Jefferson Parish Council

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

With Leadership from Iftikhar Ahmad, Armstrong International Growing By

Vol. 24, No. 6 Kenner’s Community Newspaper Since 1991 JUNE 2015 Kenner traffic With leadership from Iftikhar Ahmad, Armstrong International growing concerns being by leaps and bounds addressed as design By Allan Katz work begins on new Armstrong New Orleans International Airport is Louisiana’s largest airport processing over 80.3 per- airport access road cent of all passengers traveling into the state. The air- port is also the region’s largest asset having a $5.3 bil- An ordinance spelling out the details of a lion economic impact on the regional economy in 2013 “Memorandum of Understanding” between Kenner as found in a recent economic study by economist Dr. and the New Orleans Aviation Board, in advance of a Timothy Ryan. In the five years since Iftikhar Ahmad $7 million project to build a new, four-lane airport ac- was named to the top job at Louis Armstrong New Or- cess road and make other traffic improvements, was leans International Airport, the Kenner-based facility introduced at the Kenner City Council meeting held has shown an incredible growth spurt. Still to come is on April 23, 2015. a new $650 million North Terminal with construction The new access road is needed because con- slated to begin later this year. struction is expected to begin this summer on a Armstrong International was serving 7.7 million $650 million project to build a new North Terminal passengers in 2009. In 2010, Ahmad’s first year at the at Louis Armstrong New Orleans International Air- helm of the airport, the passenger count jumped to port with two concourses and 30 gates along with a $8.2 million. -

2019 Annual Budget, General Fund Revenues Are Estimated at $98.2 Million

JEFFERSON PARISH, LOUISIANA 2019 PROPOSED BUDGET JEFFERSON PARISH OFFICIALS Jefferson Parish President Michael S. Yenni MEMBERS, JEFFERSON PARISH COUNCIL Christopher L. Roberts Councilman-at-Large, Division A Council Chairman Cynthia Lee-Sheng Ricky J. Templet Councilwoman-at-Large, Division B Councilman, 1st District Paul D. Johnston Mark D. Spears, Jr. Councilman, 2nd District Councilman, 3rd District Dominick F. Impastato, III Jennifer Van Vrancken Councilman, 4th District Councilwoman, 5th District Government Finance Officers Association of the United States and Canada (GFOA) presented a Distinguishing Budget Presentation Award to Jefferson Parish, Louisiana for its Annual Budget for the fiscal year beginning January 1, 2018. In order to receive this award, a governmental unit must publish a budget document that meets program criteria as a policy document, as a financial plan, as an operations guide, and as a communications device. This award is valid for a period of one year only. We believe our current budget continues to conform to program requirements, and we are submitting it to GFOA to determine its eligibility for another award. 2019 Jefferson Parish Annual Budget i Table of Contents by Function Description Page Description Page Budget Award i Public Safety (Cont.) Table of Contents ii Board of Zoning Adjustments 115 Transmittal Letter 1 Inspection & Code Enforcement 117 Administrative Adjudication 119 Parish Profile Bureau of Administrative Adjudication 121 Parish Profile 5 Dept of Property Maint Zoning/Quality of Life 122 -

