Draft Audit Report on the Accounts of Tehsil Municipal Administration Kohistan Audit Year 2013-14

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Floods in Pakistan Pakistan Health Cluster Bulletin No 13 21 August 2010

Floods in Pakistan Pakistan Health Cluster Bulletin No 13 21 August 2010 Vaccination campaign at an IDP camp at Government Girls High School in Taluka Sehwan, Jamshoro district, Sindh province. • Number of reporting disease cases is increasing. Until 18 August, 204 040 of acute diarrhoea, 263 356 cases of skin diseases and 204 647 of acute respiratory have been reported in flood-affected provinces. More than 1.5 million patient consultations have been conducted in flood-affected provinces since 29 July. • Daily number of reported acute diarrhoea cases, monitored since 31 July is rising, particularly in Charsadda, Nowshera and Peshawar. • From 16-18 August, 6 new suspected acute diarrhoea alerts reported from Khyber Pakhtunkhwa (KPK). • WHO establishing diarrhoeal treatment centres in flood-affected districts with government and partner support. • Health Cluster to have access to UNHAS flights for delivery of medical items. • Health Cluster coordination active in 5 hubs - Islamabad, Peshawar, Multan, Sukkur, Quetta. • WHO delivers large shipment of medicines to Sukkur coordination hub on 20 August. • In first 3 days of emergency vaccination campaign launched in Peshawar and Charsadda on 16 August, 104 640 children under 5 years were vaccinated against polio. All aged over 6 months (92 269 children) also vaccinated against measles and received vitamin A capsules. • As of 21 August, 39% of the US$56.2 million requested to support the health response has been funded. • According to the National Disaster Management Authority (NDMA), more than 20 million people have been affected by the floods. Almost 1500 people have been reported killed and more than 2000 injured, while around 1 million are left homeless. -

Languages of Kohistan. Sociolinguistic Survey of Northern

SOCIOLINGUISTIC SURVEY OF NORTHERN PAKISTAN VOLUME 1 LANGUAGES OF KOHISTAN Sociolinguistic Survey of Northern Pakistan Volume 1 Languages of Kohistan Volume 2 Languages of Northern Areas Volume 3 Hindko and Gujari Volume 4 Pashto, Waneci, Ormuri Volume 5 Languages of Chitral Series Editor Clare F. O’Leary, Ph.D. Sociolinguistic Survey of Northern Pakistan Volume 1 Languages of Kohistan Calvin R. Rensch Sandra J. Decker Daniel G. Hallberg National Institute of Summer Institute Pakistani Studies of Quaid-i-Azam University Linguistics Copyright © 1992 NIPS and SIL Published by National Institute of Pakistan Studies, Quaid-i-Azam University, Islamabad, Pakistan and Summer Institute of Linguistics, West Eurasia Office Horsleys Green, High Wycombe, BUCKS HP14 3XL United Kingdom First published 1992 Reprinted 2002 ISBN 969-8023-11-9 Price, this volume: Rs.300/- Price, 5-volume set: Rs.1500/- To obtain copies of these volumes within Pakistan, contact: National Institute of Pakistan Studies Quaid-i-Azam University, Islamabad, Pakistan Phone: 92-51-2230791 Fax: 92-51-2230960 To obtain copies of these volumes outside of Pakistan, contact: International Academic Bookstore 7500 West Camp Wisdom Road Dallas, TX 75236, USA Phone: 1-972-708-7404 Fax: 1-972-708-7433 Internet: http://www.sil.org Email: [email protected] REFORMATTING FOR REPRINT BY R. CANDLIN. CONTENTS Preface............................................................................................................viii Maps................................................................................................................. -

