BYD Electronic | 285.HK

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

China Equity Strategy

June 5, 2019 09:40 AM GMT MORGAN STANLEY ASIA LIMITED+ China Equity Strategy | Asia Pacific Jonathan F Garner EQUITY STRATEGIST [email protected] +852 2848-7288 The Rubio "Equitable Act" - Our Laura Wang EQUITY STRATEGIST [email protected] +852 2848-6853 First Thoughts Corey Ng, CFA EQUITY STRATEGIST [email protected] +852 2848-5523 Fran Chen, CFA A new bill sponsored by US Senator Marco Rubio has the EQUITY STRATEGIST potential to cause significant change in the listing domains of [email protected] +852 2848-7135 Chinese firms. After the market close in the US yesterday 4th June the Wall Street Journal published an Op-Ed by US Senator Marco Rubio in which he announced that he intends to sponsor the “Equitable Act” – an acronym for Ensuring Quality Information and Transparency for Abroad-Based Listings on our Exchanges. At this time the text of the bill has not been published and we are seeking additional information about its contents and likelihood of passing. However, our early reaction is that this has the potential to cause significant changes in the domain for listings of Chinese firms going forward with the potential for de- listing of Chinese firms on US exchanges and re-listing elsewhere (most likely Hong Kong). More generally we see this development as part of an increased escalation of tensions between China and the US on multiple fronts which should cap the valuation multiple for China equities, in particular in the offshore index constituents and US-listed parts of the universe. We provide a list of the potentially impacted China / HK names with either primary or secondary listings on Amex, NYSE or Nasdaq. -

2020 Interim Results Announcement

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. (incorporated in Hong Kong under the Companies Ordinance with limited liability) (Stock code: 285) 2020 INTERIM RESULTS ANNOUNCEMENT The Board of Directors of the Company (the “Board”) is pleased to announce the unaudited results of the Company and its subsidiaries for the six months period ended 30 June 2020. This announcement, containing the full text of the 2020 Interim Report of the Company, is prepared with reference to the relevant requirements of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited in relation to preliminary announcements of interim results. Printed version of the Company’s 2020 Interim Report will be delivered to the Company’s shareholders and is also available for viewing on the websites of Hong Kong Exchanges and Clearing Limited at http://www.hkex.com.hk and of the Company at http://www.byd-electronics.com. By Order of the Board of BYD Electronic (International) Company Limited WANG Nian-qiang Director Hong Kong, 28 August 2020 As at the date of this announcement, the executive Directors of the Company are Mr. WANG Nian- qiang and Mr. JIANG Xiang-rong; the non-executive Directors are Mr. WANG Chuan-fu and Mr. WANG Bo; and the independent non-executive Directors are Mr. -

Technology 6 November 2017

INDUSTRY NOTE China | Technology 6 November 2017 Technology EQUITY RESEARCH China Summit Takeaway: AI, Semi, Smartphone Value Chain Key Takeaway We hosted several experts and 24 A/H corporates at our China Summit and Digital Disruption tour last week. Key takeaways: 1) AI shifting from central cloud to the edge (end devices), driving GPU/FPGA demand in near term, 2) AI leaders in China rolling out own ASICs in the next 2~3 years, 3) China's new role in semi, forging ahead in design and catching up in foundry. In smartphone value chain, maintain AAC as top pick for lens opportunity and Xiaomi strength. CHINA Artificial Intelligence - From cloud to edge computing: The rise of AI on the edge (terminal devices, like surveillance cameras, smartphones) from central cloud, can solve one key weakness of AI: the brains are located thousands of miles away from the applications. The benefits of AI on the edge include: 1) better analysis based on non-compressed raw data, which contains more information, 2) lower requirement on bandwidth, as transmitted data has been pre-processed, 3) faster response. This will keep driving the demands for GPUs and FPGAs in near term. Meanwhile, China's leading AI companies including Hikvision (002415 CH) and Unisound (private, leader in voice recognition) also noted they may develop own ASICs in the next 2~3 years, for better efficiency and low power. While machines getting smarter, we notice increasing concerns on data privacy. Governments are not only implementing Big Data laws and policies, also starts investing AI leaders, like Face ++ (computer vision) in China. -

