AB STABLE VIII LLC, ) ) Plaintiff/Counterclaim-Defendant, ) ) V

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Post Event Report

presents 9th Asian Investment Summit Building better portfolios 21-22 May 2014, Ritz-Carlton, Hong Kong Post Event Report 310 delegates representing 190 companies across 18 countries www.AsianInvestmentSummit.com Thank You to our sponsors & partners AIWEEK Marquee Sponsors Co-Sponsors Associate Sponsors Workshop Sponsor Supporting Organisations alternative assets. intelligent data. Tech Handset Provider Education Partner Analytics Partner ® Media Partners Offical Broadcast Partner 1 www.AsianInvestmentSummit.com Delegate Breakdown 310 delegates representing 190 companies across 18 countries Breakdown by Organisation Institutional Investors 46% Haymarket Financial Media delegate attendee data is Asset Managemer 19% independently verified by the BPA Consultant 8% Fund Distributor / Private Wealth Management 5% Media & Publishing 4% Commercial Bank 4% Index / Trading Platform Provider 3% Association 2% Other 9% Breakdown of Institutional Investors Insurance 31% Endowment / Foundation 27% Corporation 13% Pension Fund 13% Family Office 8% Breakdown by Country Sovereign Wealth Fund 6% PE Funds of Funds 1% Mulitlateral Finance Hong Kong 82% Institution 1% ASEAN 10% North Asia 5% Australia 1% Europe 1% North America 1% Breakdown by Job Function Investment 34% Finance / Treasury 20% Marketing and Investor Relations 19% Other 11% CEO / Managing Director 7% Fund Selection / Distribution 7% Strategist / Economist 2% 2 www.AsianInvestmentSummit.com Participating Companies Haymarket Financial Media delegate attendee data is independently verified by the BPA 310 institutonal investors, asset managers, corporates, bankers and advisors attended the Forum. Attending companies included: ACE Life Insurance CFA Institute Board of Governors ACMI China Automation Group Limited Ageas China BOCOM Insurance Co., Ltd. Ageas Hong Kong China Construction Bank Head Office Ageas Insurance Company (Asia) Limited China Life Insurance AIA Chinese YMCA of Hong Kong AIA Group CIC AIA International Limited CIC International (HK) AIA Pension and Trustee Co. -

Allianz Se Allianz Finance Ii B.V. Allianz

2nd Supplement pursuant to Art. 16(1) of Directive 2003/71/EC, as amended (the "Prospectus Directive") and Art. 13 (1) of the Luxembourg Act (the "Luxembourg Act") relating to prospectuses for securities (loi relative aux prospectus pour valeurs mobilières) dated 12 August 2016 (the "Supplement") to the Base Prospectus dated 2 May 2016, as supplemented by the 1st Supplement dated 24 May 2016 (the "Prospectus") with respect to ALLIANZ SE (incorporated as a European Company (Societas Europaea – SE) in Munich, Germany) ALLIANZ FINANCE II B.V. (incorporated with limited liability in Amsterdam, The Netherlands) ALLIANZ FINANCE III B.V. (incorporated with limited liability in Amsterdam, The Netherlands) € 25,000,000,000 Debt Issuance Programme guaranteed by ALLIANZ SE This Supplement has been approved by the Commission de Surveillance du Secteur Financier (the "CSSF") of the Grand Duchy of Luxembourg in its capacity as competent authority (the "Competent Authority") under the Luxembourg Act for the purposes of the Prospectus Directive. The Issuer may request the CSSF in its capacity as competent authority under the Luxemburg Act to provide competent authorities in host Member States within the European Economic Area with a certificate of approval attesting that the Supplement has been drawn up in accordance with the Luxembourg Act which implements the Prospectus Directive into Luxembourg law ("Notification"). Right to withdraw In accordance with Article 13 paragraph 2 of the Luxembourg Act, investors who have already agreed to purchase or subscribe for the securities before the Supplement is published have the right, exercisable within two working days after the publication of this Supplement, to withdraw their acceptances, provided that the new factor arose before the final closing of the offer to the public and the delivery of the securities. -

