Full Ownership Equity Stakes Vehicle Assembly Alliances

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

OSB Representative Participant List by Industry

OSB Representative Participant List by Industry Aerospace • KAWASAKI • VOLVO • CATERPILLAR • ADVANCED COATING • KEDDEG COMPANY • XI'AN AIRCRAFT INDUSTRY • CHINA FAW GROUP TECHNOLOGIES GROUP • KOREAN AIRLINES • CHINA INTERNATIONAL Agriculture • AIRBUS MARINE CONTAINERS • L3 COMMUNICATIONS • AIRCELLE • AGRICOLA FORNACE • CHRYSLER • LOCKHEED MARTIN • ALLIANT TECHSYSTEMS • CARGILL • COMMERCIAL VEHICLE • M7 AEROSPACE GROUP • AVICHINA • E. RITTER & COMPANY • • MESSIER-BUGATTI- CONTINENTAL AIRLINES • BAE SYSTEMS • EXOPLAST DOWTY • CONTINENTAL • BE AEROSPACE • MITSUBISHI HEAVY • JOHN DEERE AUTOMOTIVE INDUSTRIES • • BELL HELICOPTER • MAUI PINEAPPLE CONTINENTAL • NASA COMPANY AUTOMOTIVE SYSTEMS • BOMBARDIER • • NGC INTEGRATED • USDA COOPER-STANDARD • CAE SYSTEMS AUTOMOTIVE Automotive • • CORNING • CESSNA AIRCRAFT NORTHROP GRUMMAN • AGCO • COMPANY • PRECISION CASTPARTS COSMA INDUSTRIAL DO • COBHAM CORP. • ALLIED SPECIALTY BRASIL • VEHICLES • CRP INDUSTRIES • COMAC RAYTHEON • AMSTED INDUSTRIES • • CUMMINS • DANAHER RAYTHEON E-SYSTEMS • ANHUI JIANGHUAI • • DAF TRUCKS • DASSAULT AVIATION RAYTHEON MISSLE AUTOMOBILE SYSTEMS COMPANY • • ARVINMERITOR DAIHATSU MOTOR • EATON • RAYTHEON NCS • • ASHOK LEYLAND DAIMLER • EMBRAER • RAYTHEON RMS • • ATC LOGISTICS & DALPHI METAL ESPANA • EUROPEAN AERONAUTIC • ROLLS-ROYCE DEFENCE AND SPACE ELECTRONICS • DANA HOLDING COMPANY • ROTORCRAFT • AUDI CORPORATION • FINMECCANICA ENTERPRISES • • AUTOZONE DANA INDÚSTRIAS • SAAB • FLIR SYSTEMS • • BAE SYSTEMS DELPHI • SMITH'S DETECTION • FUJI • • BECK/ARNLEY DENSO CORPORATION -

Vehicle Identification Number (VIN) Coding Summary (Internal Use Only)

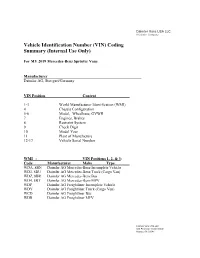

Daimler Vans USA LLC A Daimler Company Vehicle Identification Number (VIN) Coding Summary (Internal Use Only) For MY 2019 Mercedes-Benz Sprinter Vans Manufacturer Daimler AG, Stuttgart/Germany VIN Position Content 1-3 World Manufacturer Identification (WMI) 4 Chassis Configuration 5-6 Model, Wheelbase, GVWR 7 Engines, Brakes 8 Restraint System 9 Check Digit 10 Model Year 11 Plant of Manufacture 12-17 Vehicle Serial Number WMI - VIN Positions 1, 2, & 3: Code Manufacturer Make Type WDA, 8BN Daimler AG Mercedes-Benz Incomplete Vehicle WD3, 8BU Daimler AG Mercedes-Benz Truck (Cargo Van) WDZ, 8BR Daimler AG Mercedes-Benz Bus WD4, 8BT Daimler AG Mercedes-Benz MPV WDP Daimler AG Freightliner Incomplete Vehicle WDY Daimler AG Freightliner Truck (Cargo Van) WCD Daimler AG Freightliner Bus WDR Daimler AG Freightliner MPV Daimler Vans USA LLC 303 Perimeter Center North Atlanta, GA 30346 Daimler Vans USA LLC A Daimler Company Chassis Configuration - VIN Position 4: Code Chassis Configuration / Intended Market P All 4x2 Vehicle Types / U.S. B All 4x2 Vehicle Types / Canada F All 4x4 Vehicle Types / U.S. C All 4x4 Vehicle Types / Canada Model, Wheelbase, GVWR - VIN Positions 5 & 6: Code Model Wheelbase GVWR E7 C1500/C2500/P1500 3665 mm/ 144 in. 8,000 lbs. to 9,000 lbs. Class G E8 C2500/P2500 4325 mm/ 170 in. 8,000 lbs. to 9,000 lbs. Class G F0 C2500/C3500 3665 mm/ 144 in. 9,000 lbs. to 10,000 lbs. Class H F1 C2500/C3500 4325 mm/ 170 in. 9,000 lbs. to 10,000 lbs. Class H F3 C4500/C3500 3665 mm/ 144 in. -

