24-35 Top 50 0705

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Brand Armani Jeans Celebry Tees Rochas Roberto Cavalli Capcho

Brand Armani Jeans Celebry Tees Rochas Roberto Cavalli Capcho Lady Million Just Over The Top Tommy Hilfiger puma TJ Maxx YEEZY Marc Jacobs British Knights ROSALIND BREITLING Polo Vicuna Morabito Loewe Alexander Wang Kenzo Redskins Little Marcel PIGUET Emu Affliction Bensimon valege Chanel Chance Swarovski RG512 ESET Omega palace Serge Pariente Alpinestars Bally Sven new balance Dolce & Gabbana Canada Goose thrasher Supreme Paco Rabanne Lacoste Remeehair Old Navy Gucci Fjallraven Zara Fendi allure bridals BLEU DE CHANEL LensCrafters Bill Blass new era Breguet Invictus 1 million Trussardi Le Coq Sportif Balenciaga CIBA VISION Kappa Alberta Ferretti miu miu Bottega Veneta 7 For All Mankind VERNEE Briston Olympea Adidas Scotch & Soda Cartier Emporio Armani Balmain Ralph Lauren Edwin Wallace H&M Kiss & Walk deus Chaumet NAKED (by URBAN DECAY) Benetton Aape paccbet Pantofola d'Oro Christian Louboutin vans Bon Bebe Ben Sherman Asfvlt Amaya Arzuaga bulgari Elecoom Rolex ASICS POLO VIDENG Zenith Babyliss Chanel Gabrielle Brian Atwood mcm Chloe Helvetica Mountain Pioneers Trez Bcbg Louis Vuitton Adriana Castro Versus (by Versace) Moschino Jack & Jones Ipanema NYX Helly Hansen Beretta Nars Lee stussy DEELUXE pigalle BOSE Skechers Moncler Japan Rags diamond supply co Tom Ford Alice And Olivia Geographical Norway Fifty Spicy Armani Exchange Roger Dubuis Enza Nucci lancel Aquascutum JBL Napapijri philipp plein Tory Burch Dior IWC Longchamp Rebecca Minkoff Birkenstock Manolo Blahnik Harley Davidson marlboro Kawasaki Bijan KYLIE anti social social club -

Alibaba Powers American Businesses

Alibaba Powers American Businesses For more than two decades, Alibaba has been working to support American businesses. We work with thousands of brands, SMEs, farmers and retailers to help them generate sales, engage with customers, and access global markets. In 2019, US companies sold more than $40 billion worth of goods to Chinese consumers through Alibaba’s online platforms. We have a number of e-commerce platforms that support US businesses depending on their needs. Below are just some of the thousands of American companies who sell on our platforms. Click on the links below to see how American brands are reaching the more the 800 million Chinese consumers on our business-to-consumer Tmall marketplace. ARIZONA • Arthur Andrew • Babylabs • PCA Skin • TCMZone Medical • Fender • Ping • Vet Worthy CALIFORNIA • 100% Pure • California Baby • Dole • Jarrow • Lovita • A BigHug • California • Dr. Bronner’s Formulas • Manduka • AGOLDE Mango • DW Home • JBL • Marmot • Allbirds • Callaway • Elago • Jeffrey • Mattel • Alra • Camelbak • EMBER Campbell • Meade • Amazing Grass • Canidae • Esmond • JellyBelly • Meguiars • AMD • Carlo Rossi Natural • Joby • Meyer • Ameri-Vita • Celestron • Everlane • John Masters • Milani • Andorra Life • Chevron • Fitbit Organics • MOIRA • Apple • Childlife • Gano Excel • Johnson • Mommy’s Bliss • AQUIS • ChocZero • Gap Window Films • Morphe • AviDerm • Cinema Secrets • Genexa • Joyrich • MP Natural • Citizens of • Go Groove • Juicy Couture • MRM • b.glen Humanity • GoPro • K&N • Munchkin • BabyTime • Clorox • Guess • Kate Somerville • Murad • Baby Trend • Cloud B • Gundry MD • Kensington • Natrol • Barbie • Coast Science • Gunnar • KEY • Naturade • Beats • Cold Steel • Healthy Times • KingSton • Natural • bebe • Colorescience • Herbalmax • KKW Balance • Belkin • ColourPop • Hot Wheels FRAGRANCE • NatureWise • Bella B • COOLA • Hourglass • Kopari • NeilMed • Benefit • Coromega • HP • Kor • Netgear Cosmetics • DC Shoes • HUM • L.A. -

