Long Term Passenger Rolling Stock Strategy for the Rail Industry

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Project the Latest Alternative Train Tech

SEE INSIDE FOR: A national traction climate strategy n Designing a ‘green’ project n The latest alternative train tech: batteries & hydrogen n The case for more wires Decarbonisation Special 76 Decarbonisation SMART TRANSPORT CONFERENCE 2019 Special CONTENTS Full steam ahead BCRRE introduces its 40soon-to-be-launched Centre of Excellence in Decarbonisation. Ready to charge VIVARAIL explains how its 42latest innovations will revolutionise rail traction. Bright spark Why HITACHI thinks that 44battery power is the answer to powering zero emissions trains ‘off the wires’. Industry taskforce How the recommendations of 46the Decarbonisation Taskforce final report are now being implemented. The market leader ALSTOM seeks to expand the 52reach of the world’s only DATE: 17 MARCH 2020 in-service hydrogen-powered trains. PHIL METCALFE. Mean, green machine VENUE: ETC VENUES, How SIEMENS MOBILITY is 54perfectly in step with the UK’s COUNTY HALL, LONDON ambition to phase out diesel trains. Smart money Welcome SYSTRA tells RAIL how cutting Find out about local and national a project’s carbon footprint n June 12 2019, in one of her final to achieve this vision. 56 does not always mean increasing the cost. government transport challenges acts as Prime Minister, Theresa Meanwhile, Network Rail’s Head of ADVANCED • May announced that the UK will Strategic Planning Helen McAllister provides Listen to multi-modal solutions Oend its net contribution to global an update on the Traction Decarbonisation RATE NOW greenhouse gas emissions by 2050. Network Strategy (TDNS), which is being Current beliefs AVAILABLE • By amending the Climate Change Act 2008 developed to inform government decisions on Why electrification remains Network with senior public and to incorporate this target, it made the UK the providing support for further electrification, 58the future of UK railways, first G7 country to legally implement a net alongside the deployment of alternative according to FURRER + FREY. -

Records of Wolverton Carriage and Wagon Works

Records of Wolverton Carriage and Wagon Works A cataloguing project made possible by the Friends of the National Railway Museum Trustees of the National Museum of Science & Industry Contents 1. Description of Entire Archive: WOLV (f onds level description ) Administrative/Biographical History Archival history Scope & content System of arrangement Related units of description at the NRM Related units of descr iption held elsewhere Useful Publications relating to this archive 2. Description of Management Records: WOLV/1 (sub fonds level description) Includes links to content 3. Description of Correspondence Records: WOLV/2 (sub fonds level description) Includes links to content 4. Description of Design Records: WOLV/3 (sub fonds level description) (listed on separate PDF list) Includes links to content 5. Description of Production Records: WOLV/4 (sub fonds level description) Includes links to content 6. Description of Workshop Records: WOLV/5 (sub fonds level description) Includes links to content 2 1. Description of entire archive (fonds level description) Title Records of Wolverton Carriage and Wagon Works Fonds reference c ode GB 0756 WOLV Dates 1831-1993 Extent & Medium of the unit of the 87 drawing rolls, fourteen large archive boxes, two large bundles, one wooden box containing glass slides, 309 unit of description standard archive boxes Name of creators Wolverton Carriage and Wagon Works Administrative/Biographical Origin, progress, development History Wolverton Carriage and Wagon Works is located on the northern boundary of Milton Keynes. It was established in 1838 for the construction and repair of locomotives for the London and Birmingham Railway. In 1846 The London and Birmingham Railway joined with the Grand Junction Railway to become the London North Western Railway (LNWR). -