Lu Zhiqiang China Oceanwide

08 Investment.FIN.qxp_Layout 1 14/9/16 12:21 pm Page 81 Week in China China’s Tycoons Investment Lu Zhiqiang China Oceanwide Oceanwide Holdings, its Shenzhen-listed property unit, had a total asset value of Rmb118 billion in 2015. Hurun’s China Rich List He is the key ranked Lu as China’s 8th richest man in 2015 investor behind with a net worth of Rmb83 billlion. Minsheng Bank and Legend Guanxi Holdings A long-term ally of Liu Chuanzhi, who is known as the ‘godfather of Chinese entrepreneurs’, Oceanwide acquired a 29% stake in Legend Holdings (the parent firm of Lenovo) in 2009 from the Chinese Academy of Social Sciences for Rmb2.7 billion. The transaction was symbolic as it marked the dismantling of Legend’s SOE status. Lu and Liu also collaborated to establish the exclusive Taishan Club in 1993, an unofficial association of entrepreneurs named after the most famous mountain in Shandong. Born in Shandong province in 1951, Lu In fact, according to NetEase Finance, it was graduated from the elite Shanghai university during the Taishan Club’s inaugural meeting – Fudan. His first job was as a technician with hosted by Lu in Shandong – that the idea of the Shandong Weifang Diesel Engine Factory. setting up a non-SOE bank was hatched and the proposal was thereafter sent to Zhu Getting started Rongji. The result was the establishment of Lu left the state sector to become an China Minsheng Bank in 1996. entrepreneur and set up China Oceanwide. Initially it focused on education and training, Minsheng takeover? but when the government initiated housing Oceanwide was one of the 59 private sector reform in 1988, Lu moved into real estate. -

WIC Template 13/9/16 11:52 Am Page IFC1

In a little over 35 years China’s economy has been transformed Week in China from an inefficient backwater to the second largest in the world. If you want to understand how that happened, you need to understand the people who helped reshape the Chinese business landscape. china’s tycoons China’s Tycoons is a book about highly successful Chinese profiles of entrepreneurs. In 150 easy-to- digest profiles, we tell their stories: where they came from, how they started, the big break that earned them their first millions, and why they came to dominate their industries and make billions. These are tales of entrepreneurship, risk-taking and hard work that differ greatly from anything you’ll top business have read before. 150 leaders fourth Edition Week in China “THIS IS STILL THE ASIAN CENTURY AND CHINA IS STILL THE KEY PLAYER.” Peter Wong – Deputy Chairman and Chief Executive, Asia-Pacific, HSBC Does your bank really understand China Growth? With over 150 years of on-the-ground experience, HSBC has the depth of knowledge and expertise to help your business realise the opportunity. Tap into China’s potential at www.hsbc.com/rmb Issued by HSBC Holdings plc. Cyan 611469_6006571 HSBC 280.00 x 170.00 mm Magenta Yellow HSBC RMB Press Ads 280.00 x 170.00 mm Black xpath_unresolved Tom Fryer 16/06/2016 18:41 [email protected] ${Market} ${Revision Number} 0 Title Page.qxp_Layout 1 13/9/16 6:36 pm Page 1 china’s tycoons profiles of 150top business leaders fourth Edition Week in China 0 Welcome Note.FIN.qxp_Layout 1 13/9/16 3:10 pm Page 2 Week in China China’s Tycoons Foreword By Stuart Gulliver, Group Chief Executive, HSBC Holdings alking around the streets of Chengdu on a balmy evening in the mid-1980s, it quickly became apparent that the people of this city had an energy and drive Wthat jarred with the West’s perception of work and life in China. -

