Tate Economic Research Inc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Bankers Hall East

BANKERS HALL EAST Class AA SUBLEASE FLOOR 39: 12,326 SF Damon Harmon, CPA, CGA Josh Hamill Nicole Bennett 403.571.8221 403.539.0889 403.258.1872 [email protected] [email protected] [email protected] Features & AMENITIES Premises is in excellent, move-in condition Space is ideally suited for a highly collaborative team; several break- out rooms and large open area with unobstructed views to the North and West Some furniture potentially available Plus 15 connection to Bankers Court, Home Oil Tower, Royal Bank Building, The Core Shopping Centre Within walking distance to several public transit routes and CTrain stations 40,000-square-foot Bankers Hall Club, a private health club offering cardiovascular and weight training, fitness studios, 4 squash courts, lounge and pro shop Access to Bankers Hall Auditorium, a state-of-the-art facility designed to accommodate up to 175 people On-site management with 24/7 building access and security Space PROFILE Sublandlord: Bennett Jones Services Limited Partnership Subpremises: 39th Floor: 12,326 sf Availability: Immediately Term Expiry: Flexible up to May 30, 2027 Rental Rate: Market sublease rates T.I.A.: As is Op. Costs & Taxes: $21.75 per sf (est. 2019) Parking: 1 stall per 2,500 sf at market rates Building INFORMATION Exterior Address: 855 Second Street SW Year of Completion: 1988 Number of Floors: 52 Rentable Area: 820,221 sf Ave. Floor Plate: 20,500 sf Security: 7 days per week, 24 hours per day Manned security desk, card key access HVAC: 7:30 am - 6:00 pm After hours upon request Landlord/ View from Office Building Manager: Brookfield Office Properties Boardroom 39.368 ROBSON A 39.342 39-106 FLEX 39.332 39.102 39.372 39.374 39.340 39.100 39.376 39.378 39.366 39.334 BRYCE FLEX CONFERENCE CONFERENCE OPEN WORK AREA 39.338 39.336 39.104 39-134 39-386 39.370 COFFEE 39.364 39.118 ENCLAVE N. -

Eau Claire Tower

EAU CLAIRE TOWER 600 - 3rd Avenue SW Calgary, AB LIFESTYLE MEETS BUSINESS Footsteps away from the Bow River Pathway System and only 10 minutes to the Core Shopping Centre. Eau Claire Tower is one of the most balanced work life oriented buildings in downtown Calgary. WELCOME TO EAU CLAIRE TOWER OFFICE SPACE FOR SUBLEASE AVAILABLE SPACE 28,199 s.f. 600 - 3rd Avenue SW Calgary, AB SUBLANDLORD: MEG Energy Corp. PREMISES: Floor 20 AVAILABILITY: Immediately TERM: December 30, 2031 RENTAL RATE: Market Sublease Rate ADDITIONAL RENT: $23.41 p.s.f. (Est.2020) PARKING: 1:1,974 s.f. W N R D IA R O M E M W S Eau Claire E E D Plaza D A A R R Sien Lok A A P P Park Y Y A A L YMCA L C C Eau Claire R R A A Market B EAU CLAIRE AVE SW B RIVERFRONT AVE SW 1 AVE SW LOCATION & CONVENIENCE Millennium Tower 2 AVE SW 2 AVE SW 2 AVE SW 2 AVE SE Centennial Livingston Shaw Eau Claire Place Devon Calgary Place Court Tower West Tower West R Eau Claire Tower features a +15 connection, and City Centre IVER Centennial Livingston FRON T AV Place Place South E SE East 3 AVE SW quick access to public transit and major entry 3 AVE SW 3 AVE SW 3 AVE SE 615 Eau Eau Claire Sunlife 3rd Ave Claire Place II Westin North City Place I Shell Hotel Plaza Harry Hays Centre 240 n Building Jamieson w o United e 4 Ave Place t 4 v McFarland Sunlife First a 4 Altius International Asia points to Calgary’s Downtown. -

Reaching Over 5 Million People, Minutes on the Contest Page and Growing Their Facebook Fan Base