Great Britain Passenger Rail: the Current Expected Timetable

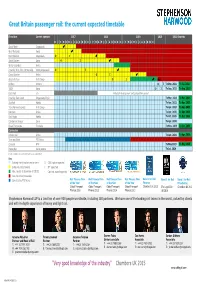

Great Britain passenger rail: the current expected timetable Franchise Current operator 2017 2018 2019 2020 2021 Onwards DJFMA MJJASONDJFMA MJJASONDJFMA MJJASOND South West Stagecoach West Midlands Govia East Midlands Stagecoach O I South Eastern Govia O I Wales & Borders Arriva InterCity W.C./W.C. Partnership Virgin/Stagecoach O I Cross Country Arriva OI Great Western First Group OI Apr. Chiltern Chiltern OITo Dec. 2021 To Jul. 2022 TSGN Govia O I To Sep. 2021 To Sep. 2023 East West n/a Potential development and competition period InterCity East Coast Stagecoach/Virgin To Mar. 2023 To Mar. 2024 ScotRail Abellio To Apr. 2022 To Apr. 2025 TransPennine Express First Group To Apr. 2023 To Apr. 2025 Northern Arriva To Apr. 2025 To Apr. 2026 East Anglia Abellio To Oct. 2025 To Oct. 2026 Caledonian Sleeper Serco To Apr. 2030 Essex Thameside Trenitalia To Nov. 2029 To Jun. 2030 Concession London Rail Arriva To Apr. 2024 To Apr. 2026 Tyne and Wear PTE Nexus Crossrail MTR To May 2023 To May 2025 MerseyRail Serco/Abellio To Jul. 2028 Based on publicly available information as at 1 April 2017 Key Existing franchise/concession term O OJEU notice expected Extension/direct award I ITT expected Max. length at discretion of DfT/TS Contract award expected New franchise/concession Operated by PTE Nexus Rail Finance Firm Rail Finance Firm Rail Finance Firm Rail Finance Firm Band 1 for Rail Band 1 for Rail Band 1 for Rail of the Year of the Year of the Year of the Year Finance Franchising Global Transport Global Transport Global Transport Global Transport Chambers UK 2015 The Legal 500 Chambers UK 2017 Finance 2016 Finance 2015 Finance 2014 Finance 2013 UK 2016 Stephenson Harwood LLP is a law firm of over 900 people worldwide, including 150 partners. -

Scotrail Franchise – Franchise Agreement

ScotRail Franchise – Franchise Agreement THE SCOTTISH MINISTERS and ABELLIO SCOTRAIL LIMITED SCOTRAIL FRANCHISE AGREEMENT 6453447-13 ScotRail Franchise – Franchise Agreement TABLE OF CONTENTS 1. Interpretation and Definitions .................................................................................... 1 2. Commencement .......................................................................................................... 2 3. Term ............................................................................................................ 3 4 Franchisee’s Obligations ........................................................................................... 3 5 Unjustified Enrichment ............................................................................................... 4 6 Arm's Length Dealings ............................................................................................... 4 7 Compliance with Laws................................................................................................ 4 8 Entire Agreement ........................................................................................................ 4 9 Governing Law ............................................................................................................ 5 SCHEDULE 1 ............................................................................................................ 7 PASSENGER SERVICE OBLIGATIONS ............................................................................................. 7 SCHEDULE 1.1 ........................................................................................................... -

& What's in Store at RAIL LIVE 2018

M A G A Z I N E The latest news & reviews from the industry What’s in Store at RAIL LIVE 2018 Revolutionising Rail: UKRRIN Centres of Excellence What does the EU-Japan Economic Partnership & Agreement Mean for the Rail Industry? Rail Live – Issue Two 2018 Letter from the Editor Dear Readers, timed perfectly for the start of summer in the Northern Hemisphere where it’s held Rail Live 2018 will take place at the Quinton Rail Technology Centre in ANDREW LUSH Director Warwickshire on 20–21 June. [email protected] As always there will be plenty to see and feature What Does the EU-Japan JOSEPHINE CORDERO SAPIÉN do. Vivarail, who are based at the Economic Partnership Agreement Editor-in-chief technology centre and whose aim is to Mean for the Rail Industry? The (revised) [email protected] produce low-cost, low-maintenance WTO Government Procurement rolling stock, will exhibit their D-train, at Agreement that came into force in 2014 NICOLA BROWN Rail Live. Founded in just 2012, Vivarail addresses government procurement for Head of Sales purchased London Underground D78 goods and services based on openness, [email protected] stock in 2014 with the purpose of transparency and non-discrimination. converting it into Class 230s. Last year’s Up until now Japan has managed to AMBER GUy-KEMP Rail Live was the first time such a keep its rail market closed despite the Head of Client Content converted Class 230 carried passengers. GPA. However the new agreement with [email protected] At this year’s Rail Live Vivarail will exhibit the EU will change this, giving rail a battery version of its D-train, which will industry suppliers on both sides greater GUy RAyMENT once again give passenger rides. -

