The Strategic Value of Information In

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Auto Retailing: Why the Franchise System Works Best

AUTO RETAILING: WHY THE FRANCHISE SYSTEM WORKS BEST Q Executive Summary or manufacturers and consumers alike, the automotive and communities—were much more highly motivated and franchise system is the best method for distributing and successful retailers than factory employees or contractors. F selling new cars and trucks. For consumers, new-car That’s still true today, as evidenced by some key findings franchises create intra-brand competition that lowers prices; of this study: generate extra accountability for consumers in warranty and • Today, the average dealership requires an investment of safety recall situations; and provide enormous local eco- $11.3 million, including physical facilities, land, inventory nomic benefits, from well-paying jobs to billions in local taxes. and working capital. For manufacturers, the franchise system is simply the • Nationwide, dealers have invested nearly $200 billion in most efficient and effective way to distribute and sell automo- dealership facilities. biles nationwide. Franchised dealers invest millions of dollars Annual operating costs totaled $81.5 billion in 2013, of private capital in their retail outlets to provide top sales and • an average of $4.6 million per dealership. These service experiences, allowing auto manufacturers to concen- costs include personnel, utilities, advertising and trate their capital in their core areas: designing, building and regulatory compliance. marketing vehicles. Throughout the history of the auto industry, manufactur- • The vast majority—95.6 percent—of the 17,663 ers have experimented with selling directly to consumers. In individual franchised retail automotive outlets are locally fact, in the early years of the industry, manufacturers used and privately owned. -

V8.1 Supported Vehicle List

® CDR Vehicle List CDR Software v8.1 Important Information about Vehicle Coverage The Bosch Crash Data Retrieval Software and Hardware Bosch takes all reasonable actions to ensure the CDR products support the retrieval of crash data from Airbag product supports all vehicles (US and Canada) listed in Control Modules (ACM), Roll-over Sensors (ROS) and this and other CDR product documentation. However, Powertrain Control Modules (PCM) installed in vehicles there may be some vehicles listed that the CDR system listed in this document as indicated by the markings in is unable to retrieve EDR data from. This may be caused the column labeled ‘‘Module’’. by (but not limited to) information that was not available to Bosch at the time the product was developed or, EDR Many vehicles listed in this document include references retrieval may be available only on vehicles with to manufacturer specific notes which may indicate particular options. limitations in CDR product coverage. Make sure that you read the reference notes prior to determining if a vehicle Please contact Bosch Technical Support if you are is supported. experiencing trouble retrieving EDR data from any of the vehicles listed. The issue will be documented and Bosch will attempt to resolve it in a future release. Supported Acura Vehicles Supported Chrysler Vehicles 2012 2005 Make Model Module Make Model Module Acura MDX (note 1) ACM Dodge Durango (note 2 & 4) ACM Acura RL ACM 2006 Acura TL ACM Make Model Module Acura TSX ACM Chrysler 300 (note 3 & 5) ACM Acura ZDX ACM Dodge Charger (note -

Mobile Air Conditioner Leakage Rates Model Year 2016 (Alphabetical List)

