Ar 20 Eng.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Reinvestment Review Book

The Department of Finance Reinvestment Review Committee Eligible Depository Designation 2012 - 2013 Division of Treasury Bank Evaluations & Recommendations Table of Contents • Executive Summary Page 3 • Bank Evaluations Page 5 • Final Scores, Rankings, and Recommendations Page 8 2 Executive Summary In accordance with Chapter 178 of the Codified Ordinances of the City of Cleveland, a Request for Proposal (RFP) was issued for banking services. Through this RFP, the City will: 1) designate depositories who are eligible to receive all or a portion of the City’s active deposits for the 2012-2013 calendar years; and 2) identify those who can offer comprehensive banking services at the most competitive rates. These services include, but are not limited to: Deposit Processing / Vault Services Wire Transfers Information Reporting Lockbox Services Investment Support Services (Safekeeping) Automated Clearing House (ACH) Services The Finance Department’s Treasury Division received RFP responses from the following nine banks: Charter One Bank Fifth Third Bank First Merit Bank Huntington Bank KeyBank Ohio Savings Bank PNC Bank US Bank Wells Fargo Bank 3 Executive Summary (continued) The Director of Finance may designate one or more banks after an evaluation of their policies and practices regarding: Loans to low and moderate income City residents Loans to businesses Loans to minority business enterprises Neighborhood development Housing Economic development The interest rates paid on deposits, fees and service charges, convenience -

PARETURN Société D'investissement À Capital Variable RCS Luxembourg N° B 47 104 Annual Report Including Audited Financial Statements As at September 30, 2018 PARETURN

PARETURN Société d'Investissement à Capital Variable RCS Luxembourg N° B 47 104 Annual Report including Audited Financial Statements as at September 30, 2018 PARETURN Pareturn Best Selection Pareturn Best Selection Side - Pocket Pareturn Croissance 2000 Pareturn Cartesio Equity Pareturn Cartesio Income Pareturn Stamina Systematic* Pareturn Stamina Systematic Plus* Pareturn Mutuafondo Global Fixed Income Pareturn Barwon Listed Private Equity Pareturn Global Balanced Unconstrained Pareturn Cervino World Investments Pareturn Entheca Patrimoine Pareturn Ataun Pareturn Invalux Fund Pareturn Gladwyne Absolute Credit Pareturn Mutuafondo España Lux Pareturn EtendAR* Pareturn GVC Gaesco Patrimonial Fund Pareturn GVC Gaesco Euro Small Caps Equity Fund Pareturn GVC Gaesco Absolute Return Fund Pareturn GVC Gaesco Columbus European Mid-Cap Equity Fund* Pareturn Mapfre Euro Bonds Fund* Pareturn Diversified Fund Pareturn Security Latam Corporate Debt Pareturn Rivendale Pareturn Fidelius Global Pareturn Santalucia Espabolsa (Luxembourg)* Pareturn Santalucia Fonvalor* PARETURN Pareturn Imantia USD Global High Yield Bond No subscription can be received on the basis of these financial statements. Subscriptions are only valid if made on the basis of the current prospectus and relevant Key Investor Information Document ("KIID") which will be accompanied by a copy of the latest annual report including audited financial statements and a copy of the latest available unaudited semi-annual report, if published after such annual report. * Please see note 1 for -

Regulation CC

Consumer Affairs Laws and Regulations Regulation CC Introduction The Expedited Funds Availability Act (EFA) was enacted in August 1987 and became effective in Septem- ber 1988. The Check Clearing for the 21st Century Act (Check 21) was enacted October 28, 2003 with an effective date of October 28, 2004. Regulation CC (12 C.F.R. Part 229) issued by the Board of Governors of the Federal Reserve System implements the EFA act in Subparts A through C and Check 21 in Subpart D. Regulation CC sets forth the requirements that depository institutions make funds deposited into transaction accounts available according to specified time schedules and that they disclose their funds availability poli- cies to their customers. The regulation also establishes rules designed to speed the collection and return of unpaid checks. The Check 21 section of the regulation describes requirements that affect banks that create or receive substitute checks, including consumer disclosures and expedited recredit procedures. Regulation CC contains four subparts: • Subpart A – Defines terms and provides for administrative enforcement. • Subpart B – Specifies availability schedules or time frames within which banks must make funds avail- able for withdrawal. It also includes rules regarding exceptions to the schedules, disclosure of funds availability policies, and payment of interest. • Subpart C – Sets forth rules concerning the expeditious return of checks, the responsibilities of paying and returning banks, authorization of direct returns, notification of nonpayment of large-dollar returns by the paying bank, check-indorsement standards, and other related changes to the check collection system. • Subpart D – Contains provisions concerning requirements a substitute check must meet to be the legal equivalent of an original check; bank duties, warranties, and indemnities associated with substitute checks; expedited recredit procedures for consumers and banks; and consumer disclosures regarding sub- stitute checks. -

