rebalance The March 2020 quarterly rebalancing results for the CXA 200 Index will be effective at the open on 23rd March 2020. The additions and deletions, as well as other changes made to the indices, resulting from the March 2020 quarterly rebalancing are shown below. Inclusions Ticker Name Reason TYR TYRO PAYMENTS LTD New Entrants with ranking equal or above 180 MSB MESOBLAST LTD New Entrants with ranking equal or above 180 OPT OPTHEA LTD New Entrants to fill up to 200 constituents IFN INFIGEN ENERGY New Entrants to fill up to 200 constituents SHV SELECT HARVESTS LTD New Entrants to fill up to 200 constituents Exclusions Ticker Name Reason AMA AMA GROUP LTD Exclusions with ranking equal or below 220 CVN CARNARVON PETROLEUM LTD Failed Eligibility Rank 273 EHE ESTIA HEALTH LTD Exclusions with ranking equal or below 220 PGH PACT GROUP HOLDINGS LTD Exclusions with ranking equal or below 220 SIG SIGMA HEALTHCARE LTD Failed Eligibility Rank 252 Please contact [email protected] with any queries. Appendix A: Constituent List The index portfolio below is based on data from 2 March 2020. Chi-X Market Operations Phone: +61 2 8078 1701 | Email: [email protected]| Web: chi-x.com.au | Disclaimer Newly added constituents are in BOLD. Chi-X indices (CXA 200 Index) Ticker Name CBA COMMONWEALTH BANK OF AUSTRAL CSL CSL LTD BHP BHP GROUP LTD WBC WESTPAC BANKING CORP NAB NATIONAL AUSTRALIA BANK LTD ANZ AUST AND NZ BANKING GROUP WOW WOOLWORTHS GROUP LTD MQG MACQUARIE GROUP -

Business Leadership: the Catalyst for Accelerating Change

BUSINESS LEADERSHIP: THE CATALYST FOR ACCELERATING CHANGE Follow us on twitter @30pctAustralia OUR OBJECTIVE is to achieve 30% of ASX 200 seats held by women by end 2018. Gender balance on boards does achieve better outcomes. GREATER DIVERSITY ON BOARDS IS VITAL TO THE GOOD GOVERNANCE OF AUSTRALIAN BUSINESSES. FROM THE PERSPECTIVE OF PERFORMANCE AS WELL AS EQUITY THE CASE IS CLEAR. AUSTRALIA HAS MORE THAN ENOUGH CAPABLE WOMEN TO EXCEED THE 30% TARGET. IF YOUR BOARD IS NOT INVESTING IN THE CAPABILITY THAT DIVERSITY BRINGS, IT’S NOW A MARKED DEPARTURE FROM THE WHAT THE INVESTOR AND BROADER COMMUNITY EXPECT. Angus Armour FAICD, Managing Director & Chief Executive Officer, Australian Institute of Company Directors BY BRINGING TOGETHER INFLUENTIAL COMPANY CHAIRS, DIRECTORS, INVESTORS, HEAD HUNTERS AND CEOs, WE WANT TO DRIVE A BUSINESS-LED APPROACH TO INCREASING GENDER BALANCE THAT CHANGES THE WAY “COMPANIES APPROACH DIVERSITY ISSUES. Patricia Cross, Australian Chair 30% Club WHO WE ARE LEADERS LEADING BY EXAMPLE We are a group of chairs, directors and business leaders taking action to increase gender diversity on Australian boards. The Australian chapter launched in May 2015 with a goal of achieving 30% women on ASX 200 boards by the end of 2018. AUSTRALIAN 30% CLUB MEMBERS Andrew Forrest Fortescue Metals Douglas McTaggart Spark Group Ltd Infrastructure Trust Samuel Weiss Altium Ltd Kenneth MacKenzie BHP Billiton Ltd John Mulcahy Mirvac Ltd Stephen Johns Brambles Ltd Mark Johnson G8 Education Ltd John Shine CSL Ltd Paul Brasher Incitec Pivot -