Mobile Air Conditioner Leakage Rates Model Year 2016 (Alphabetical List) Leakage Rate AC Charge Size Percentage loss per Make Model (MY 2016) Type of Vehicle (grams/year) (grams) year Ford Fusion 1.6L GDTI Passenger Car 7.8 570 1.4 Ford Fusion 2.5L iVCT Passenger Car 8.7 680 1.3 Ford Escape 1.6L GTDI SUV 8.4 680 1.2 Ford Escape 2.5L SUV 8.0 680 1.2 Ford Police Interceptor Sedan 3.5 GTDI Passenger Car 9.6 740 1.3 Ford Police Interceptor Sedan 3.5L/3.7L TiVCT Passenger Car 9.8 650 1.5 Ford Ford Focus RS 2.3L GDTI RS Passenger Car 7.4 600 1.2 Ford Mustang Shelby GT500 5.2L Passenger Car 7.1 650 1.1 Ford Transit 3.5L GTDI V6 148" wheelbase ext body (dual) Van 8.1 1190 0.7 Ford Transit 3.5L GTDI V6 148" wheelbase (dual) Van 8.0 1190 0.7 Ford Transit 3.5L GTDI V6 130" wheelbase (dual) Van 7.9 1190 0.7 Ford Transit 3.7L TIVCT V6 148" wheelbase ext body (dual) Van 8.1 1110 0.7 Ford Transit 3.7L TIVCT V6 148" wheelbase (dual) Van 8.0 1110 0.7 Ford Transit 3.7L TIVCT V6 130" wheelbase (dual) Van 7.9 1110 0.7 Ford Trainsit 3.7L TIVCT And 3.5L GTDI V6 Van 7.2 790 0.9 Ford Transit 3.2L Diesle I5, 148" wheelbase ext body (dual) Van 8.3 1110 0.7 Ford Transit 3.2L Diesel I5, 148" wheelbase (dual) Van 8.2 1110 0.7 Ford Transit 3.2L Diesel I5, 130" wheelbase (dual) Van 8.1 1110 0.7 Ford Transit 3.2L Diesel I5 Van 7.4 790 0.9 Ford Fiesta 1.0L TiVCT GDTI Passenger Car 7.4 680 1.1 Ford Fiesta 1.6L TiVCT GDTI Passenger Car 7.4 680 1.1 Ford Fiesta 1.6L TiVCT Passenger Car 7.4 600 1.2 Ford Transit Connect 2.5L (Dual) Van 7.8 880 0.9 Ford Transit Connect 2.5L Van 7.3 680 1.1 Ford Transit Connect 1.6L GTDI (Dual) Van 7.9 880 0.9 Ford Transit Connect 1.6L GTDI Van 7.4 680 1.1 Ford Edge 3.5L V6 TiVCT SUV 8.4 680 1.2 Ford MKX 3.7L V6 TiVCT SUV 8.4 680 1.2 Ford Edge 2.0L I4 GTDI SUV 8.7 680 1.3 Ford Police Interceptor Utility 3.5L GTDI SUV 10.3 960 1.1 Ford Police Interceptor utility 3.7L TiVCT SUV 10.4 740 1.4 Minnesota Pollution Control Agency • 520 Lafayette Rd. -

Fmvss No. 214 Amending Side Impact Dynamic Test Adding Oblique Pole Test

U.S. Department Of Transportation FINAL REGULATORY IMPACT ANALYSIS FMVSS NO. 214 AMENDING SIDE IMPACT DYNAMIC TEST ADDING OBLIQUE POLE TEST OFFICE OF REGULATORY ANALYSIS AND EVALUATION NATIONAL CENTER FOR STATISTICS AND ANALYSIS AUGUST 2007 TABLE OF CONTENTS Executive Summary.............................................................................................E-1 I. Introduction .................................................................................................I-1 II. Background ...............................................................................................II-1 III. Injury Criteria ........................................................................................... III-1 IV. Test Data and Analysis of Pole Test Data ................................................IV-1 V. Benefits .....................................................................................................V-1 VI. Technical Costs and Lead Time ...............................................................VI-1 VII. Cost-Effectiveness and Benefit-Cost Analyses .......................................VII-1 VIII. Test Data and Analysis of Moving Deformable Barrier Test ............... VIII-1 IX. Alternatives...............................................................................................IX-1 X. Regulatory Flexibility Act and Unfunded Mandates Reform Act Analysis............................................................................................... X-1 XI. Sensitivity Analyses ……………………………………………….........XI-1 -

