Transbay Joint Powers Authority

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SAN FRANCISCO 2Nd Quarter 2014 Office Market Report

SAN FRANCISCO 2nd Quarter 2014 Office Market Report Historical Asking Rental Rates (Direct, FSG) SF MARKET OVERVIEW $60.00 $57.00 $55.00 $53.50 $52.50 $53.00 $52.00 $50.50 $52.00 Prepared by Kathryn Driver, Market Researcher $49.00 $49.00 $50.00 $50.00 $47.50 $48.50 $48.50 $47.00 $46.00 $44.50 $43.00 Approaching the second half of 2014, the job market in San Francisco is $40.00 continuing to grow. With over 465,000 city residents employed, the San $30.00 Francisco unemployment rate dropped to 4.4%, the lowest the county has witnessed since 2008 and the third-lowest in California. The two counties with $20.00 lower unemployment rates are neighboring San Mateo and Marin counties, $10.00 a mark of the success of the region. The technology sector has been and continues to be a large contributor to this success, accounting for 30% of job $0.00 growth since 2010 and accounting for over 1.5 million sf of leased office space Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 2012 2012 2012 2013 2013 2013 2013 2014 2014 this quarter. Class A Class B Pre-leasing large blocks of space remains a prime option for large tech Historical Vacancy Rates companies looking to grow within the city. Three of the top 5 deals involved 16.0% pre-leasing, including Salesforce who took over half of the Transbay Tower 14.0% (delivering Q1 2017) with a 713,727 sf lease. Other pre-leases included two 12.0% full buildings: LinkedIn signed a deal for all 450,000 sf at 222 2nd Street as well 10.0% as Splunk, who grabbed all 182,000 sf at 270 Brannan Street. -

Residential Development Pipeline

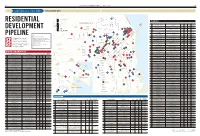

36 SAN FRANCISCO BUSINESS TIMES JUNE 26, 2015 37 SAN FRANCISCO STRUCTURES SPECIAL REPORT Columbus Ave. The Embarcadero 52 SPONSORED BY Broadway Pacific Ave. Kearny St. PLANNED Stockton St. RESIDENTIAL Jackson St. Powell St. Montgomery St. SAN FRANCISCO Polk St. 80 Project name, address Developer Done Units Sale/ Market/ Sacramento St. rental affordable NP 1654 Sunnydale Ave. Mercy Housing California, Related Cos. 2018+ 1,700 both both 34 40 78 106 DEVELOPMENT 14 Pine St. 77 Potrero Terrace, 1095 Connecticut St. Bridge Housing Corp. 2018 1,400- both both California St. Bush St. 60 7 85 71 58 Sutter St. Spear St. 1,700 79 8 1 Main St. Mission Rock, Seawall Lot 227 and SWL 337 Associates LLC (S.F. Giants) 2017+ 1,500 TBD both Gough St. 112 35 80 5 Beale St. 72 Laguna St. 113 Webster St. Pier 48 38 Fremont St. Steiner St. Geary Blvd. 90 33 Pier 70 residential Forest City 2029 1,000- both both Divisadero St. 55 48 73 KEY 95 118 107 10 2,000 PIPELINE 2nd St. NP: Not placed; outside map area 96 Market St. 103 Van Ness Ave. 64 Ellis St. 62 61 74 700 Innes St. Build Inc. 2020 980 rent market Market: A majority of units are market rate, 29 94 1st St. Residential projects in 75 10 S. Van Ness Ave. Crescent Heights 2018+ 767 TBD market though almost all projects include some affordable Geary Blvd. Mission St. 97 San Francisco of 60 units units to comply with city regulations Turk St. 102 76 5M at Fifth and Mission Streets Forest City / Hearst Corp. -

