Satisfaction with Big 5 Banks in Canada Declines As Satisfaction with Midsize Banks Improves, J.D

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2020 Public Accountability Statement

2020 PUBLIC ACCOUNTABILITY STATEMENT ABOUT CORPORATE SMALL ACCESS TO NUMBER OF DEBT TAXES BRANCH THIS REPORT DONATIONS & BUSINESS FINANCIAL EMPLOYEES FINANCING OPENINGS, PHILANTHROPIC BANKING SERVICES IN CANADA CLOSINGS & ACTIVITY RELOCATIONS What’s Inside 2 About this Report 17 Number of Employees in Canada 3 Corporate Donations & Philanthropic Activity 18 Debt Financing 9 Small Business Banking 20 Taxes 11 Access to Financial Services 21 Branch Openings, Closings & Relocations About this Report Scope of Reporting About Scotiabank This Public Accountability Statement includes Scotiabank is a leading bank in the Americas. information from November 1, 2019 to Guided by our purpose: “for every future”, we help October 31, 2020, for the following affiliates our customers, their families and their communities of Scotiabank in Canada: Scotia Capital Inc., achieve success through a broad range of advice, National Trust Company, Scotia Mortgage products and services, including personal and Corporation, Scotia General Insurance Company, commercial banking, wealth management and ADS Canadian Bank, Montreal Trust Company private banking, corporate and investment banking, of Canada, Scotia Life Insurance Company, and capital markets. With a team of over 90,000 The Bank of Nova Scotia Trust Company, employees and assets of approximately $1.1 trillion Scotia Dealer Advantage Inc., Roynat Inc., (as at October 31, 2020), Scotiabank trades on the MD Private Trust Company, and MD Life Insurance Toronto Stock Exchange (TSX: BNS) and New York Company. These affiliates are finance entities or Stock Exchange (NYSE: BNS). For more information, financial institution subsidiaries of Scotiabank please visit scotiabank.com and follow us on Twitter operating in Canada that have less than $1 billion @ScotiabankViews. -

2021 Annual Report

2021 Annual Report Built to help Albertans— then, now, and always There has never been a more powerful demonstration of the strength and resiliency of Albertans than what we witnessed over the past year. In the face of an ongoing global health crisis and the resulting economic impacts, the people of this province found ways to stay connected—offering each other support, encouragement, and hope when it was needed most. ATB is grateful to have played a part in helping Albertans navigate their way through the uncertainty and challenges of 2020. We focused first on the health and safety of our team members and our clients while building solutions to address the most urgent needs of our clients and our communities. Since then, we’ve continued to uplift Albertans, their businesses, and their communities whenever and wherever we can. Our commitment to Albertans is at the centre of everything we do. It’s why we’ve encouraged people to imagine what’s possible and why we’ve nurtured the entrepreneurial spirit of Albertans. It’s why we’ve supported local, seeded ingenuity, and spurred innovation both before and during the pandemic. And it’s what we’ll continue to do to keep Albertans moving toward the better days ahead. We know those days will come—and we’ll be here to help Albertans embrace the possibilities that come with them. Table of Contents Built to help Albertans—then, now, and always 01 Message from President and CEO Curtis Stange 03 Message from Board Chair Joan Hertz 05 Our Strategic Leadership Team 07 Business Highlights 08 Our Corporate Social Responsibility 09 Economy 11 Workplace 18 Diversity, Inclusion, and Belonging 22 Social Impact and Community Initiatives 28 Environment 34 2020–21 Financial Highlights 38 Message from Chief Financial Officer Dan Hugo 41 Stakeholder Engagement 43 About This Report 46 GRI Index 48 Locations 49 Management’s Discussion and Analysis and Financial Statements 50 Message from President and CEO Curtis Stange The act of reflection is powerful. -

