An Investment Guide to Zambia Opportunities and Conditions 2011

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Chileshe, Mutale

Economic shocks, poverty and household food insecurity in urban Zambia: an ethnographic account of Chingola Mutale Chileshe CHLMUT001 Town Cape of Thesis Presented for the Degree of Doctor of Philosophy in the Department of Environmental and Geographical UniversityScience University of Cape Town September 2014 Supervisor: Dr. Jane Battersby-Lennard The copyright of this thesis vests in the author. No quotation from it or information derived from it is to be published without full acknowledgement of the source. The thesis is to be used for private study or non- commercial research purposes only. Published by the University of Cape Town (UCT) in terms of the non-exclusive license granted to UCT by the author. Univeristy of Cape Town DECLARATION I, Mutale Chileshe, hereby declare that the work on which this thesis is based is my original work (except where acknowledgements indicate otherwise) and that neither the whole work nor any part of it has been, is being, or is to be submitted for another degree in this or any other university. I authorise the University to reproduce for the purpose of research either the whole or any portion of the contents in any manner whatsoever. Signed: ___________________________ Date: 18/09/2014 ii DEDICATION This thesis is dedicated to my husband, Kelvin Chola Chibangula, for his unwavering encouragement, patience, and support of every kind. iii ACKNOWLEDGEMENTS Completion of this doctoral dissertation was possible with the support of several people. First and foremost, I would like to thank Dr Jane Battersby for her patient, highly critical and equally encouraging supervisory role. Her dedication to my work is very much appreciated. -

George Loft Papers

http://oac.cdlib.org/findaid/ark:/13030/kt6b69r101 No online items Inventory of the George Loft papers Finding aid prepared by Hoover Institution Library and Archives Staff Hoover Institution Library and Archives © 2007 434 Galvez Mall Stanford University Stanford, CA 94305-6003 [email protected] URL: http://www.hoover.org/library-and-archives Inventory of the George Loft 2006C21 1 papers Title: George Loft papers Date (inclusive): 1957-1989 Collection Number: 2006C21 Contributing Institution: Hoover Institution Library and Archives Language of Material: English Physical Description: 11 manuscript boxes(4.4 Linear Feet) Abstract: Correspondence, memoranda, reports, interview summaries, printed matter, and photographs, relating to American Friends Service Committee activities in Africa, especially relating to housing in Zambia; international development projects in Africa; and political and social conditions in Zambia, Zimbabwe and elsewhere in Africa. Creator: Loft, George Hoover Institution Library & Archives Access The collection is open for research; materials must be requested at least two business days in advance of intended use. Publication Rights For copyright status, please contact the Hoover Institution Library & Archives. Acquisition Information Acquired by the Hoover Institution Library & Archives in 2005. Preferred Citation [Identification of item], George Loft Papers, [Box no., Folder no. or title], Hoover Institution Library & Archives. 1915 Born, New York City January 27 1931 Graduated, High School of Commerce, New York 1932-1942 Assistant to Economist, National Dairy Products Corporation, New York 1938 Graduated, Bachelor's degree in Accounting, New York University 1940 Completed Master of Business Administration, New York University 1942 Married Eleanor Riddle 1942-1945 Chief of Subsistence Requirements Section, Military Planning Division, Office of the Quartermaster General, Washington, D.C. -

