WTCG / Tomson Pacific Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report 2017/18 2017/18

NIMBLE HOLDINGS COMPANY LIMITED (於開曼群島註冊成立並於百慕達繼續經營之有限公司) (Incorporated in the Cayman Islands and continued ) (前稱嘉域集團有限公司) in Bermuda with limited liability (Formerly known as The Grande Holdings Limited) 股份代號 : 186 Stock code: 186 敏捷控股有限公司 年度報告 ANNUAL REPORT 2017/18 2017/18 追求 BUILDING ON 卓越 EXCELLENCE Annual Report 2017/18 年度報告 CONTENTS CONTENTS Corporate Information 2 Chairman’s Statement 3 Management Discussion and Analysis 4 Biographies of Directors 8 Report of the Directors 10 Corporate Governance Report 18 Environmental, Social and Governance Report 31 Independent Auditor’s Report 39 Consolidated Income Statement 41 Consolidated Statement of Comprehensive Income 42 Consolidated Statement of Financial Position 43 Consolidated Statement of Changes in Equity 45 Consolidated Statement of Cash Flows 46 Notes to Consolidated Financial Statements 48 Five-Year Financial Summary 109 Nimble Holdings Company Limited Annual Report 2017/2018 1 CORPORATE INFORMATION CORPORATE INFORMATION BOARD OF DIRECTORS LEGAL ADVISORS EXECUTIVE DIRECTORS Stephenson Harwood Mr. Tan Bingzhao Johnnie Yam, Jackie Lee & Co. Mr. Deng Xiangping AUDITOR INDEPENDENT NON-EXECUTIVE Moore Stephens CPA Limited DIRECTORS Dr. Lin Jinying REGISTERED OFFICE Dr. Lu Zhenghua Wessex House, 5th Floor Dr. Ye Hengqing 45 Reid Street Hamilton HM 12, Bermuda AUDIT COMMITTEE Dr. Lu Zhenghua (Chairman) PRINCIPAL PLACE OF BUSINESS IN Dr. Lin Jinying HONG KONG Dr. Ye Hengqing 11/F., The Grande Building 398 Kwun Tong Road REMUNERATION COMMITTEE Kowloon Dr. Lin Jinying (Chairman) Hong Kong Dr. Lu Zhenghua Dr. Ye Hengqing SHARE REGISTRAR AND TRANSFER OFFICE NOMINATION COMMITTEE Tricor Tengis Limited Mr. Tan Bingzhao (Chairman) Level 22, Hopewell Center Dr. Lin Jinying 183 Queen’s Road East Dr. -

Far East Consortium International Limited Annual Report 2012

F ar East Consortium Stock Code股份代號: 035 International Limited 遠東發展有限公司 Ann u al R e po r t 2012 年報 16th Floor, Far East Consortium Building, 121 Des Voeux Road Central, Hong Kong 年報 香港德輔道中121號遠東發展大廈16樓 2012 Annual Report Website 網址:www.fecil.com.hk STAR RUBY Hong Kong Corporate Information BOARD OF DIRECTORS PRINCIPAL BANKERS Executive Directors Hong Kong David CHIU, Tan Sri Dato’, B.Sc. Cathay United Bank Company, Limited (Chairman and Chief Executive Offi cer) Chong Hing Bank Limited Dennis CHIU, B.A. Citic Bank International Limited Craig Grenfell WILLIAMS, B. ENG. (CIVIL) Dah Sing Bank, Limited DBS Bank (Hong Kong) Limited Non-Executive Director Hang Seng Bank Limited Daniel Tat Jung CHIU Industrial and Commercial Bank of China (Asia) Limited Nanyang Commercial Bank, Limited Independent Non-Executive Directors Public Bank (Hong Kong) Limited Kwok Wai CHAN The Hongkong and Shanghai Banking Corporation Limited Peter Man Kong WONG, J.P. Wing Hang Bank, Limited Kwong Siu LAM Malaysia AUDIT COMMITTEE AmBank (M) Berhad Kwok Wai CHAN (Chairman) OCBC Bank (Malaysia) Berhad Peter Man Kong WONG Public Bank Berhad Kwong Siu LAM Singapore NOMINATION COMMITTEE The Hongkong and Shanghai Banking Corporation Limited David CHIU (Chairman) Kwok Wai CHAN Australia Peter Man Kong WONG Australia and New Zealand Banking Group Limited Kwong Siu LAM Commonwealth Bank of Australia Limited REMUNERATION COMMITTEE Mainland China Kwok Wai CHAN (Chairman) Agricultural Bank of China Limited David CHIU China Construction Bank Corporation Peter Man Kong WONG DBS Bank (China) Limited HSBC Bank (China) Company Limited EXECUTIVE COMMITTEE Shanghai Pudong Development Bank Company, Limited David CHIU Wing Hang Bank (China) Limited Dennis CHIU Craig Grenfell WILLIAMS PLACE OF INCORPORATION Chris Cheong Thard HOONG Cayman Islands Denny Chi Hing CHAN Boswell Wai Hung CHEUNG REGISTERED OFFICE P.O. -

