Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Analisys of Incentives and Disincentives for Cotton In

ANALYSIS OF INCENTIVES AND DISINCENTIVES FOR COTTON IN MOZAMBIQUE OCTOBER 2012 This technical note is a product of the Monitoring African Food and Agricultural Policies project (MAFAP). It is a technical document intended primarily for internal use as background for the eventual MAFAP Country Report. This technical note may be updated as new data becomes available. MAFAP is implemented by the Food and Agriculture Organization of the United Nations (FAO) in collaboration with the Organisation for Economic Co-operation and Development (OECD) and national partners in participating countries. It is financially supported by the Bill and Melinda Gates Foundation, the United States Agency for International Development (USAID), and FAO. The analysis presented in this document is the result of the partnerships established in the context of the MAFAP project with governments of participating countries and a variety of national institutions. For more information: www.fao.org/mafap Suggested citation: Dias P., 2012. Analysis of incentives and disincentives for cotton in Mozambique. Technical notes series, MAFAP, FAO, Rome. © FAO 2013 FAO encourages the use, reproduction and dissemination of material in this information product. Except where otherwise indicated, material may be copied, downloaded and printed for private study, research and teaching purposes, or for use in non-commercial products or services, provided that appropriate acknowledgement of FAO as the source and copyright holder is given and that FAO’s endorsement of users’ views, products or services is not implied in any way. All requests for translation and adaptation rights, and for resale and other commercial use rights should be made via www.fao.org/contact-us/licence-request or addressed to [email protected]. -

Half Marathon. Kariba Town 11-16 August

Dear All They were playing polocrosse this weekend so I went down to take a look. It is being held at Chundukwa where the club is based. Lots of fun for all the family. There are four teams playing: Livingstone, Choma, Leopards Hill and Lusaka South. These are the main teams in Zambia. The Zambia Police used to play but have not been joining in for some time. Come on, Zambia Police, get your team going again – it is good for public/private relationships. Zambia has a national team which recently played in South Africa. Since that time our team has been recognised internationally and we are now 8 th in the world. Even ts on the Way 11 August: Half Marathon. Kariba Livingstone Airport Town 11-16 August: Cycle Zambia. Our town is looking very smart. Work continues on the roads 12-22 August: Mzanzi Trophy – Etosha and other facilities. The airport is due to be completed by to Livingstone. th August 13 , according to George who showed me around the 21 August: Zambezi Classic Fishing other day. However, according to a report in the press, the Competition. Katima Mulilo work was supposed to have been completed by 1 August. 24-29 August: UNWTO Transport, Works, Supply and Communications Minister 2-4 October: Fishing Competition. Yamfwa Mukanga, on a visit to the airport: I don't want to be Kariba Town coming here and waste my time just to see uncompleted 26 October: Zambezi Kayak Festival. structures. I am giving you 10 days to complete the structure. 26-31 October: World Adventure Travel Summit. -

HOW CASHEW NUT SHIPPERS GOT CRACKING M © 2008 Service Parcel United C C ANN ERI KSON 116542

October 2014 FREIGHT & TRADING WEEKLY MOZAMBIQUE READY, STEADY... MAPUTO GOES FOR GROWTH CUSTOMS MAKES SMOOTH MOVES HOW CASHEW NUT SHIPPERS GOT CRACKING © 2008 United Parcel Service Deliver more Deliver Toll free number: 0860 877 772 free Toll IT’S PEACE OF MIND FOR YOU & YOUR CUSTOMERS & PEACE OF IT’S MIND YOU FOR UPS are the world’s largest express carrier. We have 100 years of From service international and freight the to widest small portfolio packages, of you shipping can solutions. rest assured that when we’re on the job there’s nothing to worry about. IT’S NOT A BADGE A NOT IT’S MCCANN ERICKSON 116542 FTW1473SD CONTENTS www.ftwonline.co.za ozambique is a country full of (mostly) pleasant surprises. There was little talk 10 years ago that it would become a major energy producer. Or that we would see vehicles made in Mozambique. Logistics companies best positioned in the Mmarket are those with their feet on the ground – and readers of FTW, the only freight publication to invest in regular fact-finding visits to SADC countries. FTW’s Africa correspondent, Ed Richardson, reports. Cashew processing in Nampula province, Mozambique. Photo: Ton Rulkens Port of Maputo Photo: Cover Design: Zoya Lubbee Editor Joy Orlek Consulting Editor Alan Peat GENERAL NEWS SEAFREIGHT Assistant Editor Liesl Venter 2 Journalist Adele Mackenzie MODERNISING LOGISTICS HELPING SHIPPERS TO MATCH GROWTH Photographer Shannon Van Zyl 3 18 SAVE COSTS Advertising Jodi Haigh (Manager) Yolande Langenhoven Publisher Anton Marsh SMOOTHER CUSTOMS OPENING NEW Correspondents -

