Food Service - Hotel Restaurant Institutional

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Associative Meaning in the Original Slogan of Fast Food Advertisement

1 ASSOCIATIVE MEANING IN THE ORIGINAL SLOGAN OF FAST FOOD ADVERTISEMENT SKRIPSI Submitted in Partial Fulfillment of Requirements for the Degree of Sarjana Pendidikan (S.Pd) English Education Program By: YUNI WULANDARI NPM: 1302050369 FACULTY OF TEACHER TRAINING AND EDUCATION UNIVERSITY OF MUHAMMADIYAH SUMATERA UTARA MEDAN 2017 2 ABSTRACT Wulandari, Yuni. 1302050369. “Associative Meaning in the Original Slogan of Fast Food Advertisement”. Skripsi: English Education Program. Faculty of Teacher Training and Education. University of Muhammadiyah Sumatera Utara. Medan. 2017 This study deals with associative meaning in the original slogan of fast food advertisement. The aims of this study were (1) to figure out the kinds of associative meaning in the original slogan of fast food advertisement and (2) to describe the associative meaning in the original slogan of fast food advertisement. The technique used in this study was a library research, and was conducted at the library UMSU at Jalan Muchtar Basri No. 3 Medan by using descriptive qualitative method. The data of this study was taken from slogan of twelve fast food restaurants where in restaurant there was being more than one slogan, finally there were 25 slogans finally obtained into the data to be analyzed related with the associative meaning. After being analyzed and based on the Leech theory. The result showed that there were 5 types of associative meaning found in slogan of fast food advertisement and the used of connotative meaning very worked well in the used of the slogan. The used of Stylistic meaning was very influential of social circumstance of language use in the slogan. -

BAB I PENDAHULUAN 1.1 Latarbelakangmasalah

BAB I PENDAHULUAN 1.1 LatarBelakangMasalah Perkembangan bisnis di era globalisasi ini semakin pesat ditandai tingkatpersaingan antar perusahaan yang semakin ketat. Persaingan bisnis ini telahmembuat berbagai perusahaan berlomba untuk merebut dan mempertahankanpangsa pasarnya. Berbagai macam produk baru bermunculan mengikuti aruskebutuhan persaingan pasar. Produk baru lahir biasanya lebih mengutamakandaya tarik untuk merebut posisi di pasar, baik dari segi kualitas, kemasan maupuncita rasa. Dalam kondisi semakin meningkatnya persaingan antara produk sejenis,maka perusahaan saling bersaing merebutkan konsumen. Perusahaan yang mampumenciptakan dan mempertahankan pelangganlah yang akan sukses dalampersaingan. Perusahaan menyadari dalam era globalisasi, pemasaran merupakan kuncidan faktor kesuksesan, peran pemasaran semakin penting seiring denganpersaingan yang sangat ketat dengan kondisi pasar juga yang semakin tidakmenentu, padatnya persaingan yang akan menyebabkan pelanggan menghadapilebih banyak pilihan alternatif untuk produk, harga, dan kualitas yang bervariasi,sehingga pelanggan akan selalu mencari nilai yang dianggap paling tinggi daribeberapa produk. Kondisi inilah yang memaksa berbagai perusahaan untukmenemukan berbagai strategi yang tepat untuk mencapai keunggulan kompetitifdengan harapan perusahaan dapat mempertahankan pasarnya dan 1 2 memenangkanpersaingan. Karena itu pemasaran akan terfokus pada bagaimana produk dan jasabisa memenuhi permintaan dan kebutuhan para konsumennya. Dalam hal ini sektor-sektor yang termasuk di dalam -

Haggerty Will Not Seek Another Term by Janet Armantrout Alameda County Supervisor Haggerty Has a Long List of Still Have Reserves." Completed