Pakistan Water and Power Development Authority

PAKISTAN WATER AND POWER DEVELOPMENT AUTHORITY Public Disclosure Authorized DASU HYDROPOWER PROJECT Public Disclosure Authorized Public Disclosure Authorized SOCIAL AND RESETTLEMENT MANAGEMENT PLAN VOLUME 7: PUBLIC HEALTH ACTION PLAN Public Disclosure Authorized General Manager (Hydro) Planning WAPDA, Sunny view, Lahore, Pakistan Final Version 08 March 2014 Social and Resettlement Management Plan Vol. 7 Public Health Action Plan i Dasu Hydropower Project Social and Resettlement Management Plan Vol. 7 Public Health Action Plan SOCIAL AND RESETTLEMENT MANAGEMENT PLAN INDEX OF VOLUMES Volume 1 Executive Summary Volume 2 Socioeconomic Baseline and Impact Assessments Volume 3 Public Consultation and Participation Plan Volume 4 Resettlement Framework Volume 5 Resettlement Action Plan Volume 6 Gender Action Plan Volume 7 Public Health Action Plan Volume 8 Management Plan for Construction-related Impacts Volume 9 Grievances Redress Plan Volume 10 Communications Plan Volume 11 Downstream Fishing Communities: Baseline and Impact Assessments Volume 12 Area Development and Community Support Programs Volume 13 Costs and Budgetary Plan Volume 14 Safeguards Implementation and Monitoring Plan ii Dasu Hydropower Project Social and Resettlement Management Plan Vol. 7 Public Health Action Plan ABBREVIATIONS AFB Acid Fast Bacilli AIDS Acquired Immune Deficiency Syndrome ANC Antenatal Care ARI Acute Respiratory Tract Infection asl Above Sea Level AWD Acute Watery Diarrhoea BHU Basic Health Unit COI Corridor of Impact CPR Contraceptive Prevalence Rate CSC -

Audit Report on the Accounts of Earthquake Reconstruction & Rehabilitation Authority Audit Year 2015-16

AUDIT REPORT ON THE ACCOUNTS OF EARTHQUAKE RECONSTRUCTION & REHABILITATION AUTHORITY AUDIT YEAR 2015-16 AUDITOR GENERAL OF PAKISTAN TABLE OF CONTENTS ABBREVIATIONS & ACRONYMS ........................................................................... i PREFACE .............................................................................................................. vi EXECUTIVE SUMMARY ........................................................................................ vii SUMMARY TABLES & CHARTS ..............................................................................1 I Audit Work Statistics ..............................................................................1 II Audit observations regarding Financial Management ...........1 III Outcome Statistics ............................................................................2 IV Table of Irregularities pointed out ..............................................3 V Cost-Benefit ........................................................................................3 CHAPTER-1 Public Financial Management Issues (Earthquake Reconstruction & Rehabilitation Authority 1.1 Audit Paras .............................................................................................4 CHAPTER-2 Earthquake Reconstruction & Rehabilitation Authority (ERRA) 2.1 Introduction of Authority .....................................................................18 2.2 Comments on Budget & Accounts (Variance Analysis) .....................18 2.3 Brief comments on the status of compliance -

Pak-Swiss INRMP (2010) Study on Timber Harvesting Ban in NWFP

2 Study on timber harvesting ban in NWFP, Pakistan Disclaimer This study was conducted in an independent manner. The views expressed in this study do not present the official position of the NWFP Forest Department and the funding agency (SDC) but those of the Study Team ISBN: 969-9082-02-x Parts of this publication may be copied with proper citation in favour of the Authors and the publishing organization Integrated Natural Resource Management Project 3 This publication is based on 15 months continuous engagement of the team in collecting data, analyses and documentation by the study team. Initiated by: Pak-Swiss Integrated Natural Resource Management Project (INRMP) on request of the NWFP Forest Department in the first yearly planning workshop of the project, to conduct an independent study The Study Team and Authors: Dr. Knut M. Fischer (Team Leader) Muhammad Hanif Khan Alamgir Khan Gandapur Abdul Latif Rao Raja Muhammad Zarif Hamid Marwat Publication editing: Arjumand Nizami Syed Nadeem Bukhari Fatima Daud Kamal Layout: Salman Beenish Printing: PanGraphics (Pvt) Ltd., Islamabad Available from: Swiss Agency for Development and Cooperation (SDC) Intercooperation Delegation Office Pakistan INRMP / NWFP Forest Department, Planning, Monitoring and Evaluation Circle, Peshawar Cover photographs: Aamir Rana Amina Ijaz Arjumand Nizami Irshad Ali Mian Roshan Ara Tahir Saleem Technical cooperation: Intercooperation Head Office Berne, Switzerland and Pakistan Pak-Swiss Integrated Natural Resource Management Project (INRMP) GIS lab of Forest Planning and Monitoring Circle, NWFP Forest Department Published by Intercooperation Pakistan through Pak-Swiss Integrated Natural Resource Management Project (INRMP). INRMP is funded by Swiss Agency for Development and Cooperation (SDC) 4 Study on timber harvesting ban in NWFP, Pakistan About Intercooperation Intercooperation (IC) in Pakistan and worldwide has been actively engaged in forestry sector right from its inception in 1982. -

