The Brief Mergermarket’S Weekly Private Equity Round-Up

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Russian M&A Review 2017

Russian M&A review 2017 March 2018 KPMG in Russia and the CIS kpmg.ru 2 Russian M&A review 2017 Contents page 3 page 6 page 10 page 13 page 28 page 29 KEY M&A 2017 OUTLOOK DRIVERS OVERVIEW IN REVIEW FOR 2018 IN 2017 METHODOLOGY APPENDICES — Oil and gas — Macro trends and medium-term — Financing – forecasts sanctions-related implications — Appetite and capacity for M&A — Debt sales market — Cross-border M&A highlights — Sector highlights © 2018 KPMG. All rights reserved. Russian M&A review 2017 3 Overview Although deal activity increased by 13% in 2017, the value of Russian M&A Deal was 12% lower than the previous activity 13% year, at USD66.9 billion, mainly due to an absence of larger deals. This was in particular reflected in the oil and gas sector, which in 2016 was characterised by three large deals with a combined value exceeding USD28 billion. The good news is that investors have adjusted to the realities of sanctions and lower oil prices, and sought opportunities brought by both the economic recovery and governmental efforts to create a new industrial strategy. 2017 saw a significant rise in the number and value of deals outside the Deal more traditional extractive industries value 37% and utility sectors, which have historically driven Russian M&A. Oil and gas sector is excluded If the oil and gas sector is excluded, then the value of deals rose by 37%, from USD35.5 billion in 2016 to USD48.5 billion in 2017. USD48.5bln USD35.5bln 2016 2017 © 2018 KPMG. -

A Genealogy of Top Level Cycling Teams 1984-2016

This is a work in progress. Any feedback or corrections A GENEALOGY OF TOP LEVEL CYCLING TEAMS 1984-2016 Contact me on twitter @dimspace or email [email protected] This graphic attempts to trace the lineage of top level cycling teams that have competed in a Grand Tour since 1985. Teams are grouped by country, and then linked Based on movement of sponsors or team management. Will also include non-gt teams where they are “related” to GT participants. Note: Due to the large amount of conflicting information their will be errors. If you can contribute in any way, please contact me. Notes: 1986 saw a Polish National, and Soviet National team in the Vuelta Espana, and 1985 a Soviet Team in the Vuelta Graphics by DIM @dimspace Web, Updates and Sources: Velorooms.com/index.php?page=cyclinggenealogy REV 2.1.7 1984 added. Fagor (Spain) Mercier (France) Samoanotta Campagnolo (Italy) 1963 1964 1965 1966 1967 1968 1969 1970 1971 1972 1973 1974 1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Le Groupement Formed in January 1995, the team folded before the Tour de France, Their spot being given to AKI. Mosoca Agrigel-La Creuse-Fenioux Agrigel only existed for one season riding the 1996 Tour de France Eurocar ITAS Gilles Mas and several of the riders including Jacky Durant went to Casino Chazal Raider Mosoca Ag2r-La Mondiale Eurocar Chazal-Vetta-MBK Petit Casino Casino-AG2R Ag2r Vincent Lavenu created the Chazal team. -

