Proposed Statement of Accounts Content

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Playing Pitch Strategy and Action Plan 2019

THREE RIVERS DISTRICT COUNCIL PLAYING PITCH STRATEGY & ACTION PLAN APRIL 2019 QUALITY, INTEGRITY, PROFESSIONALISM Knight, Kavanagh & Page Ltd Company No: 9145032 (England) MANAGEMENT CONSULTANTS Registered Office: 1 -2 Frecheville Court, off Knowsley Street, Bury BL9 0UF T: 0161 764 7040 E: [email protected] www.kkp.co.uk THREE RIVERS DISTRICT COUNCIL PLAYING PITCH STRATEGY CONTENTS ABBREVIATIONS ............................................................................................................. 1 PART 1: INTRODUCTION ................................................................................................ 2 PART 2: VISION ............................................................................................................. 14 PART 3: AIMS................................................................................................................. 15 PART 4: SPORT SPECIFIC ISSUES SCENARIOS AND RECOMMENDATIONS .......... 16 PART 5: STRATEGIC RECOMMENDATIONS ............................................................... 34 PART 6: ACTION PLAN .................................................................................................. 50 PART 7: HOUSING GROWTH SCENARIOS .................................................................. 71 PART 8: DELIVER THE STRATEGY AND KEEP IT ROBUST AND UP TO DATE ......... 73 APPENDIX 1: SPORTING CONTEXT ............................................................................ 79 APPENDIX TWO: FUNDING PLAN ............................................................................... -

Annex a - Secondary Schools 2016/17 If an Academy)

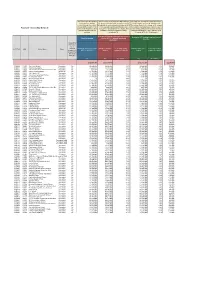

The school's baseline funding These columns show illustrative NFF funding if In the first year of transition towards the formula, is the total core funding the proposed formula had been implemented in LAs will continue to determine funding locally. received through the schools full and without any transitional protections in 2016- This column illustrates the change in the amount block and MFG in 2016-17 (or 17. We use pupil numbers and characteristics the department would allocate to LAs in respect Annex A - Secondary Schools 2016/17 if an academy). Other from 2016-17 to illustrate the NFF impact, and of each school, taking into account the maximum grants/funding sources are compare to the school's baseline funding, change proposed in NFF year 1 (gains of up to excluded. including MFG. 3% and an MFG of -1.5% per pupil). Illustrative NFF funding if formula implemented Illustrative NFF funding in the first year of Baseline funding in full in 2016-17, without transitional transition protections Has data for this school been excluded, Funding the school received in Illustrative total NFF Percentage change Illustrative NFF year 1 Percentage change LAESTAB URN School Name Phase because it is 2016-17 or 2016/17 funding compared to baseline funding compared to baseline a new school that is still filling up? [a] [b] [c] = [b]/[a] - 1 [d] [e] = [d]/[a] - 1 £328,011,000 £323,834,000 £325,767,000 -£2,244,000 9194000 117499 The Priory School Secondary No £4,506,000 £4,540,000 0.8% £4,540,000 0.8% £34,000 9194001 138747 Hertswood Academy Secondary -

