(18 August 2015).Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Transportation Systems 2018 – 2020

Transportation Systems 2018 – 2020 DE | EN | FR Liebherr-Transportation Systems News from the Company | p. 12 - 31 Locations Partners in Rapid Development | p. 20 The Liebherr Group Insights | p. 38 ff. From left to right: Holger Dörre, Adrian Gunis, Stefan Pachowsky, Dirk Junghans Dear reader, In the face of growing environmental awareness worldwide plus, for the first time, series-ready cold vapor systems using and the increasing changes in mobility, it seems likely that the CO2 as the refrigerant. transport of passengers and freight by rail will continue to play a significant role as part of the overall transportation systems of The outlook for our Hydraulics division is also very positive. the future. However, the demands made in terms of reliability, In this sector, Liebherr has been able to expand its product efficiency and environmental compatibility are also increasing portfolio considerably once again, including dampers for level in parallel. The rail system must therefore be continuously regulation systems. In addition, we are also working within the further developed and made fit for purpose for the future so framework of a research project with partners in the UK on that it can survive in the long term as part of an integrated the development of a system for the active radial suspension. transportation network. The aim of this project is to considerably reduce wear on rails and wheels. Liebherr-Transportation Systems is ready to face the associ- ated challenges, and is consistently pushing forward with the We have also further expanded our customer service activities, development of innovative technologies and products with a and not only in the well developed markets of Europe and North high customer benefit in all product areas. -

中國中鐵股份有限公司 CHINA RAILWAY GROUP LIMITED (A Joint Stock Limited Company Incorporated in the People’S Republic of China with Limited Liability) (Stock Code: 390)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. 中國中鐵股份有限公司 CHINA RAILWAY GROUP LIMITED (A joint stock limited company incorporated in the People’s Republic of China with limited liability) (Stock Code: 390) This overseas regulatory announcement is made pursuant to Rule 13.10B of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited. Please refer to the attached “Announcement of China Railway Group Limited on Winning of Bids for Material Projects” published by China Railway Group Limited on the Shanghai Stock Exchange website on 2 January 2018 for your information. By Order of the Board China Railway Group Limited LI Changjin Chairman 2 January 2018 As at the date of this announcement, the executive directors of the Company are LI Changjin (Chairman), ZHANG Zongyan, ZHOU Mengbo and ZHANG Xian; the independent non- executive directors are GUO Peizhang, WEN Baoman, ZHENG Qingzhi and CHUNG Shui Ming Timpson; and the non-executive director is MA Zonglin. A Shares Stock Name: China Railway A Shares Stock Code: 601390 Announcement No.: H Shares Stock Name: China Railway H Shares Stock Code: 00390 Lin 2018-002 Announcement of China Railway Group Limited on Winning of Bids for Material Projects The board of directors of China Railway Group Limited (the “Company”) and all the directors hereby undertake that this announcement does not have any false or misleading statements or any material omissions, and assume the joint and several liabilities for the truthfulness, accuracy and completeness of the contents. -