ICSC CANADIAN SHOPPING CENTRE AWARDS PRESENTS Reaching N E W Heights SEPTEMBER 23, 2014 2014 AWARD WINNERS GOLDEN MOMENT Congratulations to this year’s ICSC Award winners and nominees for their outstanding achievements in excellence and innovation. Oxford Properties Group portfolio includes office developments in major urban centres, luxury resort hotels across the country, and some of Canada’s most prestigious shopping centres. SQUARE ONE, SOUTHCENTRE, SCARBOROUGH TOWN CENTRE, YORKDALE, KINGSWAY MALL, PROMENADES CATHÉDRALE, HILLCREST MALL, UPPER CANADA MALL, LES PROMENADES GATINEAU, EDMONTON CITY CENTRE, LES GALERIES DE LA CAPITALE www.oxfordproperties.com 2014 CANADIAN SHOPPING CENTRE AWARD WINNERS The ICSC Canadian Shopping Centre Awards are designed to honour our industry’s brightest and best. The Awards bring information and insight to the entire industry on what it takes to achieve high levels of success. MARKETING ADVERTISING Centres 150,000 to 400,000 sq. ft. of total retail space SILVER SILVER Get Your Red On It’s The Little Things Cottonwood Mall Eglinton Square Shopping Centre Chilliwack, British Columbia Toronto, Ontario Management Company: Morguard Management Company: Bentall Kennedy (Canada) LP Owner: 2046459 Ontario Inc. Owner: Kingsett Capital Investments Cottonwood Mall had three events wrapped in an effective ad Eglinton Square’s 2013 campaign “It’s The Little Things” was the answer campaign titled “Get Your Red On” which reduced the creative and to a demographic shift in the PTA that saw young families moving into placement costs. The combined media mix drove over 3.2 million post-war bungalows. Family traffic and related tenant sales grew in audience impressions, 9.5% more than projected, and retail sales the double-digits by altering the Centre’s voice to one that was more volume increased an incredible 12.3% for November and 8.6% for family-oriented. -

A Surgeon's Memories…

COMMUNICATING WITH PHYSICIANS IN ALBERTA February 2016 ZONE MEDICAL STAFF ASSOCIATIONS OF ALBERTA VITAL SIGNS President’s Message: For Such a Time as This A Curved Road to Medicine The Department: A Surgeon’s Memories…Before I Forget Celebrate What Works The Illustrious Goal To Achieve Work-Life Balance Researcher Joins World Health Organization’s Essential Medicines Committee May You Live in Interesting Times… 2 3 1 Aspen Landing Crowchild Trail NW Aspen Landing Shopping Centre John Laurie Blvd NW 105, 339 Aspen Glen Landing SW 2 2 Castleridge NE DeerfootTrail Castleridge Plaza McKnight Blvd NE 20, 55 Castleridge Blvd. NE 1 4 3 Crowfoot Sarcee Trail SW Crowfoot Business Centre 16 Avenue NE 401, 400 Crowfoot Cres. NW 1 Memorial Drive 4 Market Mall 6 Market Mall Shopping Centre 10 333, 4935 - 40 Ave. NW 11 9 Ave SE ail SE 5 Mayfair Place 1 Tr 110/132, 6707 Elbow Dr. SW 6 Riley Park MacLeod Riley Park Health Centre Building 2 110, 1402 - 8th Ave. NW SE Trail Deerfoot Glenmore Trail SW 7 South Calgary Health Centre (X-ray only) 105, 31 Sunpark Plaza SE 5 8 Southcentre Southcentre Mall Shopping Centre 177, 100 Anderson Rd. SE 9 Sunpark Anderson Road SW 8 Sunpark Professional Centre 125, 40 Sunpark Plaza SE 10 The CORE The CORE Shopping Centre 417, 751 - 3 St. SW 2 11 Westbrook Sun Valley Blvd SE Westbrook Professional Building 7 200, 1610 - 37 St. SW 9 22X Marquis of Lorne Trail SW Community • X-Ray • Mammography Convenience • Bone Densitometry • Vascular Ultrasound Centre • Image-Guided Pain Therapy • Ultrasound • Ultrasound-Guided Biopsy • Echocardiography • Nuclear Imaging • Myocardial Perfusion Imaging • Exercise Stress Testing Physician Line 403.777.1999 Customer Contact Centre 403.777.3000 radiology.ca A CALGARY & AREA MEDICAL STAFF SOCIETY PUBLICATION February 2016 CAMSS EXECUTIVE Contents: President: Dr. -