765Kv Dasu Transmission Line Project Resettlement Action Plan (Rap)

GOVERNMENT OF PAKISTAN MINISTRY OF ENERGY (POWER DIVISION) NATIONAL TRANSMISSION & DISPATCH COMPANY (NTDC) 765KV DASU TRANSMISSION LINE PROJECT RESETTLEMENT ACTION PLAN (RAP) November 2019 National Transmission & Despatch Company Ministry of Energy (Power Division) Government of Pakistan National Transmission & Despatch Company TABLE OF CONTENTS 1. INTRODUCTION ....................................................................................................................................... 1 1.1 BACKGROUND ........................................................................................................................................... 1 1.2 PROJECT DESCRIPTION AND COMPONENTS ...................................................................................................... 1 1.2.1 Project Description and Components ................................................................................................ 1 1.2.2 Access Tracks and Roads ................................................................................................................... 3 1.2.3 Construction Methodology ............................................................................................................... 4 1.2.4 Project Cost and Construction Time .................................................................................................. 6 1.3 THE PROJECT AREA .................................................................................................................................... 6 1.4 PROJECT BENEFITS AND IMPACTS -

PAK102 Revision 2 for Approval 16September 2010

SECRETARIAT 150 route de Ferney, P.O. Box 2100, 1211 Geneva 2, Switzerland TEL: +41 22 791 6033 FAX: +41 22 791 6506 www .actalliance.org Appeal Pakistan Pakistan Floods Emergency (PAK102) – Rev. 2 Appeal Target: US$ 12,441,347 Balance Requested: US$ 6,478,821 Geneva, 17 September 2010 Dear colleagues, Since 21 July 2010, heavy monsoon rains have led to the worst flooding in Pakistan’s history. Please see the ACT website ( www.actalliance.org/resources/alertsandsitreps ) for the latest ACT Situation Reports from Pakistan on this fast changing emergency. The members of the ACT Pakistan Forum, Church World Service- Pakistan/Afghanistan (CWS-P/A), Norwegian Church Aid (NCA), and Diakonie Katastrophenhilfe (DKH) continue to distribute urgent relief assistance to the flood-affected communities with the financial, material aid and personnel support of many international ACT members, their national constituencies and institutional donors, as well as other supporters from around the world. This ACT appeal was first issued on 4 August and then replaced by a revised version issued on 11 August to include the proposed responses of DKH and NCA, as well as a scaled-up version of the CWS-P/A programme. This second revision of the appeal significantly scales-up the entire proposed programme from a previous funding target of US $4,101,731 to US$ 12,441,347. CWS P/A is increasing the number of operational areas to include Sukkur and Thatta Districts in Sindh Province and Muzaffargarh District in Punjab Province. CWS P/A is now working with an additional partner – the Church of Pakistan (CoP) Diocese of Raiwind. -