Global Report Global Metro Projects 2020.Qxp

Table of Contents 1.1 Global Metrorail industry 2.2.2 Brazil 2.3.4.2 Changchun Urban Rail Transit 1.1.1 Overview 2.2.2.1 Belo Horizonte Metro 2.3.4.3 Chengdu Metro 1.1.2 Network and Station 2.2.2.2 Brasília Metro 2.3.4.4 Guangzhou Metro Development 2.2.2.3 Cariri Metro 2.3.4.5 Hefei Metro 1.1.3 Ridership 2.2.2.4 Fortaleza Rapid Transit Project 2.3.4.6 Hong Kong Mass Railway Transit 1.1.3 Rolling stock 2.2.2.5 Porto Alegre Metro 2.3.4.7 Jinan Metro 1.1.4 Signalling 2.2.2.6 Recife Metro 2.3.4.8 Nanchang Metro 1.1.5 Power and Tracks 2.2.2.7 Rio de Janeiro Metro 2.3.4.9 Nanjing Metro 1.1.6 Fare systems 2.2.2.8 Salvador Metro 2.3.4.10 Ningbo Rail Transit 1.1.7 Funding and financing 2.2.2.9 São Paulo Metro 2.3.4.11 Shanghai Metro 1.1.8 Project delivery models 2.3.4.12 Shenzhen Metro 1.1.9 Key trends and developments 2.2.3 Chile 2.3.4.13 Suzhou Metro 2.2.3.1 Santiago Metro 2.3.4.14 Ürümqi Metro 1.2 Opportunities and Outlook 2.2.3.2 Valparaiso Metro 2.3.4.15 Wuhan Metro 1.2.1 Growth drivers 1.2.2 Network expansion by 2025 2.2.4 Colombia 2.3.5 India 1.2.3 Network expansion by 2030 2.2.4.1 Barranquilla Metro 2.3.5.1 Agra Metro 1.2.4 Network expansion beyond 2.2.4.2 Bogotá Metro 2.3.5.2 Ahmedabad-Gandhinagar Metro 2030 2.2.4.3 Medellín Metro 2.3.5.3 Bengaluru Metro 1.2.5 Rolling stock procurement and 2.3.5.4 Bhopal Metro refurbishment 2.2.5 Dominican Republic 2.3.5.5 Chennai Metro 1.2.6 Fare system upgrades and 2.2.5.1 Santo Domingo Metro 2.3.5.6 Hyderabad Metro Rail innovation 2.3.5.7 Jaipur Metro Rail 1.2.7 Signalling technology 2.2.6 Ecuador -

Annual Report Contents

2012 Annual Report Contents Corporate Information 2 Chairman of the Board’s Report 3 Business Overview 5 Management Discussion and Analysis 23 Corporate Governance Report 38 Report of Directors 44 Biographical Details of Directors and Senior Management 55 Independent Auditor’s Report 59 Consolidated Statement of Comprehensive Income 61 Consolidated Statement of Financial Position 62 Consolidated Statement of Changes in Equity 64 Consolidated Statement of Cash Flows 65 Notes to the Consolidated Financial Statements 67 Financial Summary 144 Annual Report 2012 1 Corporate Information REGISTERED OFFICE AUTHORISED REPRESENTATIVES Cricket Square, Hutchins Drive Dr. Chen Yuhong P. O. Box 2681 Mr. Fok Ming Fuk, William, MBA, FCCA, FCPA Grand Cayman, KY1-1111 CHARTERED ACCOUNTANT, FTIHK, CTA Cayman Islands INTERNATIONAL AUDITOR HEAD OFFICE AND PRINCIPAL Deloitte Touche Tohmatsu PLACE OF BUSINESS IN THE PRC North Wing 12/F, PRINCIPAL SHARE REGISTRAR Raycon Infotech Park Tower C, AND TRANSFER OFFICE No. 2 Kexuiyuan Nanlu, Haidian District, Royal Bank of Canada Trust Company (Cayman) Limited Beijing, 100190, PRC 4th Floor, Royal Bank House 24 Shedden Road, George Town PRINCIPAL PLACE OF BUSINESS IN Grand Cayman, KY1-1110 HONG KONG Cayman Islands Units 4607-8, 46th Floor, COSCO Tower HONG KONG SHARE REGISTRAR AND No.183 Queen’s Road Central TRANSFER OFFICE Hong Kong Computershare Hong Kong Investor Services Limited 46th Floor, Hopewell Centre WEBSITE 183 Queen’s Road East www.chinasofti.com Wanchai Hong Kong COMPANY SECRETARY Mr. Fok Ming Fuk, William, MBA, FCCA, FCPA PRINCIPAL BANKERS CHARTERED ACCOUNTANT, FTIHK, CTA Bank of China Haidian sub-branch COMPLIANCE OFFICER No. 58 Beisihuan West Road Dr. -

