2015 Annual Results 19 August 2015 Agenda

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

6 January 2021 – Correct As of 4Pm You Will Be Denied Entry to a Greengate Village If You Have Visited One of the Following CO

6 January 2021 – correct as of 4pm You will be denied entry to a Greengate Village if you have visited one of the following COVID-19 hot spots or case locations: HOT SPOTS: • Ashfield Wednesday 23 December 2020 • Auburn BCF (Boating Fishing Camping) Wednesday 30 December 2020 • Auburn Reading Cinema Auburn Tuesday 22 December 2020 • Balmain Balmain Post Office Monday 28 December 2020 • Bankstown Bankstown Sports Club Monday 28 December 2020 • Bankstown La Piazza - Bankstown Sports Club Monday 28 December 2020 • Bankstown Monkey Mania - Bankstown Sports Club Thursday 24 December 2020 • Bankstown Priceline Pharmacy Bankstown Monday 28 December 2020 • Bardwell Park Earlwood Bardwell Park RSL Thursday 24 December 2020 • Bass Hill #Hair Management Thursday 24 December 2020 • Bass Hill BWS Bass Hill Thursday 24 December 2020 • Bass Hill Bass Hill Plaza Thursday 24 December 2020 • Bass Hill Venus Nail Salon Thursday 24 December 2020 • Belfield Mancini’s Pizza @ Belfield Tuesday 22 December 2020 • Wednesday 23 December 2020 Thursday 24 December 2020 Saturday 26 December 2020 • Sunday 27 December 2020 Monday 28 December 2020 Tuesday 29 December 2020 Wednesday 30 December 2020 Thursday 31 December 2020 • Berala BWS Berala Saturday 26 December 2020 Monday 28 December 2020 • Berala Pure Thai Berala Monday 21 December 2020 Wednesday 23 December 2020 Sunday 20 December 2020 Thursday 24 December 2020 Saturday 26 December 2020 Monday 28 December 2020Tuesday 22 December 2020 Sunday 27 December 2020 Tuesday 29 December 2020 Wednesday 30 December 2020 Thursday -

Suburb Pharmacy Name Address Allambie Heights Allambie Neighbourhood Pharmacy 44 Kentwell Road

Suburb Pharmacy Name Address Allambie Heights Allambie Neighbourhood Pharmacy 44 Kentwell Road Allambie Heights Troys Pharmacy 10 Grigor Place Artarmon Nick Logan Pharmacist Advice 96 Hampden Road Asquith SuperSave Chemist Asquith 343 Pacific Highway Avalon Beach Avalon Beach Pharmacy 40 Avalon Parade Avalon Beach Chemist Warehouse Avalon Shop 4 74 Old Barrenjoey Road Avalon Beach Herforts Yousave Chemist Avalon Beach 60 Old Barrenjoey Road Balgowlah Balgowlah Pharmacy 361 Sydney Road Balgowlah Pharmacy Nutrition Warehouse Balgowlah 352 Sydney Road Balgowlah Heights Balgowlah Heights Pharmacy 67 New Street West Baulkham Hills Chemist Outlet Baulkham Hills 323 Windsor Road Baulkham Hills Crestwood Centre Pharmacy Shop 2 Glanmire Road Baulkham Hills Mullane's Pharmacy Shop 99 Stockland Mall, near Woolworths Baulkham Hills Soul Pattinson Chemist Baulkham Hills Shop 3-4 Stockland Mall, next to Aldi Beaumont Hills Pauls Pharmacy Plus Beaumont Hills Shop 10-12 70 The Parkway Beecroft Beecroft Pharmacy 11 Wongala Crescent Beecroft Denny Pharmacy Beecroft Arcade, 6-8 Hannah Street Bella Vista Choice Pharmacy Bella Vista Shop 21 1 Circa Boulevard Belrose Belrose Chemist Shop 41-42 Glenrose Centre, Glen Street Belrose Cincotta Chemist Belrose Homemaker Supa Centa, 4-6 Niangala Close Berowra Berowra Station Pharmacy 1/993 Pacific Highway Berowra Heights Berowra Heights Chemist 2A The Market Place 15 Turner Road Berowra Heights Berowra Village Pharmacy Shop 3, 1A Turner Road Blackheath Dash's Blackheath Pharmacy 239 Great Western Highway Blaxland -