Blissful Christmas Rewards SOGO X Chappie

SOGO X chappie 2/12-5/1 2/12-5/1 限量商品換購$1,000( 2 ) 慈善義賣SOGO X chappie 凡即日累積購物每滿 最多 張發票 , 凡購買 聖 誕 老 人 隨 身 袋, SOGO X chappie 1 2 即可換購 限量商品 件。 崇光將捐出 倍換購金額予「願望成真基金」, 幫助患病兒童實現願望。 暖笠笠小毯 換購價 盡情扭計骰 換購價 聖誕老人隨身袋 慈善價 ( $180) $80 ( $90) $45 ( $150) $65 價值 價值 價值 POINTASTIC POINTASTIC SOGO Rewards SOGO Rewards 積分換購 積分換購 5,000 + $70 5,000 + $35 5,000 + $50 積分 積分 積分 • SOGO CLUB 11/F LG/F 換購處設於崇光銅鑼灣店 ���咀� SOGO Rewards 會員專櫃。 受惠機構: • SOGO Rewards 換購金額只收現金及不可享 積分。 • / 5 每�每日 每組發票最多只限換購 件。數量有限,售完即止。 Blissful Christmas Rewards 2/12-27/12 SOGO Rewards $2,000 會員凡即日單一購物�滿淨值 , 1 即可獲贈$100 張。 $100 購物現金券 $1,500 現金券需於指定品牌商戶單一購物滿淨值 或以上 使用,詳情請參閱現金券背面之條款及細則。 • SOGO Rewards 會員須出示會員手機頁面及印有其相符會員號碼之發票正本,方可享此優惠。 • B1/F 1/F SOGO CLUB 12/F 1/F 現金券換領處設於崇光銅鑼灣店新翼 、 至 及尖沙咀� 指定收銀處。 • / / 20 每人每日 每單一發票 每個會員號碼最多只限換領現金券 張,並需即日於同一店內換領。 • POINTASTIC 購買崇光購物禮券、千足純金貨品� �賞之發票不可享此優惠。 指定品牌商戶名單 *崇光銅鑼灣店/ 只限正價 指定貨品 珠寶及手錶 B1/F Alexandre Zouari* Emporio Armani Watch Les Nereides APM MONACO Ginza Diamond Monica Vinader ARTE Madrid Gucci Timepieces & Jewellery Sunglass Hut Carat John Hardy Swarovski Charriol Just Gold WSI (Time +Style) 美妝 G/F Albion Gucci Beauty Shiseido Clarins Guerlain Sisley Cle de Peau Helena Rubinstein Sulwhasoo Decorte La Mer the history of whoo Estee Lauder La Prairie Tom Ford Beauty Fresh Lancome Valmont* Givenchy Laneige YSL Beauté B1/F Aramis Fragrance HABA Montblanc Fragrance Aveda Ipsa Moschino Fragrance bareMinerals Issey Miyake Fragrance Narciso Rodriguez Fragrance Biotherm Jimmy Choo Fragrance Nars Bobbi Brown Jo Malone London Nina Ricci Fragrance Bottega Veneta Fragrance -