AALA2009 Percentages R1.Xls 8/7/2009

Page 1 AALA2009 Percentages_r1.xls 8/7/2009 Passenger car Other Vehicle Type Manufactured in: Manufactured in: Percent Content US/ US/ US/ Manufacturers Makes Carlines Models Canada Canada Outside Canada Outside American Honda Acura RL 0% X American Honda Acura TSX 0% X American Honda Honda Fit 0% X American Honda Honda S2000 0% X American Suzuki Motor Suzuki Grand Vitara 0% X American Suzuki Motor Suzuki SX4 0% X 612 Scaglietti, Scaglietti F1 & 599 GTB Fiat Ferrari Fiorano/F1 0% X F430/F430 F1, F430 Spider, F430 Spider F1, 430 Scuderia & Fiat Ferrari Scuderia Spider 16M 0% X Fuyi Heavy Industries Subaru Forester 0% X Fuyi Heavy Industries Subaru Impreza 0% X Lotus Lotus Elise/Exige0%X Mazda Motor Corp. Mazda CX-7 0% X Mazda3 - 4D Sedan & Mazda Motor Corp. Mazda Hatchback 0% Mazda Motor Corp. Mazda Mazda5 0% X Mazda Motor Corp. Mazda MX-5 Miata 0% X Mazda Motor Corp. Mazda RX-8 0% X Mercedes Benz Mercedes C-Class 0% X Mercedes Benz Mercedes CL & CLS 0% X CLK-Class, Mercedes Benz Mercedes Cabriolet/Coupe 0% X Mercedes Benz Mercedes E-Class 0% X Mercedes Benz Mercedes G-Class 0% X Mercedes Benz Mercedes Maybach 0% X Mercedes Benz Mercedes S & SL Class 0% X Mercedes Benz Mercedes SLK-Class 0% X Mercedes Benz Mercedes SLR 0% X Mitsubishi Motors Mitsubishi Lancer 0% X Mitsubishi Motors Mitsubishi Outlander 0% X Nissan North America Infiniti EX35 0% X Nissan North America Infiniti FX35/50 0% X G37 Sedan, Coupe, Nissan North America Infiniti Convertible 0% X Nissan North America Infiniti M35/45 0% X Nissan North America Nissan 350Z Convertible -

Toyota in the World 2011

"Toyota in the World 2011" is intended to provide an overview of Toyota, including a look at its latest activities relating to R&D (Research & Development), manufacturing, sales and exports from January to December 2010. It is hoped that this handbook will be useful to those seeking to gain a better understanding of Toyota's corporate activities. Research & Development Production, Sales and Exports Domestic and Overseas R&D Sites Overseas Production Companies North America/ Latin America: Market/Toyota Sales and Production Technological Development Europe/Africa: Market/Toyota Sales and Production Asia: Market/Toyota Sales and Production History of Technological Development (from 1990) Oceania & Middle East: Market/Toyota Sales and Production Operations in Japan Vehicle Production, Sales and Exports by Region Overseas Model Lineup by Country & Region Toyota Group & Supplier Organizations Japanese Production and Dealer Sites Chronology Number of Vehicles Produced in Japan by Model Product Lineup U.S.A. JAPAN Toyota Motor Engineering and Manufacturing North Head Office Toyota Technical Center America, Inc. Establishment 1954 Establishment 1977 Activities: Product planning, design, Locations: Michigan, prototype development, vehicle California, evaluation Arizona, Washington D.C. Activities: Product planning, Vehicle Engineering & Evaluation Basic Research Shibetsu Proving Ground Establishment 1984 Activities: Vehicle testing and evaluation at high speed and under cold Calty Design Research, Inc. conditions Establishment 1973 Locations: California, Michigan Activities: Exterior, Interior and Color Design Higashi-Fuji Technical Center Establishment 1966 Activities: New technology research for vehicles and engines Toyota Central Research & Development Laboratories, Inc. Establishment 1960 Activities: Fundamental research for the Toyota Group Europe Asia Pacific Toyota Motor Europe NV/SA Toyota Motor Asia Pacific Engineering and Manfacturing Co., Ltd. -

