IR Corporate Presentation Agenda

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Department of Chemistry Annual Report 2019

Department of Chemistry Annual Report 2019 Scan the QR-code and read more at kemi.dtu.dk DTU Technical University of Denmark Department of Chemistry Kemitorvet Building 207 DK-2800 Kgs. Lyngby kemi.dtu.dk Picture: Greg Stewart/SLAC A well-tuned Department The DTU Chemistry Management Group (left to right) Lise Peitersen, Erling H. Stenby, Jens O. Duus, Inge Holkmann Olsen, and Klaus B. Møller. Content Welcome to the DTU Chemistry Annual Report In 2019, the researchers of DTU Chemistry and we are glad to present some of these expanded by approximately 12 % to 66 new 2019 – a year characterized by innovation, were very productive. The number of researchers as seminar speakers. These students in 2019. 3 Welcome evaluation, and academic excellence. Peer-Reviewed articles (228) rose by 30 % inspiring talks are fueling new ideas at the 4 Faculty: Synergy as compared to 2018. Three very promising Department. In 2019, a record number of 26 PhD students a driving force In the fall, an international research evaluation patents were obtained and currently, we began their research at the Department 6 Recruiting enzymes for panel consisting of four international have 28 ongoing patent-cases. In addition, Significant external funding has once again while 17 graduated. It is inspiring to see how new tasks in chemistry researchers visited the Department to scruti nize several DTU Chemistry spin-out companies strengthened our research groups with productive our PhD school is. Our research our activities. The overall feedback was very are flourishing with new investments and talents from Denmark and abroad. It has also groups benefit vastly from the curiosity 8 A peek into the molecular positive. -

Annual Report 2006 Carlsberg A/S Annual Report 2006

Carlsberg A/S Annual Report 2006 Annual Report 2006 Management review 1 Profi le 2 CEO statement 4 Five-year summary 5 Results and expectations 7 Strategy 10 Markets 12 Western Europe 16 Baltic Beverages Holding 20 Eastern Europe excl. BBH 24 Asia 28 Other activities 30 People and management 34 Social and environmental responsibility 38 Shareholder information 42 Corporate governance 47 Risk management 49 Financial review Financial statements 57 Consolidated fi nancial statements 58 Income statement 59 Statement of recognised income and expenses for the year 60 Balance sheet 62 Statement of changes in equity 63 Cash fl ow statement 64 Notes 110 Group companies Carlsberg A/S 113 Parent Company fi nancial statements CVR No. 61056416 Ny Carlsberg Vej 100 134 Management statement DK-1760 Copenhagen V, Denmark 135 Auditor’s report Phone: +45 3327 3300 136 Board of Directors, Executive Board and Fax: +45 3327 4701 other senior executives E-mail: [email protected] www.carlsberg.com This report is provided in Danish and in English. In case of any discrepancy between the two versions, the Danish wording shall apply. Probably the best … Carlsberg is one of the world’s largest brewery groups. We have a beer for every occasion and for every palate and lifestyle. The Group’s broad portfolio of beer brands includes Carlsberg Pilsner, known as Probably the best beer in the world, and strong regional brands such as Tuborg, Baltika and Holsten. We also have a wide range of leading brands in our local markets. We operate primarily in mature markets in Western Europe but are generating an ever-growing share of revenue in selected growth markets in Eastern Europe and Asia. -

04Carlsberg 'Our City'

EXPLORING CARLSBerg 04 ’OUR CIty’ 25 FantastiC INDUSTRIES SEE WWW.25FANTASTISKE.DK At the end of 2008, the Carlsberg Breweries turned off the taps at the Valby brewery, relocating production to Fredericia. From 2009 onwards Brewer Jacobsen’s Carlsberg estate, between the Vesterbro and Valby districts, will undergo radical redevelopment as a new district incorporating a wealth of listed and preservation- worthy buildings and gardens. FOLD HERE // CARLSBerg ’our cITy’ HUMLEBY SØNDERMARKEN 04 09 03 02 vaLBY LANGGADE NY CARLSBERG VEJ 05 10 07 07 GAMLE CARLSBERG VEJ 06 01 08 VESTER FÆLLED VEJ CARLSBERG JERNBANE VIGERSLEV ALLÉ NY CARLSBERGVEJ 100 1760 COPENHAGEN V FOLD HERE OLD CARLSBerg NEW CARLSBerg 03 ENTRANCE J.C. Jacobsen, master brewer, had enjoyed so much success J.C. Jacobsen’s son Carl also became a brewer. He rented The Dipylon Gate (dipylon from Greek, meaning double gate) brewing bottom-fermented beer at his father’s brewery in his father’s Annex Building (anneksbyggeriet). Soon after, he served as a portal to the New Carlsberg Brewery from the Brolæggerstræde since 1826 that by 1847 the premises had acquired Bakkegården, the neighbouring property, where he Vesterbro side. It was designed by Vilhelm Dahlerup and was become cramped and outdated. Meanwhile, Zealand’s first set about building a new brewery in 1880-81. This, among erected in 1892. Dahlerup also designed the Elephant Gate, railway was being built to connect Copenhagen with Roskilde, other things, caused the father to terminate his son’s lease which was completed in 1901. and when the railway company began laying tracks near Valby and assume sole charge of the original brewery from 1882. -