International Smallcap Separate Account As of July 31, 2017

International SmallCap Separate Account As of July 31, 2017 SCHEDULE OF INVESTMENTS MARKET % OF SECURITY SHARES VALUE ASSETS AUSTRALIA INVESTA OFFICE FUND 2,473,742 $ 8,969,266 0.47% DOWNER EDI LTD 1,537,965 $ 7,812,219 0.41% ALUMINA LTD 4,980,762 $ 7,549,549 0.39% BLUESCOPE STEEL LTD 677,708 $ 7,124,620 0.37% SEVEN GROUP HOLDINGS LTD 681,258 $ 6,506,423 0.34% NORTHERN STAR RESOURCES LTD 995,867 $ 3,520,779 0.18% DOWNER EDI LTD 119,088 $ 604,917 0.03% TABCORP HOLDINGS LTD 162,980 $ 543,462 0.03% CENTAMIN EGYPT LTD 240,680 $ 527,481 0.03% ORORA LTD 234,345 $ 516,380 0.03% ANSELL LTD 28,800 $ 504,978 0.03% ILUKA RESOURCES LTD 67,000 $ 482,693 0.03% NIB HOLDINGS LTD 99,941 $ 458,176 0.02% JB HI-FI LTD 21,914 $ 454,940 0.02% SPARK INFRASTRUCTURE GROUP 214,049 $ 427,642 0.02% SIMS METAL MANAGEMENT LTD 33,123 $ 410,590 0.02% DULUXGROUP LTD 77,229 $ 406,376 0.02% PRIMARY HEALTH CARE LTD 148,843 $ 402,474 0.02% METCASH LTD 191,136 $ 399,917 0.02% IOOF HOLDINGS LTD 48,732 $ 390,666 0.02% OZ MINERALS LTD 57,242 $ 381,763 0.02% WORLEYPARSON LTD 39,819 $ 375,028 0.02% LINK ADMINISTRATION HOLDINGS 60,870 $ 374,480 0.02% CARSALES.COM AU LTD 37,481 $ 369,611 0.02% ADELAIDE BRIGHTON LTD 80,460 $ 361,322 0.02% IRESS LIMITED 33,454 $ 344,683 0.02% QUBE HOLDINGS LTD 152,619 $ 323,777 0.02% GRAINCORP LTD 45,577 $ 317,565 0.02% Not FDIC or NCUA Insured PQ 1041 May Lose Value, Not a Deposit, No Bank or Credit Union Guarantee 07-17 Not Insured by any Federal Government Agency Informational data only. -