San Francisco Ethics Commission Disclosure Report for Permit

DocuSign Envelope ID: 22F915A2-4A57-4DCD-ABD1-3562213B15D9 San Francisco Ethics Commission 25 Van Ness Avenue, Suite 220, San Francisco, CA 94102 Received on: Phone: 415.252.3100 . Fax: 415.252.3112 04-14-2020\DateSigned | 16:28:46\ PDT [email protected] . www.sfethics.org \DateSigned\ Disclosure Report for Permit Consultants SFEC Form 3410B (S.F. Campaign and Governmental Conduct Code § 3.400A et seq.) A Public Document 1. FILING INFORMATION TYPE OF FILING DATE OF ORIGINAL FILING (for amendment only) \OriginalFilingType\ \OriginalFilingDate\ PERIOD COVERED \PeriodMonths\ \PeriodYear\ January 1 to March 31 2020 2. PERMIT CONSULTANT AND EMPLOYER INFORMATION NAME OF PERMIT CONSULTANT NAME OF EMPLOYER Kyle Thompson \PermitConsultantName\ A.R.\PermitConsultantEmployer Sanchez-Corea & \Associates, Inc. BUSINESS ADDRESS 301 Junipero Serra Blvd., Suite 270, San Francisco, CA 94127 \PermitConsultantAddress\ BUSINESS TELEPHONE BUSINESS EMAIL ADDRESS 415-333-8080 [email protected] \PermitConsultantTelephone\ \PermitConsultantEmail\ 3. CLIENT INFORMATION Enter the name, business address, contact person (if applicable), e-mail address, and business telephone number of each client for whom you performed permit consulting services during the reporting period. Also enter the amount of compensation you or your employer received or expected to receive from each client for permit consulting services during the reporting period. # CLIENT INFORMATION NAME OF CLIENT One De Haro, LLC c/o SKS Investments \ClientName1\ BUSINESS ADDRESS OF CLIENT 601 -

Transbay Transit Center

Transbay Transit Center TRANSBAY JOINT POWERS AUTHORITY FREQUENTLY ASKED QUESTIONS Transbay Transit Center Why do we need the Transbay Transit Center? It is time for public infrastructure to meet the needs of the 21st century. The project will centralize a fractured regional transportation network—making transit connections be- tween all points in the Bay Area fast and convenient. The new Transit Center will make public transit a convenient option as it is in other world-class cities, allowing people to travel and commute without the need for a car, thereby decreasing congestion and pollution. The Transit Center will provide a downtown hub in the heart of a new transit- friendly neighborhood with new homes, parks and shops, providing access to public transit literally at the foot of people’s doors. When will I be able to use the Transit Center? The Transit Center building will be completed in 2017 and will be a bustling transit and retail center for those who live, work and visit the heart of downtown San Francisco. When will I be able to take Caltrain into the new Transit Center? The construction of the underground rail extension for the Caltrain rail line and future High Speed Rail is planned to begin in 2012. It is estimated to be completed and operational, along with the Transit Center’s underground rail station, in 2018 or sooner if funding becomes What is the Transbay Transit available. Center Project? How many people will use it? When the rail component is complete, it is estimated that The Transbay Transit Center Project is a visionary more than 20 million people will use the Transit Center transportation and housing project that will transform annually. -

Sports and Concert Facilities / Special Events Golden State Warriors Event Center and Mixed-Use Development SEIR, San Francisco, CA

EDUCATION Mr. Mitchell has provided project management and technical analysis capabilities for a wide variety of projects requiring environmental review, B.S., Civil Engineering, San including transportation and transit, industrial, institutional, commercial, Francisco State residential, mixed-use, educational and recreational projects. He has served University as project director / project manager for a number of CEQA environmental 23 YEARS documents, including environmental review for sports facilities and sporting EXPERIENCE events, capital improvement projects, wineries and vineyards, quarries, university and local school district master plans, specific plans, planned use developments, transit service plans, multi-modal stations, and demolition projects. Mr. Mitchell’s technical analysis responsibilities include required CEQA/NEPA analysis of transportation, air quality, noise, land use and policies, and infrastructure issues. Sports and Concert Facilities / Special Events Golden State Warriors Event Center and Mixed-Use Development SEIR, San Francisco, CA. Project Manager. Paul recently managed a Subsequent EIR for a landmark $1 billion, privately funded development within the thriving Mission Bay neighborhood in San Francisco. The centerpiece is an 18,000-plus–seat event center that will be the new home of the Golden State Warriors basketball team, during the NBA season, and provide a year-round venue for a variety of other uses, including concerts, family shows, other sporting events, cultural events, conferences and conventions. Office, retail, and open space uses and structured parking are also proposed. A Subsequent EIR (SEIR) was prepared for the project, tiering from the 1998 Mission Bay Final SEIR. The project was processed under CEQA streamlining legislation of both AB 900 (“environmental leadership project”) and SB 743. -

