Li Ka-Shing's Flagship Is Looking Like a Bargain

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CK HUTCHISON HOLDINGS LIMITED (“CK Hutchison”) And

HUTCHISON WHAMPOA INTERNATIONAL (03/33) LIMITED (the “Issuer”) US$1,500,000,000 7.45% Guaranteed Notes due 2033 (the “Notes”) (ISIN: US44841SAC35/CUSIP: 44841SAC3/Common Code: 018124572 for Rule 144A Notes) (ISIN: USG4672CAC94/CUSIP: G4672CAC9/Common Code: 018124629 for Regulation S Notes) unconditionally and irrevocably guaranteed by CK HUTCHISON HOLDINGS LIMITED (“CK Hutchison”) and HUTCHISON WHAMPOA LIMITED In accordance with Regulation (EU) No. 596/2014 on market abuse and the law of 11 January 2008 on transparency requirements, as amended, the Issuer is filing with the Commission de Surveillance du Secteur Financier, storing with the Officially Appointed Mechanism and publishing the attached unaudited results for the six months ended 30 June 2019 of CK Hutchison, a guarantor of the Notes issued by the Issuer. The attached document was also published by CK Hutchison at 4:31 pm and 4:32 pm (Hong Kong time), 1 August 2019 on the websites of Hong Kong Exchanges and Clearing Limited and CK Hutchison, respectively. Hutchison Whampoa International (03/33) Limited Edith Shih Director and Company Secretary 1 August 2019 Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this document, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this document. UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 30 JUNE 2019 HIGHLIGHTS -

Stock Code Stock Name Margin Category HK 1 CK HUTCHISON HOLDINGS LTD

UOB KAY HIAN (SINGAPORE) PRIVATE LIMITED MARGIN STOCK LIST - HONG KONG MARKET 1 April 2021 Stock Code Stock Name Margin Category HK 1 CK HUTCHISON HOLDINGS LTD. SA HK 2 CLP HOLDINGS LTD. A HK 3 HONG KONG AND CHINA GAS CO. LTD. A HK 4 WHARF (HOLDINGS) LTD. A HK 5 HSBC HOLDINGS PLC SA HK 6 POWER ASSETS HOLDINGS LTD. SA HK 8 PCCW LTD. C HK 10 HANG LUNG GROUP LTD. A HK 11 HANG SENG BANK LTD. SA HK 12 HENDERSON LAND DEVELOPMENT CO. LTD. A HK 14 HYSAN DEVELOPMENT CO. LTD. B HK 16 SUN HUNG KAI PROPERTIES LTD. SA HK 17 NEW WORLD DEVELOPMENT CO. LTD. A HK 19 SWIRE PACIFIC LTD. 'A' A HK 23 BANK OF EAST ASIA, LTD. A HK 27 GALAXY ENTERTAINMENT GROUP LTD. A HK 38 FIRST TRACTOR CO LTD. - H SHARES D HK 41 GREAT EAGLE HOLDINGS LTD. C (Max Net Loan H$10M) HK 45 HONGKONG AND SHANGHAI HOTELS, LTD. B (Max Net Loan H$10M) HK 53 GUOCO GROUP LTD. B (Max Net Loan H$10M) HK 56 ALLIED PROPERTIES (HK) LTD. D HK 62 TRANSPORT INTERNATIONAL HOLDINGS LTD. D (Max Net Loan H$1M) HK 66 MTR CORPORATION LTD. SA HK 69 SHANGRI-LA ASIA LTD. A HK 81 CHINA OVERSEAS GRAND OCEANS GROUP LTD. C HK 83 SINO LAND CO. LTD. A HK 86 SUN HUNG KAI & CO. LTD. D HK 87 SWIRE PACIFIC LTD. 'B' A (Max Net Loan H$10m) HK 101 HANG LUNG PROPERTIES LTD. A HK 107 SICHUAN EXPRESSWAY CO. -