OF ZAMBIA ...Three Infants Among Dead After Overloaded Truck Tips Into

HOME NEWS: FEATURE: ENTERTAINMENT: SPORT: KK in high Rising suicide RS\ FAZ withdraws spirits, says cases source of industry has from hosting Chilufya– p3 concern- p17 potential to U-23 AfCON grow’ – p12 tourney – p24 No. 17,823 timesofzambianewspaper @timesofzambia www.times.co.zm TIMES SATURDAY, JULY 22, 2017 OF ZAMBIA K10 ...Three infants among dead after overloaded 11 killed as truck tips into drainage in Munali hills truck keels over #'%$#+,$ drainage on the Kafue- goods –including a hammer-mill. has died on the spot while four Mission Hospital,” Ms Katongo a speeding truck as the driver “RTSA is saddened by the other people sustained injuries in said. attempted to avoid a pothole. #'-$%+Q++% Mazabuka road on death of 11 people in the Munali an accident which happened on She said the names of the The incident happened around +#"/0$ &301"7,'%&2T &'**1 20$L'! !!'"#,2 -, 2&# $3# Thursday. victims were withheld until the 09:40 hours in the Mitec area on #-++-$ Police said the 40 passengers -Mazabuka road. The crash The accident happened on the next of keen were informed. the Solwezi-Chingola road. ++0+% .#-.*#Q +-,% travelling in the back of a Hino could have been avoided had the Zimba-Kalomo Road at Mayombo Ms Katongo said in a similar North Western province police truck loaded with an assortment passengers used appropriate area. ',!'"#,2Q L'4#V7#0V-*" -7 -$ !&'#$36#,1'-)'"#,2'L'#"2&# 2&#+ 2&0## $Q &4# of goods - including a hammer means of transport,” he said. Police spokesperson Esther Hospital township in Chama deceased as Philip Samona, saying died on the spot while mill - were heading to various Southern Province Minister Katongo said in a statement it district, died after he was hit by he died on the spot. -

Half Marathon. Kariba Town 11-16 August

Dear All They were playing polocrosse this weekend so I went down to take a look. It is being held at Chundukwa where the club is based. Lots of fun for all the family. There are four teams playing: Livingstone, Choma, Leopards Hill and Lusaka South. These are the main teams in Zambia. The Zambia Police used to play but have not been joining in for some time. Come on, Zambia Police, get your team going again – it is good for public/private relationships. Zambia has a national team which recently played in South Africa. Since that time our team has been recognised internationally and we are now 8 th in the world. Even ts on the Way 11 August: Half Marathon. Kariba Livingstone Airport Town 11-16 August: Cycle Zambia. Our town is looking very smart. Work continues on the roads 12-22 August: Mzanzi Trophy – Etosha and other facilities. The airport is due to be completed by to Livingstone. th August 13 , according to George who showed me around the 21 August: Zambezi Classic Fishing other day. However, according to a report in the press, the Competition. Katima Mulilo work was supposed to have been completed by 1 August. 24-29 August: UNWTO Transport, Works, Supply and Communications Minister 2-4 October: Fishing Competition. Yamfwa Mukanga, on a visit to the airport: I don't want to be Kariba Town coming here and waste my time just to see uncompleted 26 October: Zambezi Kayak Festival. structures. I am giving you 10 days to complete the structure. 26-31 October: World Adventure Travel Summit. -

The Coincidence of Ecological Opportunity with Hybridization Explains Rapid Adaptive Radiation in Lake Mweru Cichlid fishes

ARTICLE https://doi.org/10.1038/s41467-019-13278-z OPEN The coincidence of ecological opportunity with hybridization explains rapid adaptive radiation in Lake Mweru cichlid fishes Joana I. Meier 1,2,3,4, Rike B. Stelkens 1,2,5, Domino A. Joyce 6, Salome Mwaiko 1,2, Numel Phiri7, Ulrich K. Schliewen8, Oliver M. Selz 1,2, Catherine E. Wagner 1,2,9, Cyprian Katongo7 & Ole Seehausen 1,2* 1234567890():,; The process of adaptive radiation was classically hypothesized to require isolation of a lineage from its source (no gene flow) and from related species (no competition). Alternatively, hybridization between species may generate genetic variation that facilitates adaptive radiation. Here we study haplochromine cichlid assemblages in two African Great Lakes to test these hypotheses. Greater biotic isolation (fewer lineages) predicts fewer constraints by competition and hence more ecological opportunity in Lake Bangweulu, whereas opportunity for hybridization predicts increased genetic potential in Lake Mweru. In Lake Bangweulu, we find no evidence for hybridization but also no adaptive radiation. We show that the Bangweulu lineages also colonized Lake Mweru, where they hybridized with Congolese lineages and then underwent multiple adaptive radiations that are strikingly complementary in ecology and morphology. Our data suggest that the presence of several related lineages does not necessarily prevent adaptive radiation, although it constrains the trajectories of morphological diversification. It might instead facilitate adaptive radiation when hybridization generates genetic variation, without which radiation may start much later, progress more slowly or never occur. 1 Division of Aquatic Ecology & Evolution, Institute of Ecology and Evolution,UniversityofBern,Baltzerstr.6,CH-3012Bern,Switzerland.2 Department of Fish Ecology and Evolution, Centre of Ecology, Evolution and Biogeochemistry (CEEB), Eawag Swiss Federal Institute of Aquatic Science and Technology, Seestrasse 79, CH-6047 Kastanienbaum, Switzerland. -