Summary of Laws and Procedures Pertaining to Depository Contracts

Summary of Laws and Procedures Pertaining to Depository Contracts for Independent School Districts Note: Legislative acts passed during a current legislative session may alter the requirements summarized in this document. Related Statutes and Rules The state laws pertaining to school district depositories are found in the Texas Education Code (TEC), Chapter 45, Subchapter G (§§45.201–45.209). The TEC, §45.202, provides that the school depository or depositories of every independent school district may be selected only as provided by that subchapter. In accordance with the TEC, §45.206, in selecting a depository, your school district must use a uniform bid or proposal blank in the form prescribed by the State Board of Education (SBOE) rule, which is 19 Texas Administrative Code (TAC) §109.51. The Texas Education Code (TEC), §45.208(e), was amended by Senate Bill 1376. As a result, as of June 4, 2019, a school district is not required to submit its Depository Contract for Funds of Independent School Districts and its Texas Surety Bond form, if applicable, to TEA. All remaining depository contract rules are still in effect. If a school district makes changes to its direct deposit account, the district still must electronically submit a Direct Deposit Authorization form to TEA. Two-Year Term of the Contract Your school district must renew its depository contract(s) every two years. The two-year contract term begins and ends in odd-numbered years and is from either July 1 of one year through June 30 two years later or September 1 of one year through August 31 two years later (for example, the period from either July 1, 2021, through June 30, 2023, or September 1, 2021, through August 31, 2023). -

Deposit Account Agreement and Disclosure

DEPOSIT ACCOUNT AGREEMENT AND DISCLOSURE August 1, 2021 DEPOSIT ACCOUNT AGREEMENT AND DISCLOSURE Table of Contents GENERAL PROVISIONS – Part I.................................................................................................................................................... 5 1. Legal Effect of Provisions in this Disclosure. .................................................................................................................... 5 2. Effect of State and Federal Laws and Regulations ............................................................................................................ 5 3. Plain Language.............................................................................................................................................................. 5 4. Identification Notice (USA Patriot Act) ............................................................................................................................ 5 5. Taxpayer Identification Number (TIN) and Backup Withholding ........................................................................................ 5 6. Address ........................................................................................................................................................................ 5 TYPES OF ACCOUNTS – Part II .................................................................................................................................................... 5 7. Checking Accounts ....................................................................................................................................................... -

Bank Depository Services RFP (Opened 10-24-18)

CITY OF BEEVILLE REQUEST FOR PROPOSALS BANK DEPOSITORY SERVICES Introduction The City of Beeville requests proposals pursuant to Chapter 105, Tex. Loc. Govt. Code from qualified banking institutions to be the City’s Depository Bank for the period beginning February 1st, 2019 and ending Februar 1st, 2024 or until the successor Depository shall have been duly selected and qualified per state laws. A proposer must be a Federal or State of Texas chartered bank located within the City limits. If the headquarters of the proposer is not located within the City limits, a branch bank of the proposer located within the City must be able to offer the full range of services required by this RFP. Bidding Procedures The Proposal for Bank Depository Services included in the RFP is intended to serve as the proposal form for the Depository agreement. If a service requirement cannot be supplied, the term “NO Proposal” should be entered, or another alternative service offered. The proposing bank shall submit a copy of its last annual financial statement, and its last FDIC call report with the proposal. The proposal must be submitted in a sealed envelope bearing the title, “City of Beeville Request for Proposal-Bank Depository Services,” with the name of the proposer. The proposal should contain one copy of the proposal form, and should be directed to the Office of the City Secretary, Beeville City Hall, 400 N. Washington Street, Beeville, Texas 78102, no later than 3:00 p.m. on November 20th, 2018. Selection of Depository Kristine Horton, Finance Director, is the City’s contact person for all aspects of this RFP. -

