STOXX Hong Kong All Shares 50 Last Updated: 02.10.2017

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

MKS/EQD/07/21 日期 Date: 01/02/2021

編號 Ref. No.: MKS/EQD/07/21 日期 Date: 01/02/2021 香港聯合交易所有限公司 (香港交易及結算所有限公司全資附屬公司) THE STOCK EXCHANGE OF HONG KONG LIMITED (A wholly-owned subsidiary of Hong Kong Exchanges and Clearing Limited) 通告 CIRCULAR Subject: Introduction of New Stock Option Class on Kuaishou Technology Enquiry: Mr. Wallace Chan (Tel: 2211-6139 E-mail: [email protected]) The Stock Exchange of Hong Kong Limited (the “Exchange”) is pleased to announce that stock option class on Kuaishou Technology (“KST”) will commence trading on Friday, 5 February 2021 (“Commencement Date”), subject to the successful listing of KST: Expiry Months Contract Min. No. of Trading Underlying Stock HKATS Tier Available Size Fluctuation Board Tariff (Stock Code) Code Level on the (shares) (HK$) Lots (HK$) Commence ment Date Feb 21, Mar 21, Apr 21, Kuaishou Technology May 21, KST 500 $0.01 5 1 $3 (1024) Jun 21, Sep 21 & Dec 21 The list of stock option classes available for trading is set forth in Attachment I. For details of the contract specifications, please refer to Appendix B of the Operational Trading Procedures for Options Trading Exchange Participants (“Options Contract Specifications”). Strike Price In order to offer more choices for investors, 28 strikes above and below HK$115 (which is the offer price of the underlying stock) will be available for trading on the Commencement Date (see Attachment II). New strike prices subsequent to the Commencement Date will be introduced according to the Operational Trading Procedures for Options Trading Exchange Participants. 2 Position Limit The position limit for KST options contracts will be 50,000 open contracts in any one market direction for all expiry months combined. -

Shanghai Municipal Commission of Commerce Belt and Road Countries Investment Index Report 2018 1 Foreword

Shanghai Municipal Commission of Commerce Belt and Road Countries Investment Index Report 2018 1 Foreword 2018 marked the fifth year since International Import Exposition Municipal Commission of Commerce, President Xi Jinping first put forward (CIIE), China has deepened its ties releasing the Belt and Road Country the Belt and Road Initiative (BRI). The with partners about the globe in Investment Index Report series Initiative has transformed from a trade and economic development. to provide a rigorous framework strategic vision into practical action President Xi Jinping has reiterated at for evaluating the attractiveness during these remarkable five years. these events that countries should of investing in each BRI country. enhance cooperation to jointly build Based on extensive data collection There have been an increasing a community of common destiny and in-depth analysis, we evaluated number of participating countries for all mankind , and the Belt and BRI countries' (including key and expanding global cooperation Road Initiative is critical to realizing African nations) macroeconomic under the BRI framework, along with this grand vision. It will take joint attractiveness and risks, and identified China's growing global influence. By efforts and mutual understanding to key industries with high growth the end of 2018, China had signed overcome the challenges ahead. potential, to help Chinese enterprises BRI cooperation agreements with better understand each jurisdiction's 122 countries and 29 international Chinese investors face risks in the investment environment. organizations. According to the Big BRI countries, most of which are Data Report of the Belt and Road developing nations with relatively The Belt and Road Country (2018) published by the National underdeveloped transportation and Investment Index Report 2017 Information Center, public opinion telecommunication infrastructures. -

CK HUTCHISON HOLDINGS LIMITED (“CK Hutchison”) And

HUTCHISON WHAMPOA INTERNATIONAL (03/33) LIMITED (the “Issuer”) US$1,500,000,000 7.45% Guaranteed Notes due 2033 (the “Notes”) (ISIN: US44841SAC35/CUSIP: 44841SAC3/Common Code: 018124572 for Rule 144A Notes) (ISIN: USG4672CAC94/CUSIP: G4672CAC9/Common Code: 018124629 for Regulation S Notes) unconditionally and irrevocably guaranteed by CK HUTCHISON HOLDINGS LIMITED (“CK Hutchison”) and HUTCHISON WHAMPOA LIMITED In accordance with Regulation (EU) No. 596/2014 on market abuse and the law of 11 January 2008 on transparency requirements, as amended, the Issuer is filing with the Commission de Surveillance du Secteur Financier, storing with the Officially Appointed Mechanism and publishing the attached unaudited results for the six months ended 30 June 2019 of CK Hutchison, a guarantor of the Notes issued by the Issuer. The attached document was also published by CK Hutchison at 4:31 pm and 4:32 pm (Hong Kong time), 1 August 2019 on the websites of Hong Kong Exchanges and Clearing Limited and CK Hutchison, respectively. Hutchison Whampoa International (03/33) Limited Edith Shih Director and Company Secretary 1 August 2019 Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this document, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this document. UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 30 JUNE 2019 HIGHLIGHTS -