Zambeef Products PLC Annual Report 2015 Our Profile

the ing Na d ti e o e n Feeding a Growing F Products PLC Continent Zambeef Products PLC Annual Report 2015 Our profile Zambeef Products PLC (“Zambeef”, the “Company”, or, together with its subsidiaries the “Group”) is one of the largest integrated agribusinesses in Zambia. The Zambeef Group is one of the largest integrated agri-businesses in Zambia, in- volved in the primary production, processing, distribution and retailing of beef, chick- ens, pork, milk, eggs, dairy products, fish, flour and stock feed, throughout Zambia and the surrounding region, as well as Nigeria and Ghana. The Group is also one of the largest cereal row cropping operations in Zambia, with a total of 24,174 hectares planted during FY2015 comprising a mix of approximately [two growing seasons] of 8,120 Ha of irrigated land and one growing season of approximately 8,480 Ha of rain-fed/dry land, available for planting each year. Overview Strategic Corporate Financial report governance statements Overview 1 Highlights 3 Challenges 4 Zambeef at a glance 5 Feeding a growing continent Strategic report 10 Chairman’s report 14 Joint Chief Executives’ review 18 Operational and financial review Cropping Beef Chicken and eggs Pork Milk and dairy Fish Stockfeed Edible oils Mill Leather and shoes West Africa 24 Sustainability report Corporate governance 30 Corporate governance 34 Board of directors 36 Report of the directors 41 Statement of directors’ responsi- bilities Financial statements 44 Report of the independent audi- tors 45 Statement of comprehensive income 46 Consolidated -

Zambia Page 1 of 16

Zambia Page 1 of 16 Zambia Country Reports on Human Rights Practices - 2002 Released by the Bureau of Democracy, Human Rights, and Labor March 31, 2003 Zambia is a republic governed by a president and a unicameral national assembly. Since 1991 generally free and fair multiparty elections have resulted in the victory of the Movement for Multi -Party Democracy (MMD). In December 2001, Levy Mwanawasa of the MMD was elected president, and his party won 69 out of 150 elected seats in the National Assembly. The MMD's use of government resources during the campaign raised questions over the fairness of the elections. Although noting general transparency during the voting, domestic and international observer groups cited irregularities in the registration process and problems in the tabulation of the election results. Opposition parties challenged the election result in court, and court proceedings remained ongoing at year's end. The Constitution mandates an independent judiciary, and the Government generally respected this provision; however, the judicial system was hampered by lack of resources, inefficiency, and reports of possible corruption. The police, divided into regular and paramilitary units operated under the Ministry of Home Affairs, had primary responsibility for maintaining law and order. The Zambia Security and Intelligence Service (ZSIS), under the Office of the President, was responsible for intelligence and internal security. Members of the security forces committed numerous, and at times serious, human rights abuses. Approximately 60 percent of the labor force worked in agriculture, although agriculture contributed only 22 percent to the gross domestic product. Economic growth slowed to 3 percent for the year, partly as a result of drought in some agricultural areas. -