S42009131318p3.Ps, Page 1-24 @ Normalize 2

2009 年第 13 期憲報第 4 號特別副刊 S. S. NO. 4 TO GAZETTE NO. 13/2009 D1117 ENGLISH AUTHOR INDEX, 2007 139 Holdings Limited 7056 APT Satellite Holdings Limited 3135 82 Republic 8086 Aptus Holdings Limited 10975 Abbs, Brian 3107 Architectural Services Department 22, abc Multiactive Limited 10 7101-7102 Abyar, Narges 13197 Archworld 666, 2242, 2719 Accountancy Training Company 11-15, Arlon, Penelope 4919, 5035, 5544, 6766 10946-10954 Armentrout, Fred 308, 7211 Achtemeier, Paul J 2474 Armstrong, J. K. 3461, 3469, 7300, 7317, AcrossAsia Limited 3115 11138, 11148-11150, 11152, Adams, Penny 3116-3118 11161-11162 Adrian-Vallance, D’Arcy 10956-10957 Arnobius 4869 Adrian-Vallance, Evadne 10966-10967 Arnold, Bill T 10253 Aesop 1078 Arnold, Peter 9895, 13676, 13802 Agriculture and Fisheries Art Textile Technology International Department 3119, 7082 Company Limited 10979 Agriculture, Fisheries and Arterburn, Stephen 8835 Conservation Department 7083 Artfield Group Limited 3141, 7104, 10980 AGTech Holdings Limited 10958 Arthur, David 1452-1453 Ahluwalia, Libby 11577 Arthur, Kay 1146-1147, 1370-1371, 1452-1453, Ahoor, Darviz 12297 1505-1506, 1536-1537, 2198-2199, Ai, Weiwei 3120 2652-2653 Akrami, Jamaloldin 12085 Artist Commune Administration Alata 587-588, 1129, 12024-12025 Office 7804, 7849, 7857 Albaut, Corinne 18-19 Arts Optical International Holdings Albee, Edward 5952, 6891 Limited 3142 Albornoz-Chacon, Ruth 315 Aru 3031, 10784 Alco Holdings Limited 7085 Ashcroft, Minnie 9043, 9045 Alcott, Louisa May 3121 Asia Monitor Resource Center 261 Alder, C 9870 Asia -

Akai Liquidator Cosimo Borrelli's Pursuit of Truth Unravels Corporate Collapse Naomi Rovnick

Hard work pays off for 'vicious' Akai liquidator Cosimo Borrelli's pursuit of truth unravels corporate collapse Naomi Rovnick Updated on Oct 06, 2009 A tycoon is accused of stealing more than US$800 million from his international conglomerate and bankrupting the company, while another businessman allegedly conspires to hide the rest of the failed firm's assets from its creditors. The affair leads to a High Court trial, which collapses. The conglomerate's Big Four auditor is said to have fabricated documents, then gets raided by the anti-fraud police and sees one of its partners arrested. The events look like scenes from a crime thriller, but the saga of Akai Holdings, the former empire of disgraced entrepreneur James Ting that collapsed in 2000, is very real and has shaken the foundations of corporate Hong Kong, heightening fears about freewheeling tycoons and the auditors and regulators that are meant to protect companies' shareholders and lenders. The scandal resurfaced in a High Court case against Akai's former auditor, Ernst & Young Hong Kong, last month. The claimants, Akai's liquidators, accused the auditor of tampering with and faking audit files to shield itself from the US$1 billion negligence claim. The Commercial Crime Bureau has launched a fraud investigation into Ernst & Young and late last month arrested Edmund Dang, one of its partners, who was freed on bail without being charged. Yesterday, in a separate trial, Hong Kong tycoon Christopher Ho Wing-on settled a High Court case where Akai's liquidators had accused him of misappropriating the failed electronics firm's assets into his Grande Holdings vehicle in 1999, so Akai's creditors could not retrieve any money. -