Construction & Building Materials

Sector Research | China Construction & Building Materials THIS IS THE TRANSLATION OF A REPORT ORIGINALLY PUBLISHED IN CHINESE BY GUOSEN SECURITIES CO., LTD ON September 7, 2012 September 7, 2012 Construction & Building Materials Another railway construction boom could emerge in China Event: Analysts Qiu Bo This week, China approved 30 urban railway transit projects by a number of local +86 755 82133390 [email protected] governments, intercity railway plans by Jiangsu and Inner Mongolia, feasibility study S0980510120021 reports on 13 subway lines in several cities, including Chengdu, Tianjin, Changchun, etc, Liu Ping +86 755 82130678 the No.1 subway line franchise project in Hangzhou and the second Gantang-Southern [email protected] Weiwu railway line project. S0980512030001 Comment: Sales Contact Another massive railway transit construction boom may occur as the number of Dan Weil Global Head of Institutional Sales and Trading projects approved this time hit a three-year high. Managing Director +852 2248 3588 [email protected] The construction of a subway project usually lasts four years. Therefore, the Chris Berney construction of projects in seven cities approved in 2009 is drawing to an end, and it Managing Director is necessary to launch a new batch of projects to improve urban construction. On the +852 2248 3568 [email protected] other hand, we believe the NDRC’s latest move is also an important measure the government takes to stabilise economic growth. Roger Chiman Managing Director +852 2248 3598 [email protected] The investment in the 30 railway transit projects totals RMB427.8 billion and most of these projects are scheduled to be completed over 2012-15. -

International Society for Soil Mechanics and Geotechnical Engineering

INTERNATIONAL SOCIETY FOR SOIL MECHANICS AND GEOTECHNICAL ENGINEERING This paper was downloaded from the Online Library of the International Society for Soil Mechanics and Geotechnical Engineering (ISSMGE). The library is available here: https://www.issmge.org/publications/online-library This is an open-access database that archives thousands of papers published under the Auspices of the ISSMGE and maintained by the Innovation and Development Committee of ISSMGE. Geotechnical Aspects of Underground Construction in Soft Ground – Yoo, Park, Kim & Ban (Eds) © 2014 Korean Geotechnical Society, Seoul, Korea, ISBN 978-1-138-02700-8 Shield tunneling analysis and measures under elevated high-speed railway Gong Quanmei, Shan Yao,You Xiaoming & Zhou Shunhua Department of Urban Rail Transit and Railway Engineering, Tongji University, Shanghai, China Key Laboratory of Road and Traffic Engineering of the Ministry of Education, Tongji University, Shanghai, China ABSTRACT: With the development of rail transit in China more and more shield tunnels have to be constructed under or nearby high-speed railway lines in metropolis. As a result two principal problems arise: (1) since requirements of the running safety of high-speed trains and criteria of the riding comfort of passengers are quite strict, it is difficult to construct shield tunnels beneath high-speed railway lines, and (2) the influence of the load of railway lines on the tunnel construction should be considered. Consequently, treatments of the railway foundation are usually implemented during the tunnel construction to protect the high-speed railway line. In order to determine whether the treatments are actually necessary, numerical simulations based on two real construction cases are taken to evaluate the interactive influence. -

中國中車股份有限公司crrc Corporation Limited

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. 中國中車股份有限公司 CRRC CORPORATION LIMITED (a joint stock limited company incorporated in the People’s Republic of China with limited liability) (Stock code: 1766) OVERSEAS REGULATORY ANNOUNCEMENT ANNOUNCEMENT IN RELATION TO SIGNING CONTRACTS This overseas regulatory announcement is made pursuant to Rule 13.10B of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited. CRRC Corporation Limited (the “Company”) has entered into certain contracts for the period from September 2020 to November 2020 with an aggregate value of approximately RMB37.2 billion. Details of such contracts are set out below: 1. Certain subsidiaries of the Company engaged in the MUs business have entered into contracts with relevant railway administration companies of China State Railway Group Co., Ltd. (中國國家鐵路集團有限公司) respectively in relation to the sales of MUs with an aggregate value of approximately RMB22.53 billion. 2. CRRC Changchun Railway Vehicle Co., Ltd. (中車長春軌道客車股份有限公 司), a non-wholly-owned subsidiary of the Company, has entered into contracts with Chongqing Rail Transit (Group) Co., Ltd. (重慶市軌道交通(集團)有限公 司), Shenzhen Metro Group Co., Ltd. (深圳市地鐵集團有限公司), Changchun Rail Transit Group Co., Ltd. (長春市軌道交通集團有限公司), Changchun Metro Co., Ltd. (長春市地鐵有限責任公司) and China Civil Engineering Construction- Columbia Bogotá Western Railway Concession Co., Ltd. -