Virility, Enhancement and Men's Underwear

Virilty, Enahncement and Men’s Underwear Dr. Shaun Cole Programme Director Curation and Culture Course Director MA History & Culture of Fashion Graduate School London College of Fashion The early twenty-first century has seen a fascination with notions of virility expressed through the design and promotion of men’s underwear. In 2007 Australian swim and underwear brand aussieBum introduced the ‘Wonderjock,’ which, founder Sean Ashby said, developed from requests from customers who ‘expressed an interest in looking bigger, just like women using the Wonderbra’.i To achieve this effect the Wonderjock used seams around the pouch and an additional pocket within the pouch front to ‘push up’ the genitals. The Wonderjock was advertised with images of enhanced thrusting crotches, accompanied by text that noted ‘When size matters’. The emphasis on the crotch and male virility in underwear was not new in the early 2000s. Up until the 1930s men’s underwear had primarily been loose fitting, with the exception of the French ‘slip’, reputedly invented by French brand Petit Bateau (originally founded in 1893). The slip was first advertised in the 20 September 1913 edition of L’Illustration, where it was described as ‘for athletes in fine cotton jersey, with elastic belt and thighs’ and providing ‘support without hindering any movement’. Inspired by a photographic image of similar style French ‘slip’ swimwear American underwear company Cooper’s Inc. introduced ‘Model 1001’ briefs in 1935 which provided ‘masculine support’ for the wearer’s genitals, through a double layer of soft rib-knit fabric in the centre front. The waistband and leg opening bands were made from Lastex, which helped the garment sit securely against the body. -

A Study of Fashion Change Related to Men's Boxer Undershorts As Depicted in Sears Annual Merchandise Catalogs 1946-1988

AN ABSTRACT OF THESIS OF Bernadette A. Tatarka for the degree of Master of Science in Apparel, Interiors, and Merchandising presented on May 22, 1990. Title: A Study of Fashion Changes Related To Men's Boxer Undershorts As Depicted In Sears Annual Merchandise Catalogs (1946-1988) Abstract approved_Redacted for Privacy More research has been conducted regarding women's costume history than that of men's historic costume. One area in which little research has been conducted concerns men's boxer underwear. The need for additional research dealing with basic style changes of men's boxer undershorts was compelling to this researcher, as well as adding to the literature concerning men's historic costume. The purpose of this study was to research the availability of men's boxer undershorts post World War II (1946-1988). Specifically, based on pictorial underwear fashions illustrated in the Sears Annual Merchandise Catalog, this study documented and analyzed the availability of boxer undershorts as to fiber content, fabric structure, color, style features, and special design motifs during the time period studied. The objective of the study was to increase the knowledge of men's historic costume through an investigation into the styles of men's boxer undershorts. The historical continuity of fashion, as well as other theories concerning fashion change served as the theoretical framework for this study. The historical continuity process of fashion proposes that each new fashion is an evolutionary outgrowth and elaboration of the previous fashion (Blumer, 1969). Examples include past research by Young (1937), Kroeber (1919), and Robinson (1976), which indicated that changes in fashions took place in well-defined cycles. -

Munsingwear, an Underwear for America / Marcia G. Anderson

IN 1984 the Minnesota Historical Society acquired the Mun singwear, Inc., corporate records and product samples. These business records, photographs, promotional materials, and garments ojjer an especially broad and detailed docu mentation oj the company's history jrom its inception in 1886 through the modern miracle-jiber era oj the 1970s. While there are some gaps in several categories or time peri ods, the coUection as a whole is a treasure trove oj injorma g^gMMBa8"ffl—8SM tion about the company, its competitors worldwide, and the undergarment industry in general. It provides a rare oppor tunity to compare historical documents with material cul ture over a signijicant period oj time. For more injormation on the collection, see inside the back cover. \rwi^f THE INDUSTRIAL REVOLUTION affected nearly every aspect of daily life in the 19th century. Weapons, furniture, chromolithographs, appliances, and'clothing, to name a few items, were standardized, and streamlined production made more—and new—products widely available. Although standardization and mass production limited creativity and uniqueness, their result was predictable: stable designs and reliable products that could evolve or be adapted to meet the An needs of the mass market. The Industrial Revolution fostered the idea that the useful and the aesthetic were not necessarily antithetical and that the perfection of simplicity, predictabil ity, and control were values to rival elite tastes for the beauti Underwear ful and rare. The machine-made knit-goods industry began in America in 1832, when Egbert Egberts developed equipment for knit ting socks in Cohoes, New York. His simple production For method contributed to the eventual replacement of woven goods (largely flannel) with knit goods in underwear. -