Value Chain Analysis Tourism Zambia

Value Chain Analysis Tourism Zambia Commissioned by The Centre for the Promotion of Imports from developing countries (CBI) Acorn Tourism Consulting Ltd November 2018 TABLE OF CONTENTS MANAGEMENT SUMMARY 1. INTRODUCTION 2. EU TOURISM MARKETS AND ZAMBIA’S COMPETITIVE POSITION 2.1 Export Market Demand and Trends 2.2 Zambia’s Competitiveness 2.3 Strategic Context: Plans for the Zambian Tourism Sector 2.4 Potential for New Products and Regions 3. ZAMBIA’S TOURISM VALUE CHAIN 3.1 Structure and Governance of the Value Chain 3.2 Governance Challenges 3.3 Sustainability of the Tourism Value Chain 4. OPPORTUNITIES AND OBSTACLES 4.1 Key Opportunities for Zambian SMEs 4.2 Obstacles for Zambian SMEs 4.3 Public Sector Opportunities and Constraints 5. WHAT CBI CAN DO TO SUPPORT A MORE COMPETITIVE AND SUSTAINABLE TOURISM VALUE CHAIN IN ZAMBIA 2 ACCRONYMS CSR Corporate Social Responsibility DNPW Department of National Parks and Wildlife EU European Union GMA Game Management Area KAZA Kavango Zambezi KKIA Kenneth Kwanda International Airport LTA Livingstone Tourist Association NP National Park MoTA Ministry of Tourism and Arts MOU Memorandum of Understanding NHCC National Heritage Conservation Commission PMU Project Management Unit PUM PUM Netherlands Senior Experts RETOSA Regional Tourism Organisation of Southern Africa SADC South African Development Community SEO Search Engine Optimisation SME Small and Medium sized Enterprises TAP Technical Assistance Programme TCZ Tourism Council of Zambia TDA Tourism Development Area TEVETA Technical Education, Vocational and Entrepreneurship Training Authority UNWTO United Nations World Tourism Organisation ZATEX Zambia Tourism Exposition ZATO Zambia Association of Tour Operators ZITHS Zambia Institute for Tourism and Hospitality Studies ZMK Zambia kwacha ZTA Zambia Tourism Agency ZTMP Zambia Tourism Master Plan 3 MANAGEMENT SUMMARY Zambia’s appeal to the European leisure visitor is based on its natural resources, including its unspoiled and varied landscape. -

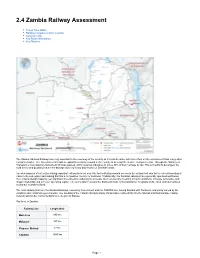

2.4 Zambia Railway Assessment

2.4 Zambia Railway Assessment Travel Time Matrix Railway Companies and Consortia Capacity Table Key Route Information Key Stations The Zambia National Railways are very important to the economy of the country as it is a bulk carrier with less effect on the environment than many other transport modes. The Government intends to expand its railway network in the country to develop the surface transport sector. Through the Ministry of Transport, a new statutory instrument (SI) was passed, which requires industries to move 30% of their carriage by rail. This is in a bid to decongest the road sector and possibly reduce the damage done by heavy duty trucks on Zambian roads. The development of rail routes linking important exit points is not only vital for facilitating smooth access to the outside but also for the overall boosting of trade in the sub-region and making Zambia a competitive country for business. Traditionally, the Zambian railways have generally operated well below their original design capacity, yet significant investment is underway to increase their volumes by investing in track conditions, increase locomotive and wagon availability and increase operating capital. The rail network remains the dominant mode of transportation for goods on the local and international routes but is under-utilized. The main railway lines are the Zambia Railways, owned by Government and the TAZARA line, linking Zambia with Tanzania, and jointly owned by the Zambian and Tanzanian governments. The opening of the Chipata-Mchinji railway link provides connectivity into the Malawi and Mozambique railway network and further connects Zambia to the port of Nacala. -

Fishing Life in the Bangweulu Swamps (2): an Analysis of Catch and Seasonal Emigration of the Fishermen in Zambia

African Stud)' Monographs, Supplementary Issue 6: 33-G3, March 1987 33 Fishing Life in the Bangweulu Swamps (2): An Analysis of Catch and Seasonal Emigration of the Fishermen in Zambia. lchiro IMAI (Research Affiliate of I. A. S.) The Institute for African Studies, University of Zambia Hirosaki University. Japan ABSTRACT The aim of this paper is to describe and characterize the swamp fishing in the Bangweulu Swamps, Zambia. The fish catch by the several fishing methods are analy sed after these methods are outlined. As a result of the analysis, it is indicated that each production unit chooses a fishing method to catch a particular group of fish, such as "-1or myridae or Cichlidae fish. The types of fishing activity among the lishermen are divided into three classes in terms of their fishing seasons and methods. These types of fishing differ from each other as to how far their villages are from the swamps and what time schedules of agriculture are made according to the limits of the season or the period of fishing in the swamps. By ana lysing these types alloted to different ethnic groups, it is clarified how the swamp area is actually utilized by the several ethnic groups from different areas. I\fost of the fishermen in the Bangweulu Swamps are the part-time fishermen who are also engaged in cultivation to a considerable extent. It is discussed why these essentially agriculturalists carry on fishing for themselves without making symbiotic relationships with other fishing specialists. They can get a good cash income by selling the catch. -

Full Text Document (Pdf)

Kent Academic Repository Full text document (pdf) Citation for published version Macola, Giacomo (2006) “It Means as If We Are Excluded from the Good Freedom”: Thwarted Expectations of Independence in the Luapula Province of Zambia, 1964-1967. Journal of African History, 47 (1). pp. 43-56. ISSN 0021-8537. DOI https://doi.org/10.1017/S0021853705000848 Link to record in KAR https://kar.kent.ac.uk/7559/ Document Version UNSPECIFIED Copyright & reuse Content in the Kent Academic Repository is made available for research purposes. Unless otherwise stated all content is protected by copyright and in the absence of an open licence (eg Creative Commons), permissions for further reuse of content should be sought from the publisher, author or other copyright holder. Versions of research The version in the Kent Academic Repository may differ from the final published version. Users are advised to check http://kar.kent.ac.uk for the status of the paper. Users should always cite the published version of record. Enquiries For any further enquiries regarding the licence status of this document, please contact: [email protected] If you believe this document infringes copyright then please contact the KAR admin team with the take-down information provided at http://kar.kent.ac.uk/contact.html ‘IT MEANS AS IF WE ARE EXCLUDED FROM THE GOOD FREEDOM’: THWARTED EXPECTATIONS OF INDEPENDENCE IN THE LUAPULA PROVINCE OF ZAMBIA, 1964-1966* BY GIACOMO MACOLA Centre of African Studies, University of Cambridge ABSTRACT: Based on a close reading of new archival material, this article makes a case for the adoption of an empirical, ‘sub-systemic’ approach to the study of nationalist and post- colonial politics in Zambia. -

Investors Guide on Poultry in Zambia

Investors Guide Poultry in Zambia Investors Guide on Poultry in Zambia Foreword As a strategy to contribute to Companies seeking the different asing poultry feed ingredient of improved investment and compe- investment opportunities. maize and soybeans. titiveness of the Zambian poultry Notwithstanding lack of data on For more information, you can industry, the Embassy of the King- Zambia’s poultry imports and visit http://zimbabwe.nlembassy. dom of the Netherlands in Harare exports, the market study esta- org/key-topics/trade-information/ in conjunction with AgriProFocus blished that the Zambia poultry doing-business-in-zambia.html . Zambia and the Poultry Associ- has been growing steadily for the ation of Zambia commissioned past five years averaging around 8 The full market study on the a market study on investment % and 20% for broilers and layers Investment Opportunities in the opportunities to inform the Dutch annual production respectively. Poultry Sector in Zambia can be businesses that have interest in The rapid poultry production accessed on the AgriProFocus investing in the Zambian poultry increase is attributed to a num- Zambia website: www.agriprofo- industry. ber of factors such as national cus.com/zambia population increase, disposable In the poultry sector lie different income rise buoyed by growing investment opportunities. This middle income class, investment guide highlights these opportu- in poultry breeding, production nities, the costs of investments, and processing as well as incre- expected returns and the Poultry 2 Investors Guide on Poultry in Zambia Overview Zambia Zambia has had a long period of all growth rate of Sub-Saharan political stability. Independent Africa.