AQR TM Emerging Multi-Style Fund June 30, 2021

AQR TM Emerging Multi-Style Fund June 30, 2021 Portfolio Exposures NAV: $685,149,993 Asset Class Security Description Exposure Quantity Equity A-Living Services Ord Shs H 2,001,965 402,250 Equity Absa Group Ord Shs 492,551 51,820 Equity Abu Dhabi Commercial Bank Ord Shs 180,427 96,468 Equity Accton Technology Ord Shs 1,292,939 109,000 Equity Acer Ord Shs 320,736 305,000 Equity Adani Enterprises Ord Shs 1,397,318 68,895 Equity Adaro Energy Tbk Ord Shs 2,003,142 24,104,200 Equity Advanced Info Service Non-Voting DR 199,011 37,300 Equity Advanced Petrochemical Ord Shs 419,931 21,783 Equity Agricultural Bank of China Ord Shs A 288,187 614,500 Equity Agricultural Bank Of China Ord Shs H 482,574 1,388,000 Equity Al Rajhi Bank Ord Shs 6,291,578 212,576 Equity Alibaba Group Holding ADR Representing 8 Ord Shs 33,044,794 145,713 Equity Alinma Bank Ord Shs 1,480,452 263,892 Equity Ambuja Cements Ord Shs 305,517 66,664 Equity Anglo American Platinum Ord Shs 174,890 1,514 Equity Anhui Conch Cement Ord Shs A 307,028 48,323 Equity Anhui Conch Cement Ord Shs H 1,382,025 260,500 Equity Arab National Bank Ord Shs 485,970 80,290 Equity ASE Technology Holding Ord Shs 2,982,647 742,000 Equity Asia Cement Ord Shs 231,096 127,000 Equity Aspen Pharmacare Ord Shs 565,696 49,833 Equity Asustek Computer Ord Shs 1,320,000 99,000 Equity Au Optronics Ord Shs 2,623,295 3,227,000 Equity Aurobindo Pharma Ord Shs 3,970,513 305,769 Equity Autohome ADS Representing 4 Ord Shs Class A 395,017 6,176 Equity Axis Bank GDR 710,789 14,131 Equity Ayala Land Ord Shs 254,266 344,300 -

Generic Internationalization Strategies of Emerging Market Multinationals: the Case of Chinese Firms

Advances in Economics and Business 5(2): 83-94, 2017 http://www.hrpub.org DOI: 10.13189/aeb.2017.050205 Generic Internationalization Strategies of Emerging Market Multinationals: The Case of Chinese Firms Kun Tan Newhuadu Business School, Minjiang University, China Copyright©2017 by authors, all rights reserved. Authors agree that this article remains permanently open access under the terms of the Creative Commons Attribution License 4.0 International License Abstract This paper investigates how the choices of the early 1980s [2] [3] [4], attention to this topic became an strategic directions by Chinese multinational enterprises import research in international business in the 2000s [5] [6] have led them to adopt distinct strategies in [7] [8] [9] [10] [11], because emerging-market firms are internationalization. The study takes a multiple case study quickly catching up and internationalizing in recent years. approach. It was found that the generic strategies of Scholars are starting to take stock of what is actually known Chinese internationalization are local optimizer; low-cost about EMNEs and what is speculation [12]. supplier, advanced-market seeker, and global consolidator, Particularly, the rise of emerging economies such as China each of which depends on a multinational enterprise’s and India has generated a number of EMNEs, providing an preference in combination with its strategic directions e.g. opportunity for scholars to review the theories of MNEs’ target countries, value chain movement, branding, and internationalization in contemporary context [13]. For mode of entry. Finally the generic strategies as a common example, Paul and Mas [14] examined the common factors framework for studying the internationalization of emerging that had contributed to the emergence of Chinese and Indian market multinationals are proposed. -