Ronald Hamburger

The Millennium Tower Settlement, Tilting and Upgrade University of Kansas Ronald O. Hamburger, S.E., SECB March 5, 2020 • Constructed 2005-2009 • 58 stories, 645 ft (197m) tall • Tallest & most expensive residential tower in San Francisco • Views from the Sierra to the Cascades to the Farallon Islands • Most expensive unit sold in 2013 for $13.5 million • Construction Cost - $600 Million Sales Cost - $750 Million 2 301 Mission The Site 350 Mission Transbay terminal and track tube 2012 2009 200 Beale 2017 Salesforce Tower 3 2014 History of the Problem • Ground breaking – 2005 – Settlement predicted 4”-6” • Construction completed 2009 – Settlement reached 10” – Transbay Terminal excavation starts • Last unit sold in 2013 – Settlement 13” • SGH retained in 2014 – Settlement 15” • Litigation initiated in 2016 – Settlement 17” • Adjacent construction complete 2017 – Settlement 18”, Tilt 17” to northwest 4 Some Homeowners Joe Montana Hall of Fame Quarterback Hunter Pence San Francisco Giants Superstar Steph Curry Golden State Warriors Icon 5 Some Homeowners Laurence Kornfield Retired Chief Deputy Building Inspector, City of SF Jerry Dodson Personal Injury Attorney 6 Why did this happen? San Francisco Downtown Area of “infirm” soils based on SF General Plan Subsurface profile (from Treadwell & Rollo) 8 10’ thick mat Subsurface conditions 75’ piles deep into Colma Sand 20’ (6m) – fill & rubble loose sand, brick, concrete, gravel 30’ (10m) – Young Bay Clay marine deposits – last 12,000 years 35’ (12m) – Colma Sand cemented sands with clay binder -

DATE: July 11, 2013 TO: Historic Preservation Commissioners FROM: Daniel A

DATE: July 11, 2013 TO: Historic Preservation Commissioners FROM: Daniel A. Sider, Planning Department Staff RE: Market Analysis of the Sale of Publicly Owned TDR In May 2012, Planning Department (“Department”) Staff provided the Historic Preservation Commission (“HPC”) an informational presentation on the City’s Transferable Development Rights (“TDR”) program. In February 2013, the Department retained Seifel Consulting, Inc. and C.H. Elliott & Associates (jointly, “Consultants”) to perform a market analysis informing a possible sale of TDR from City-owned properties. The resulting work product (“Report”) was delivered to the Department in late June. This memo and the attached Report are intended to provide the HPC with relevant follow-up information from the May 2012 hearing. The City’s TDR Program Since the mid-1980’s, the Planning Department has administered a TDR program (“Program”) through which certain historic properties can sell their unused development rights to certain non- historic properties. The program emerged from the 1985 Downtown Plan in response to unprecedented office growth, housing impacts, transportation impacts and the loss of historic buildings. The key goal of the Program is to maintain Downtown’s development potential while protecting historic resources. The metric that underpins the Program is Floor Area Ratio ("FAR"), which is the ratio of a building’s gross square footage to that of the parcel on which it sits. Under the Program, a Landmark, Significant, or Contributory building can sell un-built FAR capacity to a non-historic property which can then use it to supplement its base FAR allowance. TDRs can only be used to increase FAR within applicable height and bulk controls. -

Class Action Settlement Agreement

CLASS ACTION SETTLEMENT AGREEMENT This Class Action Settlement Agreement (“Agreement”) is entered into as of March 9, 2020 (the “Execution Date”) by and among the Class Action Settling Parties as defined below. Capitalized terms used herein are defined in Section II of this Agreement or indicated in parentheses elsewhere in this Agreement. I. FACTUAL REPRESENTATIONS 1.1 On or about July 21, 2017, Maui Peaks Corporation filed the Class Action against Transbay Joint Powers Authority (“TJPA”), Mission Street Development LLC (“MSD”), and Mission Street Holding LLC (“MSH”) on behalf of themselves and other owners of residential units in the Millennium Tower alleging causes of action relating to Plaintiffs’ allegations concerning, inter alia, the movement and tilt of Millennium Tower; 1.2 On September 14, 2017 Maui Peaks Corporation and NGMII LLC filed a First Amended Class Action Complaint in the Class Action against MSD, MSH and TJPA; 1.3 On or about January 5, 2018, Maui Peaks Corporation and NGMII LLC filed a Second Amended Class Action Complaint in the Class Action against MSD, MSH and TJPA; 1.4 On or about July 17, 2019, NGMII LLC and Ian Kao filed a Third Amended Class Action Complaint in the Class Action alleging causes of action for failure to disclose and for deceptive business practices against MSD and MSH, and causes of action for, inter alia, express indemnity, specific performance, and declaratory relief against TJPA, and Maui Peaks Corporation asserted those same causes of action against the same defendants on its own behalf; -