Audi Vs. BMW – on the Physical Heterogeneity of German Luxury Cars

Munich Personal RePEc Archive Audi vs. BMW – On the Physical Heterogeneity of German Luxury Cars Vistesen, Claus Global Economy Matters, Copenhagen Business School 18 December 2009 Online at https://mpra.ub.uni-muenchen.de/19516/ MPRA Paper No. 19516, posted 22 Dec 2009 08:51 UTC Audi vs. BMW – On the Physical Heterogeneity of German Luxury Cars Working Paper 03-09 Claus Vistesen [email protected] and www.clausvistesen.squarespace.com MSc. Applied Economics and Finance Copenhagen Business School JEL: L62 Key words: luxury cars, BMW, Audi, pure characteristics demand models Database can be obtained by contacting the author through the e-mail above 1 Audi vs BMW – On the Physcial Heterogenity of German Luxury Cars Claus Vistesen Abstract This paper uses Logit and Probit regressions to test for and quantify the physical heterogeneity between German luxury cars. Using a matched sample database, the binary response variable consisting of Audis and BMWs is fitted to a matrix of physical characteristics such as power, torque, fuel consumption, engine displacement etc. The results indicate that having a forced induction engine (e.g. turbo) is associated with a 51% lower probability of observing a BMW and that increasing fuel consumption by 1 liter per 100km lowers the probability of observing a BMW with 61%. The results are discussed in relation to the idea that consumers may not differentiate across luxury products on the basis of physical characteristics and how this may introduce a bias with respect to predicting demand in the context of available market data. 1.0 Introduction The idea that you can take some of the most arcane tools of the economist’s toolbox and apply them directly to the unstable and complex reality of the real world remain a difficult aspiration in most contexts. -

BMW M Motorsport Presents the New BMW M4 GT3.Pdf

BMW Corporate Communications For Release: Immediate Contacts: Bill Cobb BMW of North America Motorsport Press Officer 215-431-7223 (cell) / [email protected] Oleg Satanovsky BMW of North America Product and Technology Spokesperson 201-414-8694 (cell) / [email protected] Thomas Plucinsky BMW of North America Motorsport Communications 201-406-4801 (cell) / [email protected] BMW M Motorsport presents the new BMW M4 GT3 • Newest addition to BMW Motorsport’s Customer Racing program. • Based on new M4 Competition Coupe. • Eligible for 2022 IMSA WeatherTech GTD and SRO GT Classes • $530,000 excluding shipping. • Competition Package available for $55,000. Woodcliff Lake, N.J. – June 2, 2021…BMW Motorsport is proud to announce the new state-of-the-art BMW M4 GT3 customer race car based on the recently launched 2021 M4 Competition Coupe. Powering the new Coupe is the P58 3.0-liter inline-6-cylinder M TwinPower Turbo engine producing up to 590 hp. The BMW M4 GT3 will retail for $530,000 in the US (excl. shipping). The Competition Package adds $55,000 and includes additional headlights, backlit door numbers, TPMS with 8 sensors, spring and brake pedal travel measurement systems, BOSCH CAS-M rear-view camera radar system, an additional set of rims, and one day of training on the BMW M Motorsport M4 GT3 simulator. In North America, the BMW M4 GT3 will be eligible to compete in the GT Daytona and GT Daytona Pro classes of the IMSA WeatherTech SportsCar Championship, as BMW Corporate Communications well as the GT class of the SRO Fanatec GT World Challenge America powered by AWS and SRO GT America powered by AWS series. -