Reporting of the Graduate Survey

KØBENHAVNS UNIVERSIT ET REPORTING OF THE GRADUATE SURVEY Bachelor, Academic Bachelor, Master Degree Table of contents 1 Introduction 4 2 Data 5 2.2 Background data from the study administrative system STADS 6 2.3 Reading guide 6 3 Current job situation of Master’s Candidatus/Professional Bachelor’s graduates 9 3.1 Employed Master’s Candidatus/Professional Bachelor’s graduates 9 3.2 Self-employed (including freelance) 19 3.3 Unemployed, including maternity leave without being under employment contract 24 4 Correlation between Master’s Candidatus/Professional Bachelor’s education programmes and the job market 27 4.1 Academic correlation between studies and job 27 4.2 The ability of the study programme to prepare the graduates for working life 27 5 Master’s Candidatus/Professional Bachelor’s graduates routes to their first job 34 5.1 Master’s Candidatus/Professional Bachelor’s graduates first job 34 5.2 The significance of student jobs, internships, study abroad, etc. for the first job 38 5.3 Voluntary internship or project in private or public organisations 40 5.4 Study abroad 42 5.5 Activities during the programme of study such as student politics 44 6 Master's Candidatus/Professional bachelor's assessment of the program compared with their own expectations 46 7 The Master Candidatus graduates assessment of the study programme 48 7.1 The level of teaching in relation to the entry requirements 48 7.2 Specifics about the Master's Candidatus program 50 7.3 The graduates assessment of the opportunities for study abroad, internship etc. without extensions 51 7.4 The teacher's professional and educational expertise 52 8 Bachelor's/Professional Bachelor's assessment of the study programme 53 8.1 The level of teaching in relation to the entry requirements 53 8.2 Specifics about the bachelor programme 53 8.3 The graduates assessment of the opportunities for study abroad, internship etc. -

Years of Beer Discoveries Annual Report 2017

Carlsberg Brewery Malaysia Berhad (9210-K) (9210-K) Berhad Malaysia Brewery Carlsberg Annual Report 2017 Annual Report YEARS OF BEER DISCOVERIES ANNUAL REPORT 2017 Carlsberg Brewery Malaysia Berhad (9210-K) No. 55, Persiaran Selangor, Section 15 40200 Shah Alam, Selangor Darul Ehsan, Malaysia Tel : +603 5522 6688 Fax : +603 5519 1931 www.carlsbergmalaysia.com.my TABLE OF CONTENTS Carlsberg Malaysia Group at a Glance 2 Financial Statements..........................................................................93 Chairman’s Address 4 Carlsberg Malaysia’s Sales Offices 176 Our Portfolio of Brands 6 Particulars of Group Properties 177 2017 Brand Highlights 8 Analysis of Shareholdings 178 Managing Director’s Message and Material Contracts 180 Management Discussion and Analysis 24 List of Recurrent Related Party Transactions 181 Sustainability Statement 38 Notice of Annual General Meeting 183 Management Team 64 Statement Accompanying Notice of Profile of Management Team 66 Annual General Meeting 188 Profile of the Directors 68 Corporate Governance Overview Statement 72 Form of Proxy Statement on Risk Management & Corporate Information Internal Control 85 Audit & Risk Management Committee Report 89 Responsibility Statement by the Board of Directors 92 Year 2017 marked Probably The Best 170th Anniversary Celebration for Carlsberg in beer discoveries. For 170 years, we have been brewing for a better today and tomorrow and here at Carlsberg Malaysia Group, we continue to pursue perfection every day by perfecting the art of brewing, giving consumers -

