Pakistan Strategy KSE-100 Posted Highest Return in 7 Years Structural Reforms to Set the Market Tone for FY22

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Topline Market Review P

Pakistan Weekly January 12, 2018 REP‐057 Topline Market Review Gains erode as profit taking ensues KSE‐100 Index +1.0 % WoW; Weekly net FIPI US$26mn Topline Research Best Local Brokerage House [email protected] Brokers Poll 2011-14, 2016-17 Tel: +9221‐35303330, Ext: 133 Topline Securities, Pakistan www.jamapunji.pk Best Local Brokerage House 2015-16 Index gains 1% in outgoing week as profit taking ensues Market Weekly Data KSE Volume & Value KSE‐100 Index 42,933.72 (Shares mn) Volume Value (US$mn) 330 150 1‐Week Change (%) 1.0% 260 Market Cap (Rs tn) 8.9 106 190 1‐Week Change (%) 0.2% 63 Market Cap (US$ bn) 80.6 120 1‐Week Change (%) 0.2% 50 20 18 18 18 18 18 ‐ ‐ 1‐Week Avg. Daily Vol (shares mn) 276.4 ‐ ‐ ‐ n n n n n aa aa aa aa aa J J J J J ‐ ‐ 1‐Week Avg. Daily Value (Rs bn) 12.2 ‐ ‐ ‐ 9 8 1‐Week Avg. Daily Value (US$ mn) 110.2 10 11 12 Source: PSX Source: PSX Outgoing week saw the culmination of the Santa Clause rally which commenced on December 20, 2017 and peaked on Jan 10, 2018 with a net gain of 14%. Since then index has had red two sessions correcting 2%/697pts, which has trimmed weekly gains to 1%/410pts with the index closing the week at 42,934pts level. Going forward, equities maybe further pressured as agitation movement by opposition parties begin on Jan 17 to protest against the Model Town. PtiitiParticipation idimproved siifitlignificantlyasprofitswerebkdbooked, average volumes idincreased 30% WWWoW whilevalue rose 44%. -

CONTENTS FUND INFORMATION Management Company Faysal Asset Management Limited Fund Information 2 Board of Directors of the Management Company Mr

Quarter and Nine months ended March 31, 2007 Quarter and Nine months ended March 31, 2007 CONTENTS FUND INFORMATION Management Company Faysal Asset Management Limited Fund Information 2 Board of Directors of the Management Company Mr. Farook Bengali, Chairman Mr. Salman Haider Sheikh, Chief Executive Officer Mission Statement 3 Mr. Hassan Mohamed Mahmood, Director Mr. Mohammad Iqbal, Director Mr. Shahid Waqar Mahmood, Director Mr. Feroz Rizvi, Director Report of the Directors of the Management Company 4 Mr. Iqbal Alimohamed, Director Mr. Aqeel Karim Dhedhi, Director CFO of the Management Company Statement of Assets and Liabilities 6 Mr. Muhammad Shakeel Musani Company Secretary of the Management Company Mr. M. Siddique Memon Income Statement 7 Audit Committee Mr. Iqbal Alimohamed, Chairman Mr. Mohammad Iqbal, Member Distribution Statement 8 Mr. Shahid Waqar Mahmood, Member Mr. Feroz Rizvi, Member Trustee Statement of Movement in Unit Holders’ Funds 9 Central Depository Company of Pakistan Limited 8th Floor, Karachi Stock Exchange Building, Stock Exchange Road, Karachi-74000 Cash Flow Statement 10 Bankers to the Fund Faysal Bank Limited MCB Bank Limited Bank Alfalah Limited Notes to the Financial Statements 11 Habib Metropolitan Bank Limited Atlas Bank Limited Bank of Punjab Limited Auditor A.F. Ferguson & Co., Chartered Accountants Legal Advisor Mohsin Tayebaly & Co. Barristers & Advocates, Corporate legal Consultants, 2nd Floor, Dime Centre, BC-4, Block-9, KDA-5, Clifton, Karachi. Registrar Gangjees Registrar Services (Pvt) Limited Room -