STOXX Hong Kong All Shares 50 Last Updated: 01.12.2016

STOXX Hong Kong All Shares 50 Last Updated: 01.12.2016 Rank Rank (PREVIOUS ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) ) KYG875721634 BMMV2K8 0700.HK B01CT3 Tencent Holdings Ltd. CN HKD Y 128.4 1 1 HK0000069689 B4TX8S1 1299.HK HK1013 AIA GROUP HK HKD Y 69.3 2 2 CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 60.3 3 4 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 57.5 4 3 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 37.7 5 5 CNE1000001Z5 B154564 3988.HK CN0032 BANK OF CHINA 'H' CN HKD Y 32.6 6 7 KYG217651051 BW9P816 0001.HK 619027 CK HUTCHISON HOLDINGS HK HKD Y 32.0 7 6 HK0388045442 6267359 0388.HK 626735 Hong Kong Exchanges & Clearing HK HKD Y 28.5 8 8 CNE1000003X6 B01FLR7 2318.HK CN0076 PING AN INSUR GP CO. OF CN 'H' CN HKD Y 26.5 9 9 CNE1000002L3 6718976 2628.HK CN0043 China Life Insurance Co 'H' CN HKD Y 20.4 10 15 HK0016000132 6859927 0016.HK 685992 Sun Hung Kai Properties Ltd. HK HKD Y 19.4 11 10 HK0883013259 B00G0S5 0883.HK 617994 CNOOC Ltd. CN HKD Y 18.9 12 12 HK0002007356 6097017 0002.HK 619091 CLP Holdings Ltd. HK HKD Y 18.3 13 13 KYG2103F1019 BWX52N2 1113.HK HK50CI CK Property Holdings HK HKD Y 17.9 14 11 CNE1000002Q2 6291819 0386.HK CN0098 China Petroleum & Chemical 'H' CN HKD Y 16.8 15 14 HK0688002218 6192150 0688.HK 619215 China Overseas Land & Investme CN HKD Y 14.8 16 16 HK0823032773 B0PB4M7 0823.HK B0PB4M Link Real Estate Investment Tr HK HKD Y 14.6 17 17 CNE1000003W8 6226576 0857.HK CN0065 PetroChina Co Ltd 'H' CN HKD Y 13.5 18 19 HK0003000038 6436557 0003.HK 643655 Hong Kong & China Gas Co. -

FACTSHEET - AS of 30-Sep-2021 Solactive GBS Hong Kong Large & Mid Cap Index TR

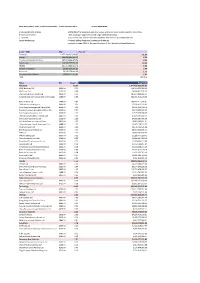

FACTSHEET - AS OF 30-Sep-2021 Solactive GBS Hong Kong Large & Mid Cap Index TR DESCRIPTION The Solactive GBS Hong Kong Large & Mid Cap Index TR is part of the Solactive Global Benchmark Series which includes benchmark indices for developed and emerging market countries. The index intends to track the performance of the large and mid cap segment covering approximately the largest 85% of the free-float market capitalization in the Hong Kong market. It is calculated as a totalreturn index in HKD and weighted by free-float market capitalization. HISTORICAL PERFORMANCE 1,400 1,200 1,000 800 600 400 Jan-2008 Jan-2010 Jan-2012 Jan-2014 Jan-2016 Jan-2018 Jan-2020 Jan-2022 Solactive GBS Hong Kong Large & Mid Cap Index TR CHARACTERISTICS ISIN / WKN DE000SLA4H36 / SLA4H3 Base Value / Base Date 462.12 Points / 08.05.2006 Bloomberg / Reuters / .SHKLMCT Last Price 1256.93 Index Calculator Solactive AG Dividends Reinvested Index Type Total Return Calculation 8:00 am to 10:30 pm (CET), every 15 seconds Index Currency HKD History Available daily back to 08.05.2006 Index Members 52 FACTSHEET - AS OF 30-Sep-2021 Solactive GBS Hong Kong Large & Mid Cap Index TR STATISTICS 30D 90D 180D 360D YTD Since Inception Performance -6.80% -10.27% -11.73% 9.67% -4.51% 171.99% Performance (p.a.) - - - - - 6.71% Volatility (p.a.) 21.54% 18.63% 16.63% 17.91% 18.51% 20.09% High 1364.34 1419.58 1482.24 1493.61 1493.61 1493.61 Low 1228.29 1228.29 1228.29 1115.51 1228.29 287.41 Sharpe Ratio -2.67 -1.91 -1.34 0.55 -0.32 0.33 Max. -