Chris Fowler

And the winners are... HeaderAward of Distinction BodyLEADER Copy OF THE YEAR Sponsored by: Award of Distinction: LEADER OF THE YEAR Chris Fowler President & CEO, CWB Financial Group Award of Distinction: LEADER OF THE YEAR Chris Fowler has served at CWB in roles with increasing responsibility since 1991, including commercial account management (1991-1995), credit risk (1995-2008) and joined the executive team in 2008 as Executive Vice President, Banking. He became President and Chief Executive Officer of CWB Financial Group in March 2013, concurrent with his election to the Board of Directors. Chris started his career in commercial and corporate banking in 1985 with Continental Bank of Canada, which was subsequently acquired by Lloyds Bank Canada and then by HSBC Bank Canada. He holds a Master of Arts Degree in Economics from the University of British Columbia. Chris sits on the University Hospital Foundation Board of Trustees and is currently the Chair of the Finance & Investment Committee. He is also a member of the Canadian Bankers Association’s Executive Council, the Business Council of Canada, Business Council of Alberta and the Alberta Economic Recovery Council. Chris is married with twin daughters. Played rugby for Team Canada in 1979, 1989 and 1990. He also played for UBC and club teams in Victoria, Vancouver and Edmonton where he won multiple provincial championships as well as the national city championships. HeaderAward of Distinction BodyCOMMUNICATOR Copy OF THE YEAR Sponsored by: Award of Distinction:COMMUNICATOR OF THE YEAR Shani Gwin Founder & Managing Partner Gwin Communications Award of Distinction:COMMUNICATOR OF THE YEAR Shani Gwin is the founder and managing partner of Gwin Communications, an Indigenous owned, led and staffed public relations agency. -

Live Canadian Bank and Supplier Connections NAME TYPE

Live Canadian Bank and Supplier Connections NAME TYPE ENHANCED Alterna Savings Banks and Credit Cards Amazon.ca Rewards Visa from Chase Banks and Credit Cards American Express (Canada) Banks and Credit Cards YES American Express Merchant Services (EUR) Banks and Credit Cards Assiniboine Credit Union Banks and Credit Cards ATB Financial (Business) Banks and Credit Cards YES ATB Financial (Personal) Banks and Credit Cards BMO Debit Card Banks and Credit Cards YES BMO Nesbitt Burns Banks and Credit Cards BMO Online Banking for Business Banks and Credit Cards Canadian Tire Options MasterCard Banks and Credit Cards Canadian Western Bank Banks and Credit Cards YES Capital One Mastercard (Canada) Banks and Credit Cards CHASE Bank Canada Banks and Credit Cards CIBC Banks and Credit Cards YES CIBC Wood Gundy Banks and Credit Cards Coast Capital Savings Banks and Credit Cards YES Costco Capital One Credit Card Banks and Credit Cards CUETS: Choice Rewards Mastercard Banks and Credit Cards Desjardins Business Banks and Credit Cards Desjardins VISA Banks and Credit Cards Envision Financial Banks and Credit Cards First National Financial Banks and Credit Cards Ford Credit (Canada) Banks and Credit Cards HBC Credit Card Banks and Credit Cards Home Depot Consumer Credit Card (Canada) Banks and Credit Cards Home Depot Revolving Commercial Charge Card (Canada) Banks and Credit Cards HSBC Bank Canada Banks and Credit Cards HSBC MasterCard Banks and Credit Cards Interior Savings Credit Union Banks and Credit Cards Island Savings Banks and Credit Cards MBNA -

The Finance Industry's Guide to Marketing Data

The Finance Industry’s Guide to Marketing Data From zero-party to third-party, how consumer data drives growth in the financial industry Introduction The financial services market is changing. A recent PwC survey revealed that 71% of U.S. banking executives consider non-traditional new market entrants to be a threati, indicating that competition from FinTech and companies like Ama- zon and Apple is putting pressure on legacy financial brands. Furthermore, evolving consumer expectations for conve- nience and personalization are creating a need for a more customer-centric approach within the financial industry. In fact, in a recent Data Axle survey, 52% of financial services consumers ranked relevant content as the most important marketing factor that influences their decision to switch to a new provider. Financial brands that master the application and analysis of consumer data to elevate customer experiences and improve marketing ROI (return on investment) will gain an edge over their competitors. Understanding how market- ing data is collected, utilized, and leveraged is the key for financial marketers to adapt and modernize for the digital consumer. pg. 1 The four types of consumer data Consumer data is divided into four categories based on how it is collected. Zero-party data Data that is shared directly and proactively by consumers about their preferences, interests, and/or intent. (e.g., surveys, preference centers, polls) First-party data Data collected by marketers about their audience and customers. (e.g., account history, email activity, web behavior) Second-party data Data that is collected, owned, and managed by a partner company (their first-party data). -