Penn West Plaza 215 - 9Th Avenue Sw Calgary, Ab

PENN WEST PLAZA 215 - 9TH AVENUE SW CALGARY, AB DOWNTOWN ‘A’ CLASS RETAIL SPACE FOR SUBLEASE Steven Goertz, Vice President Anna Sorensen, Associate 403.232.4322 403.232.4383 [email protected] [email protected] © 2018 Avison Young Real Estate Alberta Inc. All rights reserved. E. & O.E.: The information contained herein was obtained from sources which we deem reliable and, while thought to be correct, is not guaranteed by Avison Young. PENN WEST PLAZA - WEST TOWER FOR SUBLEASE 215 - 9TH AVENUE SW, CALGARY, AB BUILDING DETAILS ADDRESS: 215 – 9th Avenue SW BUILDING SIZE: 384,324 SF ZONING: CR20 - C20 / R20 NUMBER OF FLOORS: 20 LANDLORD: Morguard Investments SUBLANDLORD: Engel & Volkers Calgary LEASING INFORMATION RENTABLE AREA: Unit 140 1,441 SF OCCUPANCY: Immediately OPERATING COSTS & TAXES: $16.53 PSF (2018 est.) RENT: Market Rates TERM: Jan 30, 2025 PARKING: 2 Reserved Underground $500/stall/month COMMENTS - Beautiful and modern retail space in an ‘A’ class office building - Centrally located in Calgary’s Downtown Core - Future +15 connectivity to Gulf Canada Square - Excellent exposure onto 9th Avenue SW with 30,000 vehicles passing per day 0 WALL TYPES D0 DOOR TYPES 56'-1 1/2" 5'-8 3/4" 3'-3" 24'-3" 3'-6 1/4" 19'-4 1/2" 1 5/8"TYPE-X 1 36" STEEL DOOR c/w GLASS INSERTS(TEMPERED)- D1 D1 STEEL STUD(1 1/4"X3 5/8") (EXISTING) ROXUL SAFE & SOUND 2 36" STEEL DOOR c/w LEVER TYPE HANDLE - KEYED 3 2 (EXISTING) 5/8" TYPE-X 3 EMPTY STEEL STUD(1 1/4"X 1 5/8") " " 8" POURED CONCRETE 4 EMPTY 0 4 1 / - 1 ' 3 6 - ' 3 (EXISTING) 5 36" STEEL DOOR c/w SELF CLOSING MECHANISM & LEVER 4 Hunter & Tristan Design TEMPERED GLASS c/w ALUMINUM MULLIONS@ 60" o/c TYPE HANDLE (EXISTING) 700, 1816 Crowchild Trail N.W. -

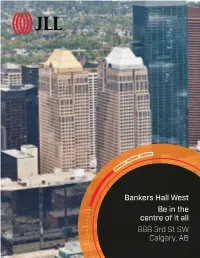

Bankers Hall West Be in the Centre of It All 888 3Rd St SW Calgary, AB for Sublease

