Market Report Summer / Fall 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Perspective on Medieval Perception of Norwegian Church Art 53

A perspective on Abstract This paper discusses the broad use of imitation techniques to give the impression of medieval perception of precious materials in Norwegian religious sacred art, with special attention to polychrome wooden objects Norwegian church art from the thirteenth century. The question of how ictive objects made out of wood, covered with chalk ground, metal foil and paint were accepted as key works of art in religious devotion is examined. What Kaja Kollandsrud the objects intended to emulate and how they could compete with precious objects will be discussed. Supporting evidence is ofered from the preserved sacred polychrome sculpture and panel paintings in Norway from the period. What makes an imitation successful is discussed in terms of the factors that contribute to the intended illusion. This is argued in relation to the attitudes towards display of such objects at the time they were installed within the church, which takes them out of the modern constraining concept of art and material value. Introduction he use of painterly materials and techniques to imitate precious metals, stone, pearls, gems, high status textiles and fur is characteristic for the painted objects from the early Middle Ages and throughout the thirteenth century in Norway as elsewhere in Europe. he Church in this period appears to have had no qualms about the emulation of such costly and precious items, as skilled imitation was common practice. In the modern attitude towards imitations, they are generally considered to be cheaper versions of the original. Although the word ‘imitation’ might suggest inferiority in our minds, these polychrome works served as iconic objects in the interiors of medieval churches.1 here were however limits to the substitution of rare and valuable materials with more readily available and cheaper materials. -

“Proud to Be Norwegian”

(Periodicals postage paid in Seattle, WA) TIME-DATED MATERIAL — DO NOT DELAY Travel In Your Neighborhood Norway’s most Contribute to beautiful stone Et skip er trygt i havnen, men det Amundsen’s Read more on page 9 er ikke det skip er bygget for. legacy – Ukjent Read more on page 13 Norwegian American Weekly Vol. 124 No. 4 February 1, 2013 Established May 17, 1889 • Formerly Western Viking and Nordisk Tidende $1.50 per copy News in brief Find more at blog.norway.com “Proud to be Norwegian” News Norway The Norwegian Government has decided to cancel all of commemorates Mayanmar’s debts to Norway, nearly NOK 3 billion, according the life of to Mayanmar’s own government. The so-called Paris Club of Norwegian creditor nations has agreed to reduce Mayanmar’s debts by master artist 50 per cent. Japan is cancelling Edvard Munch debts worth NOK 16.5 billion. Altogether NOK 33 billion of Mayanmar’s debts will be STAFF COMPILATION cancelled, according to an Norwegian American Weekly announcement by the country’s government. (Norway Post) On Jan. 23, HM King Harald and other prominent politicians Statistics and cultural leaders gathered at In 2012, the total river catch of Oslo City Hall to officially open salmon, sea trout and migratory the Munch 150 celebration. char amounted to 503 tons. This “Munch is one of our great is 57 tons, or 13 percent, more nation-builders. Along with author than in 2011. In addition, 91 tons Henrik Ibsen and composer Edvard of fish were caught and released. Grieg, Munch’s paintings lie at the The total catch consisted of core of our cultural foundation. -

Edu Immigration ACCEPTED.Pdf (882.2Kb)

ARTICLE Does education affect immigration attitudes? Evidence from an education reform / Henning Finseraas, Øyvind Søraas Skorge, Marte Strøm VERSION: POST PRINT/GREEN OPEN ACCESS This document is the author’s post print (final accepted version). The document is archived in the institutional archive of Institute for Social Research. The final publication is available in: Electoral Studies 2018, / DOI: 10.1016/j.electstud.2018.06.009 does education affect immigration attitudes? Evidence from an education reform∗ Henning Finseraas,y Øyvind Skorge,z and Marte Strømx Accepted for publication in Electoral Studies July 2, 2018 Abstract Empirical research consistently finds that people with high education have more liberal immigration attitudes. To what extent this relationship reflects a causal effect of education is, however, largely unknown. We rely on the staggered introduction of a major Norwegian education reform to get exogenous variation in respondents’ level of education. The reform lifted the bottom of the education distribution by increasing the compulsory years of education by two years. We find no significant differences in immigration attitudes between those who were educated in the old and the new education system. Our results suggest that if education has a causal effect on immigration attitudes, it is likely to operate on other education margins. ∗We would like to thank seminar participants at the Institute for Social Research, Frisch Center for Economic Research, and University of Bergen for comments on a previous draft of the paper. Funding from the Research Council of Norway is acknowledged (grant no. 270687). yInstitute for Social Research, Oslo, P.O. Box 3233 Elisenberg, 0208 Oslo, Norway. -

