China Consumer Close-Up

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Joint Action Against Online Video Piracy in China

November 13, 2013 Joint Action Against Online Video Piracy in China Lawsuits Seeking RMB300 Million in Damages Filed Against Baidu and QVOD on Claims of Spreading Pirated Videos and Engaging in Hotlinking BEIJING, Nov. 13, 2013 /PRNewswire/ -- Youku Tudou, Sohu Video, Tencent Video, LeTV, MPA, the Motion Picture Association of America (MPAA), CODA, Wanda Films, Enlight Media, Letv Films announce a joint declaration today in Beijing to fight online video infringement and piracy both on PC and mobile Internet in China. Meanwhile, the joint action announces legal action has been taken against Baidu and QVOD for compensation as high as RMB300 million. Representatives from more than a dozen Chinese and international film and television production companies attended the joint action announcement in Beijing. International attendees included the Motion Picture Association of America, Sony Pictures Entertainment, Warner Brothers, Disney and Paramount. Chinese attendees included the Capital Copyright Industry Alliance Capital Protection Division, the China Radio and Television Association of the Television Production Committee, and many Chinese production companies. "Since 2009, the video industry is facing a more severe anti-piracy situation," Sohu Group Chairman and CEO Charles Zhang said. "Especially when those big Internet companies with resource advantages participate in large-scale piracy. We cannot keep competing because where thieves and robbers are having their way, law-abiding companies cannot survive. We may even have to exit online video industry if such practices continue. Nobody will invest in content, and China's online video industry will face the sad situation as the music industry, which has already been destroyed by piracy, had faced before. -

Internet Economy 25 Years After .Com

THE INTERNET ECONOMY 25 YEARS AFTER .COM TRANSFORMING COMMERCE & LIFE March 2010 25Robert D. Atkinson, Stephen J. Ezell, Scott M. Andes, Daniel D. Castro, and Richard Bennett THE INTERNET ECONOMY 25 YEARS AFTER .COM TRANSFORMING COMMERCE & LIFE March 2010 Robert D. Atkinson, Stephen J. Ezell, Scott M. Andes, Daniel D. Castro, and Richard Bennett The Information Technology & Innovation Foundation I Ac KNOW L EDGEMEN T S The authors would like to thank the following individuals for providing input to the report: Monique Martineau, Lisa Mendelow, and Stephen Norton. Any errors or omissions are the authors’ alone. ABOUT THE AUTHORS Dr. Robert D. Atkinson is President of the Information Technology and Innovation Foundation. Stephen J. Ezell is a Senior Analyst at the Information Technology and Innovation Foundation. Scott M. Andes is a Research Analyst at the Information Technology and Innovation Foundation. Daniel D. Castro is a Senior Analyst at the Information Technology and Innovation Foundation. Richard Bennett is a Research Fellow at the Information Technology and Innovation Foundation. ABOUT THE INFORMATION TECHNOLOGY AND INNOVATION FOUNDATION The Information Technology and Innovation Foundation (ITIF) is a Washington, DC-based think tank at the cutting edge of designing innovation policies and exploring how advances in technology will create new economic opportunities to improve the quality of life. Non-profit, and non-partisan, we offer pragmatic ideas that break free of economic philosophies born in eras long before the first punch card computer and well before the rise of modern China and pervasive globalization. ITIF, founded in 2006, is dedicated to conceiving and promoting the new ways of thinking about technology-driven productivity, competitiveness, and globalization that the 21st century demands. -

Birth and Evolution of Korean Reality Show Formats

Georgia State University ScholarWorks @ Georgia State University Film, Media & Theatre Dissertations School of Film, Media & Theatre Spring 5-6-2019 Dynamics of a Periphery TV Industry: Birth and Evolution of Korean Reality Show Formats Soo keung Jung [email protected] Follow this and additional works at: https://scholarworks.gsu.edu/fmt_dissertations Recommended Citation Jung, Soo keung, "Dynamics of a Periphery TV Industry: Birth and Evolution of Korean Reality Show Formats." Dissertation, Georgia State University, 2019. https://scholarworks.gsu.edu/fmt_dissertations/7 This Dissertation is brought to you for free and open access by the School of Film, Media & Theatre at ScholarWorks @ Georgia State University. It has been accepted for inclusion in Film, Media & Theatre Dissertations by an authorized administrator of ScholarWorks @ Georgia State University. For more information, please contact [email protected]. DYNAMICS OF A PERIPHERY TV INDUSTRY: BIRTH AND EVOLUTION OF KOREAN REALITY SHOW FORMATS by SOOKEUNG JUNG Under the Direction of Ethan Tussey and Sharon Shahaf, PhD ABSTRACT Television format, a tradable program package, has allowed Korean television the new opportunity to be recognized globally. The booming transnational production of Korean reality formats have transformed the production culture, aesthetics and structure of the local television. This study, using a historical and practical approach to the evolution of the Korean reality formats, examines the dynamic relations between producer, industry and text in the -