Hang Lung Properties Wait with Patience

30 May 2018 Hong Kong EQUITIES Hang Lung Properties 101 HK Neutral Wait with patience Price (at 06:50, 30 May 2018 GMT) HK$17.96 Valuation HK$ 33.32 Key points - DCF (WACC 7.7%, beta 1.1, ERP 6.0%, RFR 1.5%) Acquired a land king in Hangzhou with good growth potential 12-month target HK$ 18.43 Large cost leads to slim yield, and long investment period impacts NAV Upside/Downside % +2.6 12-month TSR % +6.8 Benefit from strong retail sales but renovations temporarily hurt Volatility Index Low GICS sector Real Estate Event Market cap HK$m 80,779 We believe the acquisition of the new land king gives the company a good Market cap US$m 10,296 opportunity to ride on the strong retail growth and development of a quasi tier- Free float % 42 1 city. We believe the Hangzhou mall can charge the highest unit rental at 30-day avg turnover US$m 7.8 Rmb700 psm/mth among Hang Lung’s mainland shopping malls except for Number shares on issue m 4,498 Shanghai projects, which are charging more than Rmb1,500. However, as it will take six years to complete in 2024 and total investment cost could be as Investment fundamentals high as Rmb19bn with a 4-5% gross yield, the acquisition should negatively Year end 31 Dec 2017A 2018E 2019E 2020E impact the earnings, cash flow and NAV in recent years. Some previous Revenue m 11,199 10,721 11,107 9,449 EBIT m 7,330 7,452 7,704 6,020 projects have had a long development cycle for five to nine years and EBIT growth % -11.8 1.7 3.4 -21.9 experienced disappointing rentals. -

Hang Lung Properties Version 9 | Bloomberg: 101 HK EQUITY | Reuters: 101.HK Refer to Important Disclosures at the End of This Report

China / Hong Kong Company Guide Hang Lung Properties Version 9 | Bloomberg: 101 HK EQUITY | Reuters: 101.HK Refer to important disclosures at the end of this report DBS Group Research . Equity 31 Jul 2019 BUY Retail sales growth gathering Last Traded Price ( 30 Jul 2019):HK$18.64 (HSI : 28,147) momentum Price Target 12-mth: HK$22.38 (20.1% upside) (Prev HK$20.35) BUY with HK$22.38 TP. The stock is trading at a 49% discount to Analyst our estimated current NAV and offers an attractive dividend yield Jeff YAU CFA, +852 36684180 [email protected] of 4.0% for FY19. Stellar tenants’ sales growth at its retail malls in Ian CHUI +852 36684174 [email protected] Jason LAM +852 36684179 [email protected] China augurs well for reversionary growth. Portfolio expansion and asset enhancement initiatives should provide additional What’s New momentum to drive rental income, offering better earnings quality • Improving retail tenants’ sales to underpin and in turn providing share price upside. HLP is among our preferred landlords. BUY with HK$22.38 TP. reversionary growth Portfolio expansion to lift rental income. The progressive opening • New properties to spice up rental earnings of new properties in Kunming, Wuhan, Wuxi, and Shenyang in • BUY with HK$22.38 TP 2019-20 should give an additional boost to Hang Lung Properties’ recurrent earnings growth, and its ability to raise dividends. Pre- leasing at Spring City 66 in Kunming is progressing smoothly, with Price Relative 88% of retail space already pre-committed. This mall is scheduled to open for business in late Aug. -