Socially Conscious Australian Equity Holdings

Socially Conscious Australian Equity Holdings As at 30 June 2021 Country of Company domicile Weight COMMONWEALTH BANK OF AUSTRALIA AUSTRALIA 10.56% CSL LTD AUSTRALIA 8.46% AUST AND NZ BANKING GROUP AUSTRALIA 5.68% NATIONAL AUSTRALIA BANK LTD AUSTRALIA 5.32% WESTPAC BANKING CORP AUSTRALIA 5.08% TELSTRA CORP LTD AUSTRALIA 3.31% WOOLWORTHS GROUP LTD AUSTRALIA 2.93% FORTESCUE METALS GROUP LTD AUSTRALIA 2.80% TRANSURBAN GROUP AUSTRALIA 2.55% GOODMAN GROUP AUSTRALIA 2.34% WESFARMERS LTD AUSTRALIA 2.29% BRAMBLES LTD AUSTRALIA 1.85% COLES GROUP LTD AUSTRALIA 1.80% SUNCORP GROUP LTD AUSTRALIA 1.62% MACQUARIE GROUP LTD AUSTRALIA 1.54% JAMES HARDIE INDUSTRIES IRELAND 1.51% NEWCREST MINING LTD AUSTRALIA 1.45% SONIC HEALTHCARE LTD AUSTRALIA 1.44% MIRVAC GROUP AUSTRALIA 1.43% MAGELLAN FINANCIAL GROUP LTD AUSTRALIA 1.13% STOCKLAND AUSTRALIA 1.11% DEXUS AUSTRALIA 1.11% COMPUTERSHARE LTD AUSTRALIA 1.09% AMCOR PLC AUSTRALIA 1.02% ILUKA RESOURCES LTD AUSTRALIA 1.01% XERO LTD NEW ZEALAND 0.97% WISETECH GLOBAL LTD AUSTRALIA 0.92% SEEK LTD AUSTRALIA 0.88% SYDNEY AIRPORT AUSTRALIA 0.83% NINE ENTERTAINMENT CO HOLDINGS LIMITED AUSTRALIA 0.82% EAGERS AUTOMOTIVE LTD AUSTRALIA 0.82% RELIANCE WORLDWIDE CORP LTD UNITED STATES 0.80% SANDFIRE RESOURCES LTD AUSTRALIA 0.79% AFTERPAY LTD AUSTRALIA 0.79% CHARTER HALL GROUP AUSTRALIA 0.79% SCENTRE GROUP AUSTRALIA 0.79% ORORA LTD AUSTRALIA 0.75% ANSELL LTD AUSTRALIA 0.75% OZ MINERALS LTD AUSTRALIA 0.74% IGO LTD AUSTRALIA 0.71% GPT GROUP AUSTRALIA 0.69% Issued by Aware Super Pty Ltd (ABN 11 118 202 672, AFSL 293340) the trustee of Aware Super (ABN 53 226 460 365). -

