Urban Transport Energy Use in the APEC Region: Trends and Options

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Beijing Guide Beijing Guide Beijing Guide

BEIJING GUIDE BEIJING GUIDE BEIJING GUIDE Beijing is one of the most magnificent cities in Essential Information Money 4 Asia. Its history is truly impressive. The me- tropolis is dynamically evolving at a pace that Communication 5 is impossible for any European or North Amer- ican city. Holidays 6 As is quite obvious from a glance at Tianan- men, the literal center of the city, Beijing is Transportation 7 the seat of communist political power, with its vast public spaces, huge buildings designed ac- Food 11 cording to socialist realism principles and CCTV systems accompanied by ever-present police Events During The Year 12 forces. At the same time, this might be seen Things to do 13 as a mere continuity of a once very powerful empire, still represented by the unbelievable DOs and DO NOTs 14 Forbidden City. With Beijing developing so fast, it might be Activities 17 difficult to look beyond the huge construction sites and modern skyscrapers to re-discover . the peaceful temples, lively hutong streets and beautiful parks built according to ancient prin- ciples. But you will be rewarded for your ef- Emergency Contacts forts – this side of Beijing is relaxed, friendly and endlessly charming. Medical emergencies: 120 Foreigners Section of the Beijing Public Se- Time Zone curity Bureau: +86 10 6525 5486 CST – China Standard Time (UTC/GMT +8 hours), Police: 110 no daylight saving time. Police (foreigner section): 552 729 Fire: 119 Contacts Tourist Contacts Traffic information: 122 Tourist information: +86 10 6513 0828 Beijing China Travel Service: +86 10 6515 8264 International Medical Center hotline: +86 10 6465 1561 2 3 MONEY COMMUNICATION Currency: Renminbi (RMB). -

Park Mckinley West

PARK MCKINLEY WEST www.PreSelling.com.ph FOR INTERNAL USE ONLY FOR INTERNAL USE ONLY THE PHILIPPINES Strong Macroeconomic Fundamentals are vital to the investors and end-users www.PreSelling.com.ph FOR INTERNAL USE ONLY THE PHILIPPINES 2,186,091 105M 150.6 3.5 (in thousand 2,240 USD) (in thousands) Philippine Consumer Inflation Rate OFW OFW Workers Population Price Index as as of Oct. 2017 Remittances as of 2016 of Nov. 2017 As of Sept 2017 Top 5 Visitor COUNTRY NO. OF ARRIVALS Arrivals as of Korea 686,630 January to www.PreSelling.com.phUnited States 428,767 May 2017 China 388,896 Japan 255,819 Total: Australia 112,814 2,882,737 14.43% growth rate FOR INTERNAL USE ONLY THE PHILIPPINES Fitch Ratings for the Philippines BBB last December 10, 2017 (“stable” outlook) Updated Asian Development 6.8% Bank Growth Forecast (Fromwww.PreSelling.com.ph Asian Development Outlook 2017) FOR INTERNAL USE ONLY THE PHILIPPINES Comprehensive Tax Relaxation of foreign Amendments in Reform Package ownership restrictions existing laws in on retail and procurement and construction business www.PreSelling.com.ph Opportunities for Infrastructure projects development outside across the entire of Metro Manila country FOR INTERNAL USE ONLY THE PHILIPPINES Infrastructure led GDP to buoy the property sector The “Golden Age of Infrastructure” will support the decentralization project of the government. It would unlock land values outside of Metro Manila. The administration’s commitment to build crucial projects throughout the country would also be a big factor with regard to the strategies of real estate developers. -

West Japan Railway Group Integrated Report 2019 —Report on Our Value for Society—