Millennium Tower, San Francisco

MILLENNIUM TOWER, SAN FRANCISCO Settlement, Tilting and Repair John A. Egan GE Ronald O. Hamburger, SE Senior Principal, Simpson Gumpertz & Heger Nathaniel Wagner, PE Project Engineer, Slate Geotech 16 February 2021 • Constructed 2005-2009 • 58 stories, 645 ft (197m) tall • Tallest & most expensive residential tower in San Francisco • Views from the Sierra to the Cascades to the Farallon Islands • Most expensive unit sold in 2013 for $13.5 million • Construction Cost - $600 Million Sales Cost - $750 Million 2 Some Homeowners Joe Montana Hall of Fame Quarterback Hunter Pence San Francisco Giants Superstar 3 The Site 301 Mission 2005-2009 350 Mission Transbay terminal and track tube 2012 2009-2017 200 Beale 2017-18 Salesforce Tower 4 2014-16 History of the Problem • Groundbreaking – 2005 – Settlement predicted 4”-6” • Construction completed 2009 – Settlement reached 10” – Transbay Terminal excavation starts • Last unit sold in 2013 – Settlement 13” • SGH retained in 2014 – Settlement 15” • Litigation initiated in 2016 – Settlement 17” • Adjacent construction complete 2017 – Settlement 18”, Tilt 17” to northwest 5 Why did this happen? San Francisco Downtown Area of “infirm” soils based on SF General Plan 10’ thick mat Subsurface conditions 75’ piles deep into Colma Sand 20’ (6m) – fill & rubble loose sand, brick, concrete, gravel 30’ (10m) – Young Bay Clay marine deposits – last 12,000 years 35’ (12m) – Colma Sand cemented sands with clay binder (bearing pressures up to 6 -8 ksf) 140’ (45m) – Old Bay Clay overconsolidated clays with layers -

Experience Record As of 12.31.19

EXPERIENCE RECORD AS OF 12.31.19 EXPERIENCE RECORD AS OF 12-31-19 (updated semi-annually) 165 PROJECTS IN DESIGN OR UNDER CONSTRUCTION SQUARE FEET Office 21,187,413 Living/Housing 24,432,720 Industrial/Logistics 12,088,486 Retail 2,389,141 Other 1,860,592 Total SF 61,958,352 886 COMPLETED DEVELOPMENT PROJECTS Office 152,078,268 Industrial/Logistics 41,910,950 Living/Housing 30,373,890 Retail 12,748,428 Hospitality 8,147,007 Sports Facilities 3,790,107 Medical/Biotechnological 3,472,366 Arts & Cultural 2,041,130 Educational 946,952 Other 3,057,553 Total SF 258,566,651 507 ACQUISITIONS Office 144,464,501 Industrial/Logistics 37,032,278 Retail 13,118,427 Living/Housing 3,325,174 Other 2,534,460 Total SF 200,474,840 539 PROPERTY/ASSET MANAGEMENT ASSIGNMENTS Hines Investment Management, 218 projects 98,100,000 Property-Level Services, 321 projects 134,300,000 Total SF 232,400,000 205 CURRENT HINES LOCATIONS (exclusive of facility management locations) U.S. Cities 106 Cities Outside of the United States 99 Cities with Facilities Mgmt. Assignments Only 454 Global Presence (Number of Cities) 659 Projects In Design and Under Construction Office 9 STEWART STREET 36-52 WELLINGTON 92 AVENUE OF THE AMERICAS Melbourne, Victoria, Australia Melbourne, Victoria, Australia New York, NY 55,208 sq. ft. office building 22,819 sq. ft. site planned for a heavy timber A development management project 10 stories creative office building 24,181 sq. ft. office building 14 stories 100 MILL 415 20TH STREET 561 GREENWICH Tempe, AZ Oakland, CA New York, NY 279,531 sq. -