Train Sim World 2 Southeastern High Speed Driver's Manual EN.Pdf

EN SOUTHEASTERN HIGH SPEED ©2021 Dovetail Games, a trading name of RailSimulator.com Limited (“DTG”). "Dovetail Games", “Train Sim World” and “SimuGraph” are trademarks or registered trademarks of DTG. Unreal® Engine, ©1998-2021, Epic Games, Inc. All rights reserved. Unreal® is a registered trademark of Epic Games. Portions of this software utilise SpeedTree® technology (©2014 Interactive Data Visualization, Inc.). SpeedTree® is a registered trademark of Interactive Data Visualization, Inc. All rights reserved. Southeastern is the registered trade mark of The Go-Ahead Group PLC. Permission to use the Double Arrow Trade Mark is granted by the Secretary of State for Transport. All other copyrights or trademarks are the property of their respective owners and are used here with permission. Unauthorised copying, adaptation, rental, re-sale, arcade use, charging for use, broadcast, cable transmission, public performance, distribution or extraction of the product or any trademark or copyright work that forms part of this product is prohibited. Developed and published by DTG. CONTENTS 1 SOUTHEASTERN HIGH SPEED OVERVIEW 5 TRAIN SAFETY & IN-CAB SIGNALLING SYSTEMS 5 INTRODUCING SOUTHEASTERN HIGH SPEED 43 AUTOMATIC WARNING SYSTEM (AWS) 6 ROUTE MAP & POINTS OF INTEREST 44 TRAIN PROTECTION & WARNING SYSTEM (TPWS) 7 GAME MODES 45 KVB 2 THE BR CLASS 395 'JAVELIN' 47 TVM-430 8 INTRODUCING THE BR CLASS 395 'JAVELIN' 6 BRITISH RAILWAY SIGNALLING 9 BR CLASS 395 DRIVING CAB: FRONT 50 COLOUR LIGHT 10 BR CLASS 395 DRIVING CAB: REAR 56 SEMAPHORE 11 BR CLASS -

University of Southampton Research Repository Eprints Soton

University of Southampton Research Repository ePrints Soton Copyright © and Moral Rights for this thesis are retained by the author and/or other copyright owners. A copy can be downloaded for personal non-commercial research or study, without prior permission or charge. This thesis cannot be reproduced or quoted extensively from without first obtaining permission in writing from the copyright holder/s. The content must not be changed in any way or sold commercially in any format or medium without the formal permission of the copyright holders. When referring to this work, full bibliographic details including the author, title, awarding institution and date of the thesis must be given e.g. AUTHOR (year of submission) "Full thesis title", University of Southampton, name of the University School or Department, PhD Thesis, pagination http://eprints.soton.ac.uk UNIVERSITY OF SOUTHAMPTON FACULTY OF ENGINEERING AND THE ENVIRONMENT Transportation Research Group Investigating the environmental sustainability of rail travel in comparison with other modes by James A. Pritchard Thesis for the degree of Doctor of Engineering June 2015 UNIVERSITY OF SOUTHAMPTON ABSTRACT FACULTY OF ENGINEERING AND THE ENVIRONMENT Transportation Research Group Doctor of Engineering INVESTIGATING THE ENVIRONMENTAL SUSTAINABILITY OF RAIL TRAVEL IN COMPARISON WITH OTHER MODES by James A. Pritchard iv Sustainability is a broad concept which embodies social, economic and environmental concerns, including the possible consequences of greenhouse gas (GHG) emissions and climate change, and related means of mitigation and adaptation. The reduction of energy consumption and emissions are key objectives which need to be achieved if some of these concerns are to be addressed. -