Continuity Progress Making Our Vision into Reality West Japan Railway Group Integrated Report 2019 —Report on Our Value for Society— West Japan Railway Company Contents 2 On the publication of “JR-West Group Integrated Report 2019” 3 Values held by the JR-West Group Our Starting Point 5 The derailment accident on the Fukuchiyama Line 11 Recovering from heavy rain damage through cooperation and think-and-act initiatives 13 Business activities of JR-West Group 15 The president’s message 17 The value we seek to provide through the non-railway business —Messages from group company Presidents Strategy of 21 Steps toward our vision 21 JR-West Group Medium-Term Management Plan 2022: approach & overview Value Creation 23 Toward long-term sustainable growth for Our Vision 25 Progress on Groupwide strategies—example initiatives 27 Promoting our technology vision 29 Special Three-Way Discussion The challenge of evolving in the railway/transportation field in an era of innovation 33 Fiscal 2019 performance in priority CSR fields and fiscal 2020 plans for priority initiatives 37 Safety 47 Customer satisfaction 51 Coexistence with communities A Foundation 55 Human resources/motivation Supporting 59 Human rights Value Creation 61 Global environment 67 Risk management 71 Corporate governance 73 Special Three-Way Discussion The role of the Board of Directors in achieving sustainable growth and enhancing corporate value 77 Initiatives in each business 81 Consolidated 10-year financial summary Data 83 Financial statements 87 Recognizing and responding to risks and opportunities 88 Data related to human resources and motivation (non-consolidated) Corporate profile (as of March 31, 2019) Scope As a rule, JR-West Group (including some Company name West Japan Railway Company initiatives at the non-consolidated level). -

Malaysia Berhad (Plus)

SUSTAINABILITY REPORT 2020 BREAKING THROUGH DISRUPTION TABLE OF CONTENTS ABOUT THIS REPORT 1 FROM OUR LEADERS 2 WE ARE PLUS 14 RISING TOGETHER - BRAVING THE 36 COVID-19 FIGHT OUR SUSTAINABILITY JOURNEY 48 OUR ENVIRONMENTAL STEWARDSHIP 60 OUR COMMITMENT TO SOCIETY 78 OUR STRENGTH OF OUR GOVERNANCE 116 OUR JOURNEY OF ACHIEVEMENTS 136 GRI CONTENT INDEX 147 MOVING FORWARD 149 COVER RATIONALE The cover for our inaugural voluntary Sustainability Report, themed ‘Breaking Through Disruption’, reflects our success in connecting people and communities, as well as providing a safe and comfortable journey to our customers despite the challenges faced in 2020. Furthermore, it underscores the vital role we play in Nation-building as we strive to deliver sustainable value not only for our business, but also for society and the environment as a whole. Set against the backdrop of over 1,130km of highways we manage in Peninsular Malaysia, the cover of this Sustainability Report visualises our purpose of Taking Good Care of You, Every Step of the Way. ABOUT THIS REPORT This is PLUS Malaysia Berhad’s (PLUS) inaugural Sustainability Report following the formalisation of our sustainability agenda and aspirations in 2020. In this Report, we disclose our approach to sustainability, the governance functions we have put in place, the matters identified as material to our business and our stakeholders, as well as the efforts we have taken to address those matters. This Report provides our stakeholders with a balanced and fair view on the value we created across the Environmental, Social and Governance (ESG) spectrum. It also steers us towards ingraining best practices in all aspects of our business to ensure its sustainability, as well as that of our stakeholders and the environment, as we aspire to lead by example as the Nation’s leading highway operator and a Government-Linked Company (GLC). -

Essentials for Living in Osaka (English)

~Guidebook for Foreign Residents~ Essentials for Living in Osaka (English) Osaka Foundation of International Exchange October 2018 Revised Edition Essentials for Living in Osaka Table of Contents Index by Category ⅠEmergency Measures ・・・1 1. Emergency Telephone Numbers 2. In Case of Emergency (Fire, Sudden Sickness and Crime) Fire; Sudden Illness & Injury etc.; Crime Victim, Phoning for Assistance; Body Parts 3. Precautions against Natural Disasters Typhoons, Earthquakes, Collecting Information on Natural Disasters; Evacuation Areas ⅡHealth and Medical Care ・・・8 1. Medical Care (Use of medical institutions) Medical Care in Japan; Medical Institutions; Hospital Admission; Hospitals with Foreign Language Speaking Staff; Injury or Sickness at Night or during Holidays 2. Medical Insurance (National Health Insurance, Nursing Care Insurance and others) Medical Insurance in Japan; National Health Insurance; Latter-Stage Elderly Healthcare Insurance System; Nursing Care Insurance (Kaigo Hoken) 3. Health Management Public Health Center (Hokenjo); Municipal Medical Health Center (Medical Care and Health) Ⅲ Daily Life and Housing ・・・16 1. Looking for Housing Applying for Prefectural Housing; Other Public Housing; Looking for Private Housing 2. Moving Out and Leaving Japan Procedures at Your Old Residence Before Moving; After Moving into a New Residence; When You Leave Japan 3. Water Service Application; Water Rates; Points of Concern in Winter 4. Electricity Electricity in Japan; Application for Electrical Service; Payment; Notice of the Amount of Electricity Used 5. Gas Types of Gas; Gas Leakage; Gas Usage Notice and Payment Receipt 6. Garbage Garbage Disposal; How to Dispose of Other Types of Garbage 7. Daily Life Manners for Living in Japan; Consumer Affairs 8. When You Face Problems in Life Ⅳ Residency Management System・Basic Resident Registration System for Foreign Nationals・Marriage・Divorce ・・・27 1. -