Baltic Beverages Holding Christian Ramm-Schmidt President and CEO of BBH

Baltic Beverages Holding Christian Ramm-Schmidt President and CEO of BBH 16 June 1999 1 16.06.99 13:43 Agenda Introduction Strategy Development in Russia, Ukraine and the Baltic States Outlook 2 16.06.99 13:43 BBH Swedish registered company located in Stockholm − Established jointly by Hartwall and Pripps in 1991 BBH has expanded rapidly since 1991 Interests in eleven breweries and eight malteries in Russia, Ukraine and the Baltic States Leading player on the brewery markets in this region 3 16.06.99 13:43 BBH - Ownership structure Pripps Hartwall Ringnes 50% 50% BBH Russia Ukraine Baltic States Breweries Baltika (74%) Slavutich (70%) Kalnapilis (86%) - Lithuania Don Pivo (83%)* Kolos (92%)** Utenos Alus (50%) - Lithuania Yarpivo (53%) Aldaris (75%) - Latvia Taopin (69%) Saku (75%) - Estonia Chelyabinskpivo (75%**) Malteries Baltika (30%) Slavuta (66%) Litmalt (50%) - Lithuania Yarpivo (100%) Kolos (100%) Utenos (100%) - Lithuania Taopin (100%) Chelyabinskpivo (100%**) * Owned by Baltika ** After agreed ownership increases 4 16.06.99 13:43 BBH - A Successful Strategy Acquire majority interests in local breweries − Local brands − Local management − Local ownership Quality improvements − Modern technology − Beer of western quality − Extensive personnel development Support from BBH in marketing, sales and distribution Brand strategy with focus on main stream quality segment Volume growth through capacity expansion BBH “Family concept” 6 16.06.99 13:43 BBH - Sales volumes 1991-1998 Million litres 913 639 460 202 160 74 14 33 -

2012 Catalogue of Results Proudly Conducted By

2012 Catalogue of Results Proudly conducted by 2012 Catalogue of Results The Royal Agricultural Society of Victoria Limited ABN 66 006 728 785 ACN 006 728 785 Melbourne Showgrounds Epsom Road Ascot Vale Victoria 3032 Telephone +61 3 9281 7444 Facsimile +61 3 9281 7592 www.rasv.com.au List of Office Bearers As at 01/05/2012 Board of Directors S. C. Spargo (Chair) D. Pollett Hodgson (VIce Chair) I. I. Bucknall D. S. Chapman M. J. Coleman A. J. Hawkes N.E. King OAM G. J. Phillips J. A. Potter P. J. B. Ronald OAM President S. C. Spargo Vice President D. Pollett Hodgson Chief Executive Officer M. O’Sullivan Industry Advisory Group P. Manders ( Chief Judge) B. Taylor B. Rogers C Badenoch L. Ryan P. Aldred Competition Manager Michael Conolly T: +61 3 9281 7473 E: [email protected] University Of Ballarat PO Box 663 Ballarat Victoria 3353 Australia Telephone 1300 225 527 Facsimile +61 3 5327 9855 www.ballarat.edu.au Vice Chancellor Professor David Battersby Contents Report on Entries 4 2012 Judging Panel 4 2012 Trophy Winners 6 2012 Sections and Classes of Entry 9 Exhibitors List 54 2 20 Years Celebrated with AUSTRALIAN INTER NATIO AIBA’s Collaborator NAL B EER AW ARDS In celebration of the AIBA’s 20th Anniversary a commemorative beer was produced, ‘Collaborator.’ AIBA 20 TH 2011 AIBA champion trophy brewers, Brendan Varis ANNIVERS ARY BREW from Feral Brewing and Andrew Ong from 2 Brothers Brewery came together to create this limited edition brew, the brewers have termed an Australian Brown Ale. -

Annual Report 2004 1 Profi Le 2 CEO Statement 4 Key fi Gures and fi Nancial Ratios, 5 Years

Annual Report 2004 1 Profi le 2 CEO statement 4 Key fi gures and fi nancial ratios, 5 years 8 Management review 24 Shareholder information 27 Corporate Governance 28 The Carlsberg Foundation 30 Corporate social responsibility 32 Environment 36 Financial review 42 Adoption of IFRS 46 Risk management 50 Accounting policies 55 Income statement 56 Balance sheet 58 Movements in capital and reserves 60 Cash fl ow statement 61 Notes 78 Group companies 80 Management statement 81 Auditors’ report 82 Board of Directors and Executive Board Carlsberg Pilsner – a 100-year-old brand 2004 marked the 100th anniversary of the fi rst Carlsberg Pilsner being bottled at the Carlsberg brewery in Copenhagen and the distribution of the new brand in the brewery’s own drays. The brewery thus gained control of deliveries of a beer with a light and fresh taste, a clear, bright colour, a fi ne white head and – not least – a stable and high quality. The new beer was given a new oval label. It was green with a white edge and featured the distinctive Carlsberg logo designed by the architect Thorvald Bindesbøll on the occasion of the brewery’s 50th anniversary in 1897. Carlsberg A/S Carlsberg Pilsner was embraced by consumers. Today, its distribution CVR No. 61056416 covers most of the world and Carlsberg is the fastest growing international Ny Carlsberg Vej 100 brand and … Probably the best beer in the world. DK-1760 Copenhagen V, Denmark Phone: +45 3327 3300 Fax: +45 3327 4701 This report is provided in Danish and English. E-mail: [email protected] In case of any discrepancy between the two versions, the Danish wording shall apply. -