(1969 Nov)The Index Includes the Largest and Most Liquid Stocks Listed in Hong Kong

Hang Seng Index | Index Constituents Analysis | Thomson Reuters Eikon 15-Aug-2016 08:29 Index Constituents Analysis - (1969 Nov)The index includes the largest and most liquid stocks listed in Hong Kong Report: Index Sector - 10% capping is applied to avoid single stock domination 1 - 50 of 50 - Four sector sub-indexes are also available Sub-indexes: (see table below) Sector Market Cap - Finance; Utility; Properties; Commerce & Industry - represent about 58% of the capitalisation of the Hong Kong Stock Exchange Sector - TRBC USD Percent Financials 1,477,418,432,940.93 61.67 Energy 388,919,496,168.72 6.76 Telecommunications Services 287,167,406,479.74 8.94 Technology 236,946,991,592.06 10.45 Utilities 103,353,908,003.74 6.02 Consumer Cyclicals 55,503,276,570.23 2.48 Industrials 50,240,279,801.09 1.76 Consumer Non-Cyclicals 31,116,477,725.85 1.91 Total -- 100.00% Name RIC Weight % Mcap(USD) Financials 61.67 1,477,418,432,940.93 HSBC Holdings PLC 0005.HK 9.73 140,216,593,956.09 AIA Group Ltd 1299.HK 8.08 76,668,842,578.97 China Construction Bank Corp 0939.HK 6.51 184,114,982,866.54 Industrial and Commercial Bank of China Ltd 1398.HK 4.80 236,531,316,123.03 Bank of China Ltd 3988.HK 3.67 153,437,411,763.61 CK Hutchison Holdings Ltd 0001.HK 3.51 47,648,815,932.83 Hong Kong Exchanges and Clearing Ltd 0388.HK 3.10 30,937,262,168.73 Ping An Insurance Group Co of China Ltd 2318.HK 2.77 92,179,858,049.49 Sun Hung Kai Properties Ltd 0016.HK 2.19 41,545,598,968.05 Cheung Kong Property Holdings Ltd 1113.HK 2.01 27,194,797,037.17 China Life Insurance -

Watsons Experience Launches in Russia Focus Story

103 Watsons Experience Launches in Russia Focus Story Watsons Experience Launches in Russia Watsons is delighted to have opened its first Russian store in St.Petersberg. The launch of Asia’s No.1 health and beauty brand will deliver an unprecedented range of world-class products to the increasingly sophisticated Russian market. This is a country where people take great care over their appearance, and by introducing the products and advanced skincare regimens of Asia, Watsons taps into what it sees as huge market potential. WatsON 103 • Quarter 2 • 2018 01 Focus Story Russia will be the 12th market to host Watsons stores. In every market where it operates, Watsons sets the highest global standards in the health, wellness and beauty market. Putting customers first is what Watsons is all about. It offers customers real value, good service and expert advice – and St.Petersberg this is what Watsons will present to Russian customers. The launch of the first store in Russia is a significant step in the expansion of the Watsons brand. Watsons “cares deeply about its customers around the globe, addressing their health and beauty needs both instore and online. We are dedicated to making our customers Look Good and Feel Great and putting a smile on their faces. Andrei Melnikov ” General Manager Watsons Russia WatsON 103 • Quarter 2 • 2018 02 Focus Story Emerging Market, Golden Opportunity Russian customers are seeking out both new experiences Beauty trends from Asia and especially from Korea and new products in health and beauty. Russian is a – hugely popular across Asia but underdeveloped in Russia magnet for sophisticated travellers from across Europe, Digital and eCommerce solutions, which are well and it has significant potential for future growth. -