Carrier Locator: Interstate Service Providers

Carrier Locator: Interstate Service Providers November 1997 Jim Lande Katie Rangos Industry Analysis Division Common Carrier Bureau Federal Communications Commission Washington, DC 20554 This report is available for reference in the Common Carrier Bureau's Public Reference Room, 2000 M Street, N.W. Washington DC, Room 575. Copies may be purchased by calling International Transcription Service, Inc. at (202) 857-3800. The report can also be downloaded [file name LOCAT-97.ZIP] from the FCC-State Link internet site at http://www.fcc.gov/ccb/stats on the World Wide Web. The report can also be downloaded from the FCC-State Link computer bulletin board system at (202) 418-0241. Carrier Locator: Interstate Service Providers Contents Introduction 1 Table 1: Number of Carriers Filing 1997 TRS Fund Worksheets 7 by Type of Carrier and Type of Revenue Table 2: Telecommunications Common Carriers: 9 Carriers that filed a 1997 TRS Fund Worksheet or a September 1997 Universal Service Worksheet, with address and customer contact number Table 3: Telecommunications Common Carriers: 65 Listing of carriers sorted by carrier type, showing types of revenue reported for 1996 Competitive Access Providers (CAPs) and 65 Competitive Local Exchange Carriers (CLECs) Cellular and Personal Communications Services (PCS) 68 Carriers Interexchange Carriers (IXCs) 83 Local Exchange Carriers (LECs) 86 Paging and Other Mobile Service Carriers 111 Operator Service Providers (OSPs) 118 Other Toll Service Providers 119 Pay Telephone Providers 120 Pre-paid Calling Card Providers 129 Toll Resellers 130 Table 4: Carriers that are not expected to file in the 137 future using the same TRS ID because of merger, reorganization, name change, or leaving the business Table 5: Carriers that filed a 1995 or 1996 TRS Fund worksheet 141 and that are unaccounted for in 1997 i Introduction This report lists 3,832 companies that provided interstate telecommunications service as of June 30, 1997. -

Final Staff Report

CITY PLANNING COMMISSION CITY OF NEW ORLEANS MITCHELL J. LANDRIEU ROBERT D. RIVERS MAYOR EXECUTIVE DIRECTOR LESLIE T. ALLEY DEPUTY DIRECTOR City Planning Commission Staff Report Executive Summary Summary of Uptown and Carrollton Local Historic District Proposals: The Historic Preservation Study Committee Report of April 2016, recommended the creation of the Uptown Local Historic District with boundaries to include the area generally bounded by the Mississippi River, Lowerline Street, South Claiborne Avenue and Louisiana Avenue, and the creation of the Carrollton Local Historic District with boundaries to include the area generally bounded by Lowerline Street, the Mississippi River, the Jefferson Parish line, Earhart Boulevard, Vendome Place, Nashville Avenue and South Claiborne Avenue. These partial control districts would give the Historic District Landmarks Commission (HDLC) jurisdiction over demolition. Additionally, it would give the HDLC full control jurisdiction over all architectural elements visible from the public right-of-way for properties along Saint Charles Avenue between Jena Street and South Carrollton Avenue, and over properties along South Carrollton Avenue between the Mississippi River and Earhart Boulevard. Recommendation: The City Planning Commission staff recommends approval of the Carrollton and Uptown Local Historic Districts as proposed by the Study Committee. Consideration of the Study Committee Report: City Planning Commission Public Hearing: The CPC holds a public hearing at which the report and recommendation of the Study Committee are presented and the public is afforded an opportunity to consider them and comment. City Planning Commission’s recommendations to the City Council: Within 60 days after the public hearing, the City Planning Commission will consider the staff report and make recommendations to the Council. -

The Jefferson Parish Comprehensive Plan

This document is designed to be printed double-sided. This is the back of the cover and is intentionally blank. Contents 1. INTRODUCTION .................................................................... 1 2. WHO WE ARE ....................................................................... 5 3. WHAT WE SAID.................................................................. 11 4. OUR VISION ....................................................................... 13 5. LAND USE ......................................................................... 19 6. HOUSING ........................................................................... 39 7. TRANSPORTATION ............................................................ 47 8. COMMUNITY FACILITIES & OPEN SPACE .......................... 57 9. NATURAL HAZARDS & RESOURCES ................................. 71 10. ECONOMIC DEVELOPMENT ............................................ 79 11. ADMINISTRATION & IMPLEMENTATION ......................... 83 APPENDICES A: COMMUNITY PROFILE B: OPPORTUNITIES & CONSTRAINTS C: IMPLEMENTATION PROGRESS SINCE 2003 D: UPDATE PROCESS Envision Jefferson 2040 Page i As adopted on November 6, 2019 Prepared by: Under the guidance of the Comprehensive Plan Administration of Update Steering Committee appointed by the Parish Michael S. Yenni, Parish President President and Councilmembers Walter R. Brooks, Chief Operating Officer Bruce Layburn Michael J. Power, Esq., Chief Administrative Bruce Richards Assistant, Development Lloyd Tran Jefferson Parish Planning Department -