Creditor Listing

Northern Silica Corporation, Heemskirk Mining Pty. Ltd., Heemskirk Canada Holdings Limited, Heemskirk Canada Limited, Custom Bulk Services Inc. and HCA Mountain Minerals (Moberly) Limited (collectively the “NSC Companies” or the “Debtors”) List of Creditors As at June 30, 2020 Please note the following: 1. The list of creditors has be prepared from information contained in the books and records of the NSC Companies. 2. The amounts included in this list of creditors do not take into consideration any un-invoiced amounts, nor have the amounts been adjusted for any amounts that may also be receivable from creditors. 3. This list of creditors has been prepared without admission as to the liability for, or quantom of, any of the amounts shown. 4. To date, a claims procedure has not been approved by the Court, and creditors are NOT required to file a statement of account or proof of claim at this point in time. If, at a later date, a claims procedure is approved by the Court, all known creditors will be notified and claim forms will be posted to the Monitor's website. It is through such a claims procedure that creditor claims will be reviewed and determined. 5. Amounts owing to various government agencies, if any, are unknown at this time. 6. Where $USD amounts are converted to $CAD, the rate used is 1.3628. This was the posted exchange rate at June 30, 2020 on the Bank of Canada's website. Province / Amount Secured Creditors Address City State Postal Code Country Outstanding Taurus Funds Management PTY LTD. Jachthavenweg 109H, 1081 KM Amsterdam Netherlands$ 53,200,000 Qmetco Limited Level 12, 300 Queen Street Brisbane QLD 4000 Australia$ 21,500,000 First Samuel Limited Level 11, 250 Collins Street Melbourne VIC 3000 Australia$ 5,700,000 Alberta Treasury Branch 6794 - 50 Ave. -

ATB Financial Is Optimizing Customer Service with Intelligent Automation

Spotlight: Blue Prism & ATB Financial ATB Financial is optimizing customer service with Intelligent Automation BluePrism.com ATB Financial is leveraging the Blue Prism’s connected-RPA (Robotic Process Automation ) platform to drive increased customer loyalty, generate multi-million- dollar efficiency savings - and deliver major resource capacity back to the business. Maintaining competitive advantage via innovation ATB Financial is the largest Alberta-based financial institution, with assets of more than $51.9 billion and a team of 5,300 helping more than 753,000 customers in 244 Alberta communities. ATB prides itself on being a great place to work - and in 2017, was named one of Aon’s Best Employers in Canada. Operating in a rapidly changing and highly regulated market, ATB wants to maintain its competitive advantage by swiftly embracing the digital revolution that’s enveloping financial services. To achieve this goal, the company looked to build upon two clear areas of differentiation—an outstanding culture that serves its customers, and having the tools, technology, and processes to optimize operations. This journey, led by Dan Semmens, managing director of transformation - process automation at ATB Financial, started in 2016 with a twofold focus on improving the customer experience – while also enhancing operational efficiencies. This involved significantly re-designing, simplifying and improving processes - using connected-RPA (Robotic Process Automation) as a key catalyst to achieve these goals. “We’re focused on applying technology in areas that impact customers most. RPA applied to the right use-cases, means better customer experience, and more time for us to hear our customers. This is just one of the ways we are working every day to make our business better.” — DAN SEMMENS, MANAGING DIRECTOR OF TRANSFORMATION - PROCESS AUTOMATION, ATB FINANCIAL Blue Prism & ATB Financial Case Study 2 “Our first priority was to identify where we could create the most value, or solve the most pressing customer problem. -

