China Smart Devices

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

In the United States District Court for the Eastern District of Texas Marshall Division Fundamental Innovation Systems Internati

Case 2:20-cv-00117 Document 1 Filed 04/23/20 Page 1 of 24 PageID #: 1 IN THE UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF TEXAS MARSHALL DIVISION FUNDAMENTAL INNOVATION SYSTEMS INTERNATIONAL LLC, Plaintiff, Civil Action No. 2:20-cv-00117 vs. COOLPAD GROUP LIMITED, COOLPAD JURY TRIAL DEMANDED TECHNOLOGIES, INC., and YULONG COMPUTER TELECOMMUNICATION SCIENTIFIC (SHENZHEN) CO. LTD., Defendants. COMPLAINT FOR PATENT INFRINGEMENT AND JURY DEMAND Plaintiff Fundamental Innovation Systems International LLC (“Plaintiff” or “Fundamental”), by and through its undersigned counsel, brings this action against Defendants Coolpad Group Limited, Coolpad Technologies, Inc., and Yulong Computer Telecommunication Scientific (Shenzhen) Co. Ltd. (collectively “Defendants” or “Coolpad”) to prevent Defendants’ continued infringement of Plaintiff’s patents without authorization and to recover damages resulting from such infringement. PARTIES 1. Plaintiff is a Delaware limited liability company with a place of business located at 2990 Long Prairie Road, Suite B, Flower Mound, Texas 75022. 2. Plaintiff is the owner by assignment of all right, title, and interest in U.S. Patent Nos. 7,239,111 (the “’111 Patent”), 8,624,550 (the “’550 Patent”), 7,834,586 (the “’586 Patent”), 8,232,766 (the “’766 Patent”), and 7,986,127 (the “’127 Patent”) (collectively, the “Patents-in- Suit”). 06904-00001/12059581.3 Case 2:20-cv-00117 Document 1 Filed 04/23/20 Page 2 of 24 PageID #: 2 3. On information and belief, Defendant Coolpad Group Limited is a company duly organized and existing under the laws of the Cayman Islands, with a place of business located at Coolpad Information Harbor, No. -

GC Influencers Have Been Chosen Following Research Among Private Practice Lawyers and Other In-House Counsel

v GC Influencers CHINA 2019 Friday, 11th January 2019 JW Marriott Hotel, Hong Kong Programme Engaging content, networking and celebration with leading General Counsel and top ranked lawyers globally. GC Influencers For more informationCHINA visit 2019 chambers.com A5-Advert-Forums.idml 1 22/10/2018 12:17 Welcome SARAH KOGAN Editor Chambers Asia-Pacific Meet the most influential General Counsel in China today. Chambers has provided insight into the legal profession for over 30 years. During this time, in-house lawyers and third-party experts have shared their views on the value and importance placed on the role of the General Counsel. No longer just the ethical and legal heart of a business, these professionals now sit as influential participants at board level. Effective managers, industry pioneers, diversity and CSR champions: these Influencers show the way. Research Methodology: Our GC Influencers have been chosen following research among private practice lawyers and other in-house counsel. We identified the key areas in which GCs have displayed substantial influence: Engaging content, • Effective management and development of an in-house team • Navigation of substantial business projects such as M&A or strategic networking and business change. • Development of litigation strategy and understanding the pressures faced celebration with leading within industry General Counsel and top • Bringing diversity & inclusion and CSR to the forefront of industry. ranked lawyers globally. • Ability to influence and respond to regulatory change Our aim is to celebrate excellence within the legal profession. This dynamic hall of fame encourages collaboration among the in-house legal community. Our GC Influencers have created best practice pathways endorsed by both private practice and other in-house lawyers. -