Asx Clear – Acceptable Collateral List 28

et6 ASX CLEAR – ACCEPTABLE COLLATERAL LIST Effective from 20 September 2021 APPROVED SECURITIES AND COVER Subject to approval and on such conditions as ASX Clear may determine from time to time, the following may be provided in respect of margin: Cover provided in Instrument Approved Cover Valuation Haircut respect of Initial Margin Cash Cover AUD Cash N/A Additional Initial Margin Specific Cover N/A Cash S&P/ASX 200 Securities Tiered Initial Margin Equities ETFs Tiered Notes to the table . All securities in the table are classified as Unrestricted (accepted as general Collateral and specific cover); . Specific cover only securities are not included in the table. Any securities is acceptable as specific cover, with the exception of ASX securities as well as Participant issued or Parent/associated entity issued securities lodged against a House Account; . Haircut refers to the percentage discount applied to the market value of securities during collateral valuation. ASX Code Security Name Haircut A2M The A2 Milk Company Limited 30% AAA Betashares Australian High Interest Cash ETF 15% ABC Adelaide Brighton Ltd 30% ABP Abacus Property Group 30% AGL AGL Energy Limited 20% AIA Auckland International Airport Limited 30% ALD Ampol Limited 30% ALL Aristocrat Leisure Ltd 30% ALQ ALS Limited 30% ALU Altium Limited 30% ALX Atlas Arteria Limited 30% AMC Amcor Ltd 15% AMP AMP Ltd 20% ANN Ansell Ltd 30% ANZ Australia & New Zealand Banking Group Ltd 20% © 2021 ASX Limited ABN 98 008 624 691 1/7 ASX Code Security Name Haircut APA APA Group 15% APE AP -

Government Gazette of the STATE of NEW SOUTH WALES Number 160 Wednesday, 24 December 2008 Published Under Authority by Government Advertising LEGISLATION Orders

12957 Government Gazette OF THE STATE OF NEW SOUTH WALES Number 160 Wednesday, 24 December 2008 Published under authority by Government Advertising LEGISLATION Orders New South Wales Transport Administration (Sydney Ferries—Fares) Amendment Order 2008 under the Transport Administration Act 1988 I, Rear Admiral Geoff Smith AO, Chief Executive Officer of Sydney Ferries, in pursuance of the Transport Administration Act 1988, make the following Order on behalf of Sydney Ferries. Dated, this 19th day of Decemberday of December 2008. 2008. Chief Executive Officer Sydney Ferries Explanatory note The object of this Order is to amend the Transport Administration (Sydney Ferries—Fares) Order 2004 (the Principal Order) to increase, from 4 January 2009, certain multi-trip and weekly periodical fares for Sydney Ferries services in the Sydney Suburban Area. The fares include fares for services that are provided in conjunction with bus services provided by the State Transit Authority and rail services provided by RailCorp in the Sydney Suburban Area. The increases are in accordance with recent determinations of the Independent Pricing and Regulatory Tribunal. This Order also makes amendments to the Principal Order relating to the JetCat service consequential on the withdrawal from service of the JetCat fleet after 31 December 2008. This Order is made under the Transport Administration Act 1988, including section 85 (Orders fixing charges). s2008-553-09.d05 Page 1 12958 LEGISLATION 24 December 2008 Clause 1 Transport Administration (Sydney Ferries—Fares) Amendment Order 2008 Transport Administration (Sydney Ferries—Fares) Amendment Order 2008 under the Transport Administration Act 1988 1 Name of Order This Order is the Transport Administration (Sydney Ferries—Fares) Amendment Order 2008. -