BART Market Street Canopies and Escalators Modernization Project

Draft Initial Study/Mitigated Negative Declaration BART Market Street Canopies and Escalators Modernization Project San Francisco Bay Area Rapid Transit District April 30, 2018 Draft Initial Study/Mitigated Negative Declaration BART Market Street Canopies and Escalators Modernization Project Prepared for San Francisco Bay Area Rapid Transit District 300 Lakeside Drive, 21st floor Oakland, CA 94612 Prepared by 300 Lakeside Drive, Suite 400 Oakland, CA 94612 April 30, 2018 DRAFT INITIAL STUDY/MITIGATED NEGATIVE DECLARATION Date of Publication of Draft Initial Study/Mitigated Negative Declaration: April 30, 2018 Project Title: BART Market Street Canopies and Escalators Modernization Project Sponsor and Lead Agency: San Francisco Bay Area Rapid Transit District Contact Person and Phone Number: Janie Layton, (510) 874-7423 Project Location: Downtown San Francisco BART Stations (Embarcadero, Montgomery Street, Powell Street, and Civic Center/UN Plaza). Project Description: The San Francisco Bay Area Rapid Transit District (BART), in cooperation with the City and County of San Francisco, is working to improve escalator durability and security at station entrances/exits along Market Street leading to the underground Embarcadero, Montgomery Street, Powell Street, and Civic Center/UN Plaza station concourses. The existing entrances/exits consist of variations of side-by-side stairs and escalators leading down to the underground concourse level, and are currently uncovered and exposed to inclement weather and discarded trash leading to frequent breakdowns of the existing escalators. The proposed improvements would include the installation of canopy covers over the entrances/exits, as well as replacement and refurbishment of existing street-level escalators. Each protective canopy would also be equipped with a motorized security grille that would lock at the sidewalk level of the station entrance/exit when the stations are closed. -

400 Montgomery Street

400 Montgomery Street For Lease | Retail Space | North Financial District - San Francisco, CA This exceptionally well-located Downtown retail availability sits at the base of the historic 400 Montgomery Street - a 75,000 SF office building at the cross streets of Montgomery and California. Don’t miss this rare opportunity to front one of the Financial District’s busiest streets. Premises 1,951 Rentable Square Feet 20,253 Cars Per Day on Montgomery Ideal for Fitness, Non-Cooking Food, Estimated 22 Million Pedestrians or Service Per Year Pass the Intersection of Montgomery and California 101 PEIR 39 1 AQUATIC PARK JEFFERSON ST TAYLOR ST POWELL ST JONES ST MARINA GREEN NORTH POINT ST M BEACH ST A MASON ST Y R CASA WAY A IN W A KEARNY ST O B R L I V MARINA BLVD RICO WAY T JEFFERSON ST D STOCKTON ST BRODERICK ST E R GOLDEN GATE NATIONAL WEBSTER ST FORT BAY ST RECREATION AREA MASON NORTH POINT ST BUCHANAN ST GRANT AVE C PRADO ST CERVANTES BLVD R JEFFERSON ST BEACH ST HYDE ST IS S Y BAKER ST FI POLK ST BAY ST FRANCISCO ST CHESTNUT ST ELD A BEACH ST V BEACH ST MONTGOMERY ST E AVILA ST NORTH POINT ST GOUGH ST LARKIN ST T DIVISADERO ST BAY ST CHESTNUT ST H 101 E SCOTT ST E FILLMORE ST LOMBARD ST M CAPRA WAY FRANKLIN ST BAY ST B NORTH POINT ST A T SANSOME ST T E R S M FRANCISCO ST L C E A A G A D R L LOMBARD ST R D V B L A O GREENWICH ST E L M A LEAVENWORTH ST P R R B BAY ST H COLUMBUS AVE H L C O A A OCTAVIA ST CHESTNUT ST H PIERCE ST AY L N W W IL D O L BLV LIN S O A D Y LOMBARD ST C H TAYLOR ST CO TOLE GREENWICH ST K N L E E I N FILBERT ST L