School Allocation Summary Report - Main Allocation Day - 02/03/2020 NOTES

HERTFORDSHIRE COUNTY COUNCIL CHILDREN’S SERVICES Secondary / Upper / Yr 10 Transfer School Allocation Summary Report - Main Allocation Day - 02/03/2020 NOTES: 1. To view the allocation summary for a specific school, click on the school name in the Index. 2. To print the allocation summary for a specific school, click File > Print, and then specify the page numbers from the index below. School Town Phase Page Adeyfield Academy (The) Hemel Hempstead Secondary 3 Ashlyns School Berkhamsted Secondary 4 Astley Cooper School (The) Hemel Hempstead Secondary 5 Barclay Academy Stevenage Secondary 6 Barnwell School Stevenage Secondary 7 Beaumont School St Albans Secondary 8 Birchwood High School Bishop's Stortford Secondary 9 Bishop's Hatfield Girls' School Hatfield Secondary 10 Bishop's Stortford High School (The) Bishop's Stortford Secondary 12 Broxbourne School (The) Broxbourne Secondary 13 Bushey Academy (The) Bushey Secondary 14 Bushey Meads School Bushey Secondary 15 Chancellor's School Brookmans Park Secondary 16 Chauncy School Ware Secondary 17 Croxley Danes School Croxley Green Secondary 18 Dame Alice Owen's School Potters Bar Secondary 19 Elstree University Technical College Elstree Year 10 20 Fearnhill School Maths and Computing College Letchworth Secondary 21 Francis Combe Academy Garston Secondary 22 Freman College Buntingford Upper 23 Goffs Academy Cheshunt Secondary 24 Goffs-Churchgate Academy Cheshunt Secondary 25 Haileybury - Turnford School Cheshunt Secondary 26 Hemel Hempstead School (The) Hemel Hempstead Secondary 27 Hertfordshire -

Royal Holloway University of London Aspiring Schools List for 2020 Admissions Cycle

Royal Holloway University of London aspiring schools list for 2020 admissions cycle Accrington and Rossendale College Addey and Stanhope School Alde Valley School Alder Grange School Aldercar High School Alec Reed Academy All Saints Academy Dunstable All Saints' Academy, Cheltenham All Saints Church of England Academy Alsop High School Technology & Applied Learning Specialist College Altrincham College of Arts Amersham School Appleton Academy Archbishop Tenison's School Ark Evelyn Grace Academy Ark William Parker Academy Armthorpe Academy Ash Hill Academy Ashington High School Ashton Park School Askham Bryan College Aston University Engineering Academy Astor College (A Specialist College for the Arts) Attleborough Academy Norfolk Avon Valley College Avonbourne College Aylesford School - Sports College Aylward Academy Barnet and Southgate College Barr's Hill School and Community College Baxter College Beechwood School Belfairs Academy Belle Vue Girls' Academy Bellerive FCJ Catholic College Belper School and Sixth Form Centre Benfield School Berkshire College of Agriculture Birchwood Community High School Bishop Milner Catholic College Bishop Stopford's School Blatchington Mill School and Sixth Form College Blessed William Howard Catholic School Bloxwich Academy Blythe Bridge High School Bolton College Bolton St Catherine's Academy Bolton UTC Boston High School Bourne End Academy Bradford College Bridgnorth Endowed School Brighton Aldridge Community Academy Bristnall Hall Academy Brixham College Broadgreen International School, A Technology -

Atlantic Academy Portland 08/09/2017 Deficit

Academy in Receipt Date of Receipt Description Amount (£) Atlantic Academy Portland 08/09/2017 Deficit - Non-Recoverable 300,000.00 Atlantic Academy Portland 08/12/2017 Deficit - Non-Recoverable 518,326.09 Bourne End Academy 01/04/2017 Deficit - Non-Recoverable 150,000.00 Collective Spirit Free School 01/09/2017 Deficit - Non-Recoverable 119,000.00 Daventry University Technical College (UTC) 06/04/2017 Deficit - Non-Recoverable 50,000.00 Daventry UTC 02/05/2017 Deficit - Non-Recoverable 70,000.00 Greater Manchester Sustainable Engineering UTC 03/04/2017 Deficit - Non-Recoverable 40,000.00 Greater Manchester Sustainable Engineering UTC 02/05/2017 Deficit - Non-Recoverable 40,000.00 Greater Manchester Sustainable Engineering UTC 01/06/2017 Deficit - Non-Recoverable 40,000.00 Greater Manchester Sustainable Engineering UTC 03/07/2017 Deficit - Non-Recoverable 30,000.00 Greater Manchester Sustainable Engineering UTC 06/07/2017 Deficit - Non-Recoverable 71,000.00 Heathrow Aviation Engineering UTC 08/03/2018 Deficit - Non-Recoverable 20,000.00 Isle of Portland Aldridge Community Academy 06/04/2017 Deficit - Non-Recoverable 228,000.00 Isle of Portland Aldridge Community Academy 01/08/2017 Deficit - Non-Recoverable 257,500.00 Martello Grove Academy 01/11/2017 Deficit - Non-Recoverable 16,485.00 Morehall Primary 01/12/2017 Deficit - Non-Recoverable 87.55 Patchway Community College 04/08/2017 Deficit - Non-Recoverable 227,000.00 Plumberow Primary School 01/03/2018 Deficit - Non-Recoverable 773,000.00 Ringmer Community College 06/07/2017 Deficit - -