11 Electric Vehicle Stocks to Buy for 2021

INVESTOR PLACE 11 ELECTRIC VEHICLE STOCKS TO BUY FOR 2021 LUKE LANGO How to turn the electric disruption of transportation into your million-dollar opportunity When it comes to identifying next-generation breakthrough investments that could rise 100%, 200%, 500%, or more, I always come back to one saying. Where there’s disruption, there’s opportunity. Case-in-point: The internet. Throughout the 1990s, the emergence of the internet rapidly disrupted how people across the globe worked, communicated, and played. For many, it was a scary time. Change is never easy. For many more, it was an exciting time, as the internet was unlocking a new world of possibilities. But… for investors… it was an opportunity. Specifically, it was a once-in-a-decade opportunity to invest early in emerging titans of the internet industry. Like Amazon (AMZN)… when it was a $438 million company in 1997… It’s a $1.6 TRILLION company today – representing a whopping 365,000% return. That means a mere $1,000 investment in Amazon in 1997 would be worth more than $3.6 million today. 2 Luke Lango’s Hypergrowth Investing Need I say more? Where there’s disruption, there’s opportunity – and the bigger the disruption, the bigger the opportunity. Right now, we are on the cusp of an enormous disruption. This disruption will fundamentally and entirely change the world’s multi-trillion-dollar transportation work. In its wake, it will create new hundred-billion-dollar titans of the auto industry – most of whom are just tiny companies today. What disruption am I talking about specifically? The shift toward electric vehicles. -

MOST FOG LAMP A31A2 1Or+ HYUNDAI-ALL FORD-MOST

PART # QTY MAKE/MODEL PART USAGE L43A2 1or+ HYUNDAI, KIA - MOST FOG LAMP HYUNDAI-ALL FORD-MOST HOOD SENSOR LINCOLN NAVIGATOR AMBIENT TEMP, THROTTLE A31A2 1or+ KIA-ALL ACTUATOR A31B2 1or+ HYUNDAI/KIA AMBIENT TEMP WHEEL SPEED FRONT Hyundai - Tiburon, Santa Fe, Veracruz, Rondo, Genesis, Equus PIGTAIL, ABS WHEEL L51A2 1or+ KIA-RIO SENSOR A12A2 1or+ HONDA HOOD LATCH A14E3 1or+ NISSAN/INFINITI KEYLESS ENTRY BUZZER WASHER LEVEL, A71A2 1or+ HYUNDAI, KIA, MITSU COMPRESSOR WASHER LEVEL, A71B2 1or+ HYUNDAI, KIA, MITSU COMPRESSOR HORN, MARKER LAMP, ABS SENSOR, AMBIENT TEMP, B11A2 1or+ MOST DOMESTIC SIDE MARKER B12A2 1or+ MOST DOMESTIC SIDE MARKER C41C3 1or+ NISSAN/INFINITI AC PRESSURE SWITCH C25B2 1or+ MAZDA FOG LAMP SIDE MARKER, ABS C42A2 1or+ NISSAN/INFINITI SENSOR, KEYLESS ENTRY D41A2 1or+ NISSAN/INFINITI AMBIENT TEMP AMBIENT TEMP, HORN, E41A2 1or+ COOLANT TEMP F13B2 1or+ NISSAN/INFINITI WASHER PUMP F14A2 1or+ MOST ASIAN COMPRESSOR F42B8 1or+ MOST ASIAN FOG LAMP L11A1 1or+ HONDA HORN L11B2 1or+ HONDA/ACURA/MAZDA MARKER LAMP L12A2 1or+ HONDA HEAD LAMP L12B2 1or+ HONDA HEAD LAMP L15B2 1or+ HONDA, ACURA, MAZDA, SUBARU FOG LAMP, HID TPMS, TURN SIGNAL, SIDE L16C3 1or+ HONDA, ACURA MARKER L31C2 1or+ SUBARU OIL PRESSURE SWITCH L42B2 1or+ NISSAN/INFINITI HEAD LAMP, FOG LAMP L42C2 1or+ NISSAN/INFINITI FOG LAMP L43A2 1or+ HYUNDA/KIA FOG LAMP AMBIENT TEMP, ABS L44A2 1or+ MOST VEHICLES SENSOR, MARKER LAMP L51A2 1or+ HYUNDA/KIA ABS WHEEL SPEED SENSOR L51B2 1or+ HYUNDA/KIA HORN CHRYSLER, DODGE, JEEP, FOG LAMP, DRL, SIDE L64A2 1or+ MERCEDES MARKER R62C8 1or+ -