Bankers Hall West Be in the centre of it all 888 3rd St SW Calgary, AB For Sublease Property Highlights • Plus 15 connected to Gulf Canada Square, Bankers Court, TD Square / Devonian Gardens, and Bankers Hall Parkade • Built out reception on 31st floor • Internal staircase to 32nd floor • Amenities include fitness, auditorium, shopping atrium, underground heated parking, and concierge • Close proximity to a variety of local high end restaurants • Directly on Stephen Avenue Walk, Calgary’s only pedestrian mall • Quick access to the Core Shopping centre where there are a variety of restaurants and retailers • Walking distance to LRT • BOMA 360 designation/LEED Gold Certified Property Details Space Floors 31 and 32 Size 41,086 s.f. Availability Immediate Location Centre Core Total Building Size 807,241 Year Built / Renovated 1984 Rental Rate Market Rates Sublandlord Repsol Oil & Gas Canada Inc. Operating Costs $19.87 p.s.f (Est 2019) Parking Information 6 stalls per floor Expiration Date February 27, 2025 Bankers Hall West 47 46 Paramount Resources 45 44 Stikeman Elliot LLP 43 42 Canterra/Wolf Subtenant Robert Half Canada Inc. Subtenant Subtenant Custom Homes 41 BMO Newbitt Burns Inc. 40 RBC Dominion Securities / RBC 39 Capital Markets - Real Estate 38 Oculus / Conair / Spector | Cassels Brock LLP Ban rs Ha W t W rs Ha Ban 37 Bankers Petroleum 36 Persta Resources Inc. 35 34 Keywest Projects Ltd. 33 Repsol Oil and Gas Canada Inc. 32 Repsol Sublease Available 31 30 29 28 27 26 25 Repsol Oil and Gas Canada Inc. 24 23 22 21 20 19 18 CNRL 17 16 -

OFFICE SPACE for SUBLEASE Bank of Montreal Historic Building

th RARE DOWNTOWN 140 - 8 Avenue SW CHARACTER OFFICE SPACE OFFICE SPACE FOR SUBLEASE Bank of Montreal Historic Building COLLIERS INTERNATIONAL CRAIG HULSMAN TODD SUTCLIFFE 900, 335 8th Avenue SW ASSOCIATE VICE PRESIDENT VICE PRESIDENT/PARTNER Calgary, AB T2P 1C9 403 266 5544 403 571 8829 403 298 0414 www.collierscanada.com [email protected] [email protected] Salient Details Subpremises: Floor 3 - 12,712 square feet AVAILABLE FURNITURE SCHEDULE: Sublease Term: Expires November 29, 2023 LOCATION QUANTITY SYMBOL ITEM DESCRIPTION SUPPLIER: C.O.I (CONTEMPORARY OFFICE Market Sublease Rates INTERIORS) Basic Rent: MANUFACTURER: HERMAN MILLER 310.311.318 80 C1 SAYL CHAIR NAME: +WK CHR ASMBLED SAYL 333.411-A SUSPENSION MID-BCK STD-HGT Operating Costs (2019 Estimate) $19.38 per square foot 412 TLT LIM FXD ARMS F COPYRIGHT : RADEC GROUP SUBPREMISES MODEL NUMBER: AS1SA22PF ALL DIMENSIONS IN FEET AND INCHES UNLESS Availability Date: Immediate SUPPLIER: LIGHTFORM OTHERWISE NOTED. MANUFACTURER: BLU DOT DO NOT SCALE. NAME: PARAMOUNT LOUNGE CHAIR - 310 & 410 8 LOUNGE CHAIR NOTE C2 SMOKE GENERAL CONTRACTOR AND/OR SUBTRADES TO Sublandlord: Seven Generations Energy Ltd. (4 IN EACH AREA MODEL NUMBER: PM1-LNGHC... VERIFY ALL DIMENSIONS AND CONDITIONS AS ALL FURNITURE AND EQUIPMENT NOT IN CONTRACT INDICATED) (N.I.C.) AND SUPPLIED BY TENANT UNLESS TAGGED. SHOWN ON DRAWINGS WITH ACTUAL EXISTING 51561 BC Ltd. CONDITIONS. ANY DISCREPANCIES TO BE Landlord: 323.326. SUPPLIER: C.O.I (CONTEMPORARY OFFICE REPORTED PRIOR TO COMMENCEMENT OF 327.329.332. INTERIORS) CONSTRUCTION AND/OR INSTALLATION. 335.339.340. MANUFACTURER: HERMAN MILLER 341.344.345. IF IN DOUBT, ASK. -

Calgarians Are in the Top One Per Cent of Income Earners in the Country, and It Shows As the City's Luxury Market Continues to Grow