South West Herts Economic Study Final Report Final

South West Herts Economic Study Update A Final Report by Hatch Regeneris 5 September 2019 South West Herts Authorities South West Herts Economic Study Update 5 September 2019 www.hatchregeneris.com South West Herts Economic Study Update Contents Page Executive Summary i Aims of the Study i Functional Economic Market Area i Policy Context ii Recent Economic Performance iii Commercial Property Market Trends iv Future Growth Scenarios v Demand and Supply Balance viii 2. Introduction and Purpose of Study 1 3. Economic Geography of South West Herts 2 Functional Economic Market Area 2 Relationship with neighbouring areas 6 4. Recent changes in policy 15 Planning Policy 15 Economic Policy 17 5. Economic and Labour Market Performance 21 Recent Economic Performance 21 Analysing the Five Foundations of Productivity in South West Herts 26 6. Commercial Property Market Trends 54 Office Market Review 54 Industrial market review 65 7. Future Growth Scenarios 72 Employment-led Scenario 72 Labour Supply Scenario 87 Higher Growth Scenario 92 Trends Based Scenario 99 Replacement Demand 104 Conclusions 105 South West Herts Economic Study Update 8. Supply of Employment Land 112 9. Demand and Supply Balance 126 Office market balance 126 Industrial market balance 128 10. Conclusions and Recommendations 131 Appendix A - Inacuracies in Employment Datasets Appendix B - Ratios for converting total employment in to FTEs Appendix C - Method for allocating sectors to use classes Appendix D - Site Reviews South West Herts Economic Study Update Executive Summary Aims of the Study i. This report provides an update of the South West Hertfordshire Economic Study which was published in January 2016. -

Annual Report 2017

Annual Report 2017 Published February 2018 Challenge Partners is a Contents 1. THE PARTNERSHIP 2 practitioner-led education About Challenge Partners 3 Message from the Chief Executive 4 charity that enables Our principles and approach 6 collaboration between Challenge Partners by numbers 10 2. OUR COLLECTIVE AIMS 12 It is possible to have both excellence 13 schools to enhance the and equity in our education system Our aims 16 life chances of all children, Impact and performance against our aims 17 3. THE PROGRAMMES 20 especially the most Our programmes 21 The Network of Excellence 22 disadvantaged. Hubs 24 The Quality Assurance Review 27 Leadership Development Days 32 Leadership Residency Programme 32 School Support Directory 32 Events 33 Challenge the Gap 34 Getting Ahead London 40 EAL in the mainstream classroom 43 4. FINANCES 44 Income and expenditure 44 5. LOOKING FORWARD 45 6. LIST OF CHALLENGE PARTNERS SCHOOLS 46 1. The partnership About Challenge Partners Challenge Partners is a practitioner-led education charity that enables collaborative school improvement networks to enhance the life chances of all children, especially the most disadvantaged. Challenge Partners was formed to continue the learning which emerged from the development of Teaching Schools that evolved out of the London Challenge. Since its formation in 2011, the outcomes for pupils in Challenge Partners schools have consistently improved faster than the national average. We provide networks and programmes that facilitate sustainable collaboration and challenge between schools in order to underpin improvements in outcomes which would not be possible for a school, or group of schools, to achieve as effectively on its own. -