Mining Temporal Mobility Patterns in London, Singapore and Beijing Using Smart-Card Data

Research Collection Journal Article Variability in Regularity: Mining Temporal Mobility Patterns in London, Singapore and Beijing Using Smart-Card Data Author(s): Zhong, Chen; Batty, Michael; Manley, Ed; Wang, Jiaqiu; Wang, Zijia; Chen, Feng; Schmitt, Gerhard Publication Date: 2016-02-12 Permanent Link: https://doi.org/10.3929/ethz-b-000114229 Originally published in: PLoS ONE 11(2), http://doi.org/10.1371/journal.pone.0149222 Rights / License: Creative Commons Attribution 4.0 International This page was generated automatically upon download from the ETH Zurich Research Collection. For more information please consult the Terms of use. ETH Library RESEARCH ARTICLE Variability in Regularity: Mining Temporal Mobility Patterns in London, Singapore and Beijing Using Smart-Card Data Chen Zhong1*, Michael Batty1, Ed Manley1, Jiaqiu Wang1, Zijia Wang2,3, Feng Chen2,3, Gerhard Schmitt4 1 Centre for Advanced Spatial Analysis, University College London, London, United Kingdom, 2 School of Civil and Architectural Engineering, Beijing Jiaotong University, No.3 Shangyuancun, Haidian District, Beijing, P. R. China, 3 Beijing Engineering and Technology Research Centre of Rail Transit Line Safety and Disaster Prevention, No.3 Shangyuancun, Haidian District, Beijing, P. R. China, 4 Future Cities Laboratory, Department of Architecture, ETH Zurich, Zurich, Switzerland * [email protected] Abstract OPEN ACCESS To discover regularities in human mobility is of fundamental importance to our understand- Citation: Zhong C, Batty M, Manley E, Wang J, ing of urban dynamics, and essential to city and transport planning, urban management and Wang Z, Chen F, et al. (2016) Variability in Regularity: policymaking. Previous research has revealed universal regularities at mainly aggregated Mining Temporal Mobility Patterns in London, spatio-temporal scales but when we zoom into finer scales, considerable heterogeneity and Singapore and Beijing Using Smart-Card Data. -

NFC-Enabled Attack on Cyber Physical Systems: a Practical Case Study

NFC-enabled Attack on Cyber Physical Systems: A Practical Case Study Fan Dang1, Pengfei Zhou1;2, Zhenhua Li1, Yunhao Liu1 1 School of Software, TNLIST, and KLISS MoE, Tsinghua University, China 2 Beijing Feifanshi Technology Co., Ltd., China [email protected], fzhoupf05, lizhenhua1983, [email protected] Abstract—Automated fare collection (AFC) systems have been widely applied to practical transportation due to their conve- nience. Although there are many potential threats of NFC such AFC Card POS Terminal as eavesdropping, data modification, and relay attacks, NFC based AFC systems are considered secure, due to the limited 10cm communication distance. Nevertheless, the proliferation of NFC-equipped mobile phones make such system venerable. We (a) Direct communication. introduce and implement an attack on AFC cards that permits an attacker to top up his smart card and get a refund. We also propose possible countermeasures to defend against these attacks. I. INTRODUCTION AFC Card Card Reader Laptop Phone POS Terminal Automated Fare Collection (AFC) systems have been widely applied for decades to automate manual ticketing. They Relay Devices are deployed in major cities all over the world, with billions of (b) Relayed communication. contactless smart cards issued. Such a card is able to store and process data, and transceive data with a terminal wirelessly. Fig. 1: Two practical paradigms of AFC communications. Thus it is commonly used as an electronic ticket in AFC systems. The MIFARE chip was developed as a solution for AFC, method allows any Android application to emulate a card and it was seen as the major candidate for AFC systems and communicate directly to a card reader. -