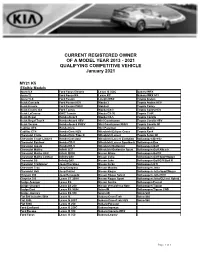

2021 QUALIFYING COMPETITIVE VEHICLE January 2021

CURRENT REGISTERED OWNER OF A MODEL YEAR 2013 - 2021 QUALIFYING COMPETITIVE VEHICLE January 2021 MY21 K5 Eligible Models Acura ILX Ford Focus Electric Lexus IS 350C Subaru WRX Acura TL Ford Focus RS Lexus RC Subaru WRX STI Acura TLX Ford Fusion Lincoln MKZ Toyota Avalon Buick Cascada Ford Fusion HEV Mazda 3 Toyota Avalon HEV Buick Encore Ford Fusion PHEV Mazda 6 Toyota Camry Buick Encore GX Ford Taurus Mazda CX-3 Toyota Camry HEV Buick LaCrosse GMC Terrain Mazda CX-30 Toyota C-HR Buick Regal Honda Accord Mazda CX-5 Toyota Corolla Buick Regal TourX Honda Accord HEV Mini Countryman Toyota Corolla HEV Buick Verano Honda Accord PHEV Mini Countryman PHEV Toyota Corolla iM Cadillac ATS Honda Civic Mini Paceman Toyota Matrix Cadillac CT4 Honda Civic HEV Mitsubishi Eclipse Cross Toyota Rav4 Chevrolet Cruze Honda Civic Type R Mitsubishi Lancer Toyota Scion iM Chevrolet Cruze Limited Honda Crosstour Mitsubishi Lancer Evolution Volkswagen Beetle Chevrolet Equinox Honda CR-V Mitsubishi Lancer Sportback Volkswagen Eos Chevrolet Impala Honda HR-V Mitsubishi Outlander Volkswagen Golf Chevrolet Malibu Infiniti G37 Mitsubishi Outlander Sport Volkswagen Golf Alltrack Chevrolet Malibu HEV Infiniti QX30 Nissan Altima Volkswagen Golf R Chevrolet Malibu Limited Infinity Q50 Nissan Cube Volkswagen Golf SportWagen Chevrolet SS Infinity Q60 Nissan Juke Volkswagen Golf/GTI/Golf R Chevrolet Trailblazer Jeep Cherokee Nissan Kicks Volkswagen GTI Chevrolet Trax Jeep Compass Nissan Maxima Volkswagen Jetta Chevrolet Volt Jeep Patriot Nissan Rogue Volkswagen Jetta SportWagen -

Ontario Fact Sheet

Note: all fact sheets are two sided 11”x8.5” folded – except quebec which is two sided 5.5”x8.5” no fold Ontario Fact Sheet ONTARIO Ontario BC Yukon Prairies Atlantic Qubec Sales, Marketing Sales, Marketing Sales, Marketing Sales, Marketing Sales, Marketing and Distribution and Distribution and Distribution and Distribution and Distribution Toyota Manufacturing Toyota Wheel Toyota Dealership Toyota Dealership Toyota Manufacturing Manufacturing Lexus Manufacturing Lexus Dealership Lexus Dealership Toyota Parts Manufacturing Toyota Dealership Toyota Parts Manufacturing Scion Dealership Scion Dealership Toyota Dealership Lexus Dealership Hino Assembly Plant Hino Dealership Hino Dealership Lexus Dealership Ontario BC Yukon Scion DealershipPrairies Atlantic Qubec Cold Weather Testing Financial Services Scion Dealership Hino Dealership Sales, Marketing Toyota Dealership Sales, Marketing Sales, Marketing Sales, Marketing Sales, Marketing Hino Dealership and Distribution and Distribution Financial Servicesand Distribution and Distribution and Distribution Lexus Dealership Financial Services Toyota Manufacturing Toyota Wheel Toyota Dealership Toyota Dealership Toyota Manufacturing Scion Dealership Manufacturing Lexus Manufacturing $ Lexus Dealership Lexus Dealership Toyota Parts Manufacturing Hino Dealership Toyota Dealership Toyota Parts Manufacturing Scion Dealership Scion Dealership Toyota Dealership Financial Services Lexus Dealership Hino Assembly Plant Hino Dealership Hino Dealership Lexus Dealership Hino Head Office Scion Dealership Cold -