Distribution, Power and Networks in Financial Markets of Pakistan

SMALL CLUB A Small Club: Distribution, Power and Networks in Financial Markets of Pakistan No. 2021:3 PIDE Working Papers Nadeem Ul Haque Amin Hussain PIDE Working Papers No. 2021:3 A Small Club: Distribution, Power and Networks in Financial Markets of Pakistan Nadeem Ul Haque Vice-Chancellor, Pakistan Institute of Development Economics, Islamabad. and Amin Husain Doktorand, Uppsala University. PAKISTAN INSTITUTE OF DEVELOPMENT ECONOMICS ISLAMABAD 2021 Editorial Committee Idrees Khawaja Saman Nazir Shahid Mehmood Disclaimer: Copyrights to this PIDE Working Paper remain with the author(s). The author(s) may publish the paper, in part or whole, in any journal of their choice. Pakistan Institute of Development Economics Islamabad, Pakistan E-mail: [email protected] Website: http://www.pide.org.pk Fax: +92-51-9248065 Designed, composed, and finished at the Publications Division, PIDE. CONTENTS Page Abstract v 1. The Stock Market That Does Not Grow! 1 2. Corporate Governance Matters 2 3. Networks and Subnetworks 6 3.1. Shareholders Networks 6 3.2. Network of Families: Mahbubul Haq Redux 7 4. Corporate Governance: What Board Memberships Tell Us! 8 4.1. Independent Directors 10 4.2. The Opportunity to be a Director: A Small Club 11 5. Network Analysis of Board Members 12 5.1. A Small Club 12 6. Who Matters in Pakistani Corporations? 13 7. Conclusion 16 References 17 List of Tables Table 1. Shareholding Proportions in KSE 100 (Market Cap) 5 Table 2. Professional Experience of Directors 11 Table 3. Number of Directors in Each Category 11 Table 4. Characteristics of 20 Directors with Highest Betweenness Centrality 15 List of Figures Figure 1. -

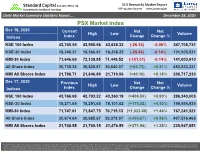

PSX Market Index

Standard Capital Securities (Pvt.) Ltd. SCS Research | Market Report Committed to intelligent investing REP-033 also log onto www.jamapunji.pk Daily Market Summary Statistics Report…. December 18, 2020 REP-033 also log onto PSX Market Indexwww.jamapunji.pk Dec 18, 2020 Current Net Net High Low Volume Indices Index Change Change % KSE 100 Index 43,740.55 43,955.56 43,638.33 (-26.14) -0.06% 247,708,731 KSE-30 Index 18,246.21 18,366.81 18,208.25 (-25.43) -0.14% 131,905,521 KMI-30 Index 71,646.60 72,139.95 71,449.52 (-101.01) -0.14% 141,003,610 All Share Index 30,738.36 30,825.87 30,640.07 (+63.72) +0.21% 482,533,331 KMI All Shares Index 21,788.71 21,846.89 21,719.06 (+40.16) +0.18% 208,717,230 Dec 17, 2020 Previous Net Net High Low Volume Indices Index Change Change % KSE 100 Index 43,766.69 43,793.22 43,360.19 (+406.50) +0.93% 286,340,005 KSE-30 Index 18,271.64 18,291.65 18,101.62 (+170.02) +0.93% 149,554,934 KMI-30 Index 71,747.61 71,847.75 70,715.13 (+1,032.48) +1.44% 167,241,521 All Share Index 30,674.64 30,685.67 30,378.97 (+295.67) +0.96% 497,516,465 KMI All Shares Index 21,748.55 21,769.15 21,476.59 (+271.96) +1.25% 239,947,851 Disclaimer: This report has been prepared by Standard Capital Securities (Pvt) Ltd. -

Shariah Compliance Screening Report

Al-Hilal Shariah Advisors December 2016 Shariah Compliance Screening Report INSIDE Key Highlights ......................................................................................................................................... 3 Shariah Compliant Companies ............................................................................................................... 5 Shariah Non - Compliant Companies ...................................................................................................... 7 Suspended & Delisted Companies………………………………………………………………………………………………….....9 Approved Islamic Banks & Windows for Placements ........................................................................... 10 Screening Guidelines for Equity Securities ........................................................................................... 11 Purification Guidelines .......................................................................................................................... 12 Al-Hilal Shariah Advisors (Pvt.) Limited. (Formerly Fortune Islamic (Pvt.) Limited) P a g e | 2 Al-Hilal Shariah Advisors (Pvt.) Limited. (Formerly Fortune Islamic (Pvt.) Limited) 27 April, 2017 KEY HIGHLIGHTS We have conducted Shariah compliance screening of 524 selected companies listed on the Pakistan Stock Exchange as per their latest financial statements (December’16), on the basis of the Shariah compliance screening mechanism approved by our Shariah Supervisory Council headed by Mufti Irshad Ahmad Aijaz. Following are the results for -