“Maritime Transport in Africa: Challenges, Opportunities, and an Agenda for Future Research”

UNCTAD Ad Hoc Expert Meeting (Under the framework of the IAME Conference 2018) 11 September 2018, Mombasa, Kenya “Maritime Transport In Africa: Challenges, Opportunities, and an Agenda for Future Research” Opportunity and Growth Diagnostic of Maritime Transportation in the Eastern and Southern Africa By Professor Godius Kahyarara Economics Department With Assistantship of Debora Simon Geography Department University of Dar-es-Salaam, United Republic of Tanzania This expert paper is reproduced by the UNCTAD secretariat in the form and language in which it has been received. Page 1 The views expressed are those of the author and do not necessarily reflect the views of the UNCTAD. OPPORTUNITY AND GROWTH DIAGNOSTIC OF MARITIME TRANSPORTATION IN THE EASTERN AND SOUTHERN AFRICA Professor Godius Kahyarara University of Dar-es-Salaam Economics Department With Assistantship of Debora Simon University of Dar-es-Salaam Geography Department SUMMARY This paper examines opportunities and undertakes growth diagnostics of maritime transportation in the Eastern and Southern Africa. To do so it adopts a ‘Growth Diagnostic ‘methodology proposed by Ricardo Hausman, Dani Rodrick and Andres Velasco (HRV) to identify constraints that impede development of the Maritime transport focusing on a wide range of aspects within transportation corridors that are most critical and binding constraints to development of maritime transportation. The paper also assesses existing opportunities for Maritime Transportation and proposes the best approach to rip such opportunities. Paper findings are that port inefficiency depicted by longer container dwell time, delays in vessel traffic clearance, lengthy documentation processing, lesser container per crane hour (with exception of South Africa) as one of the critical binding constraints. -

Results of Railway Privatization in Africa

36005 THE WORLD BANK GROUP WASHINGTON, D.C. TP-8 TRANSPORT PAPERS SEPTEMBER 2005 Public Disclosure Authorized Public Disclosure Authorized Results of Railway Privatization in Africa Richard Bullock. Public Disclosure Authorized Public Disclosure Authorized TRANSPORT SECTOR BOARD RESULTS OF RAILWAY PRIVATIZATION IN AFRICA Richard Bullock TRANSPORT THE WORLD BANK SECTOR Washington, D.C. BOARD © 2005 The International Bank for Reconstruction and Development/The World Bank 1818 H Street NW Washington, DC 20433 Telephone 202-473-1000 Internet www/worldbank.org Published September 2005 The findings, interpretations, and conclusions expressed here are those of the author and do not necessarily reflect the views of the Board of Executive Directors of the World Bank or the governments they represent. This paper has been produced with the financial assistance of a grant from TRISP, a partnership between the UK Department for International Development and the World Bank, for learning and sharing of knowledge in the fields of transport and rural infrastructure services. To order additional copies of this publication, please send an e-mail to the Transport Help Desk [email protected] Transport publications are available on-line at http://www.worldbank.org/transport/ RESULTS OF RAILWAY PRIVATIZATION IN AFRICA iii TABLE OF CONTENTS Preface .................................................................................................................................v Author’s Note ...................................................................................................................... -

Mozambique 2019 EITI Report English

Independent Report of the Extractive Industries Transparency Initiative Year 2019 Extractive Industries Transparency Initiative │I2A Consultoria e Serviços Index Limitation of the Scope ................................................................................................................... 6 List of Acronyms and Abbreviations ................................................................................................ 7 Executive Summary ....................................................................................................................... 11 Introduction .................................................................................................................................. 13 1.1 Scope of Work and Methodology .......................................................................................... 13 1.2 Brief description of the 2019 Standard ................................................................................. 15 Profile of Mozambique .................................................................................................................. 20 Requirement 2 - Legal framework and tax regime, including the allocation of licenses and agreements ........................................................................................................................................... 23 3.1 Legal framework and fiscal regime (Requirement 2.1) ......................................................... 23 3.1.1 Main legal instruments ................................................................................................. -