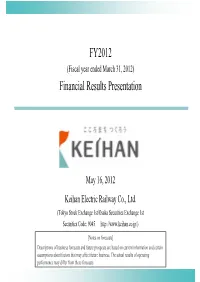

FY2012 Financial Results Presentation(361KB)

FY2012 (Fiscal year ended March 31, 2012) Financial Results Presentation May 16, 2012 Keihan Electric Railway Co., Ltd. (Tokyo Stock Exchange 1st/Osaka Securities Exchange 1st Securities Code: 9045 http://www.keihan.co.jp/) [Notes on forecasts] Descriptions of business forecasts and future prospects are based on current information and certain assumptions about factors that may affect future business. The actual results of operating performance may differ from these forecasts. Overview of FY2012 Financial Results Consolidated Statements of Income (Millions of yen) 2011/11 FY2011 FY2012 Change Main factors of changes Estimate Transportation -2,746, Real estate +4,640, Retail +1,576, Operating revenue 259,511 265,629 6,118 260,600 (2.4%) Leisure and service +2,289, Others -12 Transportation -26, Real estate +1,365, Retail +315, Operating income 16,269 18,160 1,891 15,400 (11.6%) Leisure and service +44, Others +71 Non-operating income -130 (Dividends income -24, Amortization of negative goodwill -116) Ordinary income 11,846 13,580 1,734 10,500 (14.6%) Non-operating expenses +27 (Interest expenses -193, Miscellaneous expenses +168) Extraordinary income -479 (Gain on sales of fixed assets -265, Net income 6,478 7,005 526 Compensation income for expropriation -157) 6,500 (8.1%) Extraordinary loss +88 (Impairment loss +1,222, Loss on revision of retirement benefit plan -1,074) ROA 2.7% 2.9% 0.2pt ROA: Operating income to total assets - ROE 4.9% 5.1% 0.2pt ROE: Net income to shareholders' equity - 2,284 EBITDA 33,985 36,269 EBITDA: Operating income +depreciation 33,600 (6.7%) Depreciation 17,715 18,109 393 18,200 (2.2%) Capital 2,705 29,781 32,487 33,800 expenditures (9.1%) [Changes in scope of consolidation and application of the equity method (from the previous fiscal year end)] Consolidated subsidiaries: 36 companies (No change): New: 3 companies KB Enterprise Co., Ltd. -

China Everbright Limited and Yantai Municipal Government

China Everbright Limited and Yantai Municipal Government Sign Strategic Cooperation Agreement 14 December 2015 - China Everbright Limited ("CEL", stock code: 165.HK) and the Yantai Municipal Government signed a strategic cooperation agreement on 6 December 2015 to support economic and social development in the industrial and port city of Yantai in Shandong Province, China. The agreement not only establishes a partnership between CEL and the city of Yantai, but also lays a solid foundation for the strategic planning and rapid, sustainable development of China Everbright eTransport. The signing ceremony was held at the Yantai Orient Haitian Hotel. In attendance were Yin Lianchen, Chief Investment Officer of CEL; Liu Yumeng, Managing Director of China Everbright eTransport Investment Company Limited, Wang Zhong, Member of the Yantai Municipal Standing Committee and Deputy Mayor of Yantai; Li Yongmei, Deputy Secretary-General of the Yantai Municipal Government; Liu Fusheng, Director of the Yantai Municipal Commission of Economy and Informatisation; and members of the media. Yin Lianchen and Wang Zhong delivered speeches during the ceremony and signed the strategic cooperation agreement on behalf of CEL and the Yantai Municipal Government. Liu Yumeng and Cao Jingdai, Director of the Yantai-Citizen Card, also signed an investment framework agreement on behalf of their respective parties. The signing ceremony ended on a convivial note. The agreements provide for joint investment and development opportunities in industry, infrastructure, environment, urbanisation, social enterprises and public services in the city of Yantai. This includes the Yikatong public transport smart card pilot scheme currently being promoted by the Ministry of Transport, which will be used across Yantai’s port, aviation, rail and road systems. -