Depository Services

CCE-DEP Comptroller of the Currency Administrator of National Banks Depository Services Comptroller’s Handbook August 2010 CCE Consumer Compliance Examination Depository Services Table of Contents Introduction ............................................................................................... 1 Reserve Requirements of Depository Institutions ........................................ 2 Background and Summary ................................................................ 2 Affected Institutions .......................................................................... 2 Computation of Reserves .................................................................. 3 Exemption From Reserve Requirements ............................................ 3 Regulation D Deposit Requirements ................................................. 5 Federal Reserve Board Staff Opinions and Rulings: Regulation D ...... 6 Savings Deposits .............................................................................. 9 Time Deposits ................................................................................ 24 Transaction Accounts ..................................................................... 29 References ..................................................................................... 40 Interest on Deposits ................................................................................. 42 Background and Summary .............................................................. 42 Federal Reserve Board Staff Opinions Interpreting Regulation -

ANNUAL REPORT 2002 SOCIÉTÉ GÉNÉRALE GROUP 1 Message from Daniel Bouton Chairman and Chief Executive Officer

Review 2002 Société Générale Group 2002 Review Société Générale Group Réf. 170148 Réf. RETAIL BANKING ■ ASSET MANAGEMENT & PRIVATE BANKING ■ CORPORATE & INVESTMENT BANKING RETAIL BANKING ■ ASSET MANAGEMENT & PRIVATE BANKING ■ CORPORATE & INVESTMENT BANKING Profile No.1 non-mutual The Société Générale Group retail banking group in France (1) is the ninth largest French company by market capitalization and the sixth largest bank in the euro zone. It employs 3rd largest corporate and over 80,000 people worldwide. investment bank in the euro zone (2) Its business mix is structured around three core businesses: Retail Banking, Asset Management and Private Banking, rd largest euro-zone bank and Corporate and Investment Banking. 3 (3) The Group is pursuing a profitable growth policy based in asset management on the selective development of its core activities th through a combination of organic growth and acquisitions, 9 largest market capitalization and is drawing on a strong capacity for innovation in France (EUR 23.9 billion geared towards satisfying its customers. at December 31, 2002) (4) The Group’s three fundamental values are Professionalism, Innovation and Team Spirit. AA- (Standards & Poor’s) Aa3 (Moody’s) AA (Fitch) (1) By net banking income and number of branches (source: Société Générale). (2) By net banking income (source: Société Générale). (3) By assets under management (source: Société Générale). (4) Source: Bloomberg. ANNUAL REPORT 2002 SOCIÉTÉ GÉNÉRALE GROUP 1 Message from Daniel Bouton Chairman and Chief Executive Officer The Société Générale Group turned in a satisfactory performance in 2002, despite the harsh environment Against a backdrop of highly volatile, debt and equity derivatives. -

European Esg-Sri Virtual Conference

SAVE THE DATE PARTICIPATING COMPANIES SOCIETE GENERALE CORPORATE & INVESTMENT BANKING IS DELIGHTED TO INVITE YOU TO THE ADEVINTA GECINA SAINT GOBAIN AGEAS GLAXOSMITHKLINE SHELL AIR FRANCE KLM GROUPE BRUXELLES SALZGITTER EUROPEAN AIR LIQUIDE LAMBERT SANOFI AKZO NOBEL GROUPE PSA SAP ALBIOMA GROUPE SEB SARTORIUS STEDIM BIOTECH ESG-SRI ALLIANZ HEIDELBERGCEMENT SCOR ALD AUTOMOTIVE HOCHTIEF SCHNEIDER ELECTRIC ALSTOM HSBC SIEMENS AMUNDI INTESA SANPAOLO SIGNIFY VIRTUAL KINGFISHER ARCELORMITTAL SIKA ASML KLEPIERRE SODEXO ASSA ABLOY ENI SOCIETE GENERALE CONFERENCE ASTRAZENECA LEGRAND SOITEC ATLAS COPCO LEONARDO SPA SOLVAY SA ATOS LINDE SPIE BASF LLOYDS BANKING STMICROELECTRONICS Sustainable & Positive Impact BAYER AG METRO SUEZ BBVA MERSEN SWEDISH MATCH Finance BOOHOO NATIXIS SWISS RE BP NATURGY TARKETT BUREAU VERITAS NEXANS THALES CAPGEMINI NEXITY TELEPERFORMANCE 17, 18 & 19 NOVEMBER 2020 - “Generating impact in a world in transition” CARLSBERG NESTLE TIKEHAU CAPITAL • Dialogues on ESG and SRI involving over 110 companies and institutional investors, in one CASINO NORMA GROUP TOTAL to one / one to few / fireside chat. COVESTRO NOVARTIS UNIPER CREDIT AGRICOLE NOVO NORDISK VALEO • 7 panels and keynote webinars dedicated to Sustainable & Positive Impact Finance CREDIT SUISSE OMV VEOLIA open to all participants: CRODA ORANGE VESTAS PERNOD RICARD The green economic relaunch post pandemic crisis, placing fight against climate change and loss of DAIMLER VICAT biodiversity at the heart of economic policies DEUTSCHE POST PHILIPS VINCI EDF PLASTIC OMNIUM -