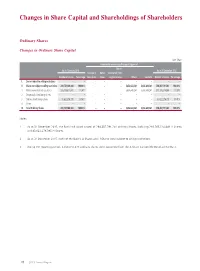

Changes in Share Capital and Shareholdings of Shareholders

Changes in Share Capital and Shareholdings of Shareholders Ordinary Shares Changes in Ordinary Share Capital Unit: Share Increase/decrease during the reporting period Shares As at 1 January 2015 As at 31 December 2015 Issuance of Bonus transferred from Number of shares Percentage new shares shares surplus reserve Others Sub-total Number of shares Percentage I. Shares subject to selling restrictions – – – – – – – – – II. Shares not subject to selling restrictions 288,731,148,000 100.00% – – – 5,656,643,241 5,656,643,241 294,387,791,241 100.00% 1. RMB-denominated ordinary shares 205,108,871,605 71.04% – – – 5,656,643,241 5,656,643,241 210,765,514,846 71.59% 2. Domestically listed foreign shares – – – – – – – – – 3. Overseas listed foreign shares 83,622,276,395 28.96% – – – – – 83,622,276,395 28.41% 4. Others – – – – – – – – – III. Total Ordinary Shares 288,731,148,000 100.00% – – – 5,656,643,241 5,656,643,241 294,387,791,241 100.00% Notes: 1 As at 31 December 2015, the Bank had issued a total of 294,387,791,241 ordinary shares, including 210,765,514,846 A Shares and 83,622,276,395 H Shares. 2 As at 31 December 2015, none of the Bank’s A Shares and H Shares were subject to selling restrictions. 3 During the reporting period, 5,656,643,241 ordinary shares were converted from the A-Share Convertible Bonds of the Bank. 79 2015 Annual Report Changes in Share Capital and Shareholdings of Shareholders Number of Ordinary Shareholders and Shareholdings Number of ordinary shareholders as at 31 December 2015: 963,786 (including 761,073 A-Share Holders and 202,713 H-Share Holders) Number of ordinary shareholders as at the end of the last month before the disclosure of this report: 992,136 (including 789,535 A-Share Holders and 202,601 H-Share Holders) Top ten ordinary shareholders as at 31 December 2015: Unit: Share Number of Changes shares held as Percentage Number of Number of during at the end of of total shares subject shares Type of the reporting the reporting ordinary to selling pledged ordinary No. -

The Arts of Making Do and Working out in Beijing, China

What are friends for?: The arts of making do and working out in Beijing, China Michelle Yang Zhang Submitted in partial fulfillment of the requirements for the degree of Doctor of Philosophy under the Executive Committee of the Graduate School of Arts and Sciences COLUMBIA UNIVERSITY 2020 © 2020 Michelle Yang Zhang All Rights Reserved Abstract What are friends for?: The arts of making do and working out in Beijing, China Michelle Yang Zhang Through a second look at the now twenty-five-year-old literature on guanxi, a form of reciprocal relationship making and using in China, I examine how the kinds of opportunities and challenges possible for young people intersect with who they know and how this has changed (with its own set of reflections on and consequences for a still-rapidly changing China) since China’s rural to urban transition. My dissertation project examines how young people in contemporary urban China form and produce guanxi ties (resource-full relationships) through the theoretical lens of practice and possibility, inspired by de Certeau’s conceptualization of practice, productive consumption, and strategies versus tactics (1984). Drawing on qualitative data gathered through participant observation and unstructured interviews, I sought to both describe and analyze when, where, and how social networks became consequential. Central to my methodology is an emphasis on people and their practices rather than the common sense categories used to describe them. The people in my field research were predominantly aged 18- 30 and came from a range of ethnic, professional, and education backgrounds. In so doing, I was able to examine the moments and contexts within which some people have opportunities and others do not, as well as when some are vulnerable while others are less so. -

Allianz Se Allianz Finance Ii B.V

3rd Supplement pursuant to Art. 16(1) of Directive 2003/71/EC, as amended (the "Prospectus Directive") and Art. 13 (1) of the Luxembourg Act (the "Luxembourg Act") relating to prospectuses for securities (loi relative aux prospectus pour valeurs mobilières) dated 25 November 2016 (the "Supplement") to the Base Prospectus dated 2 May 2016, as supplemented by the 1st Supplement dated 24 May 2016 and the 2nd Supplement dated 12 August 2016 (the "Prospectus") with respect to ALLIANZ SE (incorporated as a European Company (Societas Europaea – SE) in Munich, Germany) ALLIANZ FINANCE II B.V. (incorporated with limited liability in Amsterdam, The Netherlands) ALLIANZ FINANCE III B.V. (incorporated with limited liability in Amsterdam, The Netherlands) € 25,000,000,000 Debt Issuance Programme guaranteed by ALLIANZ SE This Supplement has been approved by the Commission de Surveillance du Secteur Financier (the "CSSF") of the Grand Duchy of Luxembourg in its capacity as competent authority (the "Competent Authority") under the Luxembourg Act for the purposes of the Prospectus Directive. The Issuer may request the CSSF in its capacity as competent authority under the Luxemburg Act to provide competent authorities in host Member States within the European Economic Area with a certificate of approval attesting that the Supplement has been drawn up in accordance with the Luxembourg Act which implements the Prospectus Directive into Luxembourg law ("Notification"). Right to withdraw In accordance with Article 13 paragraph 2 of the Luxembourg Act, investors who have already agreed to purchase or subscribe for the securities before the Supplement is published have the right, exercisable within two working days after the publication of this Supplement, to withdraw their acceptances, provided that the new factor arose before the final closing of the offer to the public and the delivery of the securities. -