Metro Manila Market Update Q4 2018

RESEARCH METRO MANILA MARKET UPDATE Q4 2018 METRO MANILA REAL ESTATE SECTOR REVIEW FDI RISES AS NEIGHBORING COUNTRIES CONTINUE TO BET ON “ASIA’S RISING TIGER” COVER | The Philippines remains a popular investment destination for Asian investors FIGURE 1 Net Foreign Direct Investment Level By Country of Origin (in USD Mn) 905.65 SNAPSHOTS 900 750 2017 2018 Economic Indicators 600 450 384.25 263.97 300 189.33 183.51 64.4 150 13.25 8.56 6.1% 0 GDP SINGAPORE HONGKONG CHINA JAPAN Q4 2018 Source: Bangko Sentral ng Pilipinas The Philippines continues to attract Foreign Direct Investments (FDI) as formulates policies that will limit the economy carries on constraints in doing business in the experiencing growth of above 6% 6.1% country. On October 2018, the 11th Inflation Rate for the past 7 consecutive years. Regular Foreign Investment December 2018 The growth was mainly brought Negative List was amended to about by the increase in include five areas that will allow government spending from the 100% foreign investment present administration’s “Build, participation. The list includes Build, Build” infrastructure program. internet businesses (as excluded from mass media), teaching at 3.1% At the end of 2017, the Philippines higher education levels provided the OFW Remittances posted the highest rise in Foreign subject being taught is not a November 2018 Direct Investments (FDI) among professional subject (i.e., included in a government board or bar ASEAN countries. FDI remains examination), training centers that robust as investments increased by are engaged in short-term high- 42% in the first half of 2018. -

Railway Transport Planning and Implementation in Metropolitan Manila, 1879 to 2014

Journal of the Eastern Asia Society for Transportation Studies, Vol.12, 2017 Railway Transport Planning and Implementation in Metropolitan Manila, 1879 to 2014 Jose Regin F. REGIDOR a, Dominic S. ALOC b a,b Institute of Civil Engineering, College of Engineering, University of the Philippines, Diliman, Quezon City, 1101, Philippines a E-mail: [email protected] b E-mail: [email protected] Abstract: This paper presents a history of rail-based transportation in Metropolitan Manila. This history focuses on urban transport including rail-based streetcars or trams that started operations in the 1880’s but were destroyed during the Second World War and never to be revived. Several plans are discussed. Among these plans are proposals for a monorail network, a heavy rail system, and the more current rail transit plans from recent studies like MMUTIS. An assessment of public transportation in Metro Manila is presented with emphasis on the counterfactual scenario of what could have been a very different metropolis if people could commute using an extensive rail transit system compared to what has been realized so far for the metropolis. Recommendations for the way forward for rail transportation in Metro Manila and further studies are stated in conclusion. Keywords: Transport Planning, Rail Transit, History 1. INTRODUCTION 1.1 Background Rail-based urban transport has had a relatively long history in Metro Manila despite what now seems to be a backlog of rail transportation in the capital city of the Philippines. In fact, the dominant mode of public transportation used to be rail-based with Manila and its adjoining areas served by a network of electric tranvias (i.e., streetcars) and heavy rail lines. -

The Mobility Opportunity Improving Public Transport to Drive Economic Growth

The Mobility Opportunity Improving public transport to drive economic growth. A research project commissioned by Siemens AG Contents 1. Executive summary 5 Why transport matters 5 A unique study 5 Key findings 6 Pointers for investment strategies 7 2. How the study was conducted 9 Scope of study 9 The true cost of transport 9 High-level approach 10 Economic audit 10 3. The economic opportunity 11 Cost and the size of the prize today 11 How cost and opportunity will change by 2030 13 4. How cities compare 17 Well-established cities 17 High density compact centres 17 Emerging cities 19 5. Pointers for investment strategies 21 The scale of the opportunity should dictate the level of investment 21 Using technology to improve quality may be the best route to economic uplift 24 Urban rail networks are a key way for larger cities to meet capacity demand 25 Integrated governance is crucial in planning and operating an efficient network 27 Appendix 1: Selected investment cases 29 Appendix 2: City profiles 35 Appendix 3: Methodology 71 Overview of approach 71 Key principles 72 Appendix 4: Technical audit 75 3 “Efficient transport can attract economic activity to cities, and boost productivity by improving connectivity and reducing time lost to travel” 4 1. Executive Summary Why transport matters cities face a need to upgrade and supplement existing infrastructure to meet modern requirements. Transport plays a key role in economic growth Cities account for around 80% of the world’s economic In other cities, such as Tokyo and Seoul, relatively recent output, and drive an even higher share of global growth.