Capital Market

7 Capital Market 7.1 Introduction Pakistan’s capital market showed a mixed trend during FY01 (see Table7.1). The benchmark KSE- 100 index shed 10.1 percent since the beginning of FY01 and closed the year at 1366.4. This downturn can be attributed to a host of factors including the lack of concrete progress on privatization, uncertain investor confidence, the continuous depreciation of the Rupee and friction between SECP and the bourses. While equity market remained bearish, the corporate bond market showed encouraging movements. The growth in this market was encouraging, as ten new TFCs issues were floated during FY01 alone, compared to ten in the last five fiscal years. 7.2 Stock Market Performance The Karachi Stock Exchange (KSE) maintained Table 7.1: Key Indicators of Capital Market its dominance in the country (see Table 7.1). FY99 FY00 FY01 Karachi Stock Exchange Primary market activities in KSE remained KSE-100 index 1054.7 1520.7 1366.4 slow, as only four new companies (with paid up SBP General index 106.4 128.8 118.7 capital of Rs 3.6 billion), were listed during Paid up capital (billion Rs) 215.0 229.3 239.9 FY01. Similarly, only two companies were Turnover of shares (billion #) 25.5 48.1 29.2 floated on the Lahore stock exchange, of which Lahore Stock Exchange Hubco was already subscribed. Like the KSE- LSE-101 index 288.9 372.0 273.2 100 index, the LSE-101 also declined by 98.8 Turnover of shares (billion #) 9.8 16.4 7.8 Paid up capital (billion Rs) 186.9 207.7 226.2 points (26.5 percent) to 273.2 by end-FY01. -

LOADS LIMITED Manufacturers of Exhaust Systems, Radiators & Sheet Metal Components

LOADS LIMITED Manufacturers of Exhaust Systems, Radiators & Sheet Metal Components HALF YEARLY REPORT December 31, 2016 Contents Company Information 02 Directors’ Report 03 CONSOLIDATED FINANCIAL INFORMATION Condensed Interim Consolidated Balance Sheet (Un-Audited) 05 Condensed Interim Consolidated Profit & Loss Account (Un-Audited) 06 Condensed Interim Consolidated Statement of Comprehensive Income (Un-Audited) 07 Condensed Interim Consolidated Cash Flow Statement (Un-Audited) 08 Condensed Interim Consolidated Statement of Changes in Equity (Un-Audited) 09 Notes to the Condensed Interim Consolidated Financial Information (Un-Audited) 10 UNCONSOLIDATED FINANCIAL INFORMATION Auditors’ Report to member on Review of Interim Financial Information 12 Condensed Interim Unconsolidated Balance Sheet (Un-Audited) 13 Condensed Interim Unconsolidated Profit & Loss Account (Un-Audited) 14 Condensed Interim Unconsolidated Statement of Comprehensive Income (Un-Audited) 15 Condensed Interim Unconsolidated Cash Flow Statement (Un-Audited) 16 Condensed Interim Unconsolidated Statement of Changes in Equity (Un-Audited) 17 Notes to the Condensed Interim Unconsolidated Financial Information (Un-Audited) 18 Company Information Board of Directors Corporate Advisors Syed Shahid Ali – Chairman Cornelius, Lane & Mufti Mr. Saulat Said – Vice Chairman Advocates & Solicitors Mr. Munir K. Bana – Chief Executive Mr. Najam I. Chaudhri – Independent Director Bankers Mr. M. Ziauddin – Executive Director Syed Sheharyar Ali – Non-Executive Director Al Baraka Bank (Pakistan) -