Education Indicators: 2022 Cycle

Contextual Data Education Indicators: 2022 Cycle Schools are listed in alphabetical order. You can use CTRL + F/ Level 2: GCSE or equivalent level qualifications Command + F to search for Level 3: A Level or equivalent level qualifications your school or college. Notes: 1. The education indicators are based on a combination of three years' of school performance data, where available, and combined using z-score methodology. For further information on this please follow the link below. 2. 'Yes' in the Level 2 or Level 3 column means that a candidate from this school, studying at this level, meets the criteria for an education indicator. 3. 'No' in the Level 2 or Level 3 column means that a candidate from this school, studying at this level, does not meet the criteria for an education indicator. 4. 'N/A' indicates that there is no reliable data available for this school for this particular level of study. All independent schools are also flagged as N/A due to the lack of reliable data available. 5. Contextual data is only applicable for schools in England, Scotland, Wales and Northern Ireland meaning only schools from these countries will appear in this list. If your school does not appear please contact [email protected]. For full information on contextual data and how it is used please refer to our website www.manchester.ac.uk/contextualdata or contact [email protected]. Level 2 Education Level 3 Education School Name Address 1 Address 2 Post Code Indicator Indicator 16-19 Abingdon Wootton Road Abingdon-on-Thames -

List of Eligible Schools for Website 2019.Xlsx

England LEA/Establishment Code School/College Name Town 873/4603 Abbey College, Ramsey Ramsey 860/4500 Abbot Beyne School Burton‐on‐Trent 888/6905 Accrington Academy Accrington 202/4285 Acland Burghley School London 307/6081 Acorn House College Southall 931/8004 Activate Learning Oxford 307/4035 Acton High School London 309/8000 Ada National College for Digital Skills London 919/4029 Adeyfield School Hemel Hempstead 935/4043 Alde Valley School Leiston 888/4030 Alder Grange School Rossendale 830/4089 Aldercar High School Nottingham 891/4117 Alderman White School Nottingham 335/5405 Aldridge School ‐ A Science College Walsall 307/6905 Alec Reed Academy Northolt 823/6905 All Saints Academy Dunstable Dunstable 916/6905 All Saints' Academy, Cheltenham Cheltenham 301/4703 All Saints Catholic School and Technology College Dagenham 879/6905 All Saints Church of England Academy Plymouth 383/4040 Allerton Grange School Leeds 304/5405 Alperton Community School Wembley 341/4421 Alsop High School Technology & Applied Learning Specialist College Liverpool 358/4024 Altrincham College Altrincham 868/4506 Altwood CofE Secondary School Maidenhead 825/4095 Amersham School Amersham 380/4061 Appleton Academy Bradford 341/4796 Archbishop Beck Catholic Sports College Liverpool 330/4804 Archbishop Ilsley Catholic School Birmingham 810/6905 Archbishop Sentamu Academy Hull 306/4600 Archbishop Tenison's CofE High School Croydon 208/5403 Archbishop Tenison's School London 916/4032 Archway School Stroud 851/6905 Ark Charter Academy Southsea 304/4001 Ark Elvin Academy -

2020 Aston Ready School and College List

School/College Name Postcode The Marlborough Science Academy AL1 2QA Townsend CofE School AL3 6DR Oaklands College AL4 0JA Sir Frederic Osborn School AL7 2AF Small Heath School B10 9RX George Dixon Academy B16 9GD Lordswood Girls' School and Sixth Form Centre B17 8QB Holte School B19 2EP Nishkam High School B19 2LF Hamstead Hall Academy B20 1HL King Edward VI Handsworth Wood Girls' Academy B20 2HL Broadway Academy B20 3DP Shenley Academy B29 4HE Central Academy B3 1SJ Greenwood Academy B35 7NL Smith's Wood Academy B36 0UE Park Hall Academy B36 9HF WMG Academy for Young Engineers (Solihull) B37 5FD John Henry Newman Catholic College B37 5GA Grace Academy Solihull B37 5JS CTC Kingshurst Academy B37 6NU Cadbury Sixth Form College B38 8QT Birmingham Metropolitan College B4 7PS Birmingham Ormiston Academy B4 7QD Q3 Academy B43 7SD North Birmingham Academy B44 0HF Great Barr Academy B44 8NU Waseley Hills High School B45 9EL The Coleshill School B46 3EX South and City College Birmingham B5 5SU North Bromsgrove High School B60 1BA Halesowen College B63 3NA Windsor High School and Sixth Form B63 4BB Ormiston Forge Academy B64 6QU Shireland Collegiate Academy B66 4ND Holly Lodge High School College of Science B67 7JG Perryfields High School Specialist Maths and Computing College B68 0RG Oldbury Academy B68 8NE Ormiston Sandwell Community Academy B69 2HE Aston University Engineering Academy B7 4AG Heartlands Academy B7 4QR Sandwell College B70 6AW Health Futures UTC B70 8DJ Sandwell Academy B71 4LG John Willmott School B75 7DY Fairfax B75 7JT Landau -