Thursday, JUNE 13, 2019 VOLUME LVI, NUMBER 24 Your Local News Source Since 1963 SERVING DUBLIN, LIVERMORE, PLEASANTON, SUNOL County Supervisor Haggerty Will Not Seek Another Term By Janet Armantrout Alameda County Supervisor Haggerty has a long list of still have reserves." completed. Scott Haggerty has announced accomplishments, with financial During the recent recession, Other accomplishments in- that he will not seek re-election stability a particular source of no county employee lost his or clude instituting a fracking ban See Inside Section A in 2020. pride. Alameda County has earned her job. for the county, expanding Bed & Section A is filled with After 23 years in office, he the county triple A ratings from all He points to the Bankhead Breakfast opportunities in South information about arts, declared, "I'm tired. The job has of the rating agencies. The reserve Theater as another project he is Livermore, and establishing a people, entertainment and really taken a toll. I need to get policy that he helped to put in proud of. Haggerty obtained $23 microbrewery ordinance. special events. There are healthy." place contains over $100 million. million from the Altamont and The ag barn at the fairgrounds, education stories, a variety He added that for the past year, He noted, "We paid $200 million Vasco landfills to make it a reality. Stanley Blvd. improvements, HOT of features, and the arts he had been thinking about not drawing down our Other Post- He made sure that the BART lanes on 580 and 680, and a ballot and entertainment and running. Employment Benefits (OPEB) and to Warm Springs extension was measure that raised over $8 billion bulletin board. -

January 2015 List of Cases Handled and Disposed

f DOLE-BWC- Republic of the Philippines DEPARTMENT OF LABOR AND EMPLOYMENT DOLE Regional Office No. X REFERENCE DATE: As of 2016 LIST OF CASES HANDLED AND DISPOSED JANUARY 2015 CASE ARISING NAME OF DATE FILED DATE DAYS NAME OF PARTY FROM: NATURE OF MONETARY WORKERS No. CASE TITLE COMPLAIN CASE NUMBER (dd-Mon- FINDINGS STATUS DISPOSED DURATION COMPLAINED OF (Indicate JA, BUSINESS BENEFITS BENEFITED ANT yy) (dd-Mon-15) * CV, OSHI) 1 MSU-IIT JA 03-Dec-14 Issued 22-Jan-15 38 NMPC GLS/OHS TUBOD MSU-IIT NMPC TUBOD RO1000-WMO-JA-2015- BRANCH BRANCH 01-0001 6 2 MOTORT JA 03-Dec-14 Issued 22-Jan-15 38 RADE - RO10-WMO-JA-2015- GLS/OHS ILIGAN 2 MOTORTRADE - ILIGAN 2 01-0002 2 3 MISAMIS RO10-WMO-JA-2015- JA 03-Dec-14 Issued 22-Jan-15 38 UNIMART MISAMIS UNIMART 01-0003 GLS/OHS 1 4 MINDANA JA 03-Dec-14 Issued 22-Jan-15 38 O GLS/OHS ORIENTA L BUILDER S INC./PHIL MINDANAO ORIENTAL . SINTER BUILDERS INC./PHIL. RO10-WMO-JA-2015- CORP. SINTER CORP. 01-0004 1 5 ELECTRI JA 03-Dec-14 Issued 22-Jan-15 38 C GLS/OHS AIRPOW ER MECHANI CAL ELECTRIC AIRPOWER RO10-WMO-JA-2015- INC./PSC MECHANICAL INC./PSC 01-0005 1 6 GRACIA' JA 03-Dec-14 Issued 22-Jan-15 38 S GLS/OHS FOODHO USE BAKESH GRACIA'S FOODHOUSE RO10-WMO-JA-2015- OP BAKESHOP 01-0006 3 7 WIZARD I JA 03-Dec-14 Issued 22-Jan-15 38 TECH GLS/OHS MULTISO WIZARD I TECH RO10-WMO-JA-2015- LES MULTISOLES 01-0007 1 8 MSU-IIT JA 03-Dec-14 Issued 22-Jan-15 38 NMPC GLS/OHS HEAD MSU-IIT NMPC HEAD RO10-WMO-JA-2015- OFFICE OFFICE 01-0008 3 9 MSU-IIT JA 03-Dec-14 Issued 22-Jan-15 38 NMPC GLS/OHS TIBANGA MSU-IIT NMPC TIBANGA RO10-WMO-JA-2015- BRANCH BRANCH 01-0009 2 10 CYCLON JA 03-Dec-14 Issued 22-Jan-15 38 E GLS/OHS TRANSP ORT CORP./P CYCLONE TRANSPORT RO10-WMO-JA-2015- SC CORP./PSC 01-0010 2 11 DES JA 03-Dec-14 Issued 22-Jan-15 38 APPLIAN GLS/OHS CE PLAZA, DES APPLIANCE PLAZA, RO10-WMO-JA-2015- INC. -