Average Net Worth of Billionaires by Country: 2013 Hurun Rich List

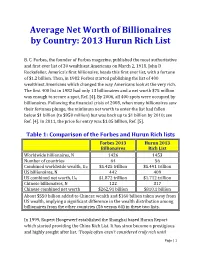

Average Net Worth of Billionaires by Country: 2013 Hurun Rich List B. C. Forbes, the founder of Forbes magazine, published the most authoritative and first ever list of 30 wealthiest Americans on March 2, 1918. John D Rockefeller, America’s first billionaire, heads this first ever list, with a fortune of $1.2 billion. Then, in 1982 Forbes started publishing the list of 400 wealthiest Americans which changed the way Americans look at the very rich. The first 400 list in 1982 had only 13 billionaires and a net worth $75 million was enough to secure a spot, Ref. [4]. By 2006, all 400 spots were occupied by billionaires. Following the financial crisis of 2008, when many billionaires saw their fortunes plunge, the minimum net worth to enter the list had fallen below $1 billion (to $950 million) but was back up to $1 billion by 2010; see Ref. [4]. In 2011, the price for entry was $1.05 billion, Ref. [5]. Table 1: Comparison of the Forbes and Hurun Rich lists Forbes 2013 Hurun 2013 Billionaires Rich List Worldwide billionaires, N 1426 1453 Number of countries 64 56 Combined worldwide wealth, UN $5.425 trillion $5.491 trillion US billionaires, N 442 409 US combined net worth, UN $1.872 trillion $1.712 trillion Chinese billionaires, N 122 317 Chinese combined net worth $262.91 billion $810.1 billion About $550 billion added to Chinese wealth and $160 billion taken away from US wealth, implying a significant difference in the wealth distribution among billionaires from the other countries (56 versus 64) in these two lists. -

In the United States District Court for the Eastern District of Texas Marshall Division Fundamental Innovation Systems Internati

Case 2:20-cv-00117 Document 1 Filed 04/23/20 Page 1 of 24 PageID #: 1 IN THE UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF TEXAS MARSHALL DIVISION FUNDAMENTAL INNOVATION SYSTEMS INTERNATIONAL LLC, Plaintiff, Civil Action No. 2:20-cv-00117 vs. COOLPAD GROUP LIMITED, COOLPAD JURY TRIAL DEMANDED TECHNOLOGIES, INC., and YULONG COMPUTER TELECOMMUNICATION SCIENTIFIC (SHENZHEN) CO. LTD., Defendants. COMPLAINT FOR PATENT INFRINGEMENT AND JURY DEMAND Plaintiff Fundamental Innovation Systems International LLC (“Plaintiff” or “Fundamental”), by and through its undersigned counsel, brings this action against Defendants Coolpad Group Limited, Coolpad Technologies, Inc., and Yulong Computer Telecommunication Scientific (Shenzhen) Co. Ltd. (collectively “Defendants” or “Coolpad”) to prevent Defendants’ continued infringement of Plaintiff’s patents without authorization and to recover damages resulting from such infringement. PARTIES 1. Plaintiff is a Delaware limited liability company with a place of business located at 2990 Long Prairie Road, Suite B, Flower Mound, Texas 75022. 2. Plaintiff is the owner by assignment of all right, title, and interest in U.S. Patent Nos. 7,239,111 (the “’111 Patent”), 8,624,550 (the “’550 Patent”), 7,834,586 (the “’586 Patent”), 8,232,766 (the “’766 Patent”), and 7,986,127 (the “’127 Patent”) (collectively, the “Patents-in- Suit”). 06904-00001/12059581.3 Case 2:20-cv-00117 Document 1 Filed 04/23/20 Page 2 of 24 PageID #: 2 3. On information and belief, Defendant Coolpad Group Limited is a company duly organized and existing under the laws of the Cayman Islands, with a place of business located at Coolpad Information Harbor, No. -