National Reports 2016 - 2018

CONGRESSO XVII - CHILE NATIONAL REPORTS 2016 - 2018 EDITED BY JAMES DOUET TICCIH National Reports 2016-2018 National Reports on Industrial Heritage Presented on the Occasion of the XVII International TICCIH Congress Santiago de Chile, Chile Industrial Heritage: Understanding the Past, Making the Future Sustainable 13 and 14 September 2018 Edited by James Douet THE INTERNATIONAL COMMITTEE FOR THE CONSERVATION OF INDUSTRIAL HERITAGE TICCIH Congress 2018 National Reports The International Committee for the Conservation of the Indus- trial Heritage is the world organization for industrial heritage. Its goals are to promote international cooperation in preserving, conserving, investigating, documenting, researching, interpreting, and advancing education of the industrial heritage. Editor: James Douet, TICCIH Bulletin editor: [email protected] TICCIH President: Professor Patrick Martin, Professor of Archae- ology Michigan Technological University, Houghton, MI 49931, USA: [email protected] Secretary: Stephen Hughes: [email protected] Congress Director: Jaime Migone Rettig [email protected] http://ticcih.org/ Design and layout: Daniel Schneider, Distributed free to members and congress participants September 2018 Opinions expressed are the authors’ and do not necessarily re- flect those of TICCIH. Photographs are by the authors unless stated otherwise. The copyright of all pictures and drawings in this book belongs to the authors. No part of this publication may be reproduced for any other purposes without authorization or permission -

Good Practice Examples of Danish Museum Education Aimed at Primary, Lower Secondary and Upper Secondary Schools

Good Practice Examples of Danish museum education aimed at primary, lower secondary and upper secondary schools 2 H e r i ta g e a gency of Denmark 5 Introduction 7 Preface 8 Naturama 10 The Danish Museum of Media 12 The Old Town 14 Thorvaldsens Museum 16 ARKEN Museum of Modern Art 18 The Museum of Copenhagen 20 Ringkøbing-Skjern Museum 22 Museum of Electricity 24 The Museum of South West Zealand / Trelleborg Viking Fortress 26 The Museum of Art Køge Sketch Collection 28 The Danish Museum of Art & Design 31 www.museumsundervisning.dk 33 www. e-museum.dk The teaching activities at Danish museums are cross-disciplinary and problem-orientated and encompass a great variety of learning styles, characterised by a high academic level and social involvement. Introduction This publication shows examples of Danish museums' educational offers for primary through In the course of the to upper secondary schools and of how the museums collaborate with educational institutions. teaching, pupils are By means of 11 examples from museums of cultural history, art and natural history across the activated as they collect country, the Heritage Agency of Denmark wishes to focus attention on the museums’ learning their own information potential. for further work. Naturama, 2008 The museums’ areas of responsibility and research within cultural and natural heritage corre- spond to the primary, lower secondary and upper secondary schools’ core areas. The teaching activities at the museums are cross-disciplinary and problem-orientated and encompass a great variety of learning styles, characterised by a high academic level and social involvement. -