NW Buyers Affiliated Resources

NW Buyers Affiliated Resources Updated: 5/16/2018 ACCESSORIES NOW 6705 Samuel Road • Edina, MN 55439 • Ph/Fax: (952) 942-6111 • www.accessoriesnowonline.com • Company Contact: Dan Leach • Email: [email protected] CATEGORIE(S): Women’s Accessories ALL AMERICAN KHAKIS (CHARDAN LTD) 1578 Warrenton Hwy/ PO Box 1015 • Thomson, GA 30824 • Ph: 706-595-8794 •Fax: 706-595-6417 • www.allamericankhakis.com Customer Service: Judy Wood • [email protected] • Email: [email protected] • Ph: 706-595-8885 • Fax: (631) 435-8018 CATEGORIE(S): Slacks, Jeans, Walk Shorts Sales Rep(s): Jack Rubinstein Ph: (913) 908-4903 • Fax: (913) 541-0008 • Email: [email protected] • Territories: MO, KS, IA, NE, IL Bob Wolfe Cell: (952) 994-4725 • Fax: (952) 829-0789 • Email: [email protected] • Territories: MN, ND, SD, NE, IA, WI, IL, IN, MI ALLEN EDMONDS 201 E. Seven Hills Road • PO Box 998 • Port Washington, WI 53074-0998 CATEGORIE(S): Accessories, Footwear (Big & Tall Available) This Resource is ordered and billed through N.W. Buyers ALL SIZE Rugvaenget 22 • Greneaa, Denmark 8500 Company Contact: Jorgen Hem • Email: [email protected] (Please contact by email) • Ph: 0047.9139.7096 • Fax: 005.8630.9955 CATEGORIE(S): Activewear Fleece, Jeans, Knitwear, Outerwear, Pajamas/Robes, Sport Shirts, Sweaters, Swimwear, Underwear, Walk Shorts (Big & Tall Available) ALL WEATHER OUTERWEAR/TRAILCREST 1425 37 th St., Ste. 607• Brooklyn, NY 11218 • Ph: (800) 965-6550 • Fax: (347) 240-9523 • Email: [email protected] Company Contact: Judy Gross • Email: [email protected] CATEGORIE(S): -

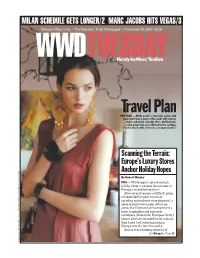

Travel Plan NEW YORK — All the World’S a Stage This Spring, with Looks That Blend a Touch of the Exotic with Natural, Simple and Pretty Elements

MILAN SCHEDULE GETS LONGER/2 MARC JACOBS HITS VEGAS/3 WWDWomen’s Wear Daily • The Retailers’TUESDAY Daily Newspaper • November 29, 2005• $2.00 Ready-to-Wear/Textiles Travel Plan NEW YORK — All the world’s a stage this spring, with looks that blend a touch of the exotic with natural, simple and pretty elements. Here, Liz McClean’s cotton gauze tunic. Jose Maria Barrera earrings; Flood’s Closet cuffs. For more, see pages 6 and 7. Scanning the Terrain: Europe’s Luxury Stores Anchor Holiday Hopes By Robert Murphy PARIS — Will shoppers spread enough holiday cheer to reverse the fortunes of Europe’s embattled retailers? After several seasons of difficult going compounded by weak consumer spending and endemic unemployment, a spate of positive economic data from across the Continent seems to point to a boost in spending and consumer confidence. Meanwhile, European luxury houses also have signaled better sales on their home turf, reporting gains in Europe over the last six months. And an overwhelming majority of See Europe’s, Page12 PHOTO BY TALAYA CENTENO; MODEL: SIMONE KERR/IMG; HAIR BY KRISTA SERAFINO; MAKEUP BY SONJA; STYLED BY MAKEUP BY SERAFINO; KRISTA CENTENO; MODEL: SIMONE KERR/IMG; HAIR BY BOBBI TALAYA PHOTO BY QUEEN 2 WWD, TUESDAY, NOVEMBER 29, 2005 WWD.COM Milan Back to Longer Show Schedule By Luisa Zargani della Moda, is completed in 2009. WWDTUESDAY Many of Milan’s fashion ex- Ready-to-Wear/Textiles MILAN — Milan Fashion Week is hibitions, such as Mipel, al- going back to a longer schedule. ready have moved to the Rho- FASHION The Camera della Moda has Pero fairgrounds outside the Designers are evoking a worldly mood for spring — one that’s created by confirmed the schedule will re- city, and will remain there. -