About Ck Hutchison Holdings Limited

ABOUT CK HUTCHISON HOLDINGS LIMITED The CK Hutchison Group (the “Group”) is a multinational conglomerate committed to development, innovation and technology in four core businesses: ports and related services, retail, infrastructure, and telecommunications. The Group operates in about 50 countries around the world with over 300,000 employees. Ports and related services Infrastructure As the world’s leading port investor, developer and operator, the The Group’s Infrastructure division includes its shareholding in Group’s Ports division holds interests in 52 ports comprising 283 CK Infrastructure Holdings Limited (“CKI”) and interests in six operational berths in 26 countries, including container terminals infrastructure assets that are co-owned with CKI. CKI is a global operating in six of the 10 busiest container ports in the world. infrastructure company with diversified investments in energy In 2020, the division handled a total throughput of 83.7 million infrastructure, transportation infrastructure, water infrastructure, twenty-foot equivalent units. It also engages in river trade, cruise waste management, waste-to-energy, household infrastructure terminal operations and ports related logistic services. and infrastructure related businesses. Its investments and operations span Hong Kong, Mainland China, the United Kingdom, Retail Continental Europe, Australia, New Zealand, Canada and the The Group’s Retail division is the world’s largest international United States. health and beauty retailer, with over 16,000 stores in 27 markets worldwide. Its diverse retail portfolio comprises health and beauty Telecommunications products, supermarkets, as well as consumer electronics and A pioneer in mobile data communication technologies, the electrical appliances. It also manufactures and distributes bottled Group’s Telecommunications division is a leading global operator water and beverage products in Hong Kong and Mainland China. -

Treatment for (I) Merger Proposal of Ck Hutchison Holdings and Hutchison Whampoaand (Ii) Spin-Off Proposal of Cheung Kong Property Holdings

TECHNICAL NOTICE 4 May 2015 INDEX TREATMENT FOR (I) MERGER PROPOSAL OF CK HUTCHISON HOLDINGS AND HUTCHISON WHAMPOAAND (II) SPIN-OFF PROPOSAL OF CHEUNG KONG PROPERTY HOLDINGS Further to the announcement regarding index adjustments with respect to Cheung Kong (Holdings) and Hutchison Whampoa Reorganisation, dated 13 February 2015, this notice provides details of the index treatments for the merger of CK Hutchison Holdings (SEHK Stock Code: 0001) and Hutchison Whampoa (SEHK Stock Code: 0013) and the spin-off of Cheung Kong Property Holdings. The expected timetable for the merger proposal of CK Hutchison Holdings and Hutchison Whampoa and the spin-off proposal of Cheung Kong Property Holdings is as follows: Date Details 26 May 2015 • Last trading day of Hutchison Whampoa (Tuesday) • Last day of dealing in the shares of CK Hutchison Holdings on a cum-entitlement basis to the distribution in specie of Cheung Kong Property Holdings 27 May 2015 • Dealing in the shares of Hutchison Whampoa on the Stock Exchange of (Wednesday) Hong Kong (SEHK) to cease • First day of dealing in the shares of CK Hutchison Holdings on an ex-entitlement basis to the distribution in specie of Cheung Kong Property Holdings 3 June 2015 • Withdrawal of the listing of the shares of Hutchison Whampoa on the (Wednesday) SEHK • Expected date of commencement of dealing in shares of Cheung Kong Property Holdings on the SEHK more… INDEX TREATMENT FOR (I) MERGER PROPOSAL OF CK HUTCHISON HOLDINGS AND HUTCHISON WHAMPOAAND (II) SPIN-OFF PROPOSAL OF CHEUNG KONG PROPERTY HOLDINGS/2 Accordingly, expected index adjustments in the Hang Seng Family of Indexes (including the Hang Seng Index) are as follows: Effective Date of Details Adjustments 27 May 2015 • Hutchison Whampoa will be removed from all relevant indexes*. -