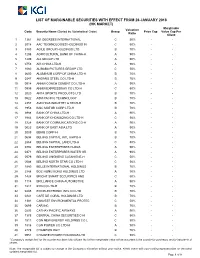

HK Marginable List

LIST OF MARGINABLE SECURITIES WITH EFFECT FROM 26 JANUARY 2018 (HK MARKET) Marginable Valuation Code Security Name (Sorted by Alphabetical Order) Group Price Cap Value Cap Per Ratio Client 1 1361 361 DEGREES INTERNATIONAL C 50% - - 2 2018 AAC TECHNOLOGIES HOLDINGS IN C 50% - - 3 3383 AGILE GROUP HOLDINGS LTD B 70% - - 4 1288 AGRICULTURAL BANK OF CHINA-H A 90% - - 5 1299 AIA GROUP LTD A 90% - - 6 0753 AIR CHINA LTD-H A 90% - - 7 1060 ALIBABA PICTURES GROUP LTD C 50% - - 8 2600 ALUMINUM CORP OF CHINA LTD-H B 70% - - 9 0347 ANGANG STEEL CO LTD-H B 70% - - 10 0914 ANHUI CONCH CEMENT CO LTD-H A 90% - - 11 0995 ANHUI EXPRESSWAY CO LTD-H C 50% - - 12 2020 ANTA SPORTS PRODUCTS LTD B 70% - - 13 0522 ASM PACIFIC TECHNOLOGY B 70% - - 14 2357 AVICHINA INDUSTRY & TECH-H B 70% - - 15 1958 BAIC MOTOR CORP LTD-H B 70% - - 16 3988 BANK OF CHINA LTD-H A 90% - - 17 1963 BANK OF CHONGQING CO LTD-H C 50% - - 18 3328 BANK OF COMMUNICATIONS CO-H A 90% - - 19 0023 BANK OF EAST ASIA LTD A 90% - - 20 2009 BBMG CORP-H B 70% - - 21 0694 BEIJING CAPITAL INTL AIRPO-H B 70% - - 22 2868 BEIJING CAPITAL LAND LTD-H C 50% - - 23 0392 BEIJING ENTERPRISES HLDGS A 90% - - 24 0371 BEIJING ENTERPRISES WATER GR A 90% - - 25 0579 BEIJING JINGNENG CLEAN ENE-H C 50% - - 26 0588 BEIJING NORTH STAR CO LTD-H C 50% - - 27 1880 BELLE INTERNATIONAL HOLDINGS B 70% - - 28 2388 BOC HONG KONG HOLDINGS LTD A 90% - - 29 1428 BRIGHT SMART SECURITIES AND C 50% - - 30 1114 BRILLIANCE CHINA AUTOMOTIVE A 90% - - 31 1211 BYD CO LTD-H B 70% - - 32 0285 BYD ELECTRONIC INTL CO LTD B 70% - - 33 0341 CAFE DE CORAL HOLDINGS LTD B 70% - - 34 1381 CANVEST ENVIRONMENTAL PROTEC C 50% - - 35 0699 CAR INC B 70% - - 36 0293 CATHAY PACIFIC AIRWAYS A 90% - - 37 1375 CENTRAL CHINA SECURITIES C-H C 50% - - 38 1811 CGN NEW ENERGY HOLDINGS CO L C 50% - - 39 1816 CGN POWER CO LTD-H A 90% - - 40 2778 CHAMPION REIT B 70% - - 41 0951 CHAOWEI POWER HOLDINGS LTD C 50% - - * Company's margin limit for the counter has been fully utilized. -

Investment Daily

Investment Daily 31 March 2021 Major Market Indicators Market Overview 30 Mar 29 Mar 26 Mar Mkt. Turn.(mn) 169,300 190,300 183,900 Resistance at 20 Day SMA; Upcoming Focus will switch to macro Stock Advances 1,014 930 1,141 factor Stock Declines 719 824 628 Dow Jones Index hit new record. And China stock market rose. Hang Seng Index rose 239 HSI 28,578 28,338 28,336 points to 28,577 on Tuesday. H-share Index rose 77 points to 11,020. Tech Index rose 199 Change +239 +2 +437 points to 8,180. Market turnover was HK$169.3 billion. Health care sector performed well. HSI Turn.($bn) 66.52 78.36 76.55 Innovent Bio(1801) jumped 6.0% while JD Health(6618) surged 7.6%. Hong Kong HSCEI 11,021 10,943 10,966 property sector rose. SHK Property(16) gained 5.0% while New World Development(17) Change +78 -23 +222 advanced 5.2%. HSCEI Turn.($bn) 66.46 82.42 74.42 Consumer Confidence Index soared obviously in March and is much higher than expectation. President Biden will announce a sizable infrastructure investment plan on HSI Technical Indicators Wednesday. Together with progress on vaccination, it boosted the outlook for a broad economic recovery and rising inflation. 10-days MA 28,588 50-days MA 29,321 US stocks consolidated on Tuesday, with the three major US stock index fell 0.1-0.3% 250-days MA 25,901 respectively. On the other hand, 10 Year US treasury yield once rose to 1.77% but finally 14-days RSI 46.46 closed flat at 1.73%. -

Emerging Markets Core Equity Portfolio-Institutional Class As of July 31, 2021 (Updated Monthly) Source: State Street Holdings Are Subject to Change