Ullensaker, Nannestad Og Eidsvoll Kommuner

FYLKESADMINISTRASJONEN Ullensaker kommune Postboks 470 2051 JESSHEIM Att. Atle Sander Vår saksbehandler Vår dato Vår referanse (oppgis ved svar) Margaret A. Mortensen 04.04.2018 2014/14795-28/47845/2018 EMNE L12 Telefon Deres dato Deres referanse 22055622 13.02.2018 2014/6151-42 Ullensaker, Eidsvoll og Nannestad kommuner - Detaljregulering for Sessvollmoen skyte- og øvingsfelt - Foreløpig uttalelse til offentlig ettersyn Det vises til kommunens oversendelse datert 13. februar 2018 av reguleringsplan til offentlig ettersyn i henhold til plan- og bygningsloven § 12-10. Planområdet er på drøyt 7 km2 og ligger hovedsakelig i Ullensaker kommune, men omfatter også arealer i Nannestad og Eidsvoll. Planforslaget er i hovedsak i samsvar med gjeldende kommuneplaner. Formålet med planen er å avklare og fastsette rammevilkårene for videre utbygging og drift av Sessvollmoen skyte- og øvingsfelt. Det opplyses at det primært foreligger planer om å modernisere eksisterende anlegg, ikke å utvide skyte- og øvingsfeltet. Tiltaket er vurdert ut fra fylkeskommunens rolle som regional planmyndighet og som fagmyndighet for kulturminnevern. Fylkesrådmannen viser til uttalelse datert 21. mai 2015 til varsel om igangsatt reguleringsarbeid for området og til øvrig korrespondanse knyttet til kulturminneverdiene i området, og har følgende merknader til planforslaget: Automatisk fredete kulturminner Planområdet ble registrert av Akershus fylkeskommune våren 2005 og høsten 2014, vår ref. 03/10966 og 2014/14795. Det ble gjort funn av automatisk fredete kulturminner som er i hensyntatt i plankartet med båndleggingssone H730 (båndlegging etter lov om kulturminner). Innenfor reguleringsområdet er det også registrert automatisk fredete kulturminner i form av flere kullgroper og kullmiler, id 91319. Dette kulturminnet er fredet i medhold av lov om kulturminner av 9. -

Fartsgrense 100 Km/T På Motorveg

Kjørefart og personskadeulykker på motorveger med fartsgrense 100 km/t En evaluering av forsøk på E6 og E18 i Akershus, Buskerud og Vestfold Rapport fra Veg- og trafikkavdelingen TS-seksjonen 07/2004 RAPPORT REPORT Tittel Title Kjørefart og personskadeulykker på motorveger Driving speed and personal injury accidents on med fartsgrense 100 km/t – en evaluering av motorways with speed limit 100 km/h – an forsøk på E6 og E18 i Akershus, Buskerud og evaluation of tests on E6 and E18 in the counties Vestfold. of Akershus, Buskerud and Vestfold in Norway Forfattere Authors Finn H Amundsen, Per Ole Roald og Finn H Amundsen, Per Ole Roald and Arild Engebretsen Arild Engebretsen Avdeling/kontor Department/division Veg og trafikkavdelingen Department of Roads and Traffic Trafikksikkerhetsseksjonen Traffic operations and safety section Prosjektnr Project number Internprosjekt No Rapportnr Report number 07/2004 07/2004 Prosjektleder Project manager Finn H Amundsen Finn H Amundsen Etatssatsingsområde/oppdragsgiver Project program/client Vegdirektoratet Norwegian Public Roads Administration Emneord Key words Fartsgrense Speed limit Trafikkulykker Traffic Accidents Dybdeundersøkelse In depth Analysis Kjørefart Driving Speed Sammendrag Summary Fra 2001 – 2003 ble fartsgrensen på noen From 2001 to 2003 the speed limit on 100 km of motorveger hevet til 100 km/t, på seks strekninger motorway in Norway was increased from 90 to med en samlet lengde på ca 100 km. Denne 100 km/h. This study shows that the driving speed undersøkelsen viser hvilke erfaringer som er increased from 3 – 5 km/h, but there were no høstet i denne forbindelse. Generelt sett viser marked significant changes in road accidents or undersøkelsen at kjørefarten økte med 3 – 5 km/t, the severity of the accidents. -