Stock Code Stock Name Margin Category HK 1 CK HUTCHISON HOLDINGS LTD

UOB KAY HIAN (SINGAPORE) PRIVATE LIMITED MARGIN STOCK LIST - HONG KONG MARKET 1 April 2021 Stock Code Stock Name Margin Category HK 1 CK HUTCHISON HOLDINGS LTD. SA HK 2 CLP HOLDINGS LTD. A HK 3 HONG KONG AND CHINA GAS CO. LTD. A HK 4 WHARF (HOLDINGS) LTD. A HK 5 HSBC HOLDINGS PLC SA HK 6 POWER ASSETS HOLDINGS LTD. SA HK 8 PCCW LTD. C HK 10 HANG LUNG GROUP LTD. A HK 11 HANG SENG BANK LTD. SA HK 12 HENDERSON LAND DEVELOPMENT CO. LTD. A HK 14 HYSAN DEVELOPMENT CO. LTD. B HK 16 SUN HUNG KAI PROPERTIES LTD. SA HK 17 NEW WORLD DEVELOPMENT CO. LTD. A HK 19 SWIRE PACIFIC LTD. 'A' A HK 23 BANK OF EAST ASIA, LTD. A HK 27 GALAXY ENTERTAINMENT GROUP LTD. A HK 38 FIRST TRACTOR CO LTD. - H SHARES D HK 41 GREAT EAGLE HOLDINGS LTD. C (Max Net Loan H$10M) HK 45 HONGKONG AND SHANGHAI HOTELS, LTD. B (Max Net Loan H$10M) HK 53 GUOCO GROUP LTD. B (Max Net Loan H$10M) HK 56 ALLIED PROPERTIES (HK) LTD. D HK 62 TRANSPORT INTERNATIONAL HOLDINGS LTD. D (Max Net Loan H$1M) HK 66 MTR CORPORATION LTD. SA HK 69 SHANGRI-LA ASIA LTD. A HK 81 CHINA OVERSEAS GRAND OCEANS GROUP LTD. C HK 83 SINO LAND CO. LTD. A HK 86 SUN HUNG KAI & CO. LTD. D HK 87 SWIRE PACIFIC LTD. 'B' A (Max Net Loan H$10m) HK 101 HANG LUNG PROPERTIES LTD. A HK 107 SICHUAN EXPRESSWAY CO. -

3I Group PLC 3M Co 58.Com Inc A2A Spa AAC Technologies Holdings

3i Group PLC 3M Co 58.com Inc A2A SpA AAC Technologies Holdings Inc ABB Ltd Abbott Laboratories AbbVie Inc Accenture PLC Accton Technology Corp ACS Actividades de Construccio Activision Blizzard Inc Acuity Brands Inc Adani Ports & Special Economic Adaro Energy Tbk PT Adecco Group AG Adelaide Brighton Ltd adidas AG Adient PLC Adobe Systems Inc Advance Auto Parts Inc Advanced Ceramic X Corp Advanced Micro Devices Inc Advanced Semiconductor Enginee Aegon NV AES Corp/VA Aetna Inc Affiliated Managers Group Inc Aflac Inc Aga Khan Fund for Economic Dev AGFA-Gevaert NV Agilent Technologies Inc AGL Energy Ltd Agnaten SE AIA Group Ltd Air Products & Chemicals Inc AirAsia Bhd Airtac International Group Akamai Technologies Inc Akbank Turk AS Akzo Nobel NV Alaska Air Group Inc Albemarle Corp Alcoa Corp Alexandria Real Estate Equitie Alexion Pharmaceuticals Inc Alibaba Group Holding Ltd Align Technology Inc ALK-Abello A/S Allegion PLC Allergan PLC Alliance Data Systems Corp Alliant Energy Corp Allianz SE Allstate Corp/The Ally Financial Inc Alphabet Inc ALS Ltd Altaba Inc/Fund Family Altice NV Altran Technologies SA Altria Group Inc Alumina Ltd Amadeus IT Group SA Amazon.com Inc Amcor Ltd/Australia Ameren Corp America Movil SAB de CV American Airlines Group Inc American Axle & Manufacturing American Electric Power Co Inc American Express Co American International Group I American Tower Corp American Water Works Co Inc Ameriprise Financial Inc AmerisourceBergen Corp AMETEK Inc Amgen Inc Amorepacific Corp AMOREPACIFIC Group AMP Ltd Amphenol Corp ams AG -