Emerging Markets Core Equity Portfolio-Institutional Class As of July 31, 2021 (Updated Monthly) Source: State Street Holdings are subject to change. The information below represents the portfolio's holdings (excluding cash and cash equivalents) as of the date indicated, and may not be representative of the current or future investments of the portfolio. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. By viewing this listing of portfolio holdings, you are agreeing to not redistribute the information and to not misuse this information to the detriment of portfolio shareholders. Misuse of this information includes, but is not limited to, (i) purchasing or selling any securities listed in the portfolio holdings solely in reliance upon this information; (ii) trading against any of the portfolios or (iii) knowingly engaging in any trading practices that are damaging to Dimensional or one of the portfolios. Investors should consider the portfolio's investment objectives, risks, and charges and expenses, which are contained in the Prospectus. Investors should read it carefully before investing. Your use of this website signifies that you agree to follow and be bound by the terms -

2019 Public Supplier List

2019 Public Supplier List The list of suppliers includes original design manufacturers (ODMs), final assembly, and direct material suppliers. The volume and nature of business conducted with suppliers shifts as business needs change. This list represents a snapshot covering at least 95% of Dell’s spend during fiscal year 2020. Corporate Profile Address Dell Products / Supplier Type Sustainability Site GRI Procurement Category Compal 58 First Avenue, Alienware Notebook Final Assembly and/ Compal YES Comprehensive Free Trade Latitude Notebook or Original Design Zone, Kunshan, Jiangsu, Latitude Tablet Manufacturers People’s Republic Of China Mobile Precision Notebook XPS Notebook Poweredge Server Compal 8 Nandong Road, Pingzhen IoT Desktop Final Assembly and/ Compal YES District, Taoyuan, Taiwan IoT Embedded PC or Original Design Latitude Notebook Manufacturers Latitude Tablet Mobile Precision Notebook Compal 88, Sec. 1, Zongbao Inspiron Notebook Final Assembly and/ Compal YES Avenue, Chengdu Hi-tech Vostro Notebook or Original Design Comprehensive Bonded Zone, Manufacturers Shuangliu County, Chengdu, Sichuan, People’s Republic of China Public Supplier List 2019 | Published November 2020 | 01 of 40 Corporate Profile Address Dell Products / Supplier Type Sustainability Site GRI Procurement Category Dell 2366-2388 Jinshang Road, Alienware Desktop Final Assembly and/ Dell YES Information Guangdian, Inspiron Desktop or Original Design Xiamen, Fujian, People’s Optiplex All in One Manufacturers Republic of China Optiplex Desktop Precision Desktop -

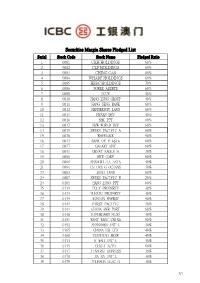

Securities Margin Shares Pledged List

Securities Margin Shares Pledged List Serial Stock Code Stock Name Pledged Ratio 1 0001 CKH HOLDINGS 60% 2 0002 CLP HOLDINGS 60% 3 0003 CHING GAS 60% 4 0004 WHARF HOLDINGS 60% 5 0005 HSBC HOLDINGS 70% 6 0006 POWER ASSETS 60% 7 0008 PCCW 40% 8 0010 HANG LUNG GROUP 40% 9 0011 HANG SENG BANK 60% 10 0012 HENDERSON LAND 60% 11 0014 HYSAN DEV 40% 12 0016 SHK PPT 60% 13 0017 NEW WORLD DEV 60% 14 0019 SWIRE PACIFIC A 60% 15 0020 WHEELOCK 50% 16 0023 BANK OF E ASIA 60% 17 0027 GALAXY ENT 60% 18 0041 GREAT EAGLE H 30% 19 0066 MTR CORP 60% 20 0069 SHANGRI-LA ASIA 40% 21 0081 CH OVS G OCEANS 30% 22 0083 SINO LAND 60% 23 0087 SWIRE PACIFIC B 20% 24 0101 HANG LUNG PPT 60% 25 0119 POLY PROPERTY 30% 26 0123 YUEXIU PROPERTY 40% 27 0135 KUNLUN ENERGY 50% 28 0142 FIRST PACIFIC 30% 29 0144 CHINA MER PORT 60% 30 0148 KINGBOARD HLDG 40% 31 0151 WANT WANT CHINA 50% 32 0152 SHENZHEN INT'L 30% 33 0165 CHINA EB LTD 40% 34 0168 TSINGTAO BREW 40% 35 0173 K WAH INT'L 30% 36 0175 GEELY AUTO 60% 37 0177 JIANGSU EXPRESS 30% 38 0178 SA SA INT'L 30% 39 0179 JOHNSON ELEC H 30% 1/7 Serial Stock Code Stock Name Pledged Ratio 40 0200 MELCO INT'L DEV 30% 41 0215 HUTCHTEL HK 20% 42 0220 U-PRESID CHINA 40% 43 0242 SHUN TAK HOLD 30% 44 0257 CHINA EB INT'L 40% 45 0267 CITIC 60% 46 0268 KINGDEE INT'L 20% 47 0270 GUANGDONG INV 40% 48 0272 SHUI ON LAND 30% 49 0285 BYD ELECTRONIC 30% 50 0288 WH GROUP 60% 51 0291 CHINA RES BEER 40% 52 0293 CATHAY PAC AIR 50% 53 0303 VTECH HOLDINGS 30% 54 0308 CHINA TRAVEL HK 30% 55 0315 SMARTONE TELE 20% 56 0322 TINGYI 50% 57 0323 MAANSHAN IRON 20% -