2002 Milestones

2002 Milestones • CKWB held its 77th Ordinary Yearly Meeting & Extraordinary General Meeting • CKWB held a cocktail reception to celebrate its • CKWB successfully issued US$250 million of 80th Anniversary & Completion of Acquisition Perpetual Subordinated Guaranteed Notes, the first- of HKCB and published a Congratulatory • CITIC Ka Wah Bank Limited (‘CKWB’) ever Perpetual Upper Tier II Capital Security in Asia Supplement in five local newspapers completed the acquisition of The (ex-Japan) Hongkong Chinese Bank, Limited • CKWB and CITIC completed the transaction of (‘HKCB’) CCMH’s Share Transfer and Subscription with CITIC Pacific. CKWB and CITIC each hold 25% of CCMH with the remaining 50% held by CITIC Pacific • CKWB launched first-in-market Mortgage Refinancing Service of up to 140% of current market value • CKWB successfully raised HK$726 • CKWB and CITIC entered into a Share Transfer million through a Rights Issue and Subscription Agreement with CITIC Pacific • Establishment of CITIC Capital Markets Limited (‘CITIC Pacific’), under which the latter Holdings Limited (‘CCMH’) as the became a substantial shareholder of CCMH holding company of Ka Wah Capital • CKWB established a Syndication Desk within the Limited (‘Ka Wah Capital’) and Cargary Corporate Banking Group Securities Limited (‘Cargary Securities’) • CKWB arranged US$20 million Syndicated Term • CKWB completed Phase Two Loan Facility for Far East Consortium International Implementation of Core Banking System Limited • CKWB launched Financial Needs Analysis Service 1JAN 3 MAR -

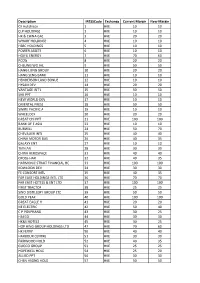

CFD Margin 201704.Xlsx

Description IRESSCode Exchange Current Margin New Margin CK Hutchison 1 HKE 10 10 CLP HOLDINGS 2 HKE 10 10 HK & CHINA GAS 3 HKE 20 20 WHARF HOLDINGS 4 HKE 10 10 HSBC HOLDINGS 5 HKE 10 10 POWER ASSETS 6 HKE 10 10 HOIFU ENERGY 7 HKE 70 60 PCCW 8 HKE 20 20 CHEUNG WO IHL 9 HKE 50 50 HANG LUNG GROUP 10 HKE 20 20 HANG SENG BANK 11 HKE 10 10 HENDERSON LAND BONUS 12 HKE 10 10 HYSAN DEV 14 HKE 20 20 VANTAGE INT'L 15 HKE 50 50 SHK PPT 16 HKE 10 10 NEW WORLD DEV 17 HKE 10 10 ORIENTAL PRESS 18 HKE 50 50 SWIRE PACIFIC A 19 HKE 10 10 WHEELOCK 20 HKE 20 20 GREAT CHI PPT 21 HKE 100 100 BANK OF E ASIA 23 HKE 10 10 BURWILL 24 HKE 50 70 CHEVALIER INTL 25 HKE 40 40 CHINA MOTOR BUS 26 HKE 40 35 GALAXY ENT 27 HKE 10 10 TIAN AN 28 HKE 30 30 CHINA AEROSPACE 31 HKE 40 40 CROSS-HAR 32 HKE 40 35 HARMONIC STRAIT FINANCIAL HO 33 HKE 100 100 KOWLOON DEV 34 HKE 30 30 FE CONSORT INTL 35 HKE 40 35 FAR EAST HOLDINGS INTL LTD 36 HKE 70 70 FAR EAST HOTELS & ENT LTD 37 HKE 100 100 FIRST TRACTOR 38 HKE 25 25 SINO DISTILLERY GROUP LTD 39 HKE 50 50 GOLD PEAK 40 HKE 100 100 GREAT EAGLE H 41 HKE 20 20 NE ELECTRIC 42 HKE 50 40 C P POKPHAND 43 HKE 30 25 HAECO 44 HKE 30 30 HK&S HOTELS 45 HKE 30 25 HOP HING GROUP HOLDINGS LTD 47 HKE 70 60 HK FERRY 50 HKE 40 40 HARBOUR CENTRE 51 HKE 30 30 FAIRWOOD HOLD 52 HKE 40 35 GUOCO GROUP 53 HKE 25 25 HOPEWELL HOLD 54 HKE 25 20 ALLIED PPT 56 HKE 30 30 CHEN HSONG HOLD 57 HKE 50 50 SUNWAY INTERNATIONAL HLDGS 58 HKE 70 70 SKYFAME REALTY 59 HKE 70 60 NORTH ASIA RESOURCES HOLDING 61 HKE 50 50 TRANSPORT INTL 62 HKE 30 30 WINFOONG INTERNATIONAL LTD 63 -