Stoxx® Australia 150 Index

STOXX® AUSTRALIA 150 INDEX Components1 Company Supersector Country Weight (%) Commonwealth Bank of Australia Banks Australia 8.37 CSL Ltd. Health Care Australia 7.46 BHP GROUP LTD. Basic Resources Australia 7.23 National Australia Bank Ltd. Banks Australia 4.37 Westpac Banking Corp. Banks Australia 4.09 Australia & New Zealand Bankin Banks Australia 3.75 Wesfarmers Ltd. Retail Australia 3.30 WOOLWORTHS GROUP Personal Care, Drug & Grocery Australia 2.87 Macquarie Group Ltd. Financial Services Australia 2.84 Rio Tinto Ltd. Basic Resources Australia 2.48 Fortescue Metals Group Ltd. Basic Resources Australia 2.27 Transurban Group Industrial Goods & Services Australia 2.20 Telstra Corp. Ltd. Telecommunications Australia 2.05 Goodman Group Real Estate Australia 1.77 AFTERPAY Industrial Goods & Services Australia 1.54 Coles Group Personal Care, Drug & Grocery Australia 1.39 Woodside Petroleum Ltd. Energy Australia 1.28 Newcrest Mining Ltd. Basic Resources Australia 1.27 Aristocrat Leisure Ltd. Travel & Leisure Australia 1.11 XERO Technology Australia 1.00 SYDNEY AIRPORT Industrial Goods & Services Australia 0.93 Brambles Ltd. Industrial Goods & Services Australia 0.91 Sonic Healthcare Ltd. Health Care Australia 0.90 ASX Ltd. Financial Services Australia 0.82 SCENTRE GROUP Real Estate Australia 0.80 Cochlear Ltd. Health Care Australia 0.74 QBE Insurance Group Ltd. Insurance Australia 0.73 SUNCORP GROUP LTD. Insurance Australia 0.71 South32 Australia Basic Resources Australia 0.71 Santos Ltd. Energy Australia 0.68 Ramsay Health Care Ltd. Health Care Australia 0.66 Insurance Australia Group Ltd. Insurance Australia 0.65 Mirvac Group Real Estate Australia 0.60 DEXUS Real Estate Australia 0.59 SEEK Ltd. -

Issue 35 Stockists

Issue 35 Stockists Outlet Name Address Ainslie Newsagency 3 Edgar Street Woolworths Supermarket 1139 Belconnen Mall Coles Supermarket 779 19771 Cnr Emubank RD & Lathlain Dve Newsfront Newsagency Shop 211 Westfield Shopping Town Newsxpress Belconnen Shop 113 Westfield S/Town Woolworths Suparmarket 1457 61 Mabo Boulevard Woolworths Supermarket 1134 Johnston Drive Canberra House Newsagency Shop1 / 121 Marcus Clark Street Hunt'S Civic Centre Newsagency 47 Northbourne Avenue NLK Relay Canberra Domestic CBR101 Ground Floor Term. Building Convention Centre Newsagency Shop 1/33 Allara Street Supa 24 Convenience 2 Mort Street Charnwood Newsagency Shop 4 Fadco Building Coles Supermarket 858 19771 Shop Centre Halley Street Supanews Canberra Centre A30 Shop EG11 Canberra Centre Lanyon Newsagency SH 18 Lanyon Market Place Curtin Newsagency & Post Office Shop 38 Curtin Place Deakin Newsagency Duff Place Coles Express 1549 25 Hopetoun Circuit Woolworths Supermarket 1073 1 Dickson Place Dickson Newsagency 4 Dickson Place Erindale Newsagency Shop 12 Shopping Centre Coles 803 19771 Cnr Hibberson St & Gungahlin Plce Woolworths Supermarket 1279 Old Joe Road Penneys Papershop Shop 17 40-56 Hibberson Street Gungahlin Centre News Shop 12 Gungahlin Market Place Hawker Place Cards & Gifts Pty Ltd Shop 1&2/72-74 Hawker Place Kippax Fair Newsagency 25-27 Kippax Ctr & Hardwick Cres Coles Supermarket 748 19771 Redfern Street Kingston Newsagency 66 Giles Street Lyneham Newsagency Shop 3 Wattle Place Jamison Plaza News Shop A 06 Jamison Plaza Woolworths Suparmarket -