Index Rebalance

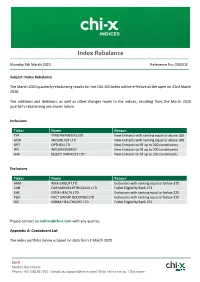

Index Rebalance Monday 9th March 2020 Reference No: 0002/20 Subject: Index Rebalance The March 2020 quarterly rebalancing results for the CXA 200 Index will be effective at the open on 23rd March 2020. The additions and deletions, as well as other changes made to the indices, resulting from the March 2020 quarterly rebalancing are shown below. Inclusions Ticker Name Reason TYR TYRO PAYMENTS LTD New Entrants with ranking equal or above 180 MSB MESOBLAST LTD New Entrants with ranking equal or above 180 OPT OPTHEA LTD New Entrants to fill up to 200 constituents IFN INFIGEN ENERGY New Entrants to fill up to 200 constituents SHV SELECT HARVESTS LTD New Entrants to fill up to 200 constituents Exclusions Ticker Name Reason AMA AMA GROUP LTD Exclusions with ranking equal or below 220 CVN CARNARVON PETROLEUM LTD Failed Eligibility Rank 273 EHE ESTIA HEALTH LTD Exclusions with ranking equal or below 220 PGH PACT GROUP HOLDINGS LTD Exclusions with ranking equal or below 220 SIG SIGMA HEALTHCARE LTD Failed Eligibility Rank 252 Please contact [email protected] with any queries. Appendix A: Constituent List The index portfolio below is based on data from 2 March 2020. Chi-X Market Operations Phone: +61 2 8078 1701 | Email: [email protected]| Web: chi-x.com.au | Disclaimer Newly added constituents are in BOLD. Chi-X indices (CXA 200 Index) Ticker Name CBA COMMONWEALTH BANK OF AUSTRAL CSL CSL LTD BHP BHP GROUP LTD WBC WESTPAC BANKING CORP NAB NATIONAL AUSTRALIA BANK LTD ANZ AUST AND NZ BANKING GROUP WOW WOOLWORTHS GROUP LTD MQG MACQUARIE GROUP -

Aurizon Debt Investor Roadshow December 2016

Aurizon Debt Investor Roadshow December 2016 “Aurizon – Australia’s largest rail freight operator” Pam Bains – VP Network Finance (Network CFO) David Collins – VP Finance & Group Treasurer Further information is available online at www.aurizon.com.au Important notice No Reliance on this document This document was prepared by Aurizon Holdings Limited (ACN 146 335 622) (referred to as “Aurizon” which includes its related bodies corporate). Whilst Aurizon has endeavoured to ensure the accuracy of the information contained in this document at the date of publication, it may contain information that has not been independently verified. Aurizon makes no representation or warranty as to the accuracy, completeness or reliability of any of the information contained in this document. Document is a summary only This document contains information in a summary form only and does not purport to be complete and is qualified in its entirety by, and should be read in conjunction with, all of the information which Aurizon files with the Australian Securities Exchange. Any information or opinions expressed in this document are subject to change without notice. Aurizon is not under any obligation to update or keep current the information contained within this document. Information contained in this document may have changed since its date of publication. No investment advice This document is not intended to be, and should not be considered to be, investment advice by Aurizon nor a recommendation to invest in Aurizon. The information provided in this document has been prepared for general informational purposes only without taking into account the recipient’s investment objectives, financial circumstances, taxation position or particular needs. -

Business Leadership: the Catalyst for Accelerating Change

BUSINESS LEADERSHIP: THE CATALYST FOR ACCELERATING CHANGE Follow us on twitter @30pctAustralia OUR OBJECTIVE is to achieve 30% of ASX 200 seats held by women by end 2018. Gender balance on boards does achieve better outcomes. GREATER DIVERSITY ON BOARDS IS VITAL TO THE GOOD GOVERNANCE OF AUSTRALIAN BUSINESSES. FROM THE PERSPECTIVE OF PERFORMANCE AS WELL AS EQUITY THE CASE IS CLEAR. AUSTRALIA HAS MORE THAN ENOUGH CAPABLE WOMEN TO EXCEED THE 30% TARGET. IF YOUR BOARD IS NOT INVESTING IN THE CAPABILITY THAT DIVERSITY BRINGS, IT’S NOW A MARKED DEPARTURE FROM THE WHAT THE INVESTOR AND BROADER COMMUNITY EXPECT. Angus Armour FAICD, Managing Director & Chief Executive Officer, Australian Institute of Company Directors BY BRINGING TOGETHER INFLUENTIAL COMPANY CHAIRS, DIRECTORS, INVESTORS, HEAD HUNTERS AND CEOs, WE WANT TO DRIVE A BUSINESS-LED APPROACH TO INCREASING GENDER BALANCE THAT CHANGES THE WAY “COMPANIES APPROACH DIVERSITY ISSUES. Patricia Cross, Australian Chair 30% Club WHO WE ARE LEADERS LEADING BY EXAMPLE We are a group of chairs, directors and business leaders taking action to increase gender diversity on Australian boards. The Australian chapter launched in May 2015 with a goal of achieving 30% women on ASX 200 boards by the end of 2018. AUSTRALIAN 30% CLUB MEMBERS Andrew Forrest Fortescue Metals Douglas McTaggart Spark Group Ltd Infrastructure Trust Samuel Weiss Altium Ltd Kenneth MacKenzie BHP Billiton Ltd John Mulcahy Mirvac Ltd Stephen Johns Brambles Ltd Mark Johnson G8 Education Ltd John Shine CSL Ltd Paul Brasher Incitec Pivot -