CK Hutchison Holdings Limited (CKHH) Facts and Figures

CK Hutchison Holdings Limited (CKHH) Facts and Figures. The company. CK Hutchison Holdings Limited (CKHH) is not only one of the largest companies that are listed at the Hong Kong stock exchange, it is also one of the oldest trade companies in Hong Kong – its roots go back to the year 1820. The various business sectors and around 290,000 employees in over 50 countries make the conglomerate one of the world´s leading companies. Business sectors. HWL operates in 5 core businesses: Ports and related services. Hutchison Port Holdings runs all the company‘s ports and related services in 25 countries. Currently, HPH holds a share of 269 berths in 48 ports. Retail. AS Watson is the largest international health and beauty retailer in Asia and Europe and runs more than 13,300 retail stores in 22 countries worldwide, counting more than 130,000 employees. In Hong Kong and on the Chinese mainland, AS Watson is responsible for the production, distribution and bottling of different mineral waters and other drinks. In Europe, the Group operates a number of health & beauty retail brands, chains - Drogas, including Kruidvat, Superdrug, Rossmann, Savers, Trekpleister, Spektr and Watsons. In addition, it also owns two luxury perfumeries and cosmetics retail brands ICI PARIS XL and The Perfume Shop. Infrastructure. The company operates in Hong Kong, the Chinese mainland, Great Britain, the Netherlands, Portugal, Australia, New Zealand and Canada. Its core fields are energy infrastructure, water infrastructure, transportation infrastructure, waste management and aircraft leasing. Energy. HWL holds about 40,2 % of Canadian Husky Energy, an energy-related company listed on the Toronto Stock Exchange. -

Templeton Foreign Fund Fact Sheet

International Templeton Foreign Fund June 30, 2021 Fund Fact Sheet | Share Class: Advisor Fund Description Performance The fund seeks long-term capital growth by investing Growth of a $10,000 Investment (from 10/05/1982-06/30/2021) at least 80% of its net assets in foreign securities, that $387,500 Templeton Foreign Fund are predominantly equity securities of companies - Advisor Class: located outside of the U.S., including developing $310,000 $364,460 markets. $232,500 Fund Overview $155,000 Total Net Assets [All Share Classes] $3,790 million $77,500 Fund Inception Date 10/5/1982 $0 Dividend Frequency Annually in December 10/82 06/92 02/02 10/11 06/21 Number of Issuers 71 Share Class Information Total Returns % (as of 6/30/2021) NASDAQ CUMULATIVE AVERAGE ANNUAL Share Class CUSIP Symbol Since Inception Advisor 880 196 506 TFFAX Share Class YTD 1 Yr 3 Yrs 5 Yrs 10 Yrs Inception Date A 880 196 209 TEMFX Advisor 10.84 35.92 3.25 6.84 3.65 9.73 10/5/1982 C 880 196 407 TEFTX Calendar Year Total Returns % R 880 196 803 TEFRX R6 880 196 878 FTFGX Share Class 2020 2019 2018 2017 2016 2015 2014 2013 2012 2011 Advisor -0.35 12.96 -15.00 17.57 11.99 -6.93 -10.55 27.32 18.89 -12.57 Fund Management 2010 2009 2008 2007 2006 2005 2004 2003 2002 2001 Years with Years of Advisor 8.87 50.18 -45.98 17.56 20.14 10.94 18.37 30.87 -8.42 -7.68 Firm Experience Christopher James Peel, 13 13 Performance data represents past performance, which does not guarantee future results. -