Rule D4 Institution Numbers and Clearing Agency/Representative Arrangements

RULE D4 INSTITUTION NUMBERS AND CLEARING AGENCY/REPRESENTATIVE ARRANGEMENTS 2021CANADIAN PAYMENTS ASSOCIATION This Rule is copyrighted by the Canadian Payments Association. All rights reserved, including the right of reproduction in whole or in part, without express written permission by the Canadian Payments Association. Payments Canada is the operating brand name of the Canadian Payments Association (CPA). For legal purposes we continue to use “Canadian Payments Association” (or the Association) in these rules and in information related to rules, by-laws, and standards. RULE D4 – INSTITUTION NUMBERS AND CLEARING AGENCY/REPRESENTATIVE ARRANGEMENTS TABLE OF CONTENTS IMPLEMENTED ............................................................................................... 3 AMENDMENTS PRE-NOVEMBER 2003 ........................................................ 3 AMENDMENTS POST-NOVEMBER 2003 ..................................................... 3 INTRODUCTION ................................................................................................................. 6 ELIGIBILITY......................................................................................................................... 6 INSTITUTION NUMBERS ................................................................................................... 6 AMALGAMATION AND ACQUISITION .............................................................................. 6 NON-MEMBER ENTITIES .................................................................................................. -

Post-Show Report Dx3 2019 Post-Show Report

MARCH 6 - 7, 2019 METRO TORONTO CONVENTION CENTRE POST-SHOW REPORT DX3 2019 POST-SHOW REPORT In 2019, Canada’s leading conference for retailers, marketers and tech innovators, DX3 took place at the Metro Toronto Convention Centre and featured more than 100 industry speakers and 50 immersive exhibitions. The event displayed the brightest established and upcoming minds in the industry from Canada and international. national. 2 POST-SHOW REPORT DX3 seems to be the right mix of direct marketing, digital marketing, technology and an ability to get ideas on how to take a business and expose it to as many people as possible.” Corby Fine, Vice President, Simplii Financial (CIBC) This is where all the major retailers are, if you want to network in this space this the show to be.” Michael Schwarzl, Key Account Manager, LG Electronics It’s a great opportunity for us at IKEA to really talk about our brand journey in the context of innovation.” Lauren McDonald, CMO, IKEA Canada POST-SHOW REPORT 3 PRESS & SOCIAL MEDIA Being featured on media platforms from CP24, Betakit, Style Democracy, Cannabis Retailer and more, Dx3 earned over 6.6 million media impressions across Canada. These were generated from press articles, TV segments, blog posts and social media buzz. 4 POST-SHOW REPORT PRESS & SOCIAL MEDIA SOCIAL REACH #DX32019 was a massive success on Twitter and the event took over Instagram feeds and stories over the two days! It generated 707 social posts, reached 479,117 people and had 2100 likes, relating to 13.5 million social media impressions. 6.6 MILLION + 13.5 MILLION + MEDIA IMPRESSIONS SOCIAL MEDIA IMPRESSIONS POST-SHOW REPORT 5 DX3 2019 DEMOGRAPHICS The event displayed a higher number of Retail and Marketing attendees, making for over 60% of the attendees and 54% of the conference attendees were retailers. -