Forskrift Om Skolerute for Viken Skoleåret 2021-2022

Forskrift om skolerute for Viken skoleåret 2021-2022 Forskrift gitt med hjemmel i opplæringslovens §3-2. Vedtatt av fylkestinget i Viken fylkeskommune dato 21.oktober 2020 Skoleruta for skoleåret 2021-2022 for skoler i Hurdal, Eidsvoll, Nes, Aurskog-Høland, Marker, Aremark, Halden, Hvaler, Sarpsborg, Rakkestad, Fredrikstad, Råde, Moss, Våler, Skiptvedt, Indre Østfold, Vestby, Ås, Frogn, Nesodden, Nordre Follo, Enebakk, Lørenskog, Rælingen, Lillestrøm, Nittedal, Gjerdrum, Ullensaker, Nannestad, Asker og Bærum Skoledager elever Ferier, fridager, kommentarer August 10 Første skoledag: uke 33, onsdag 18.08 September 22 Oktober 16 Høstferie: uke 40: f.o.m. mandag 04.10 t.o.m. fredag 08.10 November 21 Onsdag 17.11 Fri for elever, felles plandag for lærere Desember 15 Juleferie f.o.m. onsdag 22.12 Januar 21 Juleferie t.o.m. søndag 02.01 Februar 15 Vinterferie uke 8: f.o.m. mandag 21.02 t.o.m. fredag 25.02 Mars 23 April 15 Påskeferie f.o.m lørdag 09.04 t.o.m. mandag 18.04 Mai 20 Fri/helgedag: 17.05, 26.05 Juni 12 Fri 06.06 Siste skoledag: fredag 17.06 Sum 190 Offentlige fridager: Søndag 01.05 Tirsdag 17.05 Torsdag 26.05 Kr. Himmelfartsdag Mandag 06.06 2. pinsedag Oslo, 25.06.2020 Skoleruta for skoleåret 2021-2022 for skoler i Hemsedal, Gol, Ål, Nes i Hallingdal, Hol, Nore og Uvdal, Modum, Flå, Ringerike, Hole, Krødsherad, Sigdal, Rollag, Flesberg, Øvre Eiker, Kongsberg, Drammen, Lier, Jevnaker og Lunner Skoledager elever Ferier, fridager, kommentarer August 10 Første skoledag: uke 33, onsdag 18.08 September 22 Oktober 16 Høstferie: uke 40: f.o.m. -

Ja• VOL Xii NO 2 WAHPETON HOSTS 7 LAG JULY 8-11 !Iar'r1erica.Feverll THEME DRAWS ACTORS + NORSK ENTERTAINERS

•~i9bUlslaj~~ja• VOL Xii NO 2 WAHPETON HOSTS 7 LAG JULY 8-11 !IAr'r1ERICA.FEVERll THEME DRAWS ACTORS + NORSK ENTERTAINERS Historical drama and two groups from Norway make 7 Lag Stevne plans very promising for July 9-11 at Wahpeton, ND. Genealogy research opens at 10 am Thursday and continues to 10 pm for those registered, continuing Friday from 8 am til noon. This year the theme is "AMERIKA FEBER," the malady of ancestors who wanted to try life in a new country across the Atlantic. Contagion spread more rapidly for those whose futures included no rights to inherit property or in homes where there were already too many to feed, especially in the later 1800s. It was the 'fever' to board a ship for America with many promises, even if not all were true. Episodes based on E. Palmer Rockswold's book, PER, will be dramatized Friday evening to highlight the chosen theme. Following the play, there will be dancing in the Redwood Room with seating and soft drinks available in the "Hub". Music will be provided by the Eivind Lundby Orchestra of Loten, Norway--across Lake Mj0sa from Toten. sigdal Lag members will want to see the 1st showing of "SIGDAL", a gift videotape. It will be shown Saturday morning when individual groups meet from 9-3: 30 pm (approx). An afternoon showing at 2 is tentatively planned for those with membership in more than one lag. Pre-registration numbers largely determine which room is assigned, and anyone with an ancestor in sigdal, Eggedal, or Krodsherad is invited to send in the form on page 11. -