ANNUAL REPORT 年報 Annual Report 2013

Far East Consortium International Limited Incorporated in the Cayman Islands with limited liability 於開曼群島註冊成立之有限公司 Stock Code 股份代號:035 遠東發展有限公司 2013 ANNUAL REPORT 年報 Annual Report 2013 16th Floor, Far East Consortium Building, 121 Des Voeux Road Central, Hong Kong 香港德輔道中 121 號遠東發展大廈 16 樓 年報 Website 網址: www.fecil.com.hk UNITED KINGDOM CHINA • Property development UNITED KINGDOM CHINA • Investment properties • Two hotels under development • Three operational hotels and Shanghai Chengdu two hotels under development Wuhan Zhuji HONG KONG Guangzhou • Property development Zhongshan Hong Kong • Investment properties • Ten operational hotels and two hotels under development MALAYSIA • Property development • Five operational hotels Labuan Kuala LumpurMALAYSIA • Car park operations Subang Johor SINGAPORE SINGAPORE • Property development • Investment properties • One operational hotel AUSTRALIA AND NEW ZEALAND • Property development AUSTRALIA • Investment properties DIVERSIFIED AND BALANCED • Car park operations PORTFOLIO OF BUSINESSES FEC has a geographically diverse footprint across the Asia Pacifi c and Europe NEW ZEALAND Design, Printing & Production : GenNex Financial Media Limited 設計、印刷及製作 :智盛財經媒體有限公司 www.gennexfm.com CHINA • Property development • Investment properties • Three operational hotels and two hotels under development HONG KONG • Property development • Investment properties • Ten operational hotels and two hotels under development AUSTRALIA AND NEW ZEALAND • Property development AUSTRALIA • Investment properties • Car park operations NEW ZEALAND CORPORATE INFORMATION BOARD OF DIRECTORS CHIEF FINANCIAL OFFICER AUSTRALIA EXECUTIVE DIRECTORS AND COMPANY SECRETARY Australia and New Zealand Banking Group David CHIU, Tan Sri Dato’, B.Sc. Boswell Wai Hung CHEUNG Limited (Chairman and Chief Executive Officer) Commonwealth Bank of Australia Limited Chris Cheong Thard HOONG, B. ENG., ACA AUTHORISED Westpac Banking Corporation Denny Chi Hing CHAN REPRESENTATIVES Dennis CHIU, B.A. -

Foreign Banks in China

www.pwccn.com Foreign Banks in China This survey focuses on the strategic and emerging issues faced by foreign banks in China. July 2012 Growth Foreign banks more than doubled profits in 2011 to RMB 16.73 billion They also expect to grow revenues by 20% over the next three years Regulation The regulatory environment is the number one challenge for foreign banks Shanghai as an IFC Foreign banks say interest rate and RMB liberalisation are key to Shanghai’s ambition Talent Despite talent challenges, foreign banks expect to recruit 20,000 more people by 2015 Foreword Welcome to the 7th edition of our annual CEOs of foreign banks continue to view In addition to our analysis of the survey survey of China’s foreign banking sector. the impact of regulation as their biggest results, the report also contains challenge. Some banks view this perspectives from us on three key Foreign banks have so far succeeded in situation as a burden, while others are areas: future growth, Shanghai as an China but a tide of change is coming. proactively engaging with the IFC and regulation. Regulator. 2011 was a year of significant growth We would like to thank the CEOs and with the foreign banks. The sector Shanghai continues to chart a course Senior Executives who participated in posted record profits of RMB 16.73 towards becoming an International the survey. Their time and effort made billion, while total assets grew 23.6 per Financial Centre (IFC) by 2020. Foreign this publication possible. We would also cent to RMB 2.15 trillion. -