Moving up in the World

RESEARCHJanuary REPORT22, 2018 JanuaryCIBC 22, Company 2018 Pitch Insert Picture in Master View Stock Rating HOLD Price Target $131.00 Bear Price Bull Case Target Case $116.84 $131.00 $141.25 Ticker TSX:CM Canadian Imperial Bank of Commerce Market Cap. ($MM) 49,888 Moving up in the World P/TBV 2.5x ROE 17.2% Introduction 52 Week Performance The Canadian Imperial Bank of Commerce (CIBC) is one of the 120 Canadian Big Five Banks, providing various financial services and products to over 11 million people and commanding a market share of 15%. In recent years, CIBC has focused on improving client experiences, growing both customer satisfaction and their overall customer base. The bank has also recently undergone several 110 acquisitions, moving into the U.S. market and competing with other large Canadian banks in this new space. CIBC’s continuous improvement has made them increasingly well-positioned to outperform Canadian peers. 100 Investment Thesis Argument I: Building A Well-Diversified Bank through U.S. Expansion 90 22-Jan-17 22-Jul-17 19-Jan-18 Argument II: Leveraging Market Exposure to Grow Returns CM Index Argument III: Improving Financials and Operating Efficiency Financial Institutions Valuation Neil Shah When compared to the other Canadian banks, CIBC trades at a [email protected] discount on a Price-to-Tangible Book Value and Price-to-Earnings basis. CIBC also boasts the highest dividend yield among its peers. Adam Carnicelli Using a Dividend Discount Model, we arrived at a target price of [email protected] $131, implying a total return of 6.9%. -

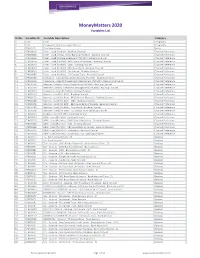

Moneymatters 2020 Variables List

MoneyMatters 2020 Variables List Order Variable ID Variable Description Category 0 CODE Code Geography 0 GEO Geographic Summarization Indicator Geography 1 CBASHHD Total Households Basics 2 CFM0001B Teller - Used [Pst Mth] - Banking Channel Channel Preference 3 CFM0002B Teller - Used for Day to Day Banking [Pst Mth] - Banking Channel Channel Preference 4 CFM0003B Teller - Used to Make Investment [Pst Mth] - Banking Channel Channel Preference 5 CFM0004B Teller - Used [Pst Mth] - BMO Bank of Montreal - Banking Channel Channel Preference 6 CFM0005B Teller - Used [Pst Mth] - CIBC - Banking Channel Channel Preference 7 CFM0006B Teller - Used [Pst Mth] - RBC Royal Bank - Banking Channel Channel Preference 8 CFM0007B Teller - Used [Pst Mth] - Scotiabank - Banking Channel Channel Preference 9 CFM0008B Teller - Used [Pst Mth] - TD Canada Trust - Banking Channel Channel Preference 10 CFM0010B Telephone - Used for Day to Day Banking [Pst Mth] - Banking Channel Channel Preference 11 CFM0011B Telephone - Used for Investment Management [Pst Mth] - Banking Channel (!) Channel Preference 12 CFM0013B Internet - Used for Day to Day Banking [Pst Mth] - Banking Channel Channel Preference 13 CFM0014B Internet - Used for Investment Management [Pst Mth] - Banking Channel Channel Preference 14 CFM0009B Telephone - Used [Pst Mth] - Banking Channel Channel Preference 15 CFM0012B Internet - Used [Pst Mth] - Banking Channel Channel Preference 16 CFM0015B Internet - Used [Pst Mth] - BMO Bank of Montreal - Banking Channel Channel Preference 17 CFM0016B Internet - -

Audited Annual Financial Statements for the Year Ended December 31, 2018

Audited Annual Financial Statements For the year ended December 31, 2018 Tangerine Balanced Portfolio Tangerine Balanced Portfolio Audited Annual Financial Statements for the year ended December 31, 2018 (In Canadian dollars, unless otherwise indicated) Independent Auditors’ Report To the Unitholders of Tangerine Balanced Portfolio (the “Fund”) Opinion We have audited the financial statements of the Fund, which comprise the statements of financial position as at December 31, 2018 and 2017, and the statements of comprehensive income, statements of changes in net assets attributable to holders of redeemable units and statements of cash flows for the years then ended, and notes to the financial statements, including a summary of significant accounting policies. In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the Fund as at December 31, 2018 and 2017, and its financial performance and its cash flows for the years then ended in accordance with International Financial Reporting Standards (IFRSs). Basis for Opinion We conducted our audit in accordance with Canadian generally accepted auditing standards. Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Fund in accordance with the ethical requirements that are relevant to our audit of the financial statements in Canada, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion. Other Information Management is responsible for the other information.