Togfonden DK – Højhastighed Og Elektrificering På Den Danske Jernbane

Togfonden DK – højhastighed og elektrificering på den danske jernbane September 2013 2 Togfonden DK Timemodellen - det danske højhastighedskoncept Forord De markant kortere rejsetider rykker familier nærmere sammen, gør Timemodellen er visionen om at kunne køre med tog fra København til det mere attraktivt at søge job, som ligger længere væk fra ens bopæl, Odense på én time, samt videre til Aarhus hhv. Esbjerg på yderligere én mindsker transporttidens andel i dagligdagen og imødekommer time, samt fra Aarhus til Aalborg på én time. Timemodellen vil være erhvervslivets behov. Hermed styrkes Danmarks konkurrenceevne, og i den største forbedring for jernbanen siden åbningen af sidste ende jobskabelsen. Ligesom selve anlægsarbejderne også vil Storebæltsforbindelsen i 1997. være gavnlige for beskæftigelsen i Danmark. Samfundet bliver rigere med Togfonden DK, og det er den relativt billigste måde at få Med projekterne i Togfonden DK realiseres Timemodellen med markant danskerne til at rejse mere kollektivt. hurtigere rejsetider som vil rykke hele Danmark tættere sammen. Med timemodellen anlægges en række nye baner i korridoren København- Med elektrificeringen i Togfonden DK, og de tog i Timemodellen, som Odense-Aarhus-Aalborg, og bestående strækninger opgraderes. for alvor skal bruge elektrificeringen vil stort set hele DSB’s udledning Effekterne af timemodellen vil imidlertid også sprede sig som ringe i af CO2 forsvinde. Samtidig sikres renere luft som følge af udfasningen vandet til hele landet. Der vil være direkte Superlyn til 9 byer vest for af dieseltogene. Yderligere vil overflytningen af bilister og flyrejsende Storebælt, og køreplanen forventes opbygget så mindst 25 byer vest virke i en grønnere retning. for Storebælt har prioriteret korrespondance til Superlynet. -

2019-01 20 Point Plan Issue14.Pdf

Fleet Management Good Practice Guide – 20 Point Plan Issue 14 – January 2019 AMENDMENT RECORD Issue Dated Notes Section 2: MP code removed from Technical incident reasons 14 December 2018 table “701D” 14 December 2018 Inclusion of new Section 10: Managing Ageing Rolling Stock 14 December 2018 Sections new cover inserted 14 December 2018 General document sections restructure 14 December 2018 Gary Cooper’s foreword updated Fleet Management Good Practice Guide: Issue 14 - January 2019 ii Foreword Our customers’ needs have been consistent ever since the birth of the railway, whether they are passengers, or businesses that send freight by rail, and the message is simply: run my train on time. Meeting this need is a priority for all of us in rail, and the desire for on-time service delivery shows in the correlation between punctuality and customer satisfaction and, in turn, the correlation between customer satisfaction and rail businesses’ revenues. It is important therefore, for the industry and the country as well as customers that we run punctual trains. We have been failing to do this for too long. After improving performance every month from 2002 – 2011, we now repeatedly miss the punctuality levels that TOCs and NR Routes agree they will deliver. The reliability of the vehicles we operate is part of that under-delivery and we have to do better. In 2013, the fleet planned a national passenger fleet performance challenge of delivering 11 500 MTIN by March 2019, a 20% improvement in reliability over this five- year control period. The reality is that we are likely to deliver only 9 000 MTIN by then. -