Greater New Orleans New Greater

Greater New Orleans Greater New Orleans Urban Water Plan Urban Water Urban Water Plan A Comprehensive, Integrated & Sustainable Water Management Strategy St. Bernard Parish and the east banks of Jefferson and Orleans Parishes Implementation Implementation Greater New Orleans Inc. State of Louisiana Office of Community Development U.S. Department of Housing & Urban Development Waggonner & Ball Architects September 2013 Greater New Orleans Urban Water Plan Implementation Waggonner & Ball Architects September 2013 4 Greater New Orleans always has been surrounded by water and has thrived for nearly 300 years. Today the region faces new challenges, both outside the levee walls from rising seas and inside from land subsidence and regular flooding. A new approach to water - the region’s most abundant natural asset - is the foundation for building a safe and sustainable future on the Mississippi River delta. Greater New Orleans Urban Water Plan 5 Waggonner & Ball Architects AUTHOR Maria Papacharalambous Waggonner & Ball Architects CONTRIBUTING AUTHORS Mark S. Davis Tulane Institute on Water Resources Law and Policy William Marshall Waggonner & Ball Architects Prisca Weems FutureProof Rebecca Rothenberg GCR Inc. CONTRIBUTING TEAM Jenna Anger FutureProof Harry Vorhoff Tulane Institute on Water Resources Law and Policy Frederic Augonnet Tulane Institute on Water Resources Law and Policy Rafael Rabalais (formerly GCR) Tyler Antrup GCR Inc. Aron Chang Waggonner & Ball Architects Ramiro Diaz Waggonner & Ball Architects 6 Background Greater New Orleans Urban Water Plan In 2010, the State of Louisiana’s Office of Community Development - Disaster Recovery Unit funded Greater New Orleans, Inc. (GNO, Inc.) to develop a Comprehensive, Integrated and Sustainable Water Management Strategy for the east banks of Orleans and Jefferson Parishes and St. -

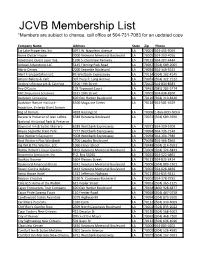

JCVB Membership List *Members Are Subject to Change, Call Office at 504-731-7083 for an Updated Copy

JCVB Membership List *Members are subject to change, call office at 504-731-7083 for an updated copy Company Name Address State Zip Phone 1st Lake Properties, Inc. 4971 W. Napoleon Avenue LA 70001 504-455-5059 Acme Oyster House 3000 Veterans Memorial Boulevard LA 70005 504-309-4056 Adventure Quest Laser Tag 1200 S. Clearview Parkway LA 70123 504-207-4444 Airboat Adventures LLC 5145 Fleming Park Road LA 70067 (504) 689-2005 Alario Center 2000 Segnette Boulevard LA 70094 504-349-5525 Alert Transportation LLC #3 Westbank Expressway LA 70114 (504) 362-4145 Amore Bakery & Cafe 307 Huey P. Long Avenue LA 70053 (504) 322-2122 Andrea's Restaurant & Catering 3100 19th Street LA 70002 504-834-8583 Any O'Cajun 103 Tapwood Court LA 70461 (985) 285-3774 ARC Document Solutions 3521 20th Street LA 70002 504-838-8300 Audubon Limousine 600 Oak Harbor Boulevard LA 70126 (504) 210-8340 Audubon Nature Institute - 6500 Magazine Street LA 70118 504-581-4629 Aquarium, Entergy Giant Screen Bag of Donuts 4828 Hastings St LA 70006 1-866-BOD-NOLA Barataria Preserve of Jean Lafitte 6588 Barataria Boulevard LA 70072 (504) 689-3690 National Historical Park & Preserve Baymont Inn & Suites Marrero 6589 Westbank Expressway LA 70072 504-309-5700 Bayou Segnette State Park 7777 Westbank Expressway LA 70094 504-736-7140 Best Western Bayou Inn 9008 Westbank Expressway LA 70094 504-304-7980 Best Western Plus Westbank 1700 Lapalco Boulevard LA 70058 504-366-5369 Big Wil & The Warden, LCC 1060 Elmer Street LA 70448 (504) 214-5591 Bobby Hebert's Cajun Cannon 4101 Veterans Memorial Boulevard LA 70001 (504) 324-6841 Bonomolo Limousine, Inc. -