Annual Report 2019/20 Contents

ANNUAL REPORT 2019/20 CONTENTS 02 GROUP 20 EXTRACT FROM THE MANAGEMENT REPORT CONSOLIDATED FINANCIAL STATEMENTS 03 Fundamental information about the group 07 Economic report 21 Consolidated income statement 17 Risk and opportunity report 22 Consolidated statement of comprehensive income 19 Forecast 23 Consolidated statement of financial position 25 Consolidated statement of cash flows 27 Consolidated statement of changes in equity Annual Report _ 2019 / 2020 GROUP MANAGEMENT REPORT 2019/20 2 03 FUNDAMENTAL INFORMATION ABOUT THE GROUP 03 PHOENIX 05 Strategy and group management 06 Processes and organisation 07 ECONOMIC REPORT 07 Economic environment 07 Business development at a glance 09 Financial performance 13 Assets and liabilities 14 Financial position 15 Employees 17 RISK AND OPPORTUNITY REPORT 17 Risk management 17 Risks 18 Opportunities 18 Management Board’s overall assessment of the risks and opportunities 19 FORECAST 19 Future economic environment 19 Future development of PHOENIX 19 Management Board’s assessment of the group’s future position PHOENIX Pharmahandel GmbH & Co KG Annual Report _ 2019 / 2020 Group management report Fundamental information about the Group FUNDAMENTAL INFORMATION ABOUT THE GROUP ° Leading market position in European pharmaceutical wholesale ° Corporate strategy builds upon three pillars ° Digitalisation brings direct communication with end customers ° Projects and initiatives aim to achieve process optimisation and cost efficiency PHOENIX NET TURNOVER PER REGION in % Leading European healthcare provider PHOENIX, with its headquarters in Mannheim, Germany, is FY 2018 / 19 a leading European healthcare provider and is one of the largest family businesses in both Germany and Europe. Its core Eastern Europe 16.3 34.5 Germany business is pharmaceutical wholesale and pharmacy retail. -

The 2013 USC Marshall International Case Competition. Each Year We

Welcome to the 2013 USC Marshall International Case Competition. Each year we invite students from schools around the world to participate in this competitive event. Of the thirty teams attending this year, 19 teams represent schools from outside the United States. We embrace all of you and hope you enjoy your brief visit to Los Angeles and the University of Southern California. This year’s case presents issues which are current and very real to this business and their competitors in this and related industries. Thus, do not feel that the only relevant and available information is found within the four corners of this document. While some of the information provided here was only made available on the day we went to press, this industry is changing so quickly that there is no doubt in our minds that additional relevant information will appear in the days running up the time you receive this document. Thus, you should feel free to look for, and use, additional information which you may find online in completing your analysis of this case. References to some additional sources of information may be found in the Appendix. In addition to testing your skills in strategic analysis this year’s case seeks to address a topic which is very relevant to each of you as consumers. Your own experience with this industry and with the companies covered in the case will no doubt influence your perspective. Give voice to your own insights. We are certain that the panel of judges and company representatives are willing and eager to listen to your recommendations for today and the future. -

TCS Group Holding PLC Annual Report 2013

A different 1034 6784 0037 9125 1034 6784 0037 9125 type of bank 1034 6784 0037 9125 1034 6784 0037 9125 1034 6784 0037 9125 1034 6784 0037 9125 TCS Group Holding PLC Annual report 2013 1 1 11 Welcome This interactive pdf allows you to easily access the information TCS Group that you want, whether printing, searching for a specific item or going directly to another page, Holding plc section or website. Use the document controls located Annual Report at the bottom of each page to navigate through this report. Use 2013 the contents to jump straight to the section you require. Search the entire document by keyword Print a single page or whole sections Return back to the contents at the beginning of the document Next Page Previous Page Links Throughout this report there are links to pages, other sections and web addresses for additional information. They are recognisable by the underline simply click to go to the relevant page or web URL www.tcsbank.ru/eng 2013 highlights Proven track record of driving high growth and profitability. Growth Profitability • Full year net loan portfolio growth 43.6% yoy to USD2.3bn • Net income of USD181m, up 48.2% yoy • Almost 800,000 new active customers acquired in 2013 • RoAE of 44.8% Credit quality Key Events • Focus on credit quality to maintain a robust portfolio • Launch of Tinkoff Online Insurance • NPLs (90d+) at 7.0% at year-end • Introduction of sales of cash loans to existing credit card customers • Conservative provisioning policy with provision coverage of 1.6x NPLs at year-end • Launch of Tinkoff -