GC Influencers Have Been Chosen Following Research Among Private Practice Lawyers and Other In-House Counsel

v GC Influencers CHINA 2019 Friday, 11th January 2019 JW Marriott Hotel, Hong Kong Programme Engaging content, networking and celebration with leading General Counsel and top ranked lawyers globally. GC Influencers For more informationCHINA visit 2019 chambers.com A5-Advert-Forums.idml 1 22/10/2018 12:17 Welcome SARAH KOGAN Editor Chambers Asia-Pacific Meet the most influential General Counsel in China today. Chambers has provided insight into the legal profession for over 30 years. During this time, in-house lawyers and third-party experts have shared their views on the value and importance placed on the role of the General Counsel. No longer just the ethical and legal heart of a business, these professionals now sit as influential participants at board level. Effective managers, industry pioneers, diversity and CSR champions: these Influencers show the way. Research Methodology: Our GC Influencers have been chosen following research among private practice lawyers and other in-house counsel. We identified the key areas in which GCs have displayed substantial influence: Engaging content, • Effective management and development of an in-house team • Navigation of substantial business projects such as M&A or strategic networking and business change. • Development of litigation strategy and understanding the pressures faced celebration with leading within industry General Counsel and top • Bringing diversity & inclusion and CSR to the forefront of industry. ranked lawyers globally. • Ability to influence and respond to regulatory change Our aim is to celebrate excellence within the legal profession. This dynamic hall of fame encourages collaboration among the in-house legal community. Our GC Influencers have created best practice pathways endorsed by both private practice and other in-house lawyers. -

From Western TV Sets to Chinese Online Streaming Services: English-Language TV Series in Mainland China

. Volume 16, Issue 2 November 2019 From Western TV sets to Chinese online streaming services: English-language TV series in mainland China Xiaoran Zhang, University of Nottingham, UK Abstract: In the age of multiple screens, online streaming has in the 2010s become the most significant way of consuming overseas television programs in Mainland China. Due to rather strict government policy and censorship, foreign television series are presently only legally distributed and circulated on licensed online streaming services. Focusing on the streaming of US/UK TV series, this paper examines online streaming services’ distribution activities in order to understand both streaming websites’ business practices surrounding transnational TV and the features they employ to cater to online audiences for these series. To grasp how the online distribution of English-language TV series operates in China, I begin by looking at China’s five major video streaming services, analyzing the design of their interfaces, scheduling of programs, and accessibility for different tiers of users. I then examine how streaming services use social media as a major tool to promote their US and UK TV series. Through this analysis, I argue that transnational TV flow has had to be localized to achieve distribution and marketing goals in a Chinese context, resulting in the uniqueness of these streaming practices. This article concludes that, with the development of online streaming technologies, distinctive modes of audience consumption in China have informed the localization of this specific transnational TV content. Keywords: Online streaming, streaming consumption, television distribution, transnational TV, Tencent Video, HBO, Game of Thrones Introduction As one of HBO’s most successful high-end shows, Game of Thrones (2011-) has earned a worldwide reputation that includes the fandom of Chinese viewers. -

Critical Masses, Commerce, and Shifting State-Society Relations in China" (2010)

University of Nebraska - Lincoln DigitalCommons@University of Nebraska - Lincoln The hinC a Beat Blog Archive 2008-2012 China Beat Archive 2010 Critical Masses, Commerce, and Shifting State- Society Relations in China Ying Zhu University of New York, College of Staten Island Follow this and additional works at: https://digitalcommons.unl.edu/chinabeatarchive Part of the Asian History Commons, Asian Studies Commons, Chinese Studies Commons, and the International Relations Commons Zhu, Ying, "Critical Masses, Commerce, and Shifting State-Society Relations in China" (2010). The China Beat Blog Archive 2008-2012. 710. https://digitalcommons.unl.edu/chinabeatarchive/710 This Article is brought to you for free and open access by the China Beat Archive at DigitalCommons@University of Nebraska - Lincoln. It has been accepted for inclusion in The hinC a Beat Blog Archive 2008-2012 by an authorized administrator of DigitalCommons@University of Nebraska - Lincoln. Critical Masses, Commerce, and Shifting State-Society Relations in China February 17, 2010 in Media, movies by The China Beat | 4 comments This essay is based on the script of a talk Ying Zhu gave at Google’s New York offices on February 12, 2010. Sections in bold were not part of the original talk, but have been added by the authors to tease out some of the issues that were left without further elaboration due to time constraints. By Ying Zhu and Bruce Robinson Editor’s note: This piece originally ran with Ying Zhu listed as its sole author. After it appeared, Ying Zhu informed us that it should be described as a co-authored commentary, in recognition of the extraordinary contribution to it by Bruce Robinson, with whom she had collaborated closely on a related project; we have followed her wishes; and both Ying Zhu and China Beat ask that in further attributions or discussion both authors be equally credited for this work. -