Louisiana Freight Mobility Plan December 2015

Louisiana Freight Mobility Plan December 2015 prepared for prepared by Louisiana Freight Mobility Plan prepared for Louisiana Department of Transportation and Development prepared by CDM Smith Inc. December 2015 LOUISIANA FREIGHT MOBILITY PLAN Table of Contents 1. INTRODUCTION AND SUMMARY OF RECOMMENDATIONS .................................................................. 1-1 1.1 Summary of Investment Recommendations ............................................................................. 1-2 1.1.1 Capital Investments ...................................................................................................... 1-2 1.2 Summary of Policy and Program Recommendations ................................................................ 1-2 1.2.1 Policy recommendations .............................................................................................. 1-3 1.2.2 Program recommendations .......................................................................................... 1-3 2. STRATEGIC GOALS AND OBJECTIVES ...................................................................................................... 2-1 2.1 Federal Requirements ............................................................................................................... 2-1 2.2 Coordination with Relevant Plans ............................................................................................. 2-2 2.2.1 Statewide Transportation Plan ..................................................................................... 2-2 2.2.2 Other -

La Mare a Bore at Center Left

Geographies of New Orleans A 'Lake' in Broadmoor? Natural Paradise Once Graced Uptown's Last Open Tract Richard Campanella Contributing writer, GEOGRAPHIES OF NEW ORLEANS Published in the Times-Picayune/New Orleans Advocate, November 1, 2020, page A1 Conversations with older residents of the Broadmoor and Fontainebleau neighborhoods often prompt recollections of a “lake” in that vicinity prior to its urbanization. Indeed, a 1922 aerial photograph shows a large undeveloped tract—the last in the area—between Jefferson and Nashville avenues, going back from South Claiborne Avenue to Gert Town. Having subsided to a few feet below sea level, those open fields probably accumulated runoff after heavy rains, creating what looked like what many secondary sources describe as a “twelve-acre lake” in Broadmoor. But if we go back a century earlier, there turns out to be more to the story than a muddy field. Descriptive evidence comes from the pen of famed lawyer and narrative historian Charles Gayarré, who grew up on the plantation encompassing that low spot, and wrote of his memories in an 1886 Harper’s New Monthly Magazine article titled “A Louisiana Sugar Plantation of the Old Regime.” Gayarré was the grandson of Etienne de Boré, the man widely credited—thanks in part to Gayarré’s own dramatized recounting—with figuring out how to granulate locally grown sugarcane juice. That 1795 breakthrough led to a massive expansion of sugar cultivation in lower Louisiana, and of the institution of slavery on which it depended. De Bore’s plantation extended from the present-day 6000 to 6300 blocks of Tchoupitoulas Street straight back to what is now the intersection of Nashville Avenue and Earhart Expressway, an area that includes the aforementioned tract that was still undeveloped as of 1922. -