Gold Star Fragrances Catalog Order Information

Gold Star Fragrances Catalog Date: 2021/10/02 This catalog lists all fragrance oils available online at the time of printing. It does not reflect the prices of related Incense Oil, Massage Oil, Body Lotion and Shampoo available in 16-ounce bottles. The prices shown reflect the 1-, 4-, 8- and 16-ounce fragrance oil sizes. (In some instances the sizes may also be referred to as quarter pound (4 oz), half pound (8 oz) and one pound (16 oz) sizes which is based on shipping weight not liquid content. You can view prices of related options online in QuikScent by clicking on the fragrance oil. The prices and fragrances are subject to change online notice. Order Information You can order online at www.goldstarfragrances.com, or by calling Gold Star Fragrances at: 212-279-4474. You can also order in person at our store located at 8 West 37th Street, NY, NYC 10018. Disclaimer: The catalog does not claim that the list of oils or perfumes are the brand shown. The brand names shown are the property of the respective owner. This list is provided only to show a similarity to the scent as indicates by the word “Type.” © 2016 Gold Star Fragrances, Inc. All rights reserved. FAM5704MA: 03# 1789 Inspired by * 3:AM by Sean John [MA], $4.95, $14.75, $29.00, $56.00. F21101FE: 22# 101 Inspired by * 212 by Carolina Herrera [FE], $4.95, $14.75, $29.00, $56.00. F21351MA: 22# 351 Inspired by * 212 by Carolina Herrera [MA] , $4.95, $14.75, $29.00, $56.00. -

G-STRING and THONG the G-String, Or Thong, a Panty Front with a Half

69134-ECF-G_121-156.qxd 8/17/2004 7:01 AM Page 121 G G-STRING AND THONG The G-string, or thong, of this form of underwear; Frederick’s began to mass- a panty front with a half- to one-inch strip of fabric at market the thong, at first known as the “scanty panty,” the back that sits between the buttocks, became one of as an erotic item alongside crotchless or edible under- the most popular forms of female underwear in the early wear. By the mid-1980s, however, the thong began to be twenty-first century. Its sources are manifold; the thong appreciated as a practical garment in its own right. By bikini designed by Rudi Gernreich in 1974, launched with 2003, it had become the fastest growing segment of a matching Vidal Sassoon hairstyle, is one which in turn women’s underwear, making “full-bottomed” panties al- spawned the more popular Brazilian string bikini brief, most obsolete. In order to persuade the few reluctant or tanga, of the late 1970s. This tiny bikini—dubbed the women left to wear the thong, a “training” garment was fio denta, or dental floss—ensured that the buttocks invented called the Rio, or “starter” thong, which rose achieved maximum exposure to the sun and openly dis- more sedately up the sides to expose less of the buttocks. played an erogenous zone that was a particular favorite In the 1990s, the thong became a garment of folk- in Latino culture. loric proportions after the White House intern Monica The stripper’s G-string is another influence and has Lewinsky’s affair with U.S. -