Spatial Competition and Marketing Strategy of Fast Food Chains in Tokyo

Geographical Review of Japan Vol. 68 (Ser. B), No. 1, 86-93, 1995 Spatial Competition and Marketing Strategy of Fast Food Chains in Tokyo Kenji ISHIZAKI* Key words: spatial competition,marketing strategy, nearest-neighbor spatial associationanalysis, fast food chain, Tokyo distributions of points, while Clark and Evans I. INTRODUCTION (1954) describe a statistic utilizing only a single set of points. This measure is suitable for de One of the important tasks of retail and res scribing the store distribution of competing taurant chain expansion is the development of firms such as retail chains. a suitable marketing strategy. In particular, a The nearest neighbor spatial association location strategy needs to be carefully deter value, R, is obtained as follows: mined for such chains, where store location is often the key to the successful corporate's R=ƒÁ0/ƒÁE (1) growth (Ghosh and McLafferty, 1987; Jones and The average nearest-neighbor distance, ƒÁ0, is Simmons, 1990). A number of chain entries into given by the same market can cause strong spatial com petition. As a result of this, retail and restaurant (2) chains are anxious to develop more accessible and well-defined location strategies. In restau where dAi is the distance between point i in type rant location, various patterns are respectively A distribution and its nearest-neighbor point in presented according to some types of restau type B distribution and dBj is the distance from rants (i.e. general full service, ethnic, fast food point j of type B to its nearest neighbor point of and so on) and stores of the same type are type A. -

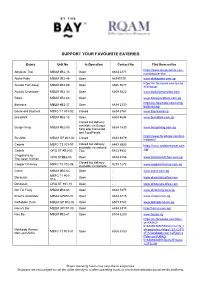

Support Your Favourite Eateries

SUPPORT YOUR FAVOURITE EATERIES Eatery Unit No In Operation Contact No. Find them online https://www.absolutethai.com. Absolute Thai MBLM #B2-16 Open 6634 2371 my/absolute-thai Aloha Poke MBLM #B2-46 Open 66340730 www.alohapoke.com.sg https://m.facebook.com/arcad Arcade Fish Soup MBLM #B2-69 Open 8566 9077 efishsoup/ Awfully Chocolate MBLM #B2-33 Open 6509 9422 www.awfullychocolate.com Boost MBLM #B2-64 Open www.boostjuicebars.com.sg https://m.facebook.com/living. Botanica MBLM #B2-37 Open 6634 2330 botanica.sg/ Boulevard Bayfront MBFC T1 #01-02 Closed 6634 8761 www.Boulevard.sg Breadtalk MBLM #B2-18 Open 6509 4644 www.breadtalk.com.sg Closed but delivery available via Burger Burger King MBLM #B2-03 6634 1530 www.burgerking.com.sg King app, Deliveroo and FoodPanda https://www.facebook.com/bus Bushido MBLM GP #01-02 Closed 6634 8879 hidoasia/ Closed but delivery Cedele MBFC T3 #01-07 6443 8553 https://www.cedelemarket.com available via website .sg/ Cedele ORQ ST #B2-02 TBC 6423 4882 Chopsticks by ORQ ST#B2-04 Open 6534 9168 www.theasiankitchen.com.sg The Asian Kitchen Closed but delivery Copper Chimney MBFC T3 #02-06 9238 1272 www.copperchimney.com.sg available via website Crave MBLM #B2-63 Open - www.crave.com.sg MBFC T1 #01- Dimbulah Open - www.dimbulahcoffee.com 01A Dimbulah ORQ ST #01-10 Open - www.dimbulahcoffee.com Din Tai Fung MBLM #B2-05 Open 6634 7877 www.dintaifung.com.sg Erwin's Gastrobar MBLM GP#01-01 Open 6634 8715 www.erwins.com.sg Forbidden Duck MBLM GP #02-02 Open 6509 8767 www.forbiddenduck.sg Harry's Bar MBLM GP#01-03 Open 6634 6318 http://harrys.com.sg/ Hey Bo MBLM #B2-41 Open 6974 6209 www.heybo.sg https://m.facebook.com/Men- ya-KAIKO- 616389838505564/menu/?p_r Hokkaido Ramen ef=pa&refsrc=https%3A%2F% MBFC T3 #01-01 Open 6509 8150 Men-ya KAIKO 2Fm.facebook.com%2Fpg%2 FMen-ya-KAIKO- 616389838505564%2Fmenu %2F&_rdr Shops operating hours may vary due to exigencies. -