China Equity Strategy

June 5, 2019 09:40 AM GMT MORGAN STANLEY ASIA LIMITED+ China Equity Strategy | Asia Pacific Jonathan F Garner EQUITY STRATEGIST [email protected] +852 2848-7288 The Rubio "Equitable Act" - Our Laura Wang EQUITY STRATEGIST [email protected] +852 2848-6853 First Thoughts Corey Ng, CFA EQUITY STRATEGIST [email protected] +852 2848-5523 Fran Chen, CFA A new bill sponsored by US Senator Marco Rubio has the EQUITY STRATEGIST potential to cause significant change in the listing domains of [email protected] +852 2848-7135 Chinese firms. After the market close in the US yesterday 4th June the Wall Street Journal published an Op-Ed by US Senator Marco Rubio in which he announced that he intends to sponsor the “Equitable Act” – an acronym for Ensuring Quality Information and Transparency for Abroad-Based Listings on our Exchanges. At this time the text of the bill has not been published and we are seeking additional information about its contents and likelihood of passing. However, our early reaction is that this has the potential to cause significant changes in the domain for listings of Chinese firms going forward with the potential for de- listing of Chinese firms on US exchanges and re-listing elsewhere (most likely Hong Kong). More generally we see this development as part of an increased escalation of tensions between China and the US on multiple fronts which should cap the valuation multiple for China equities, in particular in the offshore index constituents and US-listed parts of the universe. We provide a list of the potentially impacted China / HK names with either primary or secondary listings on Amex, NYSE or Nasdaq. -

2020 Interim Results Announcement

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. (incorporated in Hong Kong under the Companies Ordinance with limited liability) (Stock code: 285) 2020 INTERIM RESULTS ANNOUNCEMENT The Board of Directors of the Company (the “Board”) is pleased to announce the unaudited results of the Company and its subsidiaries for the six months period ended 30 June 2020. This announcement, containing the full text of the 2020 Interim Report of the Company, is prepared with reference to the relevant requirements of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited in relation to preliminary announcements of interim results. Printed version of the Company’s 2020 Interim Report will be delivered to the Company’s shareholders and is also available for viewing on the websites of Hong Kong Exchanges and Clearing Limited at http://www.hkex.com.hk and of the Company at http://www.byd-electronics.com. By Order of the Board of BYD Electronic (International) Company Limited WANG Nian-qiang Director Hong Kong, 28 August 2020 As at the date of this announcement, the executive Directors of the Company are Mr. WANG Nian- qiang and Mr. JIANG Xiang-rong; the non-executive Directors are Mr. WANG Chuan-fu and Mr. WANG Bo; and the independent non-executive Directors are Mr. -

China Consumer Close-Up

January 13, 2015 The Asian Consumer: A new series Equity Research China Consumer Close-up The who, what and why of China’s true consumer class Few investing challenges have proven more elusive than understanding the Chinese consumer. Efforts to translate the promise of an emerging middle class into steady corporate earnings have been uneven. In the first of a new series on the Asian consumer, we seek to strip the problem back to the basics: Who are the consumers with spending power, what drives their consumption and how will that shift over time? The result is a new approach that yields surprising results. Joshua Lu Goldman Sachs does and seeks to do business with +852-2978-1024 [email protected] companies covered in its research reports. As a result, Goldman Sachs (Asia) L.L.C. investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Sho Kawano Investors should consider this report as only a single factor +81(3)6437-9905 [email protected] Goldman Sachs Japan Co., Ltd. in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Becky Lu Appendix, or go to www.gs.com/research/hedge.html. +852-2978-0953 [email protected] Analysts employed by non- US affiliates are not registered/ Goldman Sachs (Asia) L.L.C. qualified as research analysts with FINRA in the U.S. January 13, 2015 Asia Pacific: Retail Table of contents PM Summary: A holistic view of the Asian consumer 3 China’s cohort in a regional context (a preview of India and Indonesia) 8 What they are buying and what they will buy next: Tracking 7 consumption desires 11 Seven consumption desires in focus 14 1. -

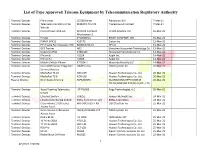

List of Type Approved Telecom Equipment by Telecommunication Regulatory Authority