Maputo, Mozambique Casenote

Transforming Urban Transport – The Role of Political Leadership TUT-POL Sub-Saharan Africa Final Report October 2019 Case Note: Maputo, Mozambique Lead Author: Henna Mahmood Harvard University Graduate School of Design 1 Acknowledgments This research was conducted with the support of the Volvo Foundation for Research and Education. Principal Investigator: Diane Davis Senior Research Associate: Lily Song Research Coordinator: Devanne Brookins Research Assistants: Asad Jan, Stefano Trevisan, Henna Mahmood, Sarah Zou 2 MAPUTO, MOZAMBIQUE MOZAMBIQUE Population: 27,233,789 (as of July 2018) Population Growth Rate: 2.46% (2018) Median Age: 17.3 GDP: USD$37.09 billion (2017) GDP Per Capita: USD$1,300 (2017) City of Intervention: Maputo Urban Population: 36% of total population (2018) Urbanization Rate: 4.35% annual rate of change (2015-2020 est.) Land Area: 799,380 sq km Roadways: 31,083 km (2015) Paved Roadways: 7365 km (2015) Unpaved Roadways: 23,718 km (2015) Source: CIA Factbook I. POLITICS & GOVERNANCE A. Multi- Scalar Governance Sixteen years following Mozambique’s independence in 1975 and civil war (1975-1992), the government of Mozambique began to decentralize. The Minister of State Administration pushed for greater citizen involvement at local levels of government. Expanding citizen engagement led to the question of what role traditional leaders, or chiefs who wield strong community influence, would play in local governance.1 Last year, President Filipe Nyusi announced plans to change the constitution and to give political parties more power in the provinces. The Ministry of State Administration and Public Administration are also progressively implementing a decentralization process aimed at transferring the central government’s political and financial responsibilities to municipalities (Laws 2/97, 7-10/97, and 11/97).2 An elected Municipal Council (composed of a Mayor, a Municipal Councilor, and 12 Municipal Directorates) and Municipal Assembly are the main governing bodies of Maputo. -

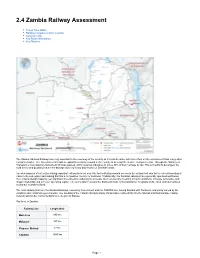

2.4 Zambia Railway Assessment

2.4 Zambia Railway Assessment Travel Time Matrix Railway Companies and Consortia Capacity Table Key Route Information Key Stations The Zambia National Railways are very important to the economy of the country as it is a bulk carrier with less effect on the environment than many other transport modes. The Government intends to expand its railway network in the country to develop the surface transport sector. Through the Ministry of Transport, a new statutory instrument (SI) was passed, which requires industries to move 30% of their carriage by rail. This is in a bid to decongest the road sector and possibly reduce the damage done by heavy duty trucks on Zambian roads. The development of rail routes linking important exit points is not only vital for facilitating smooth access to the outside but also for the overall boosting of trade in the sub-region and making Zambia a competitive country for business. Traditionally, the Zambian railways have generally operated well below their original design capacity, yet significant investment is underway to increase their volumes by investing in track conditions, increase locomotive and wagon availability and increase operating capital. The rail network remains the dominant mode of transportation for goods on the local and international routes but is under-utilized. The main railway lines are the Zambia Railways, owned by Government and the TAZARA line, linking Zambia with Tanzania, and jointly owned by the Zambian and Tanzanian governments. The opening of the Chipata-Mchinji railway link provides connectivity into the Malawi and Mozambique railway network and further connects Zambia to the port of Nacala. -

THE LAND GRABBERS of the NACALA CORRIDOR a New Era of Struggle Against Colonial Plantations in Northern Mozambique

REPORT UNAC and GRAIN February 2015 THE LAND GRABBERS OF THE NACALA CORRIDOR A new era of struggle against colonial plantations in Northern Mozambique Peasants in northern Mozambique are struggling to keep their lands as governments and foreign companies move aggressively to set up large-scale agribusiness projects. They are told that these projects will bring them benefits, but so far the country’s experience with foreign investment in agriculture has been disastrous. From liberation to land grabs Over and above this, these investments are the result Mozambique declared independence on June 25, of a very strong alliance between international capital 1975, after a decade of armed struggle. The peasants, through the big multinational corporations, with the workers, and students of Mozambique had defeated the support of the governments in their home countries Portuguese empire, guided by a common ideal of “free- with the local political-economic elite with the inten- dom of man and earth”. tion of exploiting the country’s main agro-ecological The ideals of the national liberation struggle are regions and the potential in mining and hydrocarbons. enshrined in the Republic's first constitution, which rec- It is within this context that this research analyses the ognises the right of the Mozambican people to resist all movements of the different players in the occupation forms of oppression. These ideals also resonate in the and appropriation of the Nacala Corridor, one of the first national anthem of the Republic of Mozambique, country’s richest regions, which, besides being home promising to turn the country into the grave of imperial- to the country’s main ecosystems, is the repository of ism and exploitation. -