Bulletin 21 Aug 07.FH10

July - August, 2007 Contents § Editors Corner ii § Abstract of the Bulletin 4 § Mutual Funds Development Pakistan Perspective 5 § Introduction to Mutual Fund Industry in Pakistan 8 § Prospects of Local Mutual Funds Industry 10 § Monetary Policy Statement July-December 2007 Key Features 12 § Monetary Policy Implications for the Banking Sector 14 § Trade Policy 2007-08 Highlights 15 § Performance of Microfinance Banks Operating in Pakistan 17 § Market Analysis 18 § Commercial Banks Listed on KSE at a Glance 22 § Book Reviews 23 § Pakistan Economy Key Economic Indicators 24 NBP Performance at a Glance July - August, 2007 Editors Corner Dear Readers, Pakistan celebrated 60 years of independence on August 14, 2007. The journey the nation has traversed during the last six decades has been both of achievement and difficulties. Each decade has had its challenges, success and disappointments. Various economic policies and planning processes have been pursued, giving a direction/determining the course of the economy. These policy changes have had far reaching economic consequences. Some have benefitted the economy and supported in the growth of the sub-sectors, while others have had unfavourable consequences for the different segments of the economy/population. The initial years were a period of adjustment for the new nation, with the government shouldering the task of settling the people and building an economic base. Considerable economic growth and development took place in the decade of the 60s, with significant increases in industrial and agricultural production and in the different sectors of the economy. This was despite many constraints and hurdles. It was a period when the public sector played a significant role of a facilitator and director, encouraging the private sector to come forward. -

Evidence from Equity Markets of Pakistan

Middle-East Journal of Scientific Research 13 (2): 241-247, 2013 ISSN 1990-9233 © IDOSI Publications, 2013 DOI: 10.5829/idosi.mejsr.2013.13.2.1894 Inevitability of Cross-Section Stock Returns: Evidence from Equity Markets of Pakistan Ahmad Raza Bilal, Muhammad Naveed, Noraini Bt. Abu Talib and Mohd Noor Azli Ali Khan Department of Management and Human Resource Development, Universiti Teknologi Malaysia, Skudai, Johar Bahru, Malaysia Abstract: In recent economic recession, portfolio theory progressively motivated banks to strategically concentrate on shareholders' investment returns. The analysis of the determinants of bank performance and their association with investment returns has become increasingly important. In presence of alternative investment opportunities of competitive market returns, bank stock performance is explored under depressed investment environment. For this research study, a sample of 16 banks listed at Karachi Stock Exchange was extracted on random basis. To calculate monthly stock returns, daily stock prices were used for a period of 2003-2010. Capital Asset Pricing Model (CAPM) was used to compute the expected bank stock returns. Results of performance metrics demonstrated insignificant correlation in movements of bank stock returns. Findings of this study suggested that in reflection of better market returns, banks tend to outperform for improvement of their shareholders' investment returns and value maximization. Key words: Stock returns Karachi Stock Exchange (KSE) CAPM Systematic Risk Market Returns INTRODUCTION value (NPV). Many stock exchanges around the world compute indices for specific sectors like banks and Karachi Stock Exchange (KSE) was established on financial institutions which are economic engines owing 18th September, 1947 just after independence of Pakistan to their mediator function between depository funds and with an initial capital of PKR 37 million. -

Shariah Compliance Screening Report

Al-Hilal Shariah Advisors JUNE 2017 Shariah Compliance Screening Report Al-Hilal Shariah Advisors (Pvt.) Limited. INSIDE Key Highlights ................................ .......................................................................................................... 4 Shariah Compliant Companies ................................ ............................................................................... 8 Shariah Non - Compliant Companies .................................................................................................... 10 Suspended & Delisted Companies…………………………………………………………………………………………………...12 Approved list of Sukuk………………………………………………………………………………………………….....................13 Approved Islamic Banks & Windows for Placements……………….……………………………………………………….14 Approved list of charitable orginizations ............................................................................................. 15 Screening Guidelines for Equity Securities ........................................................................................... 16 Purification Guidelines .......................................................................................................................... 16 P a g e | 2 Al-Hilal Shariah Advisors (Pvt.) Limited. P a g e | 3 Al-Hilal Shariah Advisors (Pvt.) Limited. 14 July, 2017 KEY HIGHLIGHTS We have conducted Shariah compliance screening of 554 selected companies listed on the Pakistan Stock Exchange as per their latest financial statements (June’17), on the basis of the Shariah compliance -