Law Man-Chung 羅敏聰⼤律師

LAW MAN-CHUNG 羅敏聰⼤律師 Call: 1997 (HK) Accredited as Mediator by CEDR in 2010 PROFILE MC Law has a broad civil and commercial practice, with focus on cross-border disputes and company disputes. He advises and acts in disputes in various fields, including conflict of laws, company and shareholders disputes, PRC joint ventures, corporate finance, insolvency, general commercial and contractual disputes, libel and slander, banking, probate, land and conveyancing (including DMC disputes, land resumption, etc), confidential information; discrimination, trusts and arbitration. He has also involved in various applications for interlocutory injunctions, appointment and removal of receivers and provisional liquidators. Recent cases include Competition Commission v. Nutanix (first competition trial in Hong Kong); China Life Insurance v. Li Xiaoming, Yu Rui Co Ltd (acting for China Life in investment disputes in Mongolia and winding up of foreign company); Shenzhen Futaihong v. BYD (acting for Foxconn companies against BYD companies for breach of confidence claims). CONTACT Email: [email protected] Tel: (+852) 2523 2003 Fax: (+852) 2810 0302 SECRETARY Name: Amy Chan Email: [email protected] Tel: (+852) 2248 1894 PRACTICE AREAS Conflict of Laws Company Commercial Injunction / Contempt Insolvency Equity / Trust Banking / Finance Professional Liability Defamation / Media Securities & Regulation Discrimination Civil Fraud / Asset Recovery Probate / Succession Restitution / Unjust Enrichment Arbitration Confidentiality / Privacy Technology, Media and Telecommunications Property & Conveyancing Insurance Competition Mediation APPOINTMENTS AND PUBLIC OFFICE External Examiner – Chinese University of Hong Kong PCLL (2008 - ) External Examiner - City University of Hong Kong PCLL (2008 - ) EDUCATION 1986 - 1993 Queen’s College, Hong Kong 1996 BA (Jurisprudence), University of Oxford SCHOLARSHIP AND PRIZES 1993 - 1996 Lee Shau Kee Scholarship tenable at Wadham College, University of Oxford SELECTED CASES CONFLICT OF LAWS First Laser Ltd v. -

Why BRIFE? 展會優勢? Expanding Business & Markets Developing the Belt and Road Network 擴展「一帶一路」市場 拓展「一帶一路」網絡