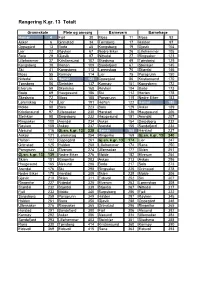

Rangering K.Gr. 13 Totalt

Rangering K.gr. 13 Totalt Grunnskole Pleie og omsorg Barnevern Barnehage Hamar 4 Fjell 30 Moss 11 Moss 92 Asker 6 Grimstad 34 Tønsberg 17 Halden 97 Oppegård 13 Bodø 45 Kongsberg 19 Gjøvik 104 Lier 22 Røyken 67 Nedre Eiker 26 Lillehammer 105 Sola 29 Gjøvik 97 Nittedal 27 Ringsaker 123 Lillehammer 37 Kristiansund 107 Skedsmo 49 Tønsberg 129 Kongsberg 38 Horten 109 Sandefjord 67 Steinkjer 145 Ski 41 Kongsberg 113 Lørenskog 70 Stjørdal 146 Moss 55 Karmøy 114 Lier 75 Porsgrunn 150 Nittedal 55 Hamar 123 Oppegård 86 Kristiansund 170 Tønsberg 56 Steinkjer 137 Karmøy 101 Kongsberg 172 Elverum 59 Skedsmo 168 Røyken 104 Bodø 173 Bodø 69 Haugesund 186 Ski 112 Horten 178 Skedsmo 72 Moss 188 Porsgrunn 115 Nedre Eiker 183 Lørenskog 74 Lier 191 Horten 122 Hamar 185 Molde 88 Sola 223 Sola 129 Asker 189 Kristiansund 97 Ullensaker 230 Harstad 136 Haugesund 206 Steinkjer 98 Sarpsborg 232 Haugesund 151 Arendal 207 Ringsaker 100 Arendal 234 Asker 154 Sarpsborg 232 Røyken 108 Askøy 237 Arendal 155 Sandefjord 234 Ålesund 116 Gj.sn. k.gr. 13 238 Hamar 168 Harstad 237 Askøy 121 Lørenskog 254 Ringerike 169 Gj.sn. k.gr. 13 240 Horten 122 Oppegård 261 Gj.sn. k.gr. 13 174 Lier 247 Grimstad 125 Halden 268 Lillehammer 174 Rana 250 Porsgrunn 133 Elverum 274 Ullensaker 177 Skien 251 Gj.sn. k.gr. 13 139 Nedre Eiker 276 Molde 182 Elverum 254 Skien 151 Ringerike 283 Askøy 213 Askøy 256 Haugesund 165 Ålesund 288 Bodø 217 Sola 273 Arendal 176 Ski 298 Ringsaker 225 Grimstad 278 Nedre Eiker 179 Harstad 309 Skien 239 Molde 306 Gjøvik 210 Skien 311 Eidsvoll 252 Ski 307 Ringerike -

Switching Relations: the Rise and Fall of the Norwegian Telecom Industry

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by NORA - Norwegian Open Research Archives Switching Relations The rise and fall of the Norwegian telecom industry by Sverre A. Christensen A dissertation submitted to BI Norwegian School of Management for the Degree of Dr.Oecon Series of Dissertations 2/2006 BI Norwegian School of Management Department of Innovation and Economic Organization Sverre A. Christensen: Switching Relations: The rise and fall of the Norwegian telecom industry © Sverre A. Christensen 2006 Series of Dissertations 2/2006 ISBN: 82 7042 746 2 ISSN: 1502-2099 BI Norwegian School of Management N-0442 Oslo Phone: +47 4641 0000 www.bi.no Printing: Nordberg The dissertation may be ordered from our website www.bi.no (Research - Research Publications) ii Acknowledgements I would like to thank my supervisor Knut Sogner, who has played a crucial role throughout the entire process. Thanks for having confidence and patience with me. A special thanks also to Mats Fridlund, who has been so gracious as to let me use one of his titles for this dissertation, Switching relations. My thanks go also to the staff at the Centre of Business History at the Norwegian School of Management, most particularly Gunhild Ecklund and Dag Ove Skjold who have been of great support during turbulent years. Also in need of mentioning are Harald Rinde, Harald Espeli and Lars Thue for inspiring discussion and com- ments on earlier drafts. The rest at the centre: no one mentioned, no one forgotten. My thanks also go to the Department of Innovation and Economic Organization at the Norwegian School of Management, and Per Ingvar Olsen. -