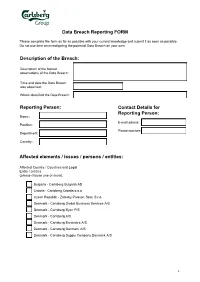

Data Breach Reporting FORM Reporting Person

Data Breach Reporting FORM Please complete the form as far as possible with your current knowledge and submit it as soon as possible. Do not use time on investigating the potential Data Breach on your own. Description of the Breach: Description of the factual observations of the Data Breach: Time and date the Data Breach was observed: Whom identified the Data Breach: Reporting Person: Contact Details for Reporting Person: Name: E-mail adress: Position: Phone number: Department: Country: Affected elements / issues / persons / entities: Affected Country / Countries and Legal Entity / entities (please choose one or more): Bulgaria - Carlsberg Bulgaria AD Croatia - Carlsberg Croatia d.o.o. Czech Republic - Zatecky Pivovar, Spol. S.r.o. Denmark - Carlsberg Global Business Services A/S Denmark - Carlsberg Byen P/S Denmark - Carlsberg A/S Denmark - Carlsberg Breweries A/S Denmark - Carlsberg Danmark A/S Denmark - Carlsberg Supply Company Danmark A/S 1 Denmark - Dansk Retursystem A/S Estonia - Saku Olletehase AS Finland - Oy Sinebrychoff Ab Finland - Sinebrychoff Supply Company Oy France - Kronenbourg SAS France - Kronenbourg Supply Company SAS France - Onyx SAS France - Etablissement Tafanel SA France - Sae de Socodis SA France - CHR Conseil SARL France - Tafanel Gestion SARL France - Tafanel Installations SARL France - SAS Secobra Recherches Germany - Baltika Deutschland GmbH Germany - Carlsberg Deutschland GmbH Germany - Carlsberg Deutschland Logistik GmbH Germany - Carlsberg Supply Company Deutschland GmbH Germany - GEDAT Getränkedaten GmbH Germany - GELOS Getränke Logistik & Gastronomie Service GmbH & Co Germany - Kick in Getränkefachmarkt GmbH Germany - NDC Norddeutsches Dienstleistungs Contor Brauerei Service GmbH Greece - Olympic Brewery SA Greece - Hellenic Beverage Company SA Hungary - Carlsberg Hungary kft. Italy - Carlsberg Italia S.p.A Italy - Carlsberg Horeca Srl Latvia - Aldaris JSC Lithuania - Svyturys-Utenos Alus UAB Lithuania - UAB "Svyturys Brewery" Norway - Ringnes AS Norway - Ringnes Supply Company AS Norway - E. -

Group Companies

128 Carlsberg Group Group companies CARLSBERG A/S Nominal Owner- share ship capital Cur- Exchange share (1,000) rency rate Europe Western BBH Group BBH excl. Europe Eastern Asia activities Other VersaMatrix A/S, Copenhagen, Denmark 100% 1,750 DKK 100.00 Ejendomsaktieselskabet Tuborg Nord B, Copenhagen, Denmark 100% 25,000 DKK 100.00 Ejendomsaktieselskabet Tuborg Nord C, Copenhagen, Denmark 100% 10,000 DKK 100.00 Ejendomsaktieselskabet Tuborg Nord D, Copenhagen, Denmark 100% 10,000 DKK 100.00 Ejendomsinteressentskabet Tuborg Nord B, Copenhagen, Denmark 70% - DKK 100.00 Ejendomsaktieselskabet af 4. Marts 1982, Copenhagen, Denmark 100% 9,500 DKK 100.00 Investeringsselskabet af 17. Januar 1991, Copenhagen, Denmark 100% 14,500 DKK 100.00 Boliginteressentskabet Tuborg Nord, Copenhagen, Denmark 3) 50% - DKK 100.00 Ejendomsinteressentskabet Waterfront, Copenhagen, Denmark 3) 50% - DKK 100.00 Carlsberg Breweries A/S, Copenhagen, Denmark 100% 500,000 DKK 100.00 Carlsberg Danmark A/S, Copenhagen, Denmark 3 subsidiaries 100% 100,000 DKK 100.00 Investeringselskapet RH, Oslo, Norway 100% 49,900 NOK 93.51 Ringnes a.s., Oslo, Norway 6 subsidiaries 100% 238,714 NOK 93.51 Oy Sinebrychoff Ab, Helsinki, Finland 100% 96,707 EUR 745.66 Pripps Ringnes AB, Stockholm, Sweden 1 subsidiary 100% 287,457 SEK 78.92 Carlsberg Sverige AB, Stockholm, Sweden 9 subsidiaries 100% 70,000 SEK 78.92 BBH – Baltic Beverages Holding AB, Stockholm, Sweden 50% 12,000 EUR 745.66 Saku Brewery AS, Estonia 1) 75% 80,000 EEK 47.66 A/S Aldaris, Lithuania 85% 7,500 LVL 1,069.80 Baltic Beverages Invest AB, Stockholm, Sweden 100% 11 EUR 745.66 Baltic Beverages Holding Oy, Helsinki, Finland 100% 4 EUR 745.66 Svyturys-Utenos Alus AB, Lithuania 75% 118,000 LTL 215.96 Slavutich Brewery, Ukraine 92% 853,692 UAH 100.51 Lvivska Brewery, Ukraine 100% 72,741 UAH 100.51 Baltic Beverages Eesti, Estonia 100% 400 EEK 47.66 Baltika Brewery, St.