Testview Based on DOHMH New York City Restaurant Inspection Results

TestView Based on DOHMH New York City Restaurant Inspection Results DBA INSPECTION DATE 04/26/2006 1 1001 NIGHTS CAFE 2 10 02 LOUNGE AND 15 RESTAURANT 100 FUN 33 100% MR LIN 4 101 CAFE 4 101 DELI 18 101 MEAT SHOP 42 101 TAIWAN STATION INC 1 101 WILSON BAR 11 1020 BAR 21 104-01 FOSTER AVENUE 16 COFFEE SHOP(UPS) 107 DAILY & GRILL 1 1080 BREW 32 108 DOUBLE CHINESE 12 RESTAURANT 108 FOOD DRIED HOT POT 10 10BELOW ICE CREAM 19 10TH AVENUE 1 Page 1 of 255 09/27/2021 TestView Based on DOHMH New York City Restaurant Inspection Results 10TH AVENUE COOKSHOP 28 10TH AVENUE PIZZA & CAFE 25 10TH FL CATERING 1 10TH FL FOOD HALL 1 10TH FLOOR LOUNGE 11 1107 Nostrand Ave Corp 1 110 KENNEDY FRIED CHICKEN 11 110 Nutrition 1 11:11 RESTAURANT LOUNGE 1 111 RESTAURANT 17 118 Kitchen 1 118 KITCHEN 15 11 HOWARD KITCHEN 5 11 STREET CAFE 17 11TH FL CLIENT DINING 1 11TH ST BAR 13 120 BAY CAFE 13 123 Burger Shot Beer 5 1 2 3 BURGER SHOT BEER 9 123 MARKET PLACE 1 123 NIKKO 26 124 CAFE 14 Page 2 of 255 09/27/2021 TestView Based on DOHMH New York City Restaurant Inspection Results 129 GOURMET DELI & 17 GROCERY 12 CHAIRS CAFE 38 12 CORAZONES RESTAURANT 43 & BAR 12 CORNERS COFFEE 12 12TH ST. ALE HOUSE 4 13106 GRAND EVERGREEN 12 CHINESE RESTAURANT 1392 SEAFOOD MUSIC BAR 5 141 EL KUCHO MEXICAN 6 RESTAURANT 146 NO. 1 YUMMY TACO 3 14 OLD FULTON STREET 3 151 ATLANTIC AVE CORP 1 151 JB BAR 1 1.5 DAK GALBI 20 15 EAST RESTAURANT 18 15 FLAVORS 2 15 FLAVORS NYC 4 15 STORIES 9 161 DELI & GRILL 2 Page 3 of 255 09/27/2021 TestView Based on DOHMH New York City Restaurant Inspection Results 161 HOT POT RICE 8 161 LAFAYETTE 2 167 Empanadas by chefs 1 168 HI TEA 25 168 KIM WEI KITCHEN 21 169 BAR 42 16 Handles 1 16 HANDLES 83 16TH AVENUE GLATT 8 173 WEBSTER CAFE 31 1803 NYC 39 1821 NOVELTY EATS 1 1847 INTERNATIONAL 14 1893 SPORTS BAR 5 18 BAKERY 51 18 BELOW 1 18 EAST GUNHILL PIZZA 8 18 HIPOT 18 18 LOUNGE KTV 15 18 RESTAURANT 14 18TH AVE CAFE G 7 18TH WARD BREWPUB 5 Page 4 of 255 09/27/2021 TestView Based on DOHMH New York City Restaurant Inspection Results 191 KNICKERBOCKER AVENUE 8 1927 Cafe Bar Popularr 1 197 NO. -

(Awarded in 6X STAR$®) with the American Express® Capitacard

Earn up to 3% rebate (Awarded in 6X STAR$®) with The American Express® CapitaCard Participating Merchants at CapitaLand Malls in town (S$1 spend = 30 STAR$®, T&Cs Apply) Updated as of 1 July 2021 Important Notes Please visit amex.co/capitacardterms for the full terms and conditions for earning STAR$® with your American Express® CapitaCard. Please note that under the terms and conditions: 1. Additional 25 STAR$® will be awarded, on top of the base 5 STAR$, on eligible purchases of goods and services, in blocks of S$1, on a cumulative basis at the end of every calendar month, capped at S$1,200 per calendar month. 2. On top of excluded charges and purchases, the following transactions are also not eligible to earn additional 25 STAR$®: charges at pushcarts, temporary vendors/pop-up shops, events, roadshows, SISTIC, SAM machines and AXS machines within CapitaLand Malls in town. American Express International Inc (UEN S68FC1878J) 1 Marina Boulevard #22-00, One Marina Boulevard, Singapore 018919. americanexpress.com.sg. Incorporated with Limited Liability in the State of Delaware, U.S.A ®Registered Trademark of American Express Company. © Copyright 2021 American Express Company. AXP Public 1 American Express® CapitaCard Participating Merchants @ Bugis Junction 200 Victoria Street Singapore 188021 Participating Merchant Name 6IXTY8IGHT Hi-Tec Mobile Polar Puffs & Cakes Action City HLH SABER LILY Pop Mart adidas HoneyMoon Dessert Premier Football Ajisen Ramen Honguo Purpur Akihabara HP By AddOn Q & M Dental Centre (Bugis) Alcoholiday HUAWEI Raffles -