La Place Du Risque De Réputation Et Du Risque De Mauvaise Gouvernance

La place du risque de réputation et du risque de mauvaise gouvernance dans les comptes annuels et plus généralement dans les “ Documents de référence ”, ou les “ Documents d’enregistrement universel ” élaborés par les sociétés du SBF 120 soumises aux normes comptables françaises pour l’exercice comptable 2018 et 2019 Jean-Louis Navarro To cite this version: Jean-Louis Navarro. La place du risque de réputation et du risque de mauvaise gouvernance dans les comptes annuels et plus généralement dans les “ Documents de référence ”, ou les “ Documents d’enregistrement universel ” élaborés par les sociétés du SBF 120 soumises aux normes comptables françaises pour l’exercice comptable 2018 et 2019. [Rapport de recherche] Université Lumière (Lyon 2). 2020. hal-02963783 HAL Id: hal-02963783 https://hal.univ-lyon2.fr/hal-02963783 Submitted on 11 Oct 2020 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. 1 La place du risque de réputation et du risque de mauvaise gouvernance dans les comptes annuels et plus généralement dans les « Documents de référence », ou les « Documents d’enregistrement universel » élaborés par les sociétés du SBF 120 soumises aux normes comptables françaises pour l’exercice comptable 2018 et 2019 Etude empirique réalisée par M. -