The Norwegian Hydrogen Highway

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Juelich Shared Electronic Resources HyNor – The Norwegian Hydrogen Highway B. Simonsen, A.M. Hansen This document appeared in Detlef Stolten, Thomas Grube (Eds.): 18th World Hydrogen Energy Conference 2010 - WHEC 2010 Parallel Sessions Book 6: Stationary Applications / Transportation Applications Proceedings of the WHEC, May 16.-21. 2010, Essen Schriften des Forschungszentrums Jülich / Energy & Environment, Vol. 78-6 Institute of Energy Research - Fuel Cells (IEF-3) Forschungszentrum Jülich GmbH, Zentralbibliothek, Verlag, 2010 ISBN: 978-3-89336-656-9 Proceedings WHEC2010 241 HyNor – The Norwegian Hydrogen Highway Bjørn Simonsen, Lillestrøm Centre of Expertise, Norway Anne Marit Hansen, Statoil, Norway 1 Introduction Hydrogen is one of the most promising energy carriers which can make the transport sector emission-free. The challenges related to hydrogen as an energy carrier are however not only technical. Due to the nature and purpose of transport, a number of refueling points or hydrogen stations are needed for it to be attractive as a fuel. The cliché “chicken and egg”- situation is often used to describe the dilemma of implementing new fuels such as hydrogen. Without hydrogen stations where people can refuel the cars, it is not profitable to produce the few cars that will be needed. Without many customers asking for hydrogen fuel and very few customers actually using the existing stations, the operators of the station will not want to build more stations due to the economical loss it presents. Hydrogen has many years been looked upon as an alternative to conventional fuels, either because of energy security and/or environmental reasons. -

Kommentarer Til Regulering Av Høgda (Kværner-Tomta) På Tranby Planutvalget Har I Møte 8

Lier kommune, Planseksjonen, Postboks 205, 3401 Lier Lierskogen, 03. januar 2017 Kommentarer til regulering av Høgda (Kværner-tomta) på Tranby Planutvalget har i møte 8. november 2016, vedtatt å legge detaljregulering for Høgda (Kværner-tomta) på Tranby ut til offentlig ettersyn i henhold til plan- og bygningslovens § 12-10. Planen omfatter eksisterende næringsområde og en utvidelse i sørvest for nye næringsarealer, samt oppgradering av Gjellebekkveien med utvidelse av kulverten under E18. Området foreslås regulert til kombinert formål for kontor og industri. Lierskogen Vel og Samfunnslag har ingen merknader til selve reguleringen av næringsarealene. Vi ønsker derimot å komme med kommentarer til planforslaget med bakgrunn i trafikksituasjonen den planlagte oppgradering av Gjellebekkveien, med utvidet kulvert under E 18, vil kunne få for trafikkbelastningen på Drammensveien (Fv16). Lierskogen Vel og Samfunnslag er opptatt av trafikksikring, både langs kommunale og fylkeskommunale veier/riksveier. Vi har spesielt fokus på trafikkøkningen på Drammensveien (Fv16), og det er alle rede i dag store trafikale utfordringer på denne veistrekningen. Vi er bekymret for at den planlagte oppgraderingen av Gjellebekkveien, med en utvidet undergang under E18, vil øke trafikkbelastningen på Drammensveien – særlig i østlig retning over Lierskogen. Trafikkanalysen som er gjort i forbindelse med reguleringen konkluderer, riktig nok, med at bare 5% av trafikken fra Gjellebekkveien vil fortsette østover forbi Lierskogen. Vi vil gjør oppmerksom på at selv en liten trafikkøkning vil forverre eksisterende trafikkproblemer på denne strekningen. Vi vil minne om at det har skjedd flere alvorlige trafikkulykker på Drammensveien, mellom Liertoppen og Heiatoppen, de siste åra - flere med tap av menneskeliv. Økt trafikk vil selvsagt også øke støybelastningen for boliger langs veien. -

Upcoming Projects Infrastructure Construction Division About Bane NOR Bane NOR Is a State-Owned Company Respon- Sible for the National Railway Infrastructure

1 Upcoming projects Infrastructure Construction Division About Bane NOR Bane NOR is a state-owned company respon- sible for the national railway infrastructure. Our mission is to ensure accessible railway infra- structure and efficient and user-friendly ser- vices, including the development of hubs and goods terminals. The company’s main responsible are: • Planning, development, administration, operation and maintenance of the national railway network • Traffic management • Administration and development of railway property Bane NOR has approximately 4,500 employees and the head office is based in Oslo, Norway. All plans and figures in this folder are preliminary and may be subject for change. 3 Never has more money been invested in Norwegian railway infrastructure. The InterCity rollout as described in this folder consists of several projects. These investments create great value for all travelers. In the coming years, departures will be more frequent, with reduced travel time within the InterCity operating area. We are living in an exciting and changing infrastructure environment, with a high activity level. Over the next three years Bane NOR plans to introduce contracts relating to a large number of mega projects to the market. Investment will continue until the InterCity rollout is completed as planned in 2034. Additionally, Bane NOR plans together with The Norwegian Public Roads Administration, to build a safer and faster rail and road system between Arna and Stanghelle on the Bergen Line (western part of Norway). We rely on close