STOXX Hong Kong All Shares 50 Last Updated: 01.12.2016

STOXX Hong Kong All Shares 50 Last Updated: 01.12.2016 Rank Rank (PREVIOUS ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) ) KYG875721634 BMMV2K8 0700.HK B01CT3 Tencent Holdings Ltd. CN HKD Y 128.4 1 1 HK0000069689 B4TX8S1 1299.HK HK1013 AIA GROUP HK HKD Y 69.3 2 2 CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 60.3 3 4 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 57.5 4 3 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 37.7 5 5 CNE1000001Z5 B154564 3988.HK CN0032 BANK OF CHINA 'H' CN HKD Y 32.6 6 7 KYG217651051 BW9P816 0001.HK 619027 CK HUTCHISON HOLDINGS HK HKD Y 32.0 7 6 HK0388045442 6267359 0388.HK 626735 Hong Kong Exchanges & Clearing HK HKD Y 28.5 8 8 CNE1000003X6 B01FLR7 2318.HK CN0076 PING AN INSUR GP CO. OF CN 'H' CN HKD Y 26.5 9 9 CNE1000002L3 6718976 2628.HK CN0043 China Life Insurance Co 'H' CN HKD Y 20.4 10 15 HK0016000132 6859927 0016.HK 685992 Sun Hung Kai Properties Ltd. HK HKD Y 19.4 11 10 HK0883013259 B00G0S5 0883.HK 617994 CNOOC Ltd. CN HKD Y 18.9 12 12 HK0002007356 6097017 0002.HK 619091 CLP Holdings Ltd. HK HKD Y 18.3 13 13 KYG2103F1019 BWX52N2 1113.HK HK50CI CK Property Holdings HK HKD Y 17.9 14 11 CNE1000002Q2 6291819 0386.HK CN0098 China Petroleum & Chemical 'H' CN HKD Y 16.8 15 14 HK0688002218 6192150 0688.HK 619215 China Overseas Land & Investme CN HKD Y 14.8 16 16 HK0823032773 B0PB4M7 0823.HK B0PB4M Link Real Estate Investment Tr HK HKD Y 14.6 17 17 CNE1000003W8 6226576 0857.HK CN0065 PetroChina Co Ltd 'H' CN HKD Y 13.5 18 19 HK0003000038 6436557 0003.HK 643655 Hong Kong & China Gas Co. -

The Trade War and China's Oil and Gas Supply Security

HIGH ANXIETY: THE TRADE WAR AND CHINA’S OIL AND GAS SUPPLY SECURITY BY ERICA DOWNS NOVEMBER 2019 “If Oil Supplies Are Cut Off, How Much Oil Does China Have?” —Cover of the June 15, 2019, issue of China Petroleum & Petrochemical1 “Is China’s Oil Supply Still Secure?” —Cover of the August 15, 2018, issue of China Petroleum & Petrochemical2 Introduction In summer 2018, China’s president Xi Jinping, facing pressure from the US-China trade war, intervened in a long-running debate within China’s oil industry about the extent to which national security concerns or market forces should determine domestic oil and natural gas production. Xi effectively tipped the scales in favor of advocates of prioritizing self-sufficiency over cost as part of a broader push for self-reliance amidst trade tensions. As a result, China’s national oil companies (NOCs) are accelerating investment in domestic exploration and production. While this ramp-up in spending is likely to result in an increase in output, especially of natural gas, it is unlikely to alter China’s substantial and growing reliance on oil and natural gas imports. However, the trade war probably will continue to contribute to shifts in the composition of China’s import portfolio, with both traditional and new suppliers gaining shares as a result of the slowdown in the flows of US liquified natural gas (LNG) and crude oil to China and decreases in deliveries of Iranian and Venezuelan crudes due to US sanctions. Xi instructed China’s NOCs to ramp up domestic exploration and production of oil and natural gas to enhance national energy security in July 2018. -