有限公司 BYD ELECTRONIC (INTERNATIONAL) COMPANY LIMITED (Incorporated in Hong Kong Under the Companies Ordinance with Limited Liability) (Stock Code: 285)

比亞迪電子(國際)有限公司 BYD ELECTRONIC (INTERNATIONAL) COMPANY LIMITED (incorporated in Hong Kong under the Companies Ordinance with limited liability) (Stock Code: 285) Form of proxy for use at the extraordinary general meeting (the “EGM”) to be held on Wednesday, 9 September 2020 (and at any adjournment thereof) I/We (Note 1) of , being the registered holder(s) of shares (Note 2) in the share capital of BYD Electronic (International) Company Limited (the “Company”) HEREBY APPOINT THE CHAIRMAN OF THE MEETING (Note 3),or of as my/our proxy to vote and act for me/us and on my/our behalf at the EGM (and any adjournment thereof) of the Company to be held at the conference room of BYD Company Limited, No. 3009, BYD Road, Pingshan District, Shenzhen, the People’s Republic of China at 10:00 a.m. on Wednesday, 9 September 2020 for the purposes of considering and, if thought fit, passing the resolution as set out in the notice convening the said meeting (the “Notice”) and as hereunder indicated, and, if no such indication is given, as my/our proxy thinks fit (Note 4). ORDINARY RESOLUTION FOR AGAINST To approve the Second Supplemental Agreement and the Proposed Annual Cap. Dated this day of 2020 Signed Notes: 1. name(s) and address(es) to be inserted in BLOCK CAPITALS. 2. Please insert the number of shares registered in your name(s). If no number is inserted, this form of proxy will be deemed to relate to all the shares in the capital of the Company registered in your name(s). -

BYD Electronic International

Asia Pacific Equity Research 28 February 2016 ▲ Overweight Previous: Neutral BYD Electronic International 0285.HK, 285 HK Resuming fast growth on strong orders and margin Price: HK$4.18 ▲ Price Target: HK$6.00 upticks; Upgrade to OW Previous: HK$4.30 We upgrade BYD-E to an OW rating with a new Dec-16 PT of HK$6.0 (9x China 2016 EPS, one notch higher). The debut of multiple flagship models at MWC Asian Technology 2016 adds to our conviction of metal casing adoption and we see volume upside AC Michael Fan from both Samsung and Chinese brands. We have raised our 2016 earnings (852) 2800-8541 forecasts by ~25% on stronger metal casing orders and margin upticks. We [email protected] expect the stock to further outperform in the next six to 12 months, driven by Bloomberg JPMA FAN <GO> near-term catalysts such as model launches at key customers, upward revisions J.P. Morgan Securities (Asia Pacific) Limited to Street estimates and strong 1H16 earnings (JPMe 60%+ YoY), along with Gokul Hariharan AC long-term re-rating opportunities in auto electronics. (852) 2800-8564 Stronger metal casing orders with more balanced customer mix: Our [email protected] research shows that BYD-E is seeing: 1) stable metal casing allocation from Bloomberg JPMA HARIHARAN <GO> Samsung S7 and volume upside from A-Series, 2) increased share allocation J.P. Morgan Securities (Asia Pacific) Limited from existing customers (such as Huawei), and 3) customer wins among JJ Park both foreign and domestic brands. We believe BYD-E could penetrate (82-2) 758-5717 [email protected] almost half of the flagship models launched by major Android brands and J.P.