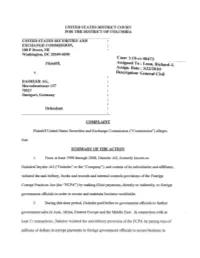

Daimler AG, Formerly Known As

UNITED STATES DISTRICT COURT FOR THE DISTRICT OF COLUMBIA UNITED STATES SECURITIES AND EXCHANGE COMMISSION, 100 F Street,NE Washington, DC 20549-6030 Case: 1:10-cv-00473 Plaintiff, Ass~gned To : Leon, RichardJ-.- ASSIgn. Date: 3/22/2010 v. Description: General Civil DAIMLERAG, .Mercedesstrasse 137 70327 . Stuttgart, Germany Defendant. COMPLAINT PlaintiffUnited States Securities and Exchange Commission ("Commission") alleges that: SUMMARY OF THE ACTION 1. From at least 1998 through 2008, Daimler AG, formerly knoWn as DaimlerChrysler AG ("Daimler" or the "Company"), and certain ofits subsidiaries and affiliates, violated the anti-bribery, books and records and internal controls provisions ofthe Foreign _ Corrupt Practices Act (the "FCPA") by making illicit payments, directly or indirectly, to foreign government officials in order to secure and maintain business worldWide. 2. During this time period, Daimler paid bribes to government officials to further government sales in Asia, Africa, Eastern Europe and the Middle East. In connection With at least 51 transactions, Daimler violated the anti-bribery provision of the FCPA by paying tens of millions of dollars in corrupt payments to foreign government officials to secure business in · Russia,Chilia,Vietnam, Nigeria, Hungary, Latvia, Croatia and Bosnia. These corrupt payments were made through the use ofU.S. mails or the means or instrumentality ofU.S. interstate commerce. 3. Daimler also violated the FCPA's books and records and internal controls provisions in connection with the 51 transactions and at least an additional 154 transactions, in which it made improper payments totaling atleast $56 million to secure business in 22 countries, including, among others, Russia, China, Nigeria, Vietnam, Egypt, Greece, Hungary, North Korea, andIndonesia. -

Separate Financial Statements Fiscal Year 2019

201Separate financial9 statements PPorscheorsche TaycanTaycan TurboTurbo S 3 Content Group management report and management report of Porsche Automobil Holding SE 6 Fundamental information about the group 10 Report on economic position 12 Significant events and developments at the Porsche SE Group 12 Significant events and developments at the Volkswagen Group 20 Business development 24 Results of operations, financial position and net assets 31 Porsche Automobil Holding SE (financial statements pursuant to the German Commercial Code) 37 Sustainable value enhancement in the Porsche SE Group 41 Overall statement on the economic situation of Porsche SE and the Porsche SE Group 43 Remuneration report 44 Opportunities and risks of future development 52 Publication of the declaration of compliance and corporate governance report 78 Subsequent events 79 Forecast report and outlook 80 Glossary 85 4 Financials 86 Balance sheet of Porsche Automobil Holding SE 90 Income statement of Porsche Automobil Holding SE 91 Notes to the consolidated fi nancial statements 92 Independent auditor’s report 212 Responsibility statement 220 5 VVolkswagenolkswagen IID.3D.3 6 1 Group management report and management report of Porsche Automobil Holding SE 7 8 Group management report and management report of Porsche Automobil Holding SE 6 Fundamental information about the group 10 Report on economic position 12 Significant events and developments at the Porsche SE Group 12 Significant events and developments at the Volkswagen Group 20 Business development 24 Results -

Baltic Rim Economies

Baltic Rim Economies Estonia - Latvia - Lithuania - Poland - Baltic Russia Bimonthly Review ISSUE NO. 5, 31 OCTOBER 2008 ECONOMIC REVIEWS: ESTONIA Page 1 LATVIA Page 2 LITHUANIA Page 3 POLAND Page 4 ST. PETERSBURG Page 5 LENINGRAD REGION Page 6 KALININGRAD REGION Page 7 EXPERT ARTICLES: José Manuel Durão Barroso: EU Strategy for the Baltic Sea Region Page 8 Paula Lehtomäki : Cleaner, safer and brighter future of the Baltic Sea Page 9 Jaak Aaviksoo: Events in Georgia provoke discussions on security in good, old, peaceful Europe Page 10 Siiri Oviir: Gas pipeline to the Baltic Sea – should it come in a civilized way or under the dictate of the big and the powerful? Page 12 Artis Pabriks: Baltic security reflections in the aftermath of the Russian-Georgian conflict Page 13 Efthimios E. Mitropoulos: Busy Baltic to benefit from global pollution measures Page 14 Jari Luoto: EU focuses on the Baltic Sea Page 15 André Mernier: A role for the Energy Charter in a new Russia-EU Partnership Agreement Page 16 Timo Rajala: Finland is facing major energy decisions Page 18 Karlis Mikelsons: Environmentally friendly for sustainable growth Page 19 Reinier Zwitserloot: Nord Stream – making more European energy solidarity possible Page 20 Viktoras Valentukevicius: Current and future activities of Lietuvos Dujos AB Page 21 Seppo Remes: Russian gas can unite Europe – if we allow it Page 22 Aleksandra Mierzyńska and Krzysztof Parkoła: PGNiG – trying to be one step further Page 24 Tapio Reponen: Profiling as a key success factor in modern university strategies Page 25 EXPERT ARTICLES CONTINUED ON NEXT PAGE To receive a free copy, print or register at www.tse.fi/pei Baltic Rim Economies ISSUE NO. -