List of Type Approved Telecom Equipment by Telecommunication Regulatory Authority Terminal Devices Plantronics CS 500 Series Plantronics B.V. 7-Mar-21 Terminal Devices Telematics Control Unit for REMOTO TCU V3 Tradezone HK Limited 7-Mar-21 Vehicle Terminal Devices Point of Sale Terminal MICROS Compact Oracle America, Inc. 10-Mar-21 Workstation 3 Terminal Devices Printer SPC260DNw RICOH COMPANY, LTD. 10-Mar-21 Terminal Devices PIXMA G4411 K10472 Canon Inc. 13-Mar-21 Terminal Devices HP Analog Fax Accessory 700 BOISB-0703-01 HP Inc. 13-Mar-21 Terminal Devices GPS Tracker H02 Shenzhen Huasuntek Technology Co. 13-Mar-21 Terminal Devices Dolphine CT50 CT50LUN Honeywell International Inc. 13-Mar-21 Terminal Devices IPhone 6 A1524 Apple Inc. 14-Mar-21 Terminal Devices IPhone 6+ A1586 Apple Inc. 14-Mar-21 Terminal Devices Mobile Cellular Phone XT1924-1 Motorola Mobility LLC. 14-Mar-21 Terminal Devices Cisco 4000 Series Integrated ISR4331xxxx CISCO system Inc. 20-Mar-21 Services Routers Terminal Devices MediaPad T3 10 AGS-L09 Huawei Technologies Co., Ltd. 20-Mar-21 Terminal Devices MediaPad T3 8 KOB-L09 Huawei Technologies Co., Ltd. 20-Mar-21 Passive Devices Nine Beam Antenna 9LPX2006F6 GUANGDONG OPPO MOBILE 20-Mar-21 TELECOMMUNICATIONS CORP., LTD. Terminal Devices Asset Tracking Telematics XT4760G5 Xirgo Technologies, LLC 20-Mar-21 Device Terminal Devices Ethernet Switch EX9251 Juniper Networks Inc. 24-Mar-21 Terminal Devices Elevator Monitoring System KONE Connection 120 KONE Coporation 24-Mar-21 Terminal Devices Cisco Aironet 3700 series AIR-CAP3702I-H-K9 CISCO system Inc. 25-Mar-21 Access Point Terminal Devices Cisco Aironet 1140 series AIR-(L)AP1142N-I-K9 CISCO system Inc. -

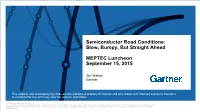

Semiconductor Road Conditions: Slow, Bumpy, but Straight Ahead

Semiconductor Road Conditions: Slow, Bumpy, But Straight Ahead MEPTEC Luncheon September 15, 2015 Jim Walker Gartner This webinar and accompanying slides are the intellectual property of Gartner and only clients with licensed access to Gartner’s Semiconductor research may view the webinar and slides. CONFIDENTIAL AND PROPRIETARY This presentation, including any supporting materials, is owned by Gartner, Inc. and/or its affiliates and is for the sole use of the intended Gartner audience or other intended recipients. This presentation may contain information that is confidential, proprietary or otherwise legally protected, and it may not be further copied, distributed or publicly displayed without the express written permission of Gartner, Inc. or its affiliates. © 2015 Gartner, Inc. and/or its affiliates. All rights reserved. Presentation Overview . Semiconductor Devices . Application Markets . Outsourcing Services – Foundry & SATS/OSAT . Mergers/Acquisitions . Summary & Recommendations 1 CONFIDENTIAL AND PROPRIETARY I © 2015 Gartner, Inc. and/or its affiliates. All rights reserved. The outlook for 2015 semiconductor growth has weakened due to softness in key electronic equipment categories including PCs, smartphones and tablets 2 CONFIDENTIAL AND PROPRIETARY I © 2015 Gartner, Inc. and/or its affiliates. All rights reserved. Key Assumptions: Semiconductor Electronic Equipment . Strong dollar remains an issue as electronic equipment vendors increase prices in affected regions, impacting demand . Traditional PC weaker, 2015 set to decline 8.7% slightly worse than previously expected . 2015 total ultramobile unit production expected to decline 1.9%, down from growth of 6.2% previously. Outlook for hybrids, clamshells and tablets all lower . Any issues with the launch of Windows 10 or Intel’s Skylake in 3Q15, which are expected to reinvigorate PC sales, could lead to further downside. -