The Treachery of Strategic Decisions

The treachery of strategic decisions. An Actor-Network Theory perspective on the strategic decisions that produce new trains in the UK. Thesis submitted in accordance with the requirements of the University of Liverpool for the degree of Doctor in Philosophy by Michael John King. May 2021 Abstract The production of new passenger trains can be characterised as a strategic decision, followed by a manufacturing stage. Typically, competing proposals are developed and refined, often over several years, until one emerges as the winner. The winning proposition will be manufactured and delivered into service some years later to carry passengers for 30 years or more. However, there is a problem: evidence shows UK passenger trains getting heavier over time. Heavy trains increase fuel consumption and emissions, increase track damage and maintenance costs, and these impacts could last for the train’s life and beyond. To address global challenges, like climate change, strategic decisions that produce outcomes like this need to be understood and improved. To understand this phenomenon, I apply Actor-Network Theory (ANT) to Strategic Decision-Making. Using ANT, sometimes described as the sociology of translation, I theorise that different propositions of trains are articulated until one, typically, is selected as the winner to be translated and become a realised train. In this translation process I focus upon the development and articulation of propositions up to the point where a winner is selected. I propose that this occurs within a valuable ‘place’ that I describe as a ‘decision-laboratory’ – a site of active development where various actors can interact, experiment, model, measure, and speculate about the desired new trains. -

Britain's Railways

BRITAIN’S RAILWAYS MUCH MORE FOR MUCH LESS August 2010 Front cover picture of Siemens Desiro electric train at Northampton by Philip Bisatt Rear cover picture of Glasgow by Network Rail The Railway Development Society Limited Registered in England and Wales No: 5011634 A Company Limited by Guarantee Registered Office: 24 Chedworth Place, Tattingstone, Suffolk IP9 2ND www.railfuture.org.uk INTRODUCTION Railfuture is Britain’s only completely independent voice on railway development. We are not affiliated to or supported by any political party, trade union or by private industry. We receive almost no funding from any source other than our members. We are convinced that in the current economic climate rail travel and rail freight represent wise investments for the future of this country. We are pro-rail but not anti-road. We believe that all transport modes have their place in a vibrant, modern, integrated, environmentally efficient market economy. We believe that investment can be made sensibly and cost-effectively to achieve: Britain’s Railways – Much More for Much Less. COSTS INDUSTRY COSTS – MYTH AND REALITY We need to emphasise that there is a significant difference between the gross and net costs of the rail industry after allowing for money paid to government from Corporation tax, Industrial Buildings tax, fuel tax, Community Infrastructure Levy, VAT, Uniform Business Rates and income tax from a combined workforce of about 150,000 people, together with premium payments and revenue sharing agreements paid by the train operating companies. Investment should be excluded from annual costs since rail projects have a very long payback period. -

The Railcar Association Bulletin November 2011

The Railcar Association Bulletin November 2011 Introduction A busy bulletin this time thanks to the number of contributions and the coincidental number of newsworthy events that have involved DMUs over the last two months. The highlight was of course the annual convention which we are pleased to report came off without a hitch. The Association would like to thank the Keighley & Worth Valley Railway for their efforts in accommodating us. It may be a cliché but I had feedback from several individuals who thought the convention was one of the best in recent years. Following feedback from members, we have agreed the dates and venue for the next convention nice and early, so there will be no excuses for not getting time off work! I hope you all agree that the choice for next years event is a good one. Finally, a separate “Restoration & Overhauls” section has been included this issue, as groups have clearly been busy this autumn doing lots of work on preserved vehicles. 17th Annual Railcar Convention The Railcar Association are pleased to announce that the 17th Annual Convention will be held at the Great Central Railway from Friday 7th September to Sunday 9th September 2012. This will be the first time the Great Central have hosted the event, which should prove unique with the railway’s mainline ethos and five mile double track section. Following feedback from members, the initial announcement has been made earlier than normal so delegates have plenty of time to make arrangements with work etc. This means much of the weekend is still to be planned and confirmed, and updates will be released during 2012.