CHINA FIELD TRIP May 10Th –12Th, 2011

CHINA FIELD TRIP May 10th –12th, 2011 This presentation may contain forward-looking statements. Such forward-looking statements do not constitute forecasts regarding the Company’s results or any other performance indicator, but rather trends or targets, as the case may be. These statements are by their nature subject to risks and uncertainties as described in the Company’s annual report available on its Internet website (www.psa-peugeot-citroen.com). These statements do not reflect future performance of the Company, which may materially differ. The Company does not undertake to provide updates of these statements. More comprehensive information about PSA PEUGEOT CITROËN may be obtained on its Internet website (www.psa-peugeot-citroen.com), under Regulated Information. th th China Field Trip - May 10 –12 , 2011 2 PSA in Asia – Market Forecast, PSA in China: ongoing successes and upsides Frédéric Saint-Geours Executive VP, Finance and Strategic Development Grégoire Olivier, Executive VP, Asia Table of contents Introduction China: the new auto superpower China: a global economic power The world’s largest automotive market The growth story is set to continue PSA in China China: a second home market for PSA 2 complementary JVs Key challenges in China and PSA differentiation factors A sustainable profitable growth Extending the Chinese Success ASEAN strategy Capturing the Indian opportunity th th China Field Trip - May 10 –12 , 2011 4 PSA – a global automotive player (1/2) > 39% of PSA’s 2010 sales are realized outside of Europe, of -

France Toutes Les Voitures Particulières Du Groupe

ANALYSE DE PRESSE DE 14H00 30/08/2018 FRANCE TOUTES LES VOITURES PARTICULIÈRES DU GROUPE PSA HOMOLOGUÉES EN WLTP Toutes les voitures particulières Peugeot, Citroën, DS, Opel et Vauxhall sont aujourd’hui homologués selon le protocole WLTP, plus représentatif de la consommation de carburant en usage réel. Grâce à des choix technologiques judicieux réalisés par anticipation de la réglementation – SCR « Selective Catalytic Reduction » et GPF « Filtre à particules essence », le Groupe PSA est ainsi à l’avant-garde de la mise en œuvre des normes les plus strictes. « Nos choix technologiques pour traiter les émissions polluantes, comme la SCR lancée en 2013 sur tous nos moteurs diesel, et plus récemment le GPF sur les moteurs essence à injection directe, nous permettent de proposer à nos clients des véhicules respectueux de l’environnement et de maintenir notre leadership en matière de réduction des émissions », explique Gilles Le Borgne, directeur de la qualité et de l’ingénierie du Groupe PSA. La prochaine étape concernera la norme Euro-6.d-Temp, qui sera applicable à partir de septembre 2019. Cette dernière prendra également en compte les émissions polluantes (NOx, PN) mesurées en conditions de conduite réelles sur routes ouvertes ou RDE (Real Driving Emissions). Source : COMMUNIQUE DE PRESSE GROUPE PSA (29/8/18) Par Alexandra Frutos ALLEMAGNE BMW S’EST ASSOCIÉ À LUFTHANSA POUR PROMOUVOIR LA VISION INEXT Le constructeur allemand BMW s’est associé à la compagnie aérienne Lufthansa pour promouvoir la Vision iNext, sa voiture hautement automatisée et 100 % électrique. BMW a en effet organisé une tournée sur 5 jour pour présenter la Vision iNext en Europe, aux Etats- Unis et en Chine. -

Analysis of the Dynamic Relationship Between the Emergence Of

Annals of Business Administrative Science 8 (2009) 21–42 Online ISSN 1347-4456 Print ISSN 1347-4464 Available at www.gbrc.jp ©2009 Global Business Research Center Analysis of the Dynamic Relationship between the Emergence of Independent Chinese Automobile Manufacturers and International Technology Transfer in China’s Auto Industry Zejian LI Manufacturing Management Research Center Faculty of Economics, the University of Tokyo E-mail: [email protected] Abstract: This paper examines the relationship between the emergence of independent Chinese automobile manufacturers (ICAMs) and International Technology Transfer. Many scholars indicate that the use of outside supplies is the sole reason for the high-speed growth of ICAMs. However, it is necessary to outline the reasons and factors that might contribute to the process at the company-level. This paper is based on the organizational view. It examines and clarifies the internal dynamics of the ICAMs from a historical perspective. The paper explores the role that international technology transfer has played in the emergence of ICAMs. In conclusion, it is clear that due to direct or indirect spillover from joint ventures, ICAMs were able to autonomously construct the necessary core competitive abilities. Keywords: marketing, international business, multinational corporations (MNCs), technology transfer, Chinese automobile industry but progressive emergence of independent Chinese 1. Introduction automobile manufacturers (ICAMs). It will also The purpose of this study is to investigate -