Attention ASX Company Announcements Platform. Lodgement of Open Briefing

Attention ASX Company Announcements Platform. Lodgement of Open Briefing. Wesfarmers Limited Wesfarmers House 40 The Esplanade Perth Western Australia 6000 Date of Lodgement: 17-Nov-2004 Title: Open Briefing. Wesfarmers. Briefing Day Discussion The content of this Open Briefing reflects management and analyst discussion at the Wesfarmers Briefing Day held in Sydney on Thursday November 11, 2004. General Corporate Issues corporatefile.com.au Wesfarmers seems to be a little more conservative than other companies on the macro outlook for some of its industries. BHP, for example, seems a lot more bullish. Is there a risk Wesfarmers misses out on some good projects if you are too conservative? Michael Chaney, CEO Wesfarmers We often think about this issue and we’re continually reviewing our assumptions but I’m confident that we haven’t been too conservative. I believe that our assumptions are broadly similar to companies such as BHP for example. Projects or companies are often valued differently by different parties because of strategic considerations rather than different pricing assumptions. Although we have missed opportunities over the years, we’ve still recorded the highest TSR on the ASX over 20 years. Investors should be confident with our management team because we have entrenched and strict valuation disciplines and methodologies. We’ll miss out on more opportunities but enough opportunities should come up to maintain our shareholder returns. corporatefile.com.au Coal prices will fall at some stage. Will that influence you to take a more conservative stance on dividends in the next couple of years in order to avoid the possibility of having to cut dividends after coking prices fall? 1 Michael Chaney I don’t think so because that would be inconsistent with our dividend policy which is to always pay out 100% of our franking credits. -

Amazon Coming to a Car Yard Near You: Cole

Amazon coming to a car yard near you: Cole Digital ‘story teller’ Jeff Cole, right, with David Evans. ‘Eventually (Jeff Bezos) will sell every new automobile in North America’ October 7, 2018 By DAMON KITNEY, STUART McEVOY Amazon could be set to transform another industry He calls himself a “story teller” of the digital world. His clients think he can see into the future. Jeffrey Cole has spent more than three decades advising governments and many of the world’s largest and most successful companies on their digital strategies. In Australia those companies have included Telstra, Wesfarmers, Westpac and the other big banks. Amazon coming to a car yard near you: Cole !2 These days he is a member of the investment committee of the listed Evans & Partners Global Disruption Fund, which now has over $400 million under management and ambitions to grow that to $1 billion in the short to medium term. The fund has just completed an $8m capital raising to provide liquidity for new unit holders. Ask Cole the next industry in the world to be “Amazoned” — that is, disrupted and transformed by Jeff Bezos’s global tech colossus — and his answer is instant. “I think eventually he will sell every new automobile in North America. A lot of manufacturers feel they are saddled to their dealers. A lot of them now want to get rid of the dealer relationship. Tesla, for instance, does not have dealerships. I think you will see Amazon go to manufacturers and say ‘Get out of the dealership business’, and turn the dealerships into service centres,’’ the fast-talking American tells The Australian during a visit to Australia from his US base. -