How Much Do Japanese Really Care About Food Origin? a Case of Beef Bowl Shop Koichi Yamaura Department of International Environm

How Much Do Japanese Really Care about Food Origin? A Case of Beef Bowl Shop Koichi Yamaura Department of International Environmental and Agricultural Science Tokyo University of Agriculture and Technology [email protected] Hikaru Hanawa Peterson Department of Applied Economics University of Minnesota [email protected] Selected Poster prepared for presentation at the 2016 Agricultural & Applied Economics Association Annual Meeting, Boston, MA, July 31 – Aug. 2. Copyright 2016 by Koichi Yamaura and Hikaru Hanawa Peterson. All rights reserved. Readers may make verbatim copies of this document for non-commercial purposes by any means, provided this copyright notice appears on all such copies. How Much Do Japanese Really Care about Food Origin? A Case of Beef Bowl Shop Koichi Yamaura*1 and Hikaru Hanawa Peterson2 1Assistant Professor, Dept. of International Environmental & Agricultural Science, Tokyo University of Agriculture & Technology. [email protected] 2 Professor, Dept. of Applied Economics, University of Minnesota. [email protected] Problem Identification Objectives Results Gyudon, or beef bowl, is one of Japanese popular fast foods Examines the preferences of Japanese consumers toward food Latent Class model & WTP results Table 3. Latent Class model results for Beef Bowl consisting of a bowl of rice topped with beef and onion origins including beef, after the 3.11 Earthquake and the Meal Ingredients Class Probability Model Meal Ingredients focused focused focused focused simmered in a mildly sweet sauce flavored with soy sauce and Fukushima nuclear disaster and resumption of U.S. beef trade. PRICE -0.0198 *** -0.0119 ** FEMALE -1.2522 *** -- (0.0010) (0.0052) (0.2092) other seasoning. -

House of Cards Season 5 Vendor List

House of Cards ‐ Season 5 Maryland Vendor List The following list of Maryland vendors has been compiled and submitted by the production company, Knight Takes King Productions, Inc., for Season 5 of the Netflix series House of Cards . The entities listed here provided goods or services to the production. In addition, the production company was required to research and designate those entities that qualify as a Minority Business Enterprise (MBE) and/or are considered Small Businesses (SBE). The Department provided the production company with a link to the MBE website housed within the Department of Transportation which is the State's official certification program for MBE's, as well as a link to the eMaryland M@rketplace website housed within the Department of General Services which provides a listing of Small Businesses as sanctioned by the State. Those entities marked with an "Y" under M/O were registered on the State sanctioned website. Those entities marked with an "N" were not registered on the State sanctioned website. This does not mean that they are not minority owned, only that they are not registered as such with the State. Those marked with a "Y" under Small Business were registered as a small business on the State sanctioned website. Those marked with a "N" were not registered as a small business on the State sanctioned website. This does not mean that they are not a small business, only that they are not registered as such with the State. HOUSE OF CARDS ‐ SEASON 5 Total Number of Vendors: 1757 Vendor Information for Tax Credit VENDOR ADDRESS CITY STATE ZIP PHONE #M/OSMALL BUSINESS & Pizza 1201 S. -