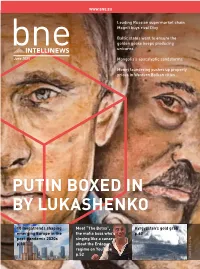

Putin Boxed in by Lukashenko

WWW.BNE.EU Leading Russian supermarket chain Magnit buys rival Dixy Baltic states want to ensure the golden goose keeps producing unicorns June 2021 Mongolia’s apocalyptic sandstorms Money laundering pushes up property prices in Western Balkan cities PUTIN BOXED IN BY LUKASHENKO 10 megatrends shaping Meet “The Botox”, Kyrgyzstan’s gold grab emerging Europe in the the mafia boss who’s p.62 post-pandemic 2020s singing like a canary p.38 about the Erdogan regime on YouTube p.52 ISSN 2059-2736 ISSN 2 I Contents bne June 2021 Senior editorial board Ben Aris editor-in-chief & publisher I Berlin 20 +49 17664016602 I [email protected] Clare Nuttall news editor I Glasgow +44 7766 513641 I [email protected] William Conroy editor Eurasia & SE Europe I Prague +420 774 849 172 I [email protected] ——— Subscriptions Stephen Vanson 5 18 London I +44 753 529 6546 [email protected] ——— COMPANIES & MARKETS Advertising 4 Poland says it will not 17 Russian supermarket business Elena Arbuzova comply with EU court’s order rapidly consolidating as Lenta buys business development director I Moscow +7 9160015510 I [email protected] to stop Turow mine Billa Russia to become second- ——— largest chain in Moscow 5 Hungary turns down EU's Design €9.4bn recovery fund 18 The average income of couriers is Olga Gusarova credit line up to twice the average regional art director I London salary +44 7738783240 I [email protected] 6 Centerra files arbitration suit as Kyrgyzstan moves to seize 19 Baltic states want to ensure the Please direct comments, letters, press releases Kumtor gold mine golden goose keeps producing and other editorial enquires to [email protected] unicorns 7 Russian ice cream All rights reserved. -

Leveraging Our Global Capabilities

Subsea 7 S.A. Annual Report and Financial Statements 2010 Leveraging our global capabilities Subsea 7 S.A. (Formerly Acergy S.A.) Annual Report and Financial Statements 2010 Leveraging our global capabilities Subsea 7 S.A. is a global leader in seabed-to-surface engineering, construction and services. The Combination of Acergy S.A. and Subsea 7 Inc. in January 2011 created a global leader in seabed-to-surface engineering, construction and services able to offer clients access to a high end, diversified fleet, comprising 42 vessels supported by extensive fabrication and onshore facilities able to deliver the full spectrum of subsea engineering, construction and services. Subsea 7 S.A. is well positioned to take advantage of future growth opportunities in the global seabed-to-surface market. We are leveraging our global capabilities through our greater depth of project management, engineering and technical expertise along with our high-end diversified fleet to secure and deliver complex offshore projects on behalf of our clients, in safe and sustainable ways. For all the latest up-to-date information visit www.subsea7.com Subsea 7 S.A. Registered office: 412F, route d’Esch L-2086 Luxembourg Registered number: B 43 172 Creating a new force in seabed-to-surface May 2010 Awarded $120 million Dec 2009 Dec 2009 contract, offshore Acquires Borealis Awarded three-year Nigeria Acergy acquired Borealis, a DSV contract Awarded Conventional state-of-the-art deepwater Awarded three-year project for the removal construction and pipelay contract for the provision of existing risers, vessel. Borealis is ideally of Dive Support Vessel the installation of new suited to meeting the services to the DSVi pipelines and associated exacting requirements of Collective of companies risers, together with ultra-deep and deepwater in the North Sea. -