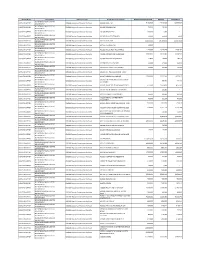

District Name Department DDO Description Detail Object

District Name Department DDO Description Detail Object Description Budget Estimates 2017-18 Releases Expenditure KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A01101 BASIC PAY 9,184,500 12,316,580 10,833,687 DEPARTMENT KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A01102 PERSONAL PAY 50,000 50,000 - DEPARTMENT KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A01103 SPECIAL PAY 100,000 5,000 - DEPARTMENT KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A01105 QUALIFICATION PAY 50,000 22,250 2,250 DEPARTMENT KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A01151 BASIC PAY 15,629,500 16,706,650 15,067,318 DEPARTMENT KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A01152 PERSONAL PAY 15,000 - - DEPARTMENT KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A01202 HOUSE RENT ALLOWANCE 1,475,000 1,618,520 1,269,132 DEPARTMENT KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A01203 CONVEYANCE ALLOWANCE 3,382,000 3,813,790 3,058,502 DEPARTMENT KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A01207 WASHING ALLOWANCE 19,800 70,800 18,450 DEPARTMENT KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A01208 DRESS ALLOWANCE 12,000 19,600 12,150 DEPARTMENT KD21C09 REVENUE & ESTATE KOHISTAN UPPER KD6108 Deputy Commisioner Kohistan A0120D INTEGRATED ALLOWANCE 92,000 92,000 70,200 DEPARTMENT -

Ehsaas Emergency Cash Payments

Consolidated List of Campsites and Bank Branches for Ehsaas Emergency Cash Payments Campsites Ehsaas Emergency Cash List of campsites for biometrically enabled payments in all 4 provinces including GB, AJK and Islamabad AZAD JAMMU & KASHMIR SR# District Name Tehsil Campsite 1 Bagh Bagh Boys High School Bagh 2 Bagh Bagh Boys High School Bagh 3 Bagh Bagh Boys inter college Rera Dhulli Bagh 4 Bagh Harighal BISP Tehsil Office Harigal 5 Bagh Dhirkot Boys Degree College Dhirkot 6 Bagh Dhirkot Boys Degree College Dhirkot 7 Hattain Hattian Girls Degree Collage Hattain 8 Hattain Hattian Boys High School Chakothi 9 Hattain Chakar Boys Middle School Chakar 10 Hattain Leepa Girls Degree Collage Leepa (Nakot) 11 Haveli Kahuta Boys Degree Collage Kahutta 12 Haveli Kahuta Boys Degree Collage Kahutta 13 Haveli Khurshidabad Boys Inter Collage Khurshidabad 14 Kotli Kotli Govt. Boys Post Graduate College Kotli 15 Kotli Kotli Inter Science College Gulhar 16 Kotli Kotli Govt. Girls High School No. 02 Kotli 17 Kotli Kotli Boys Pilot High School Kotli 18 Kotli Kotli Govt. Boys Middle School Tatta Pani 19 Kotli Sehnsa Govt. Girls High School Sehnsa 20 Kotli Sehnsa Govt. Boys High School Sehnsa 21 Kotli Fatehpur Thakyala Govt. Boys Degree College Fatehpur Thakyala 22 Kotli Fatehpur Thakyala Local Govt. Office 23 Kotli Charhoi Govt. Boys High School Charhoi 24 Kotli Charhoi Govt. Boys Middle School Gulpur 25 Kotli Charhoi Govt. Boys Higher Secondary School Rajdhani 26 Kotli Charhoi Govt. Boys High School Naar 27 Kotli Khuiratta Govt. Boys High School Khuiratta 28 Kotli Khuiratta Govt. Girls High School Khuiratta 29 Bhimber Bhimber Govt. -