A CALGARY HERALD ADVERTISING PUBLICATION • OCTOBER 23, 2013 • ISSUE TWO • WWW.CALGARYHERALD.COM/LUXURY LUXURY AUTO • REAL ESTATE • HOME DECOR • FURNITURE • FASHION & ACCESSORIES one for ALL Calgarians are in the top one per cent of income earners in the country, and it shows as the city's luxury market continues to grow Barb Livingstone compared to 2.3 per cent and 3.1 per cent respectively across the country. What do you get when you combine the most “one- “We generally see the highest retail spending in the percenters” per capita, a new national flagship Fer- country,” says Brunnen. rari Maserati showroom, the entry of high-end retailer And while this city is not a large retail market com- Nordstrom next year and the biggest increase ever in pared to bigger cities such as Toronto and Vancouver, $1 million-plus home sales? he says international retailers are, more and more, see- You get Calgary — a city that, despite devastating floods ing Calgary as a good market to be in. this summer, continues to power this country’s economy, High-end U.S. retailer Nordstrom is entering the luxury including the purchasing power for all things “luxury.” market next year with a store at Chinook Centre, com- Ben Brunnen, a Calgary economic consultant, says peting against Holt Renfrew — whose Calgary store is the city — with the largest number of head offices per seen as one of the most profitable per square foot in the capita in the country — has more executives, higher country. pay and the type of industries (oil and gas, mining, utili- Calgarians can also find luxury vehicles in the city, ties, construction, manufacturing) that contribute to the from Ferrari to Bentley dealerships. -

TD Square - Dome Tower 900, 335 8Th Avenue SW Calgary, AB T2P 1C9 the Dome Tower Offers Tenants Unprecedented Amenities and Convenience

JIM REA Executive Vice President | Partner 403 215 7250 [email protected] TODD SUTCLIFFE Vice President | Partner 403 298 0414 [email protected] FOR SUBLEASE | 333 7th Avenue SW, Calgary, AB Colliers International TD Square - Dome Tower 900, 335 8th Avenue SW Calgary, AB T2P 1C9 The Dome Tower offers tenants unprecedented amenities and convenience. Located at the www.colliers.com/calgary core of downtown Calgary’s financial and retail centres, the location provides convenient +1 403 266 5544 transportation and parking with direct access to the adjacent east/west LRT and to the neighbouring developments via Calgary’s Plus 15 and Plus 30 walkways. World class accommodations are within a few blocks at the nearby Sheraton, Hyatt, Fairmont Palliser and Westin Hotels. Direct access to The CORE Shopping Centre and Stephen Avenue pedestrian mall provides tenants to easily experience Calgary’s premier retail shops, restaurants and entertainment. Accelerating success. FOR SUBLEASE | 333 7th Avenue SW, Calgary, AB OFFICE OFFICE OFFICE OFFICE OFFICE BOARDROOM OFFICE OFFICE OFFICE OFFICE OFFICE OFFICE Sublease Information OFFICE OFFICE KITCHEN/DINING OFFICE OFFICE ENCLOSED STAIR (NO RECEPTION OFFICE OFFICE OFFICE Available Subpremises Floor 27 - Approx. 13,950 square feet* MEETING Potential to Demise ACCESS) TILE OFFICE Sublandlord Enerplus Corporation CARPET CARPET COPY TILE OFFICE OFFICE Annual Net Rent Market Rates OFFICE OFFICE OFFICE N Operating Costs and Taxes $18.09 per square foot (2019 estimate) OFFICE OFFICE OFFICE TOWEL DISPENSER -