(As Defined Below) Located Outside of the United States

IMPORTANT NOTICE THIS OFFERING IS AVAILABLE ONLY TO INVESTORS WHO ARE NON-U.S. PERSONS (AS DEFINED BELOW) LOCATED OUTSIDE OF THE UNITED STATES. IMPORTANT: You must read the following before continuing. The following applies to the Preliminary Prospectus following this page and you are therefore advised to read this page carefully before reading, accessing or making any other use of the Preliminary Prospectus. In accessing the Preliminary Prospectus, you agree to be bound by the following terms and conditions, including any modifications to them any time you receive any information from the Issuer (as defined in the Preliminary Prospectus), Goldman Sachs International or J.P. Morgan Securities plc as a result of such access. NOTHING IN THIS ELECTRONIC TRANSMISSION CONSTITUTES AN OFFER OF SECURITIES FOR SALE IN THE UNITED STATES OR ANY OTHER JURISDICTION WHERE IT IS UNLAWFUL TO DO SO. THE NOTES HAVE NOT BEEN, AND WILL NOT BE, REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED (THE "SECURITIES ACT"), OR THE SECURITIES LAWS OF ANY STATE OF THE U.S. OR OTHER JURISDICTION AND THE NOTES MAY NOT BE OFFERED OR SOLD, DIRECTLY OR INDIRECTLY, WITHIN THE U.S. OR TO, OR FOR THE ACCOUNT OR BENEFIT OF, U.S. PERSONS (AS DEFINED IN REGULATION S UNDER THE SECURITIES ACT), EXCEPT PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND APPLICABLE STATE OR LOCAL SECURITIES LAWS. THE ATTACHED PRELIMINARY PROSPECTUS MAY NOT BE FORWARDED OR DISTRIBUTED TO ANY OTHER PERSON AND MAY NOT BE REPRODUCED IN ANY MANNER WHATSOEVER, AND, IN PARTICULAR, MAY NOT BE FORWARDED TO ANY U.S. -

Market News Legislation Company News SECURITIES MARKET

SSEECCUURRIIITTIIIEESS MMAARRKKEETT NNEEWWSSLLEETTTTEERR weekly Presented by: VTB Bank, Custody December 17, 2020 Issue No. 2020/49 Market News St. Petersburg bourse says can start trading derivatives in 2021 On December 14, 2020 President of parent association NP RTS Roman Goryunov said that the Saint- Petersburg Exchange (SPB Exchange) planned to launch a derivative market in 2021. He stated that there was natural demand for foreign securities derivatives, but how and in which form it would be done, was a bit early to say, because it would depend on the readiness of the participants. He mentioned that this is going to be a priority for the next year. Legislation Government approves ratification of Luxembourg tax deal On December 14, 2020 it was reported that the Russian government approved ratification of an agreement on double taxation avoidance with Luxembourg. In March, Russian President Vladimir Putin suggested imposing a 15% tax on dividend yields withdrawn to the accounts in foreign jurisdictions, which needs adjustments to the agreements on avoidance of double taxation with other countries. Russia will cancel such agreements unilaterally if consensus is not reached. The Finance Ministry sent notifications to Cyprus first, and then to Luxembourg, Malta, and the Netherlands. Amendments to the accord with Cyprus have already been made, and the government coordinated them with Malta and Luxembourg. But negotiations with the Netherlands are difficult, Finance Minister Anton Siluanov said earlier. The Finance Ministry also launched a procedure to denounce the double taxation accord with the Netherlands. Company News Altus now says to buy only 25% in Detsky Mir On December 11, 2020 it was reported that investment company Altus Capital lowered the number of shares it was ready to buy in children goods retailer Detsky Mir to 25% from 29.9% due to the new procedure of accepting bids and settlements. -

TCS Group Holding PLC: Total Conversion of Class B Shares and Reclassification and Redesignation of All Issued Shares As 'Ordinary Shares'

TCS Group Holding PLC: Total conversion of Class B shares and reclassification and redesignation of all issued shares as 'ordinary shares' Released : 07 January 2021 07:22 TCS Group Holding PLC (TCS) TCS Group Holding PLC: Total conversion of Class B shares and reclassification and redesignation of all issued shares as 'ordinary shares' 07-Jan-2021 / 10:22 MSK Dissemination of a Regulatory Announcement that contains inside information according to REGULATION (EU) No 596/2014 (MAR), transmitted by EQS Group. The issuer is solely responsible for the content of this announcement. THIS ANNOUNCEMENT CONTAINS INSIDE INFORMATION FOR THE PURPOSES OF ARTICLE 7 OF REGULATION (EU) NO 596/2014 FOR IMMEDIATE RELEASE TCS Group Holding PLC: Total conversion of Class B shares and reclassification and redesignation of all issued shares as 'ordinary shares' Limassol, Cyprus - 7 January 2021. TCS Group Holding PLC (TCS LI) (the "Group"), Russia's leading provider of online retail financial services, today announces that it has received an instruction to implement the conversion of all outstanding 69,914,043 Class B shares in the Group held by The Rigi Trust and the Bernina Trust, British Virgin Islands trusts connected with Oleg Tinkov. It is anticipated that these Class B shares shall be converted to Class A shares with effect from 7 January 2021. The converted Class B shares rank pari passu in all respects and for all purposes with each pre existing Class A share. Following the conversion, each share shall carry a single vote, and the total number of votes capable of being exercised shall be equal to the total number of issued shares (currently 199,305,492 shares following the Class B share conversion). -