© 2020 Thomson Reuters. No Claim to Original U.S. Government Works. 1 AB STABLE VIII LLC, Plaintiff/Counterclaim-Defendant, V...., Not Reported in Atl

AB STABLE VIII LLC, Plaintiff/Counterclaim-Defendant, v...., Not Reported in Atl.... 2020 WL 7024929 Only the Westlaw citation is currently available. MEMORANDUM OPINION UNPUBLISHED OPINION. CHECK *1 AB Stable VIII LLC (“Seller”) is an indirect subsidiary COURT RULES BEFORE CITING. of Dajia Insurance Group, Ltd. (“Dajia”), a corporation organized under the law of the People's Republic of China. Court of Chancery of Delaware. Dajia is the successor to Anbang Insurance Group., Ltd. (“Anbang”), which was also a corporation organized under AB STABLE VIII LLC, Plaintiff/ the law of the People's Republic of China. For simplicity, Counterclaim-Defendant, and because Anbang was the pertinent entity for much of v. the relevant period, this decision refers to both companies as MAPS HOTELS AND RESORTS ONE LLC, “Anbang.” MIRAE ASSET CAPITAL CO., LTD., MIRAE ASSET DAEWOO CO., LTD., MIRAE ASSET Through Seller, Anbang owns all of the member interests in GLOBAL INVESTMENTS, CO., LTD., and Strategic Hotels & Resorts LLC (“Strategic,” “SHR,” or the MIRAE ASSET LIFE INSURANCE CO., “Company”), a Delaware limited liability company. Strategic in turn owns all of the member interests in fifteen limited LTD., Defendants/Counterclaim-Plaintiffs. liability companies, each of which owns a luxury hotel. C.A. No. 2020-0310-JTL | Under a Sale and Purchase Agreement dated September 10, Date Submitted: October 28, 2020 2019 (the “Sale Agreement” or “SA”), Seller agreed to sell | all of the member interests in Strategic to MAPS Hotel and Date Decided: November 30, 2020 Resorts One LLC (“Buyer”) for a total purchase price of $5.8 billion (the “Transaction”). -

Trumpworld. Gli Affari Del Giovane Kushner E Le Grandi Manovre Cinesi

Trumpworld. Gli affari del giovane Kushner e le grandi manovre cinesi [da Hong Kong] Il 16 novembre scorso, in una sala dell’hotel Waldorf Astoria di New York, Jared Kushner – 35 anni, rampollo di un ricco costruttore, genero e consigliere del nuovo presidente americano Donald Trump – si è incontrato con Wu Xiaohui, Chief Executive Officier (CEO) della conglomerata cinese Anbang, che, tra le altre cose, è proprietaria dello stesso Waldorf. | 1 Trumpworld. Gli affari del giovane Kushner e le grandi manovre cinesi | 2 Trumpworld. Gli affari del giovane Kushner e le grandi manovre cinesi | 3 Trumpworld. Gli affari del giovane Kushner e le grandi manovre cinesi Jared Kushner Per inciso, ricordiamo che nel prestigioso albergo di Midtown Manhattan ha recentemente alloggiato il presidente cinese Xi Jinping mentre il presidente americano uscente Barack Obama ha preferito trovare un’altra sistemazione per i suoi soggiorni a New York, temendo di essere spiato. | 4 Trumpworld. Gli affari del giovane Kushner e le grandi manovre cinesi Il Chrysler Building, una delle icone di Manhattan, visto da una stanza del Waldorf Astoria | 5 Trumpworld. Gli affari del giovane Kushner e le grandi manovre cinesi In gennaio, poi, Trump ha ricevuto Jack Ma, il CEO di Alibaba, il gigante cinese del commercio online. La Anbang è una società estremamente interessante. “Si tratta – spiega Willy Lam, professore all’Università Cinese di Hong Kong e autore di numerosi libri sulla politica cinese – di un’impresa che ha solidi legami politici. Si ritiene che il suo presidente Wu Xiaohui sia sposato con una nipote di Deng Xiaoping (il leader succeduto a Mao Zedong che lanciò alla fine degli anni Settanta la politica di “riforma e apertura”). -