China Chuanglian Education Financial Group Limited 中國創聯教育金融集團有限公司

China Chuanglian Education Financial Group Limited 中國創聯教育金融集團有限公司 年報 Annual Report 2017 2017 A N N U A L R E P O R T 2 0 17 中國創聯教育金融集團有限公司 年報 China Chuanglian Education Financial Group Limited (前稱「中國創聯教育集團有限公司」) (formerly known as “China Chuanglian Education Group Limited”) (於開曼群島註冊成立之有限公司 ) (incorporated in the Cayman Islands with limited liability) (股份代號:2371) (Stock Code: 2371) Page Contents Corporate Information 2 Financial Summary 3 Chairman’s Statement 4 Management Discussion and Analysis 7 Biographical Details of Directors and Senior Management 20 Corporate Governance Report 23 Environmental, Social and Governance Report 35 Report of the Directors 47 Independent Auditor’s Report 61 Consolidated Statement of Profit or Loss and 68 Other Comprehensive Income Consolidated Statement of Financial Position 70 Consolidated Statement of Changes in Equity 72 Consolidated Statement of Cash Flows 74 Notes to the Consolidated Financial Statements 76 Corporate Information Executive Directors Principal Bankers Mr. LU Xing (Chairman of the Board) Citibank, N.A. Mr. LI Jia Mr. WU Xiaodong Registered Office Mr. WANG Cheng Cricket Square Mr. LI Dongfu Hutchins Drive P.O. Box 2681 Independent Non-executive Directors Grand Cayman KY1-1111 Mr. LEUNG Siu Kee Cayman Islands Mr. WU Yalin Ms. WANG Shuping Principal Place of Business in Hong Kong Room 905–06, 9/F., Company Secretary China Evergrande Centre Mr. SUNG Chi Keung 38 Gloucester Road Wanchai, Hong Kong Audit Committee Principal Share Registrar and Transfer Office Mr. LEUNG Siu Kee (Chairman of the Audit Committee) SMP Partners (Cayman) Limited Mr. WU Yalin Royal Bank House — 3rd Floor Ms. WANG Shuping 24 Shedden Road P.O. -

The Chinese Luxury Traveller 2018 Executive Summary

VIEW from ILTM REPORT THE CHINESE LUXURY TRAVELLER 2018 EXECUTIVE SUMMARY Photo by Yiran Ding VIEW from ILTM REPORT FOREWORD The Hurun Research Institute and ILTM China have joined forces to release The Chinese Luxury Traveller 2018 for the eight successive year. The report is based on deep research into travel preferences and consumption among Chinese high-end travellers, and the trends expected to arise in future. The data behind the research are global high-end travel industry leader, drawn from the Chinese Luxury for the twelfth successive year, and Travel and Lifestyle Survey 2018, a that we have collaborated to release cooperative venture between Hurun the Chinese Luxury Traveller for the Report and four travel agencies, past eight years, to explore the trends namely DIADEMA, MAGIC TRAVEL, and trajectories of the high-end ZANADU and 8 Continents. travel market.” The quantitative survey encompasses ILTM China Event Manager Andy data from 236 respondents hailing Ventris added, “ILTM China has been from 43 cities nationwide, including created as a platform for the most first-tier cities such as Beijing, valuable luxury travel advisors from Shanghai, Guangzhou and Shenzhen, across China to meet with the world’s and second- and third-tier cities such very best luxury travel providers. We as Xi’an, Qingdao, Hangzhou, Nanjing, are delighted to once again partner Nanchang, Qingdao, Dalian and with Hurun Report, who are a leading Suzhou. Further details concerning voice in the conversation concerning the respondents demographic can be China’s high-net worth consumers. found in the methodology. The findings of the Chinese Luxury Traveller 2018 will continue to help Rupert Hoogewerf, Chairman & our partners and clients grow their Chief Researcher of Hurun Report, businesses in this region.” said: “Chinese high-end travellers more and more recognise the value The following report includes insights of services, and are less concerned such as the emergence of parent- about the prices compared to the child travel, the rise of holiday home past. -