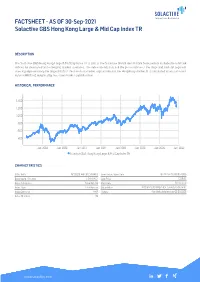

FACTSHEET - AS of 30-Sep-2021 Solactive GBS Hong Kong Large & Mid Cap Index TR

FACTSHEET - AS OF 30-Sep-2021 Solactive GBS Hong Kong Large & Mid Cap Index TR DESCRIPTION The Solactive GBS Hong Kong Large & Mid Cap Index TR is part of the Solactive Global Benchmark Series which includes benchmark indices for developed and emerging market countries. The index intends to track the performance of the large and mid cap segment covering approximately the largest 85% of the free-float market capitalization in the Hong Kong market. It is calculated as a totalreturn index in HKD and weighted by free-float market capitalization. HISTORICAL PERFORMANCE 1,400 1,200 1,000 800 600 400 Jan-2008 Jan-2010 Jan-2012 Jan-2014 Jan-2016 Jan-2018 Jan-2020 Jan-2022 Solactive GBS Hong Kong Large & Mid Cap Index TR CHARACTERISTICS ISIN / WKN DE000SLA4H36 / SLA4H3 Base Value / Base Date 462.12 Points / 08.05.2006 Bloomberg / Reuters / .SHKLMCT Last Price 1256.93 Index Calculator Solactive AG Dividends Reinvested Index Type Total Return Calculation 8:00 am to 10:30 pm (CET), every 15 seconds Index Currency HKD History Available daily back to 08.05.2006 Index Members 52 FACTSHEET - AS OF 30-Sep-2021 Solactive GBS Hong Kong Large & Mid Cap Index TR STATISTICS 30D 90D 180D 360D YTD Since Inception Performance -6.80% -10.27% -11.73% 9.67% -4.51% 171.99% Performance (p.a.) - - - - - 6.71% Volatility (p.a.) 21.54% 18.63% 16.63% 17.91% 18.51% 20.09% High 1364.34 1419.58 1482.24 1493.61 1493.61 1493.61 Low 1228.29 1228.29 1228.29 1115.51 1228.29 287.41 Sharpe Ratio -2.67 -1.91 -1.34 0.55 -0.32 0.33 Max. -

中國中車股份有限公司 Crrc Corporation Limited

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt as to any aspect of this circular or as to the action to be taken, you should 14A.69(4) consult your licensed dealer in securities, bank manager, solicitor, professional accountant or other professional adviser. If you have sold or transferred all your shares in CRRC Corporation Limited (the “Company”), you should at once hand this circular and the enclosed New Proxy Form to the purchaser or the transferee or to the bank, licensed dealer in securities or other agent through whom the sale or transfer was effected for transmission to the purchaser or the transferee. Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no 14A.70(1) 13.52 Note 5 responsibility for the contents of this circular, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. 中國中車股份有限公司 CRRC CORPORATION LIMITED (a joint stock limited company incorporated in the People’s Republic of China with limited liability) 13.28(1) 13.51A (Stock code: 1766) A1B1 (1) PROPOSED ISSUANCE AND PLACING OF NEW A SHARES; (2) CONNECTED TRANSACTION: PROPOSED SUBSCRIPTION OF NEW A SHARES BY CRRC GROUP; AND (3) SUPPLEMENTAL NOTICE OF 2015 ANNUAL GENERAL MEETING Independent Financial Adviser to the Independent Board Committee and the Independent Shareholders A supplemental notice of the AGM of the Company, which will be held as originally scheduled at Empark Grand Hotel, No. -

The Mineral Industry of China in 2016

2016 Minerals Yearbook CHINA [ADVANCE RELEASE] U.S. Department of the Interior December 2018 U.S. Geological Survey The Mineral Industry of China By Sean Xun In China, unprecedented economic growth since the late of the country’s total nonagricultural employment. In 2016, 20th century had resulted in large increases in the country’s the total investment in fixed assets (excluding that by rural production of and demand for mineral commodities. These households; see reference at the end of the paragraph for a changes were dominating factors in the development of the detailed definition) was $8.78 trillion, of which $2.72 trillion global mineral industry during the past two decades. In more was invested in the manufacturing sector and $149 billion was recent years, owing to the country’s economic slowdown invested in the mining sector (National Bureau of Statistics of and to stricter environmental regulations in place by the China, 2017b, sec. 3–1, 3–3, 3–6, 4–5, 10–6). Government since late 2012, the mineral industry in China had In 2016, the foreign direct investment (FDI) actually used faced some challenges, such as underutilization of production in China was $126 billion, which was the same as in 2015. capacity, slow demand growth, and low profitability. To In 2016, about 0.08% of the FDI was directed to the mining address these challenges, the Government had implemented sector compared with 0.2% in 2015, and 27% was directed to policies of capacity control (to restrict the addition of new the manufacturing sector compared with 31% in 2015.