Deutsch, Kerrigan & Stiles Ellsworth Corp

Deutsch, Kerrigan & Stiles Ellsworth Corp. sponsored by Congratulations to our employees for making Walton Construction the Best Place to Work! WWW.WALTONBUILT.COM 504.733.2212 Quality of People Quality of Life McGlinchey Team Stafford Where Business and Law Intersect. 643 Magazine Street | New Orleans, LA 70130 | (504) 586-1200 | FAX (504) 596-2800 www.mcglinchey.com This is an advertisement. A Winning Place to Work Our 2,400 krewe members are the heart and soul of our business. Harrah’s is proud to be their Employer of Choice, providing them with competitive wages, quality benefits and a fun work environment. “I have been with Harrah’s for almost ten years and it has been a wonderful growth opportunity for me. Working here has enabled me to expand my career and my educational experiences. Now I am in a position to help other employees here to do the same. It is a wonderful feeling to be a part of the Harrah’s Family.” Shannon LaVigne Senior Training Specialist “As a first-time homeowner and single mother, Harrah’s Home Ownership Program made the difference for me being able to purchase a home for my family.” Shantrell Ringo Housekeeping Coordinator “Harrah’s offers a wide range of free courses on site, including computer training and finance, which I have taken advantage of to further my professional and personal development. They even have a college tuition reimbursement program.” Laurie Porter Food & Beverage Administrative Assistant At Harrah’s, we’re always looking for upbeat, energetic individuals to join our krewe. If you’d like to be part of our future success, apply online at www.harrahs.com or visit our employment office on the 9th floor of One Canal Place between 9am and 3pm, Tuesdays through Thursdays. -

New Orleans 2032 MTP.Pdf (1.140Mb)

Metropolitan Transportation Plan NewOrleans Urbanized Area F Y 2 0 3 2 Regional Planning Commission Jefferson, Orleans Plaquemines, St. Bernard and St.Tammany Parishes, Louisiana June 12, 2007 Metropolitan Transportation Plan New Orleans Urbanized Area Regional Planning Commission 1340 Poydras Street, Suite 2100 New Orleans, LA 70112 504-568-6611 504-568-6643 (fax) www: norpc.org [email protected] The preparation of this document was fi nanced in part through grants from the U.S. Department of Transportation, Federal Highway Administration in accordance with the Safe, Accountable, Flexible, Effi cient Transportation Equity Act - A Legacy for Users (SAFETEA-LU; P.L. 109-59). Contents Chapter 1 Introduction and Overview of the Planning Process Introduction--------------------------------------------------------------------------------------------- 2 Transportation Philosophy in SAFETEA-LU---------------------------------------------------------- 3 The Metropolitan Planning Organization----------------------------------------------------------- 4 Statutory Authority for Plan Development---------------------------------------------------------- 5 Hurricane Katrina--------------------------------------------------------------------------------------- 6 Metropolitan Transportation Plan-------------------------------------------------------------------- 8 Metropolitan Planning Process----------------------------------------------------------------------- 9 Safety Conscious Planning----------------------------------------------------------------------------- -

Flight Paths

NEW ORLEANS NOSTALGIA Remembering New Orleans History, Culture and Traditions By Ned Hémard Flight Paths Some New Orleans natives remember their airport on Airline Highway as Moisant Field. On July 11, 2001, it was renamed for Louis Armstrong in honor of the famous jazz musician’s centennial birthday (actually August 4, 1901). For years, everyone (including Louis, it seems) believed he was born on July 4, 1900. His baptismal certificate was finally located at Sacred Heart of Jesus Church on Canal Street after his death (revealing the correct date). Things are not always what they seem. For example, if you were to presume that Airline Highway was named because of the airport or airplanes, you would be wrong. It was built in the 1930s and 1940s to provide a direct route between Baton Rouge and New Orleans. Airline was once a synonym for a beeline, or a straight direct route. Governor Huey Long was said to have pushed for this route so he would have a shorter trip as he shuttled between the capital and New Orleans. Rather than running along the bending Mississippi River, Airline Highway runs in a relatively straight path. A portion of it has been renamed Airline Drive in an effort to clean up its history of no-tell motels (to which some in times past have made a beeline … including televangelist Jimmy “I have sinned!” Swaggart). “I have sinned!” A February 23, 1988, article in the Times-Picayune reported that a witness told interrogators that Swaggart “on several occasions visited the Texas Motel at 3520 Airline and the Travel Inn at 1131 Airline, where he could park his plush Lincoln Town Car in the rear.” Running roughly parallel to Airline Drive is the Earhart Expressway, an extension of Earhart Boulevard.