Rail Transit

Japanese Geotechnical Society Special Publication The 15th Asian Regional Conference on Soil Mechanics and Geotechnical Engineering Practices in the design of excavation engineering for Ningbo rail transit Ye Junnengi) i) Ningbo urban rail transit project construction headquarters, Zhejiang Ningbo, P. R. china ABSTRACT Ningbo is located in the southeast coast plain. There are thick, soft soil deposits lying in the sub-ground, which challenges the construction of urban rail transit in this area. A project of Ningbo Rail Transit Line 1 and the soil conditions for the construction site are firstly presented. Then, the excavation engineering designs for the project are summarized from four aspects: the design of building envelope, vertical and horizontal layout of supporting system, underground water dewatering and ground treatment. Simultaneously, the problems occurred in the design are also described. Lastly, the experiences gained from the project are summed up, so as to guide the further subway construction in the area and also provide a reference for the construction of similar project.. Keywords: rail transit; excavation engineering; soft soil; dewatering; ground treatment. 1 INTRODUCTION strata. For about 80m along the depth of the ground, the soil layer contains clay, silt and sand, as shown in Tab.1. In complex urban environments, the construction of The stratigraphic distribution for soil layers is complex. rail transit has negative impact on the nearby buildings and underground pipelines (Liu 2009). There are a lot Tab.1 Typical soil conditions for the proposed site of challenges on the construction of Ningbo rail transit project as marine sedimentary soft soil, which has Soil layer Soil property ① characteristics of high clay content, high water content, 1 miscellaneous fill ① high compressibility, low permeability and high 2 clay ① sensitivity, is widely distributed with uneven thickness 3 mucky silty clay ② in this area. -

Rail Transit

Rail Transit Contents Xi’an Urban Rail Transit Network Analysis ..................................................................................................5 The Calculation of Bus Topological Structure High Speed Railway Lines’Capacity ......................6 Analysis of the Characteristics and Robustness of Metro Network Based on User Demand ....7 Identification of Important Nodes on Urban Based on CRITIC Method ...........................................8 Rail Transit Network Service Spatial Dynamics: Insights from Multiyear AFC Data ......................9 Multi-Objective Planning Method for Layout of Suburban Railway Stations .............................. 10 Discussion About the Multi-Line Corridor in Guangzhou Urban Railway Planning .................. 11 Quantitative Analysis of Operation Optimization Measure for Beijing Metro Line 13 ............. 12 Comparison and Selection of Operation Plan of Sunset-Departure and Sunrise-Arrival Train by Grey Correlation Analysis and TOPSIS Method ............................................................................... 13 Study on Pedestrian Traffic Organization of Railway Passenger Transport Hub-Taking Xi’an North Station as an Example ........................................................................................................................ 14 Study on the Capacity of High-Speed Rail Passenger Hub-Taking Haxi Station as an Example ............................................................................................................................................................................... -

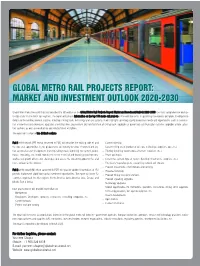

Global Report Global Metro Projects 2020.Qxp

GLOBALGLOBAL METROMETRO RAILRAIL PROJECTSPROJECTS REPORT:REPORT: MARKETMARKET ANDAND INVESTMENTINVESTMENT OUTLOOKOUTLOOK 2020-20302020-2030 Global Mass Transit Research has just launched the fifth edition of the Global Metro Rail Projects Report: Market and Investment Outlook 2020-22030, the most comprehensive and up- to-date study on the metro rail segment. The report will provide information on the top 150 metro rail projects in the world in terms of upcoming investments and plans. It will provide details on the existing network, stations, ridership, rolling stock, technology and fare systems. It will highlight upcoming capital investment needs and opportunities such as construc- tion of new lines and extensions, upgrades of existing lines, procurement and refurbishment of rolling stock, upgrades of power and communication systems, upgrades of fare collec- tion systems, as well as construction and refurbishment of stations. The report will comprise two distinct sections. Part 1 of the report (PPT format converted to PDF) will describe the existing state of, and - Current ridership the expected opportunities in, the global metro rail industry in terms of network and sta- - Current rolling stock (number of rail cars, technology, suppliers, age, etc.) tion construction and development, ridership, rolling stock, signalling, fare system, power, - Existing signalling system (type of system, suppliers, etc.) tracks, consulting, etc. It will examine the recent technical and financing developments; - Power and tracks analyse key growth drivers and challenges; and assess the upcoming opportunities and - Current fare system (type of system, ticketing infrastructure, suppliers, etc.) future outlook for the industry. - Extensions/ Capital projects - upcoming network and stations - Planned investments, cost estimates and funding Part 2 of the report (MS Word converted to PDF) will provide updated information on 150 - Projected ridership projects that present significant capital investment opportunities. -