Chapter 2 China's Cars and Parts

Chapter 2 China’s cars and parts: development of an industry and strategic focus on Europe Peter Pawlicki and Siqi Luo 1. Introduction Initially, Chinese investments – across all industries in Europe – especially acquisitions of European companies were discussed in a relatively negative way. Politicians, trade unionists and workers, as well as industry representatives feared the sell-off and the subsequent rapid drainage of industrial capabilities – both manufacturing and R&D expertise – and with this a loss of jobs. However, with time, coverage of Chinese investments has changed due to good experiences with the new investors, as well as the sheer number of investments. Europe saw the first major wave of Chinese investments right after the financial crisis in 2008–2009 driven by the low share prices of European companies and general economic decline. However, Chinese investments worldwide as well as in Europe have not declined since, but have been growing and their strategic character strengthening. Chinese investors acquiring European companies are neither new nor exceptional anymore and acquired companies have already gained some experience with Chinese investors. The European automotive industry remains one of the most important investment targets for Chinese companies. As in Europe the automotive industry in China is one of the major pillars of its industry and its recent industrial upgrading dynamics. Many of China’s central industrial policy strategies – Sino-foreign joint ventures and trading market for technologies – have been established with the aim of developing an indigenous car industry with Chinese car OEMs. These instruments have also been transferred to other industries, such as telecommunications equipment. -

Download PDF, 19 Pages, 505.25 KB

VOLKSWAGEN AKTIENGESELLSCHAFT Shareholdings of Volkswagen AG and the Volkswagen Group in accordance with sections 285 and 313 of the HGB and presentation of the companies included in Volkswagen's consolidated financial statements in accordance with IFRS 12 as of 31.12.2019 Exchange rate VW AG 's interest Equity Profit/loss (1€ =) in capital in % in thousands, in thousands, Name and domicile of company Currency Dec. 31, 2019 Direct Indirect Total local currency local currency Footnote Year I. PARENT COMPANY VOLKSWAGEN AG, Wolfsburg II. SUBSIDIARIES A. Consolidated companies 1. Germany ASB Autohaus Berlin GmbH, Berlin EUR - 100.00 100.00 16,272 1,415 2018 AUDI AG, Ingolstadt EUR 99.64 - 99.64 13,701,699 - 1) 2019 Audi Berlin GmbH, Berlin EUR - 100.00 100.00 9,971 - 1) 2018 Audi Electronics Venture GmbH, Gaimersheim EUR - 100.00 100.00 60,968 - 1) 2019 Audi Frankfurt GmbH, Frankfurt am Main EUR - 100.00 100.00 8,477 - 1) 2018 Audi Hamburg GmbH, Hamburg EUR - 100.00 100.00 13,425 - 1) 2018 Audi Hannover GmbH, Hanover EUR - 100.00 100.00 16,621 - 1) 2018 AUDI Immobilien GmbH & Co. KG, Ingolstadt EUR - 100.00 100.00 82,470 3,399 2019 AUDI Immobilien Verwaltung GmbH, Ingolstadt EUR - 100.00 100.00 114,355 1,553 2019 Audi Leipzig GmbH, Leipzig EUR - 100.00 100.00 9,525 - 1) 2018 Audi München GmbH, Munich EUR - 100.00 100.00 270 - 1) 2018 Audi Real Estate GmbH, Ingolstadt EUR - 100.00 100.00 9,859 4,073 2019 Audi Sport GmbH, Neckarsulm EUR - 100.00 100.00 100 - 1) 2019 Audi Stuttgart GmbH, Stuttgart EUR - 100.00 100.00 6,677 - 1) 2018 Auto & Service PIA GmbH, Munich EUR - 100.00 100.00 19,895 - 1) 2018 Autonomous Intelligent Driving GmbH, Munich EUR - 100.00 100.00 250 - 1) 2018 Autostadt GmbH, Wolfsburg EUR 100.00 - 100.00 50 - 1) 2018 B.