Conference Brochure

CONFERENCE BROCHURE 13-14 June 2017 | Sandton Convention Centre | Johannesburg, South Africa Africa’s largest and only rail exhibition 100 Speakers| 7500 attendees | 850 VIP buyers | 250 exhibitors #africarail /africarail Created by: Visit www.terrapinn.com/africarail “It is a very informative conference and “Plenty of knowledge regarding African “This is a must attend event for the rail “Congratulations, one of the best and a good opportunity to network” railways is shared during the event.” industry!” most professional conferences outside Hlengiwe Sayd, Director, Department Of Transport Arvind Khare, Former CEO, Campanhia Dos Matthias Handschin, Business Development Europe!” Caminhos De Ferro Da Beira S.A.R.L. - C.C.F.B. Director, Alstom Christoph Uhl, VP Sales, Voith Turbo GmbH & Co KG “Its extremely informative and great place for networking“ Edwin Besa, Chief Director: Financial Analyst, Department of Public Enterprises – 2 – – 3 – OUR STORY AFRICA’S LONGEST RUNNING AND MOST SUCCESSFUL RAILWAYS EVENT NOW ENTERS ITS 20TH SUCCESSFUL YEAR. From humble beginnings as a small conference with a handful of exhibition stands, it now takes up 2 massive halls at the Sandton Convention Centre in Johannesburg. And has grown to become Africa’s most important and best supported railways conference and exhibition. For 2 decades, Africa Rail has become the undisputed leader. It is an unrivalled platform for the continent’s railways industry to come together … to learn, to network and to do business. Billions of dollars of business have either been initiated, Its where they open the doors to fantastic opportunities. concluded or influenced at this show. And it continues to Its where they form new and lucrative relationships & provide the meeting place for buyers, sellers and their partnerships. -

The Preparatory Survey on Nacala Port Development Project in the Republic of Mozambique

Ministry of Transport and Communications Portos e Caminhos de Ferro de Moçambique THE PREPARATORY SURVEY ON NACALA PORT DEVELOPMENT PROJECT IN THE REPUBLIC OF MOZAMBIQUE FINAL REPORT SUMMARY June 2011 JAPAN INTERNATIONAL COOPERATION AGENCY The Overseas Coastal Area Development Institute of Japan Oriental Consultants Co., Ltd. ECOH CORPORATION Ides Inc. EID CR(3) 11-079 Cost Estimation Base: the average rate in 2010 Exchange Rate: 1USD = 88.79JPY = 33.19MZN PREFACE Japan International Cooperation Agency (JICA) decided to conduct the preparatory survey on Nacala Port Development Project in the Republic of Mozambique, and organized a survey team headed by Dr. Kobune of Ides and consists of OCDI, Oriental Consultants, ECOH CORPORATION, and Ides between June, 2010 and April, 2011. The survey team held a series of discussions with the officials concerned of the Government of the Republic of Mozambique, and conducted field investigations. As a result of further studies in Japan, the present report was finalized. I hope that this report will contribute to the promotion of the project and to the enhancement of friendly relations between our two countries. Finally, I wish to express my sincere appreciation to the officials concerned of the Government of the Republic of Mozambique for their close cooperation extended to the survey team. June, 2011 Kiyofumi KONISHI Director General, Economic Infrastructure Department Japan International Cooperation Agency LETTER OF TRANSMITTAL June 2011 Mr. Kiyofumi KONISHI Director General Economic Infrastructure Department Japan International Cooperation Agency Dear Sir, It is my great pleasure to submit herewith the Final Report of “The Preparatory Survey on Nacala Port Development Project in the Republic of Mozambique”. -

Victoria Falls Day Tours & Excursions from Livingstone Day Tour

Victoria Falls Day Tours & Excursions from Livingstone Day Tour & Excursion Prices 2019 This document summarizes some of our recommended excursions & tours at Victoria Falls, if you are staying on the Zambian side. It doesn’t aim to cover absolutely everything you can do but it gives you our candid opinions. Most of the excursions below are available from either side of the Victoria Falls. If it is only available on Zimbabwe, we’ve included here as well. With the new Uni-Visa, there’s not much to stop you from enjoying activities on either side of the Victoria Falls. Times & prices of the excursions may vary by specific supplier so these prices & timings may differ slightly at time of confirmation. Water levels can also influence whether some of the water-based excursions are available at your time of travel. Note: The Zambia excursion prices below assume that you are staying at one of the Falls Resort Hotels eg The Royal Livingstone or Avani Zambezi Resort (called RLH/Avani from now on). If you are staying at one of the riverside lodges, there will be extra transfer costs (but usually these lodges transfer their guests to the various activities). Similarly there may be extra transfer and park fee costs from the David Livingstone Safari Lodge. CEDARBERG AFRICA Tel: +27 27 482 2444 Fax: +27 27 482 1420 E-mail: [email protected] Web: www.cedarberg-travel.com TOURS Tour of the Falls (Zambia & Zimbabwe) It’s a truly awe-inspiring experience – the sights, sounds and, smell of nature’s supreme force.