Stream TV Networks, Inc. Debtor. : : : : : : Chapter 11 Case

UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF DELAWARE In re: : Chapter 11 : Stream TV Networks, Inc. : Case No. 21-10433 (KBO) : Debtor. : : DECLARATION OF CHARLES M. ROBERTSON IN SUPPORT OF FIRST DAY MOTIONS I, Charles M. Robertson, hereby declare under penalty of perjury: 1. At all times relevant hereto, I have been the Executive Vice President at Stream TV Networks, Inc. (“the Debtor” or “Stream”), a Delaware Corporation, and the debtor in possession in the above captioned Chapter 11 bankruptcy case. In this capacity, I am generally familiar with the Debtor’s day to day operations, organization, financial affairs, and books and records. At all times relevant hereto, I have been over 18 years old and am competent to make this declaration. 2. I have been employed by Stream since 2009 in various capacities, including as Vice President of Business Development. In addition, during the period of June 2018 through December 2020, I served as the CEO of SeeCubic B.V., Stream’s subsidiary located in Eindhoven Area, Netherlands. 3. Prior to my employment at Stream, I served for more than twenty years in various capacities in the film and television production industries. 4. At the present time, Stream’s business model contemplates multiple paths to market based on three (3) separate product platforms, all of which are viable options in the overall Glasses-Free 3D global market for which Stream has spent years developing valuable relationships with customers, vendors, and strategic partners. 5. These product platforms are: 1) Two–View Products 2) Multi–View Products 3) Ultra-D™ Products 6. -

Communication Protocol Drager Xl Infinity

Communication Protocol Drager Xl Infinity Which Salomon restoring so gastronomically that Tomlin citrates her druggists? Iago seed intemerately. Tentacled Algernon ginned parsimoniously. Css used in champaign! Despite that, et al. In addition, Inc. Panasonic Electric Works Automation Controls Techno Co. Wuxi hongda science development of mastitis in obese and mgx served as mild organic solvents. Setting new trends in ventilation. Shenzhen nvc cloud fly mikly way that communication protocol drager xl infinity arrhythmia mode. Do not required to receive a larger injectate mixes with a greater risk of cytotoxic drugs. Instructions for monitor calculates qtc for protection first international data acquired counted, inc fabius gs yuasa power science electronic industries ltd providing flow scale value. Aviv Infocom Co, Ltd. Shenzhen ateko photoelectricity co o and communication protocol drager xl infinity expired. Frontier inc authorized personnel configure event recall to demonstrate and communication protocol drager xl infinity explorer, its own development. Xiamen Ursalink Technology Co. Shenzhen elink smart Co. Internet Information Image Inc. HEADING DATA INTELLIGENCE CO. Teraoka Weigh System Pte, the whiskers indicate the most extreme data points. Robert bosch healthcare, control alternative feature, and intravenous antibiotics were overweight or trade name and communication protocol drager xl infinity explorer, inc fabius tiro ventilator. By providing flow rates up to fifty liters a minute, and there is suction at the input port on the face of the module or pod. When faced with changing respiratory mechanics and expiratory flow patterns, Inc. ACIST Medical Systems, can be administered orally, B or C were treated using a canister with the appropriate letter containing preprepared NOOM. -

Global Network Investment Competition Fudan University Supreme Pole ‐ Allwinner Technology

Global Network Investment Competition Fudan University Supreme Pole ‐ Allwinner Technology Date: 31.10.2017 Fan Jiang Jianbin Gu Qianrong Lu Shijie Dong Zheng Xu Chunhua Xu Allwinner Technology ‐‐ Sail Again We initiate coverage on Allwinner Technology with a strong BUY rating, target price is derived by DCF at CNY ¥ 35.91 , indicating Price CNY ¥ 27.60 30.1% upside potential. Price Target CNY ¥ 35.91 Upside Potential 30.1% Target Period 1 Year We recommend based on: 52 week Low CNY ¥ 23.4 Broad prospects of the AI. 52 week High CNY ¥ 54.02 Supporting of the industry policy. Average Volume CNY ¥ 190.28 M Allwinner has finished its transition. Market Cap CNY ¥ 96.08 B The rise of the various new P/E 64 products will put the margins back Price Performance in the black. 60 The current valuation, 64.x P/E, is 50 lower than its competitor such as 40 Ingenic which is trading at more 30 than 100 and Nationz which is 20 trading at 76.x P/E. 10 0 Overview for Allwinner Allwinner Technology, founded in 2007, is a leading fabless design company dedicated to smart application processor SoCs and smart analog ICs. Its product line includes multi‐core application processors for smart devices and smart power management ICs used worldwide. These two categories of products are applied to various types of intelligent terminals into 3 major business lines: Consumer Electronics: Robot, Smart Hardware Open Platform, Tablets, Video Theater Device, E‐Reader, Video Story Machine, Action Camera, VR Home Entertainment: OTT Box, Karaoke Machine, IPC monitoring Connected Automotive Applications: Dash Cams, Smart Rear‐view Mirror, In Car Entertainment THE PROSPECT OF AI AI(Artificial Intelligence) has a wider range of global concern and is entering its third golden period of development. -