National Jazz Summit Kicks Off in Style First Artists-In-Residence Create

2012 Report to the Community National Jazz Summit kicks off in style First Artists-in-Residence create brand new work NMC develops crucial new partnerships Why volunteers love giving back Hi, my name is: 16 new staff in 2012 nmc.ca welcome From the President International Organ Festival, CKUA Radio Network, the Anne Murray Centre, the Banff Centre and others. • Engaging volunteers from Music heals. across Canada to sit on It helps us committees and the board. understand the • Inviting Canadian artists from world around across the musical spectrum us; it comforts to participate in residencies to and inspires to create new work. overcome life’s challenges. The • Networking regionally and National Music Inventing a new home for music nationally on education Centre promises in Canada is both invigorating initiatives/best practices. to be a safe and challenging every day. In my • Travelling collections and haven where travels all over Canada, I meet exhibitions to partner loca- we connect, with people – in both official lan- tions across Canada. grow, learn and guages – who are excited about find community NMC and the unique opportunity Our mission is to amplify the through music. it has created to make Canada love, sharing and understanding stronger through music. of music. We strive to serve and Roger C. Jackson, collaborate with thousands of OC, AOE. Chair, NMC At NMC, we are very conscious people every year, as we in turn Board of Directors of our intention to be a national amplify our own efforts and organization that serves all transform from a small Calgary- Canadians in a meaningful way, based arts organization, to a and so we are: national hub. -

Office Space for Lease Leased

7TH FLOOR PLAN Full Floor: 10,810 SF 8TH FLOOR PLAN Suite 801: 2,983 SF Suite 802: LEASED Suite 804: 1,028 SF Suite 810: 2,277 SF TECK PLACE 205 9TH AVENUE SE, CALGARY, AB Partnership. Performance. OFFICE SPACE FOR LEASE Opportunity LEASED - 1,028 SF - 10,979 SF of Downtown office space available - Convenient downtown location one block to the +15 & two blocks to LRT Eric Horne, Principal Jason Kopchia, Associate © 2018 Avison Young Real Estate Alberta Inc. All rights reserved. 403.232.4339 587.293.3361 E. & O.E.: The information contained herein was obtained from sources which we deem reliable and, while thought to be correct, is [email protected] [email protected] not guaranteed by Avison Young. CiCityty ofof CCalgaryalgary Bridge Street Centre LEGENDLEGEND City of Calgary Memorial Drive 3 Number of Floors Light Rail Transit (C-Train) Downtown & Beltline Waterfront Condos Plus 15 Connections DDowntownowntown && BBeltlineeltline Anthem (C-Train) Properties Proposed Plus 15 Connections The Concord One Way Indicator NE 4 Street Trail Edmonton Eau Claire Avenue SW Riverfront Avenue CP Rail Future Future Development Development Memorial Drive Site Site Q Haute Chinese Cuisine United P P Church 2 Avenue SW Daqing Avenue 2 Avenue SE Riverfront Avenue 36 AVISON YOUNG REAL ESTATE ALBERTA INC. Eau Claire Centennial Future City City Tower Place West Centre Eighth Avenue Place - West Tower Centre Phase I Centennial Devon Phase II 1200, 585 - 8th Avenue SW 24 Place East Tower Calgary, AB T2P 1G1 Barclay Mall Barclay T. 403.262.3082 3 Avenue SW 3 Avenue SE Future HSBC F. -

Centre City Plan Refresh What We Heard: 2018 Public Engagement

Centre City Plan Refresh What We Heard: 2018 public engagement March 13, 2019 calgary.ca | contact 311 03 Centre City Plan Refresh What We Heard: 2018 public engagement About this what we heard report This report summarizes the activities and results of engagement for the Centre City Plan Refresh project. It outlines the project, the purpose of the public engagement, the activities we did, and a summary of what we heard at the events. A full list of comments received through public engagement is included in this report. This report does not outline what has happened as a result of the public engagement. That summary will be published at a later date, once all engagement has been completed and project plans have been finalized. Project overview In 2007, based on extensive citizen input, City Council adopted the Centre City Plan, a vision document that describes what the Centre City could look like in 30 years. The Centre City Plan is a coordinated strategy document that pulls together the vision for the Centre City along with strategies and actions relating to land use planning, economic, cultural, and social development, and governance. With the approval of the adoption of the Centre City Plan (CPC2007-049), it included a recommendation for regular monitoring and reporting. In January 2017 the Centre City Plan was identified as one of 28 Council policies to be amended. It’s time to review and refresh the original Centre City Plan. Calgary’s Centre City is the area south of the Bow River (including Prince’s Island Park) from 17th Avenue Southwest and 14th Street Southwest, to the Elbow River.