Innovation in Non Destructive Testing

Innovation in Non Destructive Testing Entrepreneurship Casper Wassink Innovation in Non Destructive Testing Proefschrift Ter verkrijging van de graad van doctor aan de Technische Universiteit Delft, op gezag van de Rector Magnificus prof.ir. K.C.A.M. Luyben, voorzitter van het College van Promoties, in het openbaar te verdedigen op donderdag 12 januari 2012 om 12:30 uur door Casper Harm Philip WASSINK Natuurkundig Ingenieur geboren te Aalsmeer Dit proefschrift is goedgekeurd door de promotor: Prof. dr. ir. A.J. Berkhout Copromotor: Dr. J.R. Ortt Samenstelling promotiecommissie: Rector Magnificus, Technische Universiteit Delft, Voorzitter Prof. dr. ir. A.J. Berkhout, Technische Universiteit Delft, Promotor Dr. J.R. Ortt, Technische Universiteit Delft, Copromotor Prof. dr. A.H. Kleinknecht, Technische Universiteit Delft Prof. dr. ir. J.G. Slootweg, Technische Universiteit Eindhoven Prof. dr. B.J.M. Ale, Technische Universiteit Delft Prof. dr. U. Ewert, Bundesanstalt für Materialforschung und -prüfung Dr. ir. M. Lorenz, Shell Global Solutions Prof. dr. ir. P.M. Herder, Technische Universiteit Delft, reservelid ISBN 978-90-8570-795-0 Copyright © 2011 Casper Wassink, Rotterdam, The Netherlands Printed by: Wöhrmann Print Service All rights reserved, No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form, or by any means, electronic, mechanical, photocopying, recording, or otherwise, without prior consent of the author. Samenvatting Innovatie is vandaag de dag geen activiteit meer die kan worden overgelaten aan een aparte afdeling of een kennisinstituut. Het is een kerncompetentie van succesvolle ondernemingen. Echter, in veel gevestigde ondernemingen is de snelheid van innovatie laag. De Niet Destructie Onderzoek sector is een voorbeeld van een sector waar de snelheid van innovatie zeer laag is. -

Acergy S.A. Announces Second Quarter Results

Acergy S.A. Announces Second Quarter Results London, England – July 14, 2010 – Acergy S.A. (NASDAQ-GS: ACGY; Oslo Stock Exchange: ACY), announced today results for the second quarter which ended on May 31, 2010. The Group’s accounts are prepared in accordance with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB) and as adopted by the European Union and were approved by the Board on July 14, 2010. Highlights - Revenue from continuing operations was $581 million (Q2 2009: $526 million) - Adjusted EBITDA(a) from continuing operations was $121 million (Q2 2009: $113 million) corresponding to an Adjusted EBITDA margin of 20.9% (Q2 2009: 21.5%) - Income from continuing operations was $63 million (Q2 2009: $76 million) - Strong cash and cash equivalents position of $631 million (February 28, 2010: $667 million) - Awarded $120 million Conventional contract, offshore Nigeria - As part of our ongoing fleet development programme, Acergy acquired two vessels post quarter end; the Polar Queen and the Antares, a shallow water barge for the West African Conventional market - Post quarter end, on June 21, 2010 the Boards of Directors of Acergy S.A. and Subsea 7 Inc. announced that they had agreed to combine the two companies Jean Cahuzac, Chief Executive Officer, said: “We have delivered a solid quarterly performance driven by excellent project execution, additional variation orders on ongoing projects and strong Conventional activity. We remain on track to deliver our 2010 expectations. In line with our strategy to develop the fleet, we acquired the Antares and Polar Queen, reinforcing our commitment to capture opportunities and invest in the business.