Table of Contents

Advances in Civil and Industrial Engineering IV ISBN(softcover): 978-3-03835-165-8 ISBN(eBook): 978-3-03826-548-1 Table of Contents Preface and Conference Organiztaion Chapter 1: Geotechnical Engineering 3D Finite Element Analysis on Behaviour of Piled Raft Foundations A. Vu, D. Pham, T. Nguyen and Y. He 3 A Modified Method to Fit Probability Distributions of Geotechnical Parameters Using Stochastic Weighted Entropy Principle S.J. Zhang, Z.J. Xu, L. Zhong and Z.R. Xiao 9 A Research on Elastoplastic Theory Based on Full State Function Z.H. Wei, M.S. Wang and D.L. Zhang 17 Affect of Large Deep Foundation Pit Dewatering on the Neighboring Buildings K.W. Ding, F. Zhao and X.Z. Zhang 24 Analysis of Monitoring Results of a Deep Foundation Pit with Pile-Anchor Retaining Structure X.H. Yang, F.W. Wu, T. Chen and X. Liu 28 Analysis on Strengthening of Plant to Slope Soil under Orthogonal States J.B. Gu 34 Centrifuge Model Study of High Strength Piles Composite Foundation Settlement & Instability under Embankment in Different Kind Soils by Different Pile Spacing Q.J. Wang, S.J. Zhang, C. Guo and Z.R. Lu 38 Comparative Experimental Research of Soil Freezing with Pressure and Non-Pressure S.Y. Zhang 48 Discussion on Treatment Technology of Reinforcement Pile in Karst Area C.B. Zheng and J. Xu 52 Effect of Variable Permeability Coefficient on Consolidation of Ultra-Soft Ground under Vacuum Preloading B.B. Xu, A.H. Liang and M.Y. Li 56 Experimental Application of Fractal Theory into Selection of Subgrade Filling Materials X.G. -

Table of Contents

TABLE OF CONTENTS WELCOME 02 COMMITTEE MEMBERS 06 GENERAL INFORMATION 09 - Conference Venue 09 - Registration 09 - On-site Registration Rate 09 - Conference Information Booth 10 - Conference Proceedings 10 - Oral Presentation 10 - Poster Session 10 - Exhibition 10 - Catering 10 - Bank 11 - Mobile Phone 11 - Duplication and Recording 11 - Emergencies 11 - Wi-Fi Network 11 - Conference Hall 12 CONFERENCE AGENDA 15 SOCIAL PROGRAM 17 - Welcome Reception 17 - Banquet Dinner 17 - Post-Conference Technical Visit 17 - Urban Thinkers Campus 18 TECHNICAL PROGRAM 19 KEYNOTE LECTURES 31 SHORT COURSES 34 TRANSPORTATION & ACCOMMODATION 35 - Transportation 35 - Weather Forecast 37 - Accommodation 37 PLATINUM SPONSOR 38 CONTACT INFORMATION 39 www.euus2019.com WELCOME Dear Colleagues and Friends, We take great pleasure in inviting you to the 1st International Conference on Exploration and Utilization of Underground Space (EUUS2019), held on 15–18 November 2019, at the Hongshan Hotel, Wuhan, China. From the perspective of humankind building development history, the 19th century was marked by bridge building and its development, and the 20th century was dominated by a rapid growth in ground buildings. As predicted in the Tokyo Declaration by the Associated Research Centers for Urban Underground Space (ACUUS) in 1991, the 21st century, however, is marked as the development and utilization of the underground space. In the past 30 years, underground engineering has been developing greatly and is characterized as a large scale, deeper stratum, complex environment and extensive fields. Acquiring space and resources and security from underground are the common demand during the modernization development of all countries and regions in the world. Therefore, the efficient development and sustainable utilization of underground space has become an international issue.