Current Budget Estimates 2016-17

District Name Department DDO Description Detail Object Description Budget Estimates 2016-17 KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A01101 BASIC PAY OF OFFICER 10,246,500 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A01102 PERSONAL PAY 50,000 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A01103 SPECIAL PAY 100,000 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A01105 QUALIFICATION PAY 50,000 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A01151 BASIC PAY OTHER STAFF 15,743,500 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A01152 PERSONAL PAY 15,000 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A01202 HOUSE RENT ALLOWANCE 4,623,000 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A01203 CONVEYANCE ALLOWANCE 5,520,000 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A01207 WASHING ALLOWANCE 34,500 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A01208 DRESS ALLOWANCE 23,000 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A0120D INTEGRATED ALLOWANCE 287,500 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN UPPERKD21C09 REVENUE & ESTATE DEPARTMENT A0120X ADHOC ALLOWANCE - 2010 8,337,500 KOHISTAN KD6108 DEPUTY COMMISSIONER KOHISTAN -

Project Compilation Report on Two Weeks Campaig to Celebrate 16 Days of Acti

PROJECT COMPLETION REPORT DISABILITY UNIT DISTRICT KOHISTAN SALIK DEVELOPMENT FOUNDATION (SDF) KOHISTAN (Khyber Pukhtoonkhwa) 2 Table of Contents Topic Page Number 1. Table of Contents ………………………………………………….………………… 2-3 2. List of Acronyms ………………………………………………………….………….. 4 3. Project Identification Information............................................. 5 4. Training Objectives ……………………………………………………………. 6 5. Area Background ……………………………………………………………….. 6 6. Map of District Kohistan …………………………………………………….. 7 7. Union Council Wise Population of Kohistan ………………………….. 7 8. Rationale of the Project …………………………………………………… 8 9. Pre-Training Activities ………………………………………………………. 8 10. Dialogue between the SDF and Master Trainers (Tailoring) ….. 8 11. Signing of MOU ……………………………………………………………….. 9 12. Identification of Trainees …………………………………………………. 9 13. Training formally takes start (May 24, 2011) …………………….. 9 14. Tailoring Course ……………………………………………………………… 10 ______________________________________________________________________________ Salik Development Foundation Disability Program Kohistan 3 15. Opening Ceremony (May 24, 2011) ………………………………….. 11 16. Certificates Awarding Ceremony (June 22, 2011) ………………….. 13 17. Requisition for provision of Training Kits (Sewing Machine)……… 18 18. Distribution ceremony of Tailoring Kits ………………………………..…19 19. Graph of distribution of Tailoring Kits and Assistive Devices ……….20 20. Picture Gallary ………………………………………………………………………. 24 21. Community awareness regarding PWD……………………………………… 25 ______________________________________________________________________________ -

PAK102 Appeal Revision1 App

SECRETARIAT 150 route de Ferney, P.O. Box 2100, 1211 Geneva 2, Switzerland TEL: +41 22 791 6033 FAX: +41 22 791 6506 www .actalliance.org Appeal Pakistan Emergency Assistance to Flood-Affected in Pakistan (PAK102) - Revision 1 Appeal Target: US$ 4,101,731 912 Balance Requested: US$ 2,652,504 Geneva, 11 August 2010 Dear colleagues, Since July 21 st 2010, heavy monsoon rains have led to the worst flooding in 80 years in Pakistan. Destruction is wide-spread across 40% of the country. As the rains continue, the waters are moving downstream like a “rolling earthquake” affecting Punjab and Sindh provinces further south. Transport and communications have been widely disrupted. Many areas remain inaccessible and thousands have yet to receive assistance. Latest estimates are that between 12 to 14.5 million are affected with the figures rising. The death toll has reached well over 1,600 and around 1.5 million people are made homeless. There are concerns about further deaths due to water-borne diseases as communities struggle to survive. The UN’s Emergency Response Coordinator, John Holmes, has observed that the overall humanitarian donor response to date is not commensurate to the massive level of need in this crisis. The members of the ACT Pakistan Forum, Church World Service- Pakistan/Afghanistan (CWS-P/A), Norwegian Church Aid (NCA), and Diakonie Katastrophenhilfe (DKH) are distributing urgent relief assistance to the flood-affected communities. This revision of the appeal first issued on August 4 th includes the proposed responses of DKH and NCA, as well as a revised, scaled-up version of the CWS- P/A response.