Distributor Supplier List

Distributor Supplier List Preferred Suppliers Alliance Mercantile, Inc. Gemline Regent Apparel American Dawn (ADI) GEMPIRE RJ Schinner Ammex Golden Star S&S Activewear Augusta Sportswear GT Linens Sanford B2B Holloway Handstands Schermerhorn Co. Bros. High Five High Caliber Line Seville Gear Backpacker HTT Apparel Showdown Displays Badger Sport Illini Spector & Co Bag Makers Key Apparel St. Regis Crystal BIC Graphic Logistics Supply K&R New York Norwood Logo Mats, LLC MiPen Company Biz Collection Prestige Glass The Magnet Group Blue Generation R.S. Owens 1919 Candy Company Calderon Ritter Pen Innovations The Martin Company Callaway by Perry Ellis The Bag Factory Waterleaf Studios Benchmark Crystal Cap America Starline Charles River Apparel Castelli Perfect Line Storm Duds Raingear Chocolate Chocolate Maevn Uniforms Suntex Industries Compass Promotional Maple Ridge Farm Tiger Hill Cutter & Buck Medique Products Tingley Rubber Dickies Medline Industries Thermopatch DockYard Apparel Natural Uniforms Towel Specialties Dunbrooke Apparel Penn Emblem Unimex Dyenomite Apparel Prime Line Universal Overall EnMart Jetline Vantage Apparel Ensign Emblem Reed Viedera (Canada Only) ERB Safety ReflectiveStripe.com WOWLine Fame Fabrics Business Services Advertising Specialty Institute (ASI) OneTranz - LTL and FTL Shipping Customer Service Intelligence, Inc. - Customer Promotional Products Association Satisfaction Followup Programs International (PPAI) Enterprise Rent-A-Car - Car Rental Promotional Capital - Business Loans EVO B2B - Credit Card Processing RJ Evans and Associates - Sales & Marketing Training Fisher Phillips - Labor Law Firm Speartek - e-Commerce Solutions Fortune Web Marketing - Online Marketing Services UPS Freight - LTL Freight Hotel Engine - Hotel Booking Note: Members also have access to many other Suppliers from the Rental Division. You’ll find outstanding table linen, scrubs, lab coats, bed linen, and other products. -

The Birth of American Sportswear Atricia Campbell Warner

University of Massachusetts Amherst ScholarWorks@UMass Amherst University of Massachusetts rP ess Books University of Massachusetts rP ess 2006 When the Girls Came Out to Play: The irB th of American Sportswear Patricia Campbell Warner Follow this and additional works at: https://scholarworks.umass.edu/umpress_books Part of the History Commons, and the Women's Studies Commons Recommended Citation Warner, Patricia Campbell, "When the Girls Came Out to Play: The irB th of American Sportswear" (2006). University of Massachusetts Press Books. 5. https://scholarworks.umass.edu/umpress_books/5 This Book is brought to you for free and open access by the University of Massachusetts rP ess at ScholarWorks@UMass Amherst. It has been accepted for inclusion in University of Massachusetts rP ess Books by an authorized administrator of ScholarWorks@UMass Amherst. For more information, please contact [email protected]. WHEN THE GIRLS CAME OUT TO PLAY WHEN THE GIRLS CAME OUT TO PLAY The Birth of American Sportswear atricia Campbell Warner UNIVERSITY OF MASSACHUSETTS PRESS Amherst and Boston Copyright © 2006 by Patricia Campbell Warner All rights reserved Printed in the United States of America LC 2006003037 ISBN 1-55849-548-7 (library cloth ed.); 549-5 (paper) Designed by Sally Nichols Set in Monotype Walbaum Printed and bound by The Maple-Vail Manufacturing Group Library of Congress Cataloging-in-Publication Data Warner, Patricia Campbell, 1936– When the girls came out to play : the birth of American sportswear / Patricia Campbell Warner. p. cm. Includes bibliographical references and index. ISBN 1-55849-549-5 (pbk. : alk. paper)—ISBN 1-55849-548-7 (library cloth : alk.