2016Semi-Annual Report

CHINA CONVERGENCE FUND A Sub-fund of Value Partners Intelligent Funds SEMI-ANNUAL 2016 REPORT For the six months ended 30 June 2016 Value Partners Limited 9th Floor, Nexxus Building 41 Connaught Road Central, Hong Kong Tel: (852) 2880 9263 Fax: (852) 2565 7975 Email: [email protected] Website: www.valuepartners-group.com In the event of inconsistency, the English text of this Semi-Annual Report shall prevail over the Chinese text. This report shall not constitute an offer to sell or a solicitation of an offer to buy shares in any of the funds. Subscriptions are to be made only on the basis of the information contained in the explanatory memorandum, as supplemented by the latest semi-annual and annual reports. CHINA CONVERGENCE FUND A Sub-fund of Value Partners Intelligent Funds (A Cayman Islands unit trust) CONTENTS Pages General information 2-3 Manager’s report 4-9 Statement of financial position (unaudited) 10 Investment portfolio (unaudited) 11-15 Investment portfolio movements (unaudited) 16 SEMI-ANNUAL REPORT 2016 For the six months ended 30 June 2016 1 CHINA CONVERGENCE FUND A Sub-fund of Value Partners Intelligent Funds (A Cayman Islands unit trust) GENERAL INFORMATION Manager Legal Advisors Value Partners Limited With respect to Cayman Islands law 9th Floor, Nexxus Building Maples and Calder 41 Connaught Road Central 53rd Floor, The Center Hong Kong 99 Queen’s Road Central Hong Kong Directors of the Manager Dato’ Seri Cheah Cheng Hye With respect to Hong Kong law Mr. Ho Man Kei, Norman King & Wood Mallesons Mr. So Chun Ki Louis 13th Floor, Gloucester Tower The Landmark Trustee, Registrar, Administrator and 15 Queen’s Road Central Principal Office Hong Kong Bank of Bermuda (Cayman) Limited P.O. -

Spirits Selection by Concours Mondial 2020 Prize List

Spirits Selection by Concours Mondial 2020 Prize list Armenia Belgium Gold Medals Gold Medals V & M 3 Yo (Brandy) Filliers Barrel Aged Genever 8 Years Old (Genever) Producer: Armenia Wine Factory LLC Producer: Filliers Distillery Australia Ginbee's (Gin) Producer: Dard-Dard Srl Silver Medals Gouden Carolus Single Malt (Whisky) Coffee Storm (Flavoured Rum) Producer: Brouwerij Het Anker - Stokerij De Queensland Molenberg Producer: Milton Distillery Pty LTD Le passionné Rhumantic (Flavoured Rum) Producer: Fabian Pierre - Rhumantic Austria Pastis Patinette (Aniseed) Gold Medals Producer: Distillerie Gervin Distillery Krauss London Dry Gin Bergamot Pepper Plus Oultre Distillery Bitter (Bitter) (Gin) Producer: Plus Oultre Distillery Producer: Distillery Krauss GmbH Shack Pecans Spiced Rum (Spiced Rum) G+ Classic Edition Gin (Gin) Producer: Plan B International BVBA Producer: Distillery Krauss GmbH Silver Medals G+ Lemon Edition Gin (Gin) Producer: Distillery Krauss GmbH Amaretto Noblesse (Liquor-Cream) Producer: Noblesse 1882 SPRL Silver Medals Belgian Owl - Passion (Whisky) Distillery Krauss Distilled Anise (Aniseed) Producer: The Owl Distillery S.A. Producer: Distillery Krauss GmbH Biercine (Liquor-Cream) G+ Flower Edition Gin (Gin) Producer: Brass des Légendes sprl-Distillerie de Producer: Distillery Krauss GmbH Biercée Cosmik Pure Diamond Vodka (Vodka) Producer: Wave Distil srl Dr.Clyde Classic Rum (Rum) Producer: Dr.Clyde Distillery Filliers Barrel Aged Genever 17 Years Old (Genever) Producer: Filliers Distillery Gin.be (Gin) Producer: