Mckinsey on Semiconductors

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Quantum Imaging for Semiconductor Industry

Quantum Imaging for Semiconductor Industry Anna V. Paterova1,*, Hongzhi Yang1, Zi S. D. Toa1, Leonid A. Krivitsky1, ** 1Institute of Materials Research and Engineering, Agency for Science Technology and Research (A*STAR), 138634 Singapore *[email protected] **[email protected] Abstract Infrared (IR) imaging is one of the significant tools for the quality control measurements of fabricated samples. Standard IR imaging techniques use direct measurements, where light sources and detectors operate at IR range. Due to the limited choices of IR light sources or detectors, challenges in reaching specific IR wavelengths may arise. In our work, we perform indirect IR microscopy based on the quantum imaging technique. This method allows us to probe the sample with IR light, while the detection is shifted into the visible or near-IR range. Thus, we demonstrate IR quantum imaging of the silicon chips at different magnifications, wherein a sample is probed at 1550 nm wavelength, but the detection is performed at 810 nm. We also analyze the possible measurement conditions of the technique and estimate the time needed to perform quality control checks of samples. Infrared (IR) metrology plays a significant role in areas ranging from biological imaging1-5 to materials characterisation6 and microelectronics7. For example, the semiconductor industry utilizes IR radiation for non-destructive microscopy of silicon-based devices. However, IR optical components, such as synchrotrons8, quantum cascade lasers, and HgCdTe (also known as MCT) photodetectors, are expensive. Some of these components, in order to maximize the signal-to-noise ratio, may require cryogenic cooling, which further increases costs over the operational lifetime. -

Global Semiconductor Industry | Accenture

GLOBALITY AND COMPLEXITY of the Semiconductor Ecosystem The semiconductor industry is a truly global affair. Around the world, semiconductor chip designers use intellectual property (IP) licenses and design verification to provide designs to wafer fabricators, which use raw silicon, photomasks, and equipment to create chips for package manufacturing to assemble with printed circuit board (PCB) substrates for delivery to end customers. In fact, components for a chip could travel more than 25,000 miles by the time it finds its way into a television set, mobile phone, automobile, computer, or any of the millions of products that now rely on chips to operate (Figure 1). 2 | Globality and Complexity of the Semiconductor Ecosystem Figure 1: Components for a chip could travel more than 25,000 miles before completion IP Licenses Euipment Modules Package Raw Silicon Manufacturing PC Substrates Asembly Standard Products and Test components Wafer Fabrication Equipment Chip Design Design Verification Photomask Wafer Manufacturing Fabrication The Global Semiconductor Alliance (GSA) and Accenture have teamed up to conduct a joint study on the globality and complexity of the semiconductor ecosystem to explore the interdependencies and benefits of the cross-border partnerships required to produce semiconductors, as well as to illustrate what’s needed to keep this global ecosystem operating efficiently and profitably. Industry executives can use this study to inform their company strategies, as well as to educate non-semiconductor partners, including policy makers, on the nature of their business to promote a better understanding of the important role semiconductors play in everyday life and on the globe-spanning ecosystem that’s needed to produce them. -

Chapter1: Semiconductor Diode

Chapter1: Semiconductor Diode. Electronics I Discussion Eng.Abdo Salah Theoretical Background: • The semiconductor diode is formed by doping P-type impurity in one side and N-type of impurity in another side of the semiconductor crystal forming a p-n junction as shown in the following figure. At the junction initially free charge carriers from both side recombine forming negatively c harged ions in P side of junction(an atom in P -side accept electron and be comes negatively c harged ion) and po sitive ly c harged ion on n side (an atom in n-side accepts hole i.e. donates electron and becomes positively charged ion)region. This region deplete of any type of free charge carrier is called as depletion region. Further recombination of free carrier on both side is prevented because of the depletion voltage generated due to charge carriers kept at distance by depletion (acts as a sort of insulation) layer as shown dotted in the above figure. Working principle: When voltage is not app lied acros s the diode , de pletion region for ms as shown in the above figure. When the voltage is applied be tween the two terminals of the diode (anode and cathode) two possibilities arises depending o n polarity of DC supply. [1] Forward-Bias Condition: When the +Ve terminal of the battery is connected to P-type material & -Ve terminal to N-type terminal as shown in the circuit diagram, the diode is said to be forward biased. The application of forward bias voltage will force electrons in N-type and holes in P -type material to recombine with the ions near boundary and to flow crossing junction. -

A Report on Semiconductor Foundry Access by US Academics (Discussion Held at a Meeting Virtually Held at the National Science Foundation on Dec 16, 2020)

A Report on Semiconductor Foundry Access by US Academics (Discussion held at a meeting virtually held at the National Science Foundation on Dec 16, 2020) Organizers: Sankar Basu1, Erik Brunvand2, Subhasish Mitra3, H.-S. Philip Wong4 Scribes: Sayeef Salahuddin5, Shimeng Yu6 1 NSF, [email protected] 2 NSF, [email protected] 3 Stanford University, [email protected] 4 Stanford University, [email protected] 5 University of California, Berkeley, [email protected] 6 Georgia Institute of Technology, [email protected] 2 Executive Summary Semiconductor technology and microelectronics7 is a foundational technology that without its continued advancement, the promises of artificial intelligence (AI), 5G/6G communication, and quantum computing will never be realized in practice. Our nation’s economic competitiveness, technology leadership, and national security, depend on our staying at the forefront of microelectronics. We must accelerate the pace of innovation and broaden the pool of researchers who possess research capability in circuit design and device technologies, and provide a pathway to translate these innovations to industry. This meeting has brought to the fore the urgent need for access to semiconductor foundry and design ecosystem to achieve these goals. Microelectronics is a field that requires sustained and rapid innovations, especially as the historical rate of progress following a predictable path, is no longer guaranteed as it had been in the past. Yet, there are many plausible paths to move forward, and the potential for further advances is immense. There is a future in system integration of heterogeneous technologies that requires end-to-end co-design and innovation. Isolated push along silos, such as miniaturization of components, will be inadequate. -

Review of Innovation Practices in Small Manufacturing Companies

Review of Innovation Practices in Small Manufacturing Companies Anthony Warren and Gerald Susman Smeal College of Business The Pennsylvania State University With the assistance of Jonathan Butz Anupam Jaiswal Prashant Jhaveri Tolga Sakman Prepared for National Institute of Standards and Technology United States Department of Commerce Table of Contents Executive Summary......................................................................................................................5 1. Background..........................................................................................................................9 2. Definition of Innovation As Applied to This Project.........................................................14 3. Models of Innovation.........................................................................................................15 4. Taxonomy Derived by Testing Factors Related to Innovation Success ............................17 4.1 Development of Primary Categories and Key Factors .............................................17 4.2 Research Methodology .............................................................................................21 4.3 Results.......................................................................................................................22 5. Support for Factors Included in the Empirically Derived Taxonomy ...............................27 5.1 Manufacturing OR Service? .....................................................................................27 5.2 The Role -

ADMINISTRATIVE PANEL DECISION Case No

ADMINISTRATIVE PANEL DECISION Case No. CN-2101385 Complainants: Canaan Creative Co., Ltd. (Complainant 1); Hangzhou Canaan Creative Information Technology Co., Limited (Complainant 2) Respondent: Bo Wang Domain Name: canaanavalonminers.com Registrar: NameCheap, Inc. 1. Procedural History On February 7, 2021, the Complainants submitted a Complaint in English to the Beijing Office of the Asian Domain Name Dispute Resolution Center (the ADNDRC Beijing Office) and elected this case to be dealt with by a one-person panel, in accordance with the Uniform Domain Name Dispute Resolution Policy (the Policy) and the Rules for Uniform Domain Name Dispute Resolution Policy (the Rules) approved by the Internet Corporation for Assigned Names and Numbers (ICANN), and the ADNDRC Supplemental Rules for Uniform Domain Name Dispute Resolution Policy (the ADNDRC Supplemental Rules) approved by the ADNDRC. On February 7, 2021, the ADNDRC Beijing Office sent to the Complainants by email an acknowledgment of the receipt of the Complaint and transmitted by email to ICANN and the Registrar, NameCheap, Inc., a request for registrar verification in connection with the disputed domain name. On April 9, 2021, the Registrar transmitted by email to the ADNDRC Beijing Office its verification response, confirming that the Respondent is listed as the registrant and providing the contact details. On April 20, 2021, the ADNDRC notified the Complainants that the Complaint has been confirmed and transmitted to the Respondent and the case officially commenced. On the same day, the ADNDRC Beijing Office transmitted the Written Notice of the Complaint to the Respondent by email and post, which informed that the Complainants had filed a Complaint against the disputed domain name and the ADNDRC Beijing Office had sent the complaint and its attachments through email according to the Rules and the Supplemental Rules. -

Timeline of the Semiconductor Industry in South Portland

Timeline of the Semiconductor Industry in South Portland Note: Thank you to Kathy DiPhilippo, Executive Director/Curator of the South Portland Historical Society and Judith Borelli, Governmental Relations of Texas Inc. for providing some of the information for this timeline below. Fairchild Semiconductor 1962 Fairchild Semiconductor (a subsidiary of Fairchild Camera and Instrument Corp.) opened in the former Boland's auto building (present day Back in Motion) at 185 Ocean Street in June of 1962. They were there only temporarily, as the Western Avenue building was still being constructed. 1963 Fairchild Semiconductor moves to Western Avenue in February 1963. 1979 Fairchild Camera and Instrument Corp. is acquired/merged with Schlumberger, Ltd. (New York) for $363 million. 1987 Schlumberger, Ltd. sells its Fairchild Semiconductor Corp. subsidiary to National Semiconductor Corp. for $122 million. 1997 National Semiconductor sells the majority ownership interest in Fairchild Semiconductor to an investment group (made up of Fairchild managers, including Kirk Pond, and Citcorp Venture Capital Ltd.) for $550 million. Added Corporate Campus on Running Hill Road. 1999 In an initial public offering in August 1999, Fairchild Semiconductor International, Inc. becomes a publicly traded corporation on the New York Stock Exchange. 2016 Fairchild Semiconductor International, Inc. is acquired by ON Semiconductor for $2.4 billion. National Semiconductor 1987 National Semiconductor acquires Fairchild Semiconductor Corp. from Schlumberger, Ltd. for $122 million. 1995 National Semiconductor breaks ground on new 200mm factory in December 1995. 1996 National Semiconductor announces plans for a $600 million expansion of its facilities in South Portland; construction of a new wafer fabrication plant begins. 1997 Plant construction for 200mm factory completed and production starts. -

The Next Growth Engine for the Semiconductor Industry

www.pwc.com The Internet of Things: The next growth engine for the semiconductor industry A study of global semi conductor trends and powerful drivers behind them – special focus on the impacts of Internet of Things. The Internet of Things: The next growth engine for the semiconductor industry A study of global semi conductor trends and powerful drivers behind them – special focus on the impacts of Internet of Things. The Internet of Things: The next growth engine for the semiconductor industry Published by PricewaterhouseCoopers AG Wirtschaftsprüfungsgesellschaft By Raman Chitkara, Werner Ballhaus, Olaf Acker, Dr. Bin Song, Anand Sundaram and Maria Popova May 2015, 36 pages, 8 figures The results of this survey and the contributions from our experts are meant to serve as a general reference for our clients. For advice on individual cases, please refer to the sources cited in this study or consult one of the PwC contacts listed at the end of the publication. Publications express the opinions of the authors. All rights reserved. Reproduction, microfilming, storing or processing in electronic media is not allowed without the permission of the publishers. Printed in Germany © May 2015 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details. MW-15-2285 Preface Preface The ever-expanding array of cutting-edge devices such as smartphones, tablets, ultramobile, electric cars, new aircraft, and wearable devices, is driving a constant expansion of the number of semiconductor components we use in our daily lives. -

SEMICONDUCTORS MCU/MPU/DSP Kionix

SEMICONDUCTORS MCU/MPU/DSP Kionix . 321 Fairchild . 534 . , 535, 536, 537, 538 Atmel . 197, 198, 199, 200, 201, 202 Maxim . 322 . , 323, 324, 325, 326, 327, 328, 329, Genesic . 539. , 540 Blackhawk . 203 . 330, 331, 332, 333, 334, 335, 336, 337, Infineon . 541, 542 Cypress . 204 . , 205, 206, 207 . 338, 339, 340, 341, 342, 343, 380, 381 IXYS . 543. Energy Micro . 208 Microchip . 344, 345, 346, 347 MA-COM . 544 . Elprotronic . 209 National . 348 . , 349, 350, 351, 352, 353 MCC . 545. FDI . 210 . NXP . 354. , 355, 356, 357, 358, 359 NXP . .546 . , 547 Freescale . 211, 212, 213, 214, 215, 216, 217, ON Semiconductor . .360, 361, 362 ON Semiconductor . 548, 549, 550, 551 . 218, 219, 220, 221, 222, 223, 224 Pericom . 363. , 364 Panasonic Semiconductor . .552 . , 553, 554 IAR Systems . .Available . at mouser.com PLX Technology . .365 . , 366 Power Integrations . 555 Keil . 225 ROHM Semiconductor . 367, 368 Rectron . 556 Code Red . 226. Silicon Labs . 369 . , 370 ROHM Semiconductor . 557 Embedded Artists . 226 . SMSC . 371 . STMicroelectronics . .558, 559, 560 Microchip . 227, 228, 229, 230, 231, 232 STMicroelectronics . 372, 373, 374, 375, 376 Toshiba . 561 NXP . 233 . , 234, 235 Supertex . .377 . , 378, 379 Vishay General Semiconductor .562, 563, 564, 565 Parallax . 236 Texas Instruments . 382, 383, 384, 385, 386, 387, Vishay Semiconductor . 566, 567, 568, 569, 570, 571 Signum Systems . Available at mouser.com . 388, 389, 390, 391, 392, 393, 394, 395, 396 Transistors Silicon Labs . .237 . , 238, 239, 240, 241, 242 THAT Corporation . 397 . Renesas/CEL . 572. , 573 STMicroelectronics . .243, 244, 245 Vishay/Siliconix . .398, 399, 400 Central . .574, 575 Spectrum Digital . -

Microscope Innovation Issue Fall 2020

Masks • COVID-19 Testing • PAPR Fall 2020 CHIhealth.com The Innovation Issue “Armor” invention protects test providers 3D printing boosts PPE supplies CHI Health Physician Journal WHAT’S INSIDE Vol. 4, Issue 1 – Fall 2020 microscope is a journal published by CHI Health Marketing and Communications. Content from the journal may be found at CHIhealth.com/microscope. SUPPORTING COMMUNITIES Marketing and Communications Tina Ames Division Vice President Making High-Quality Masks 2 for the Masses Public Relations Mary Williams CHI Health took a proactive approach to protecting the community by Division Director creating and handing out thousands of reusable facemasks which were tested to ensure they were just as effective after being washed. Editorial Team Sonja Carberry Editor TACKLING CHALLENGES Julie Lingbloom Graphic Designer 3D Printing Team Helps Keep Taylor Barth Writer/Associate Editor 4 PAPRs in Use Jami Crawford Writer/Associate Editor When parts of Powered Air Purifying Respirators (PAPRS) were breaking, Anissa Paitz and reordering proved nearly impossible, a team of creators stepped in with a Writer/Associate Editor workable prototype that could be easily produced. Photography SHARING RESOURCES Andrew Jackson Grassroots Effort Helps Shield 6 Nebraska from COVID-19 About CHI Health When community group PPE for NE decided to make face shields for health care providers, CHI Health supplied 12,000 PVC sheets for shields and CHI Health is a regional health network headquartered in Omaha, Nebraska. The 119 kg of filament to support their efforts. combined organization consists of 14 hospitals, two stand-alone behavioral health facilities, more than 150 employed physician ADVANCING CAPABILITIES practice locations and more than 12,000 employees in Nebraska and southwestern Iowa. -

Resistors, Diodes, Transistors, and the Semiconductor Value of a Resistor

Resistors, Diodes, Transistors, and the Semiconductor Value of a Resistor Most resistors look like the following: A Four-Band Resistor As you can see, there are four color-coded bands on the resistor. The value of the resistor is encoded into them. We will follow the procedure below to decode this value. • When determining the value of a resistor, orient it so the gold or silver band is on the right, as shown above. • You can now decode what resistance value the above resistor has by using the table on the following page. • We start on the left with the first band, which is BLUE in this case. So the first digit of the resistor value is 6 as indicated in the table. • Then we move to the next band to the right, which is GREEN in this case. So the second digit of the resistor value is 5 as indicated in the table. • The next band to the right, the third one, is RED. This is the multiplier of the resistor value, which is 100 as indicated in the table. • Finally, the last band on the right is the GOLD band. This is the tolerance of the resistor value, which is 5%. The fourth band always indicates the tolerance of the resistor. • We now put the first digit and the second digit next to each other to create a value. In this case, it’s 65. 6 next to 5 is 65. • Then we multiply that by the multiplier, which is 100. 65 x 100 = 6,500. • And the last band tells us that there is a 5% tolerance on the total of 6500. -

Semiconductor Science for Clean Energy Technologies

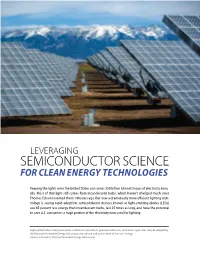

LEVERAGING SEMICONDUCTOR SCIENCE FOR CLEAN ENERGY TECHNOLOGIES Keeping the lights on in the United States consumes 350 billion kilowatt hours of electricity annu- ally. Most of that light still comes from incandescent bulbs, which haven’t changed much since Thomas Edison invented them 140 years ago. But now a dramatically more efficient lighting tech- nology is seeing rapid adoption: semiconductor devices known as light-emitting diodes (LEDs) use 85 percent less energy than incandescent bulbs, last 25 times as long, and have the potential to save U.S. consumers a huge portion of the electricity now used for lighting. High-performance solar power plant in Alamosa, Colorado. It generates electricity with multi-layer solar cells, developed by the National Renewable Energy Laboratory, that absorb and utilize more of the sun’s energy. (Dennis Schroeder / National Renewable Energy Laboratory) How we generate electricity is also changing. The costs of to produce an electrical current. The challenge has been solar cells that convert light from the sun into electricity to improve the efficiency with which solar cells convert have come down dramatically over the past decade. As a sunlight to electricity and to reduce their cost for commer- result, solar power installations have grown rapidly, and cial applications. Initially, solar cell production techniques in 2016 accounted for a significant share of all the new borrowed heavily from the semiconductor industry. Silicon electrical generating capacity installed in the U.S. This solar cells are built on wafers cut from ingots of crystal- grid-scale power market is dominated by silicon solar cells, line silicon, just as are the chips that drive computers.