Eligible Assets and Credit-To-Asset Ratio for Secured Credit

Eligible Assets and Credit-to-asset Ratio for Secured Credit Effective from 30 Sep 2021 List of Eligible Assets (Excluding Stocks) Asset Types Credit-to-asset Ratio HKD Time Deposits 100% Foreign Currency Time or Saving Deposits 85% Deposit Plus 70% Structured Investment Deposits (Including Capital Protected Investment Deposits) 70% Unit Trusts*/Bonds*#/Certificates of Deposit/Equity Link Notes/Equity Link Investment with Product Risk Level 1 70% Product Risk Level 2 70% Product Risk Level 3 50% Product Risk Level 4 30% Product Risk Level 5 – *exclude the Non-eligible Products listed below. #For new bonds issued on or after 17 Mar 2020, the timeline for assignment of Credit -to-asset Ratio for Secured Credit Facility will be revised follow: for new bonds issued between 1 Jan to 30 Jun each year, Credit-to-asset Ratio will be assigned in Sep of the same year (where applicable); for new bonds issued between 1 Jul to 31 Dec, Credit-to-asset Ratio will be assigned in Mar of next year (where applicable); Please refer to the relevant bond term sheet or the bond details in our website for the issue date of the relevant bond. Gold 0% (Credit-to-asset Ratio for Gold (Wayfoong Statement Gold) is removed from 20 Dec 2019) List of Non-eligible Products (Capital in Nature Instruments and Other TLAC-eligible Instruments, Hedge Funds, Liquid Alternative Funds are not eligible) Product Type Bond / Fund Code Bond / Fund Name Bonds US404280AN99 HSBC HOLDINGS PLC 4% USD BOND 3/30/2022 Bonds US404280AL34 HSBC HOLDINGS PLC 4.875% USD BOND 1/14/2022 Bonds -

STOXX Hong Kong All Shares 180 Last Updated: 01.08.2017

STOXX Hong Kong All Shares 180 Last Updated: 01.08.2017 Rank Rank (PREVIOU ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) S) HK0000069689 B4TX8S1 1299.HK HK1013 AIA GROUP HK HKD Y 80.6 1 1 CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 60.5 2 2 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 50.8 3 3 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 41.3 4 4 CNE1000003X6 B01FLR7 2318.HK CN0076 PING AN INSUR GP CO. OF CN 'H' CN HKD Y 32.0 5 7 CNE1000001Z5 B154564 3988.HK CN0032 BANK OF CHINA 'H' CN HKD Y 31.8 6 5 KYG217651051 BW9P816 0001.HK 619027 CK HUTCHISON HOLDINGS HK HKD Y 31.1 7 6 HK0388045442 6267359 0388.HK 626735 Hong Kong Exchanges & Clearing HK HKD Y 28.0 8 8 HK0016000132 6859927 0016.HK 685992 Sun Hung Kai Properties Ltd. HK HKD Y 20.6 9 10 HK0002007356 6097017 0002.HK 619091 CLP Holdings Ltd. HK HKD Y 20.0 10 9 CNE1000002L3 6718976 2628.HK CN0043 China Life Insurance Co 'H' CN HKD Y 20.0 11 11 KYG2103F1019 BWX52N2 1113.HK HK50CI CK Property Holdings HK HKD Y 18.3 12 12 CNE1000002Q2 6291819 0386.HK CN0098 China Petroleum & Chemical 'H' CN HKD Y 16.4 13 13 HK0823032773 B0PB4M7 0823.HK B0PB4M Link Real Estate Investment Tr HK HKD Y 15.4 14 16 HK0883013259 B00G0S5 0883.HK 617994 CNOOC Ltd.