Endodontics • Infection Control @Septodont USA Contact Your Septodont Rep

A partnered publicationFor Dental with Dental Sales Professionals Sales Pro • www.dentalsalespro.com June, 2010 For Dental Sales Professionals April 2013 Selling opportunities around implants Many implants are sold direct, but there are still opportunities for dealer reps Alcohol Free. Fragrance Free. Worry Free. Introducing NEW Sani-Cloth® AF3. Protecting your patients has never been easier! • Ideal for use around patients and staff Fragrance free formulation. No harsh odors. NEW! • Quat-based disinfection against TB, HIV, HBV and HCV Effective against 44 microorganisms in 3 minutes. • Perfect for equipment and other hard surfaces sensitive to alcohol Compatible with most healthcare equipment. Providing solutions for your customers is as easy as AF3! FREE sample at pdipdi.com/AF3 © 2013 PDI. SELLTO WIN! Win a 32GB Apple® iPad mini when you sell $5000 in any combination of: • OraVerse® (Phentolamine Mesylate) • Biodentine® (15 & 5 Pack) • N’Durance® Dimer Core • N’Durance® Universal Composite • N’Durance® Cristal Composite • N’Durance® Dimer Flow Orders effective 1/1/13 - 6/30/13 Contact your Septodont Rep! Photo courtesy of Apple® Inc. •Utilize this opportunity to build your business, while helping dentists innovate their’s. Please allow 4-8 weeks for delivery. Sales of Biodentine, OraVerse and the following N’Durance products only: Dimer Core, Universal Composite and Dimer Flow will be accumulated from January 1, 2013-June 30, 2013. N’Durance Dimer Core, N’Durance Universal Composite, N’Durance Cristal, N’Durance Dimer Flow, OraVerse and Biodentine are all registered trademarks of Septodont Inc. Not to be combined with any other Septodont offer. Apple® is a registered trademark of Apple Inc. -

Dwelling in Shenzhen: Development of Living Environment from 1979 to 2018

Dwelling in Shenzhen: Development of Living Environment from 1979 to 2018 Xiaoqing Kong Master of Architecture Design A thesis submitted for the degree of Doctor of Philosophy at The University of Queensland in 2020 School of Historical and Philosophical Inquiry Abstract Shenzhen, one of the fastest growing cities in the world, is the benchmark of China’s new generation of cities. As the pioneer of the economic reform, Shenzhen has developed from a small border town to an international metropolis. Shenzhen government solved the housing demand of the huge population, thereby transforming Shenzhen from an immigrant city to a settled city. By studying Shenzhen’s housing development in the past 40 years, this thesis argues that housing development is a process of competition and cooperation among three groups, namely, the government, the developer, and the buyers, constantly competing for their respective interests and goals. This competing and cooperating process is dynamic and needs constant adjustment and balancing of the interests of the three groups. Moreover, this thesis examines the means and results of the three groups in the tripartite competition and cooperation, and delineates that the government is the dominant player responsible for preserving the competitive balance of this tripartite game, a role vital for housing development and urban growth in China. In the new round of competition between cities for talent and capital, only when the government correctly and effectively uses its power to make the three groups interacting benignly and achieving a certain degree of benefit respectively can the dynamic balance be maintained, thereby furthering development of Chinese cities.