Allocation Summary Report - Continuing Interest 2 - 29/04/2021

HERTFORDSHIRE COUNTY COUNCIL CHILDREN’S SERVICES iire Secondary / Upper / Yr 10 Transfer School Allocation Summary Report - Continuing Interest 2 - 29/04/2021 NOTES: 1. To view the allocation summary for a specific school, click on the school name in the Index. 2. To print the allocation summary for a specific school, click File > Print, and then specify the page numbers from the index below. School Town Phase Page Adeyfield Academy (The) Hemel Hempstead Secondary 3 Ashlyns School Berkhamsted Secondary 4 Astley Cooper School (The) Hemel Hempstead Secondary 5 Barclay Academy Stevenage Secondary 6 Barnwell School Stevenage Secondary 7 Beaumont School St Albans Secondary 8 Birchwood High School Bishop's Stortford Secondary 9 Bishop's Hatfield Girls' School Hatfield Secondary 10 Bishop's Stortford High School (The) Bishop's Stortford Secondary 12 Broxbourne School (The) Broxbourne Secondary 13 Bushey Meads School Bushey Secondary 14 Chancellor's School Brookmans Park Secondary 15 Chauncy School Ware Secondary 16 Croxley Danes School Croxley Green Secondary 17 Dame Alice Owen's School Potters Bar Secondary 18 Elstree University Technical College Elstree Year 10 19 Fearnhill School Maths and Computing College Letchworth Secondary 20 Freman College Buntingford Upper 21 Future Academies Watford (previously Francis Combe Academy) Garston Secondary 22 Goffs Academy Cheshunt Secondary 23 Goffs-Churchgate Academy Cheshunt Secondary 24 Grange Academy (previously Bushey Academy) (The) Bushey Secondary 25 Haileybury - Turnford School Cheshunt Secondary -

List of Schools Who Parents Should Contact Direct Re Admissions.Xlsx

Secondary and Upper Schools and University Technical Colleges that administer their own admission arrangements Please contact these schools direct for information about how your application was considered. Contact details are available for all schools at www.hertfordshire.gov.uk/schooldirectory School Town School Name School DfE Code School Type Bishop's Stortford Birchwood High School 9194200 Academy Bishop's Stortford Bishop's Stortford High School (The) 9195405 Foundation Bishop's Stortford Hertfordshire And Essex High School and Science College (The) 9195420 Academy Bishop's Stortford Hockerill Anglo-European College 9195427 Academy Bishop's Stortford St Mary's Catholic (Bishops Stortford) 9195422 Voluntary Aided Borehamwood Yavneh College 9194802 Academy Brookmans Park Chancellor's School 9195419 Academy Bushey Grange Academy (The) (previously Bushey Academy) 9194036 Academy Bushey Queens' School 9195410 Academy Cheshunt Goffs Academy 9195415 Academy Cheshunt Goffs-Churchgate Academy 9195425 Academy Cheshunt St Mary's Church of England High School 9195423 Academy Chorleywood St Clement Danes School 9195421 Academy Croxley Green Croxley Danes School 9194025 Academy Garston Parmiter's School 9195404 Academy Garston St Michael's Catholic High School 9195417 Academy Harpenden St George's School 9194614 Academy Hemel Hempstead John F Kennedy Roman Catholic School 9194619 Voluntary Aided Hoddesdon John Warner School (The) 9195426 Academy Potters Bar Dame Alice Owen's School 9195407 Academy Potters Bar Mount Grace School 9195411 Academy