Vehicle Brands and Manufacturers • 12/2014

Vehicle Brands and Manufacturers • 12/2014 Vehicle Brand Manufactured by Website Customer Service Acura Honda www.acura.com 800-382-2238 Canada www.acura.ca 888-922-8729 Alfa Romeo Dodge www.4c.alfaromeo.com 800-253-2872 Canada www.4c.alfaromeo.com/en_ca E: 800-465-2001 F: 800-387-9983 Audi Volkswagen www.audiusa.com 800-822-2834 Canada www.audi.ca 800-822-2834 BMW BMW www.bmwusa.com 800-831-1117 Canada www.bmw.ca 800-567-2691 Buick General Motors www.buick.com 800-521-7300 Cadillac General Motors www.cadillac.com 800-458-8006 Canada www.cadillac.com 800-263-3777 Chevrolet/GEO General Motors www.chevrolet.com 800-222-1020 Canada www.chevrolet.com 800-263-3777 Chrysler Chrysler www.chrysler.com 800-247-9753 Canada www.chrysler.ca E: 800-465-2001 F: 800-387-9983 Daewoo Daewoo www.daewoous.com 877-362-1234 Dodge Chrysler www.dodge.com 800-423-6343 Canada www.chrysler.ca E: 800-465-2001 F: 800-387-9983 Eagle Chrysler www.chrysler.com 800-247-9753 Canada www.chrysler.ca E: 800-465-2001 F: 800-387-9983 Ferrari Ferrari www.ferrariusa.com 201-816-2600 or www.ferrariworld.com Fiat Chrysler www.fiatusa.com/en 888-242-6342 Canada www.fiatcanada.com E: 800-465-2001 F: 800-387-9983 Ford Ford www.ford.com 800-392-3673 Canada www.ford.ca 800-565-3673 Geo General Motors (see Chevrolet) GMC General Motors www.gmc.com 800-462-8782 Canada www.gmc.com 800-263-3777 Honda Honda www.honda.com 800-999-1009 Canada www.honda.ca 888-946-6329 Hummer General Motors www.hummer.com 800-732-5493 Canada www.hummer.com 800-263-3777 Hyundai Hyundai www.hyundaiusa.com 800-633-5151 -

Lincoln Link V5N1

The LINCOLN LINK LINKINGThe TOGETHER LINCOLN ALL ELEMENTS OF THE LINCOLN MOTORLINK CAR HERITAGE IN THIS ISSUE 3 Foundation Acquires Capizzi Literature Collection 4 The Role of Museums in Promoting Lincoln’s Heritage 7 The LMCF Archives at the AACA Library 8 Historic Wixom Plant Closes 10 Lincoln Wins Younger Customers 11 Ford Vehicle Quality Soars in 2007 12 Letters to the Editor 14 Know Your Foundation Trustees published semi-yearly Volume V, number 1 • spring, 2007 a single building to a plus wrapping and FROM THE EDITOR whole factory. Seven postage. Either version Roncelli employees makes a wonderful gift. ■ RONCELLI INC. is a can-do supported the May Contact the editor. construction management and ser- 22, 2004, unveiling vices company of Sterling Heights, ceremony. ■ ON A DIFFER- Michigan, who donated vital ser- ENT SUBJECT, your vices in the saving of the Lincoln ■ FORD MOTOR Lincoln Link editor name stones from the old Lincoln COMPANY produced a of five years must plant. (See The Lincoln Link, beautifully illustrated step down in order Volume 2, Number 2.) They have and written 272-page to pay attention to produced a quality DVD presenta- book to celebrate the 100th personal matters. Working with tion of that timely preservation birthday of the company, which the quality men who volunteer as effort, and have graciously offered occurred in 2003. These books Foundation Trustees has been a to make copies of the DVD avail- are much sought after, both as a personally rewarding experience. able to those who are interested. memento of the event and for the I do plan to remain a Trustee and Contact this editor at 703 754 timeless information and graphics support the Link and Foundation 9648 if you want a copy.