Daily Market Insights

DAILY MARKET INSIGHTS 4-Feb-2021 Change Index points KSE 100 INDEX PERFORMANCE OVERVIEW PKR % Change Closing KSE 100 Index (28) 46,906 Contributing shares Closing Price - Rs. Mari Petroleum Company Limited 104.93 7.34 60.40 1,533.98 Lucky Cement Limited 16.67 2.33 49.35 731.41 TRG Pakistan Limited (3.91) (3.17) (41.49) 119.41 KSE 100 INDEX VOLUMES Today 238 5 days average 338 304 14 days average Millions Source: https://formerdps.psx.com.pk/ & Calculations of Kifayah Investment Management Limited Top most buyer Top most seller PORTFOLIO INVESTMENT SUMMARY Mutual Funds Broker Proprietary Trading Amount (Net) 347,748,311 (276,388,859) Buying / Selling sector wise composition Oil and Gas Exploration Companies 22.53% 2.86% Cement 18.66% 10.43% Debt Market 17.35% 0.00% Technology and Communication 4.78% 39.13% All other Sectors 14.62% 32.24% Source: https://www.nccpl.com.pk/en/market-information/fipi-lipi/fipi-normal-daily FOREIGN PORTFOLIO INVESTMENT TREND Today 310 (199) 5 days average (73) 14 days average Millions Source: https://www.nccpl.com.pk/en/market-information/fipi-lipi/fipi-normal-daily & Calculations of Kifayah Investment Management Limited MATERIAL INFORMATION Disclosure of Interest by a Substantial Shareholder, sold 10,000 shares at the average Artistic Denim Mills Limited price of Rs. 134.09 each on 3 February 2021. Nishat Power Limited (NPL) a Subsidiary Company of Nishat Mills Limited and the Central Power Purchasing Agency (Guarantee) Limited have initialed “Master Nishat Mills Limited Agreement” and “PPA Amendment Agreement”. -

All Share Islamic Index for the Period Ended December 2020 (Complete Ratios)

FINAL RECOMPOSITION LIST- KMI-ALL SHARE ISLAMIC INDEX FOR THE PERIOD ENDED DECEMBER 2020 (COMPLETE RATIOS) Income Ratio / Illiquid Assets Net Liquid Share Price as Debt Ratio Investment Ratio Charity Rate Final Shariah No. Ticker Company Name Objective Ratio (IA/TA => Assets Ratio of December (D/A < 37%) (NCInv/TA < 33%) (NCInc/TR < Status 25%) (NLA < P) 31st 2020. 5%) 1 AABS Al-Abbas Sugar Mills Ltd Compliant 20.40% 30.72% 1.51% 44.61% 28.78 335.97 Compliant1 2 ABOT Abbott Lab (Pakistan) Ltd Compliant 3.28% 0.00% 0.93% 57.65% 12.54 755.37 Compliant 3 ACPL Attock Cement Pakistan Ltd * Compliant 15.03% 0.00% 0.04% 75.01% (29.21) 0 Compliant 4 AGIL Agriauto Industries Ltd * Compliant 0.24% 7.64% 0.52% 60.96% 53.75 234.25 Compliant 5 AGP AGP Limited Compliant 0.00% 0.00% 0.18% 86.28% (2.08) 0 Compliant 6 AGSML Abdullah Shah Ghazi Sugar Mills Compliant 16.05% 0.00% 0.00% 97.50% (42.42) 0 Compliant1 7 APL Attock Petroleum Ltd * Compliant 11.51% 4.71% 0.65% 56.75% (89.84) 0 Compliant 8 ASC Al Shaheer Corporation Ltd * Compliant 20.21% 0.00% 0.02% 62.15% 1.35 15.54 Compliant 9 ASTM Asim Textile Mills Ltd * Compliant 0.00% 1.34% 0.50% 76.19% (37.60) 0 Compliant 10 ATBA Atlas Battery Ltd * Compliant 19.74% 1.65% 0.13% 81.65% (70.12) 0 Compliant 11 PREMA At-Tahur Limited * Compliant 9.11% 0.00% 0.06% 86.55% (2.40) 0 Compliant 12 ATLH Atlas Honda Ltd * Compliant 1.85% 15.76% 1.41% 42.78% 6.61 500 Compliant1 13 ATRL Attock Refinery Ltd * Compliant 7.34% 0.00% 0.72% 69.84% (225.01) 0 Compliant 14 BATA Bata (Pakistan) Ltd Compliant 32.38% 12.10% 0.39% 63.64% (335.99) 0 Compliant 15 BGL Balochistan Glass Ltd * Compliant 27.62% 0.00% 0.01% 90.81% (5.28) 0 Compliant 16 BIFO Biafo Industries Ltd * Compliant 20.62% 11.92% 0.86% 64.26% 3.41 154.2 Compliant 17 BWCL Bestway Cement Ltd * Compliant 17.91% 15.32% 1.73% 76.32% (23.96) 0 Compliant 18 CEPB Century Paper & Board Mills * Compliant 29.53% 0.00% 0.14% 79.85% (37.04) 0 Compliant 19 CHCC Cherat Cement Co.