Masterplan Stage 04 - Masterplan Report

PAUL KEATING PARK MASTERPLAN STAGE 04 - MASTERPLAN REPORT PAUL KEATING PARK MASTERPLAN EXECUTIVE SUMMARY In the next 20 years, the Bankstown CBD will see substantial growth The Appian Way offers a major pedestrian entrance into the site from and increased demand on its parks, streets and cultural facilities due to Bankstown Metro Station, providing access to surrounding buildings greater amounts of jobs, students and residents. The Paul Keating Park and programs, and integrating environmental functionality. Adjacent to Masterplan presents the opportunity to respond to this future trajectory, this, the Play Space offers further amenity and shade, with a custom, focusing on the Civic Precinct, the centrepiece of Bankstown CBD, inclusive and varied playground and spaces for parents congregate. The to revitalise open space offerings whilst also addressing the current Green Incline, by contrast, offers access to sunshine and a large open challenges of the site. space for leisure, resolving connectivity between upper and lower levels of the site, and providing the opportunity for an integrated community building below. The masterplan and design outcomes presented within this report are based on a detailed understanding of these challenges, along with the current and future contexts of the site. These studies are incorporated A redesigned entryway to BLaKC, incorporating an outdoor dining within the initial chapters of the report through context mappings, site terrace and an opened-up façade, activates the existing building from considerations diagrams and design principles that were used as a Chapel St and allows a transition of programs between interior and framework for producing the masterplan. Furthermore, community exterior. -

Oriental & Continental Foods Mini Market 43 Carlotta

Customer Name Type Address Suburb Postcode ORIENTAL & CONTINENTAL FOODS MINI MARKET 43 CARLOTTA STREET ARTARMON 2064 NATURES BEST BELFIELD PRODUCE MARKET 29 BURWOOD RD BELFIELD 2191 IGA BERRY SUPERMARKET 123 QUEEN ST BERRY 2535 KEMENY'S FOOD & LIQUOR BOTTLE SHOP AND LIQUOR STORE 137/147 BONDI RD BONDI 2026 GLENAYR CONVENIENCE CONVENIENCE STORE 133/137 GLENAYR AVE, BONDI BEACH BONDI 2026 FRIENDLY GROCER 7 WAYS SUPERMARKET 85 GLENAYR AVE BONDI 2026 CAFÉ BRAZIL CAFÉ & RESTAURANT 195, BONDI RD BONDI BEACH 2026 DOCTOR EARTH MINI MARKET 444 OXFORD ST BONDI JUNCTION2022 IGA BOTANY SUPERMARKET 1128, BOTANY RD BOTANY 2019 TOPPING MAD PIZZA PIZZARIA & RESTAURANT 65, MACPHERSON ST BRONTE 2024 QUATTRO FORMAGGI DELI BROOKVALE GOURMET GROCERY STORE WESTFIELD WARRINGAH MALL, SHOP X6-X8 CROSS ST WARRINGAH MALL SHOPPING CENTRE BROOKVALE 2100 BULLI FRUIT & VEG PRODUCE MARKET 161 PRINCES HWY BULLI 2516 CANBERRA CHOICE SUPERMARKETS PTY LTD SUPERMARKET 2 BARKER ST, GRIFFITH CANBERRA 2614 FRIENDLY GROCER COOK SUPERMARKET SUPERMARKET 27 COOK PL CANBERRA 2614 DIJON FOODS PTY LTD WHOLESALER 5-7 RESOLUTION DRIVE CARINGBAH 2229 IGA CASTLECRAIG SUPERMARKET CNR EASTERN VALLEY WAY & EDINBURGH RD CASTLECRAG 2068 FRUIT EZY MKT CHATSWOOD CHASE SUPERMARKET CHATSWOOD CHASE SYDNEY, WESTFIELD CHATSWOOD, B001/345 VICTORIA AVE CHATSWOOD 2067 FRIENDLY GROCER CROYDON GROCERY STORE 11 THE STRAND CROYDON 2132 BEL FRESCO - BIRKENHEAD POINT OUTLET CENTRE GROCERY SHOP 113, BIRKENHEAD POINT SHOPPING CENTRE DRUMMOYNE 2047 BEL FRESCO - BIRKENHEAD POINT OUTLET CENTRE SHOPPING MALL 19