Asian Insurance Industry 2020

PRODUCT DETAILS Included with Purchase y Asian Insurance Industry 2020 y Digital report in PDF format Key findings Knowing Your Insurance Clients y Unlimited online firm-wide access y Analyst support y Exhibits in Excel y Interactive Report Dashboards OVERVIEW & METHODOLOGY This report analyzes Asia’s life insurance industry through the asset management lens. It Interactive Report provides both qualitative and quantitative information, including life insurance assets and Dashboards premiums, asset allocations, investment practices, and outsourcing trends. The report discusses Interact and explore select both institutional (general account) and retail (separate account or investment-linked product) report data with Cerulli’s segments, and covers China, Taiwan, Hong Kong, Korea, Singapore, Malaysia, Thailand, visualization tool. and Indonesia. The report also details key factors that influence insurers’ investments, such as regulations, asset-liability management, products, distribution landscapes, and other key developments. In addition to covering two region-wide themes on insurtech for distribution and investments y Asian Insurance Investment Landscape: in the low-interest-rate-environment, the report provides in-depth analysis of Asia ex-Japan y Review five years of historical life insurance premiums, assets, and insurance markets, capturing trends in both chart and text forms. investable assets in Asia ex-Japan by region and country, and view growth rates by asset type. USE THIS REPORT TO y Analyze the marketshare of life insurance -

2019 Insurance Fact Book

2019 Insurance Fact Book TO THE READER Imagine a world without insurance. Some might say, “So what?” or “Yes to that!” when reading the sentence above. And that’s understandable, given that often the best experience one can have with insurance is not to receive the benefits of the product at all, after a disaster or other loss. And others—who already have some understanding or even appreciation for insurance—might say it provides protection against financial aspects of a premature death, injury, loss of property, loss of earning power, legal liability or other unexpected expenses. All that is true. We are the financial first responders. But there is so much more. Insurance drives economic growth. It provides stability against risks. It encourages resilience. Recent disasters have demonstrated the vital role the industry plays in recovery—and that without insurance, the impact on individuals, businesses and communities can be devastating. As insurers, we know that even with all that we protect now, the coverage gap is still too big. We want to close that gap. That desire is reflected in changes to this year’s Insurance Information Institute (I.I.I.)Insurance Fact Book. We have added new information on coastal storm surge risk and hail as well as reinsurance and the growing problem of marijuana and impaired driving. We have updated the section on litigiousness to include tort costs and compensation by state, and assignment of benefits litigation, a growing problem in Florida. As always, the book provides valuable information on: • World and U.S. catastrophes • Property/casualty and life/health insurance results and investments • Personal expenditures on auto and homeowners insurance • Major types of insurance losses, including vehicle accidents, homeowners claims, crime and workplace accidents • State auto insurance laws The I.I.I. -

Springquarterlyjuly17

CDB ENGLISH QUARTERLY SPRING 2014 China Development Brief Summer 2014 Editors: Tom Bannister, Ph.D, Jeremie Beja Designer: Ezra Stoller CDB English Quarterly is produced by China Development Brief CDB (English) (www.chinadevelopmentbrief.cn) was started in the spring of 2011 as a program to provide English- language translations of CDB’s reporting. Its mission is to improve understanding and cooperation between the international community and China’s growing civil society sector. Its goals are twofold. One is to provide the international community with authoritative, independent information related to civil society and development in China. The other is to provide a platform for internationalizing China’s civil society by giving it more visibility and making it aware of important developments in civil society outside of China. CDB (English) staff achieve these goals by providing translations of Chinese-language reporting, and contributing to original research and reports on Chinese and international civil society. English edition: www.chinadevelopmentbrief.cn Chinese edition: www.cdb.org.cn 北京城区北河沿大街嵩祝院北巷鼓胡同15号 100009 15 Zhonggu Hutong Songzhuyuan Beixiang Beiheyan Dajie Dongcheng Qu Beijing 100009 PRC China Development Brief Summer 2014 CONTENTS People 4 Interview with Melissa Berman: “China is Part of Global Philanthropy Now, No Question” Melissa Berman, President and CEO of Rockefeller Philanthropy Advisors, talks to CDB’s Chen Yimei about philanthropy and China. 9 The Chengdu NGO Service Park: An Interview with Xu Qizhi Fu Tao interviews the Advisor for the new Chengdu NGO Service Park, a platform established by local party and government departments to provide incubation services to fledgling NGOs. 14 Han Hongmei: Expanding the Space at the Margins CDB Associate Editor Guo Ting profiles the work of educator and NGO founder Han Hongmei, who was chosen by the Narada Foundation to be a Gingko Partner in 2012.