2012 DEXUS ANNUAL Report

2012 DEXUS ANNUAL REPORT DEXUS DIVERSIFIED TRUST (ARSN 089 324 541) Letter frOM THE CHAir 1 FIVE YEAR FINANCIAL SUMMAry 3 BOArd OF DirectOrs 4 CORPORAte GOvernAnce stAteMent 6 FinAnciAL REPORT DIRECTORS’ REPORT 14 AUDITOr’S IndePendenCE DEClaRATIOn 38 CONSOLIDATED STATEMenT OF COMPREHensIVE InCOME 39 CONSOLIDATED STATEMenT OF FInanCIal POSITIOn 40 CONSOLIDATED STATEMenT OF CHanGes IN EQUITY 41 CONSOLIDATED STATEMenT OF CasH FlOWS 42 NOTes TO THE FInanCIal STATEMenTs 43 DIRECTORS’ DEClaRATIOn 89 IndePendenT AUDITOr’S RePORT 90 AdditiONAL InfORMATION 92 InvestOR InfORMAtiON 94 DirectOry 96 2012 Annual Reporting suite DEXUS Property Group (DXS) presents our 2012 annual reporting suite and supporting material for the year ending 30 June 2012: 1. The 2012 DEXUS Annual Review – an integrated report summarising our financial, operational and Corporate Responsibility and Sustainability (CR&S) performance. 2. This 2012 DEXUS Annual Report – DXS’s consolidated financial statements, Corporate Governance Statement and information about our Board of Directors. This document should be read in conjunction with the 2012 DEXUS Annual Review. 3. The 2012 DEXUS Combined Financial Statements – the Financial Statements of DEXUS Industrial Trust, DEXUS Office Trust and DEXUS Operations Trust. This document should be read in conjunction with the 2012 DEXUS Annual Report and Annual Review. It is available in hard copy on request by email at [email protected], phone on 1800 819 675 or online in our annual reporting suite at www.dexus.com/dxs/reports 4. The 2012 DEXUS Performance Pack – the data and information supporting the results outlined in the 2012 DEXUS Annual Review will be available in our online annual reporting suite from mid-October 2012. -

Presentation of the Group PDF 603KB

2 Universal Registration Document 2020 / UNIBAIL-RODAMCO-WESTFIELD Presentation of the Group Presentation of the Group 1.1 KEY FACTS 3 1.2 HISTORY 4 1.3 STRATEGY AND BUSINESS MODEL 6 1.4 BUSINESS OVERVIEW 12 Business segments 12 Portfolio breakdown 13 Development pipeline 15 CHAPTER 1.5 PORTFOLIO 16 1.5.1 France: Shopping Centres 16 1.5.2 France: Convention & Exhibition 18 1.5.3 France: Offices 19 1.5.4 Central Europe: Shopping Centres 20 1.5.5 Central Europe: Offices 21 1.5.6 Spain: Shopping Centres 21 1.5.7 Spain: Offices 21 1.5.8 Nordics: Shopping Centres 22 1.5.9 Nordics: Offices 22 1.5.10 Austria: Shopping Centres 23 1.5.11 Austria: Offices 23 1.5.12 Germany: Shopping Centres 24 1.5.13 Germany: Offices 24 1.5.14 The Netherlands: Shopping Centres 25 1.5.15 The Netherlands: Offices 25 1.5.16 United States: Shopping Centres 26 1.5.17 United States: Offices 28 1.5.18 United Kingdom: Shopping Centres 29 1.5.19 United Kingdom: Offices 29 1.6 OVERVIEW OF VALUATION REPORTS PREPARED BY UNIBAIL-RODAMCO-WESTFIELD’S INDEPENDENT EXTERNAL APPRAISERS FOR EUROPEAN ASSETS 30 1.7 OVERVIEW OF VALUATION REPORTS PREPARED BY UNIBAIL-RODAMCO-WESTFIELD’S INDEPENDENT EXTERNAL APPRAISERS FOR AMERICAN ASSETS 32 1.8 STRUCTURE 34 1.9 SIMPLIFIED GROUP ORGANISATIONAL CHART 35 Universal Registration Document 2020 / UNIBAIL-RODAMCO-WESTFIELD 3 Presentation of the Group Key facts 1.1 KEY FACTS 1. 87 16 OFFICES & OTHERS SHOPPING CENTRES BUILDINGS(1) 10 80% CONVENTION & EXHIBITION COLLECTION RATE(3) VENUES(2) 247 ~3,100 COVID-19 ESG INITIATIVES EMPLOYEES €1,790 Mn €7.28 ADJUSTED RECURRING NET RENTAL INCOME EARNINGS PER SHARE €2.3 Bn €56.3 Bn DISPOSALS(4) GROSS MARKET VALUE €166.8 €4.4 Bn EPRA NET REINSTATEMENT PIPELINE VALUE PER SHARE (1) Only standalone offices > 10,000 sqm and offices affixed to a shopping centre > 15,000 sqm, including La Vaguada offices.