Belt and Road Countries「一帶一路」國家 The Belt and Road Initiative covers and links up over 70 countries spanning over China, ASEAN, Middle East, Central and Eastern Europe etc. 「一帶一路」倡議覆蓋及聯繫70多個國家,當中包括中國、東盟、中東、中歐及東歐。 China 中國 Northeast Asia 東北亞 Australasia 澳大利西亞 • CHINA 中國 • MONGOLIA 蒙古 • NEW ZEALAND 新西蘭 • REPUBLIC OF KOREA 韓國 Southeast Asia 東南亞 Central and Eastern Europe • BRUNEI 汶萊 Middle East 中東 中歐及東歐 • CAMBODIA 柬埔寨 • BAHRAIN 巴林 • ALBANIA 阿爾巴尼亞 • INDONESIA 印尼 • EGYPT 埃及 • BELARUS 白俄羅斯 • LAOS 老撾 • IRAN 伊朗 • BOSNIA AND HERZEGOVINA • MALAYSIA 馬來西亞 • IRAQ 伊拉克 波斯尼亞與黑塞哥維那 • MYANMAR 緬甸 • ISRAEL 以色列 • BULGARIA 保加利亞 • PHILIPPINES 菲律賓 • JORDAN 約旦 • CROATIA 克羅地亞 • SINGAPORE 新加坡 • KUWAIT 科威特 • CZECH REPUBLIC 捷克 • THAILAND 泰國 • LEBANON 黎巴嫩 • ESTONIA 愛沙尼亞 • TIMOR-LESTE 東帝汶 • OMAN 阿曼 • GEORGIA 格魯吉亞 • VIETNAM 越南 • PALESTINE 巴勒斯坦 • HUNGARY 匈牙利 • QATAR 卡塔爾 • LATVIA 拉脫維亞 South Asia 南亞 • SAUDI ARABIA 沙特阿拉伯 • LITHUANIA 立陶宛 • BANGLADESH 孟加拉 • SYRIA 敘利亞 • MACEDONIA 馬其頓 • BHUTAN 不丹 • UNITED ARAB EMIRATE • MOLDOVA 摩爾多瓦 • INDIA 印度 阿拉伯聯合酋長國 • MONTENEGRO 黑山 • MALDIVES 馬爾代夫 • YEMEN 也門 • POLAND 波蘭 • NEPAL 尼泊爾 • ROMANIA 羅馬尼亞 • PAKISTAN 巴基斯坦 Africa 非洲 • RUSSIA 俄羅斯 • SRI-LANKA 斯里蘭卡 • ETHIOPIA 埃塞俄比亞 • SERBIA 塞爾維亞 • SOUTH AFRICA 南非 • SLOVAKIA 斯洛伐克 Central Asia 中亞 • SLOVENIA 斯洛文尼亞 • AFGHANISTAN 阿富汗 • TURKEY 土耳其 • ARMENIA 亞美尼亞 • UKRAINE 烏克蘭 • AZERBAIJAN 阿塞拜疆 • KAZAKHSTAN 哈薩克 • KYRGYZSTAN 吉爾吉斯 • TAJIKISTAN 塔吉克 • TURKMENISTAN 土庫曼 • UZBEKISTAN 烏茲別克 P.1 Unimpeded Trade is the Major Goal of The Belt & Road Initiative 貿易暢通是「一帶一路」倡議的主要目標 Unimpeded Trade Policy 貿易暢通 People-to-people Co-ordination Bonds 政策溝通 民心相通 1 2 3 4 5 Facilities Financial Connectivity Integration 設施聯通 資金融通 P.2 Apothegm 題辭 Mr Edward Yau Tang-wah, GBS, JP Secretary for Commerce and Economic Development Hong Kong Special Administrative Region Government 邱騰華先生, 金紫荊星章,太平紳士 香港特別行政區商務及經濟發展局局長 Converging the Gourmets, Thriving all Flavors. -

Linda Chan Sc 陳靜芬資深大律師

LINDA CHAN SC 陳靜芬資深大律師 Call: 1996 (HK); 1996 (England & Wales) Inner Bar: 2011 Accredited as mediator by CEDR in 2007 P R O F I L E Linda Chan’s practice comprises litigation and advisory work in the fields of company law, insolvency law, commercial dispute and professional negligence, with particular focus on applications under the Companies Ordinance, matters relating to directors’ duties, shareholders’ rights and remedies, corporate restructuring, capital restructuring and schemes of arrangement. She has been instructed in relation to numerous shareholders disputes, derivative actions, unfair prejudice petitions, “just and equitable” winding up petitions and bankruptcy matters. She has also been instructed to advise the liquidators in relation to complicated liquidations involving substantial listed companies in Hong Kong including the liquidation of Akai Holdings Limited, Kong Wah Holdings Limited, The New China Hong Kong Group Ltd, Ocean Grand Holdings Ltd, China Metal Recycling (Holdings) Ltd and China Medical Technologies, Inc.. C O N T A C T Email: [email protected] Tel: (+852) 2523 2003 SECRETARY Name: Karmen Yiu Tel: (+852) 2248 1883 P R A C T I C E A R E A S Company Commercial Civil Fraud / Asset Recovery Insolvency Injunction / Contempt Professional Liability Securities & Regulation Arbitration A P P O I N T M E N T S A N D P U B L I C O F F I C E Current Recorder of the Court of First Instance, High Court (2015-) Board Member, Airport Authority Board (2018-) Member, Standing Committee on Company Law Reform (2017-)