Cfc) Cbd Ciledug

ISSN 23376686 ISSNL 23383321 STRATEGI DALAM MENINGKATKAN KUALITAS PRODUK PADA CALIFORNIA FRIED CHICKEN (CFC) CBD CILEDUG Endang Suparni dan Suharini Universitas Bina Sarana Indonesia Email: [email protected], [email protected] ABSTRAK: Dalam tingkat persaingan yang semakin tajam. Setiap perusahaan dituntut untuk mampu menciptakan strategi yang tepat agar dapat berkompetitif dalam memenangkan persaingan, terutama dalam hal kualitas produk. Kualitas A yang tinggi agar unggul dalam persaingan bisnis. Produk dikatakan berkualitas apabila dapat memenuhi kebutuhan dan melebihi harapan konsumen atau pelanggan. Dampak yang ditimbulkan dengan kualitas produk yang tinggi adalah produk tetap diminati konsumen sehingga tetap eksis di pasaran. Tujuan penelitian ini adalah untuk mengetahui upaya peningkatan kualitas produk California Fried Chicken (CFC). Metode penelitian yang digunakan deskriptif kualitatif. Variabel yang diteliti adalah kualitas produk. Teknik pengumpulan data dilakukan dengan observasi, wawancara, dan studi pustaka. Teknik pengolahan data dilakukan dengan tabulasi. Analisis data dilakukan dengan deskrptif dan kualitatif. Hasil penelitian menunjukkan CFC mengutamakan kualitas produk dengan menyetarakan standar kualitas produk lokal sehingga dapat bersanding dengan produk ayam goreng cepat saji yang berasal dari Amerika seperti KFC. CFC dikenal dengan cita rasa ayam gorengnya yang nikmat dan gurih, juga menyediakan menu lainnya. Terdapat empat konsep dasar yang menjadi dasar pegangan dalam pengawasan kualitas produk, yaitu: Discipline, Quality, Service, dan Cleanliness. CFC terus berupaya dalam meningkatkan kualitas produknya agar dapat dikonsumsi sesuai dengan selera dan keinginan konsumen, antara lain; penyempurnaan kualitas produk, penyempurnaan ciri khas, keanekaragaman produk, dan penyempurnaan corak. Kesimpulan yakni CFC memiliki kualitas produk makanan siap saji yang baik sesuai dengan standar produk restoran internasional, seperti KFC. -

Pengaruh Budaya Imperatif, Budaya Adiafora Dan Budaya Eksklusif Terhadap Keputusan Pembelian Produk Internasional Mcdonald’S Oleh: Alisia Melinda Purnama

Pengaruh Budaya Imperatif, Budaya Adiafora Dan Budaya Eksklusif Terhadap Keputusan Pembelian Produk Internasional Mcdonald’s Oleh: Alisia Melinda Purnama Pendahuluan Fast food merupakan makanan yang lebih mengutamakan cita rasa daripada kandungan gizi. Misalnya, keripik kentang yang mengandung garam. Beberapa junk food juga mengandung banyak gula misalnya, minuman bersoda, permen dan kue tar. Gula, tertutama gula buatan sangat tidak baik bagi kesehatan tubuh kita karena dapat menyebabkan penyakit diabetes, kerusakan pada gigi kita dan menyebabkan obesitas. Minuman bersoda mengandung paling banyak gula, sementara kebutuhan gula dalam tubuh tidak boleh lebih dari 4 gram atau satu sendok teh sehari (Griffindors (2013)). Pada masa ini di Indonesia restoran fast food sudah sangat berkembang pesat. Seperti KFC (Kentucky Fried Chicken) yang pada saat ini sudah memiliki sekitar 540 gerai diseluruh Indonesia. Tahun 2016 diperkirakan ada tambahan 40 gerai lagi. KFC mudah disukai di Indonesia karena memajang menu ayam. Dikombinasikan dengan nasi, ini jelas bukan rasa yang asing di lidah warga Indonesia. Karena itu, tak perlu perkenalan atau adaptasi lidah terhadap menu-menu KFC. (tirto.id 2016)). Selain KFC, Burger King juga salah satu restoran fast food yang cukup berkembang di Indonesia. Burger King mulai dioperasikan oleh Mitra Adiperkasa (yang juga mengoperasikan waralaba Starbucks), pada bulan April 2007, dengan outlet pertamanya di Senayan City, Jakarta. Saat ini, Burger King memiliki cabang-cabang di Jakarta, Bandung, Surabaya, Bali dan Lombok. (id.wikipedia.org). Restoran fast food yang berkembang pesat juga di Indonesia adalah McDonald’s. Pada awalnya, McDonald’s hanya menyajikan makanan yang berupa hamburger, ice cream, kentang goreng dan minuman bersoda. Setelah McDonald’s memasuki pasar di Indonesia, harus menyesuaikan dengan lidah masyarakat Indonesia yang menjadikan nasi sebagai makanan pokoknya.