FINAL DISTRIBUTION.Xlsx

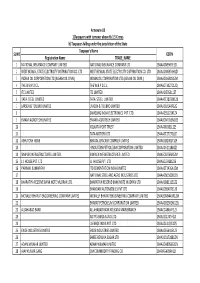

Annexure-1B 1)Taxpayers with turnover above Rs 1.5 Crores b) Taxpayers falling under the jurisdiction of the State Taxpayer's Name SL NO GSTIN Registration Name TRADE_NAME 1 NATIONAL INSURANCE COMPANY LIMITED NATIONAL INSURANCE COMPANY LTD 19AAACN9967E1Z0 2 WEST BENGAL STATE ELECTRICITY DISTRIBUTION CO. LTD WEST BENGAL STATE ELECTRICITY DISTRIBUTION CO. LTD 19AAACW6953H1ZX 3 INDIAN OIL CORPORATION LTD.(ASSAM OIL DIVN.) INDIAN OIL CORPORATION LTD.(ASSAM OIL DIVN.) 19AAACI1681G1ZM 4 THE W.B.P.D.C.L. THE W.B.P.D.C.L. 19AABCT3027C1ZQ 5 ITC LIMITED ITC LIMITED 19AAACI5950L1Z7 6 TATA STEEL LIMITED TATA STEEL LIMITED 19AAACT2803M1Z8 7 LARSEN & TOUBRO LIMITED LARSEN & TOUBRO LIMITED 19AAACL0140P1ZG 8 SAMSUNG INDIA ELECTRONICS PVT. LTD. 19AAACS5123K1ZA 9 EMAMI AGROTECH LIMITED EMAMI AGROTECH LIMITED 19AABCN7953M1ZS 10 KOLKATA PORT TRUST 19AAAJK0361L1Z3 11 TATA MOTORS LTD 19AAACT2727Q1ZT 12 ASHUTOSH BOSE BENGAL CRACKER COMPLEX LIMITED 19AAGCB2001F1Z9 13 HINDUSTAN PETROLEUM CORPORATION LIMITED. 19AAACH1118B1Z9 14 SIMPLEX INFRASTRUCTURES LIMITED. SIMPLEX INFRASTRUCTURES LIMITED. 19AAECS0765R1ZM 15 J.J. HOUSE PVT. LTD J.J. HOUSE PVT. LTD 19AABCJ5928J2Z6 16 PARIMAL KUMAR RAY ITD CEMENTATION INDIA LIMITED 19AAACT1426A1ZW 17 NATIONAL STEEL AND AGRO INDUSTRIES LTD 19AAACN1500B1Z9 18 BHARATIYA RESERVE BANK NOTE MUDRAN LTD. BHARATIYA RESERVE BANK NOTE MUDRAN LTD. 19AAACB8111E1Z2 19 BHANDARI AUTOMOBILES PVT LTD 19AABCB5407E1Z0 20 MCNALLY BHARAT ENGGINEERING COMPANY LIMITED MCNALLY BHARAT ENGGINEERING COMPANY LIMITED 19AABCM9443R1ZM 21 BHARAT PETROLEUM CORPORATION LIMITED 19AAACB2902M1ZQ 22 ALLAHABAD BANK ALLAHABAD BANK KOLKATA MAIN BRANCH 19AACCA8464F1ZJ 23 ADITYA BIRLA NUVO LTD. 19AAACI1747H1ZL 24 LAFARGE INDIA PVT. LTD. 19AAACL4159L1Z5 25 EXIDE INDUSTRIES LIMITED EXIDE INDUSTRIES LIMITED 19AAACE6641E1ZS 26 SHREE RENUKA SUGAR LTD. 19AADCS1728B1ZN 27 ADANI WILMAR LIMITED ADANI WILMAR LIMITED 19AABCA8056G1ZM 28 AJAY KUMAR GARG OM COMMODITY TRADING CO. -

Palmarès De La Féminisation Des Instances Dirigeantes Des

Note totale Note totale Note totale Présidente du Conseil Présence d'un réseau de Note totale Note globale Part des Femmes dans le Part des femmes dans le Part des femmes dans le Femme Présidente de Part de femmes dans le Part des femmes dans le Féminisation Note obtenue à Note obtenue au Sensibilisation / Rang Société Féminisation Féminisation et/ou DG / Présidente du femmes / réseau de Politiques de obtenue Conseil Comité de Nomination Comité de Rémunération Comité Comex Top 100 de la l'Index dernier indicateur Formation des dirigeants du Conseil des dirigeants Directoire mixité féminisation Présidence 100 20 5 5 5 35 30 10 40 5 5 5 5 5 5 20 1 90,10 GECINA 50,00% 20,00 66,67% 5,00 66,67% 5,00 Oui 5,00 35,00 40,00% 24,00 43,00% 8,60 32,60 Oui 5,00 5,00 92 5,00 5 2,50 100,00% 5,00 Oui 5,00 17,50 2 85,60 SODEXO 60,00% 20,00 100,00% 5,00 75,00% 5,00 Oui 5,00 35,00 30,00% 18,00 38,00% 7,60 25,60 Oui 5,00 5,00 99 5,00 10 5,00 100,00% 5,00 Oui 5,00 20,00 3 80,50 L'OREAL 53,85% 20,00 25,00% 2,50 66,67% 5,00 Oui 5,00 32,50 30,00% 18,00 51,00% 10,00 28,00 Non 0,00 0,00 95 5,00 10 5,00 100,00% 5,00 Oui 5,00 20,00 4 80,36 MERCIALYS 54,55% 20,00 60,00% 5,00 60,00% 5,00 Oui 5,00 35,00 50,00% 30,00 61,00% 10,00 40,00 Non 0,00 0,00 NA 0,00 NA 0,00 7,14% 0,36 Oui 5,00 5,36 5 80,20 MAISONS DU MONDE 57,14% 20,00 33,33% 3,33 33,33% 3,33 Oui 5,00 31,67 40,00% 24,00 47,69% 9,54 33,54 Oui 5,00 5,00 83 5,00 10 5,00 0,00% 0,00 Non 0,00 10,00 6 80,11 ENGIE 45,45% 18,18 40,00% 4,00 40,00% 4,00 Oui 5,00 31,18 35,71% 21,43 25,